Insights

Honest Insights On Upperhouse @ Orchard Boulevard

Upperhouse grades C (5.4) on the New Project Scorecard — a doorstep-MRT Orchard Boulevard address on top of the weakest growth engine we have reviewed. UOL and SingLand's 301-unit tower is 81% sold a year after its S$3,350 psf launch; what's left asks a premium over the project's own record.

By TRIBE Editorial · 16 July 2026 · 13 min read

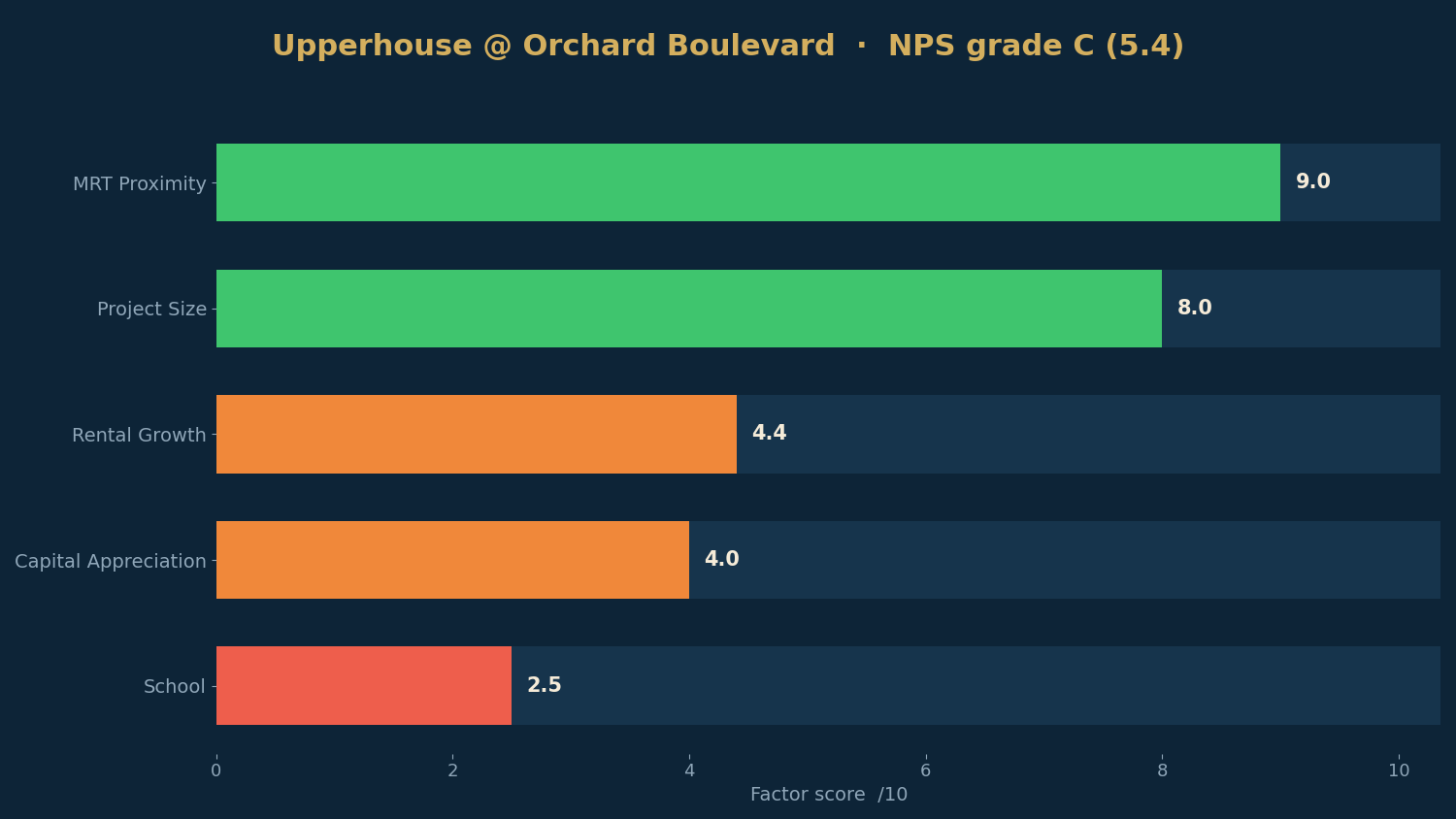

Upperhouse @ Orchard Boulevard is a 301-unit, 99-year single tower on the only Orchard-area GLS site sold since 2018 — 35 storeys by UOL Group and Singapore Land, directly above the doorstep of Orchard Boulevard MRT on the Thomson-East Coast Line, on land bought for S$428.28 million (S$1,617 psf ppr) in February 2024. It grades a C (5.4) on our New Project Scorecard (NPS), and the two halves of that sentence are the whole story: one of the best pure-location cards in the CCR, sitting on the weakest growth engine we have reviewed — a 1km prime resale ring that appreciated ~1.8% a year for a decade. The market bought the location anyway: 162 of 301 units (53.8%) on the 19 July 2025 launch day at an average of S$3,350 psf, the strongest Core Central Region debut since Watten House in late 2023, climbing to 246 sold (81%) by mid-July 2026. This is a look at what the C actually flags, what the launch proved about CCR demand, and what the remaining 55 units ask. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted for the project's own size, transport and schools, not a forecast.

The scorecard: what the C actually says

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| MRT Proximity | 9.0 | Orchard Boulevard MRT (TE13) at the doorstep — a 0.00km OneMap walk |

| Project Size | 8.0 | 301 units — mid-sized, healthy liquidity |

| Rental Growth | 4.4 | District 10 rents grew ~5.2%/yr — moderate, a tier below the 7% districts |

| Capital Appreciation | 4.0 | 1km resale grew ~1.8%/yr over the decade; lifted → 2.19%/yr — under the 3% bar |

| School | 2.5 | No primary school within 1km on the scorecard's OneMap measure |

Read this card from the bottom, because the C lives there. Capital appreciation scores 4.0 on one of the richest datasets on our board — 106 resale projects inside the kilometre — so this is not a thin-data artefact: prime-district resale around Orchard Boulevard appreciated about 1.8% a year over the past decade on a same-property basis, and even with the project's quality tilt the model projects 2.19% a year, under the 3% bar. The comp set makes it concrete: Cuscaden Reserve, the 99-year 2023-completed project 220m away, has negative past appreciation (−0.02%/yr) on the tool's read; 19 Nassim, −0.41%/yr. This is the same pattern we flagged at TMW Maxwell (1.7%/yr) and One Marina Gardens: the CCR's last decade simply did not compound. School scores 2.5: on the scorecard's OneMap door-to-door measure no primary school sits within 1km — launch coverage placed River Valley Primary inside the ring, so treat the boundary as contested and check your own unit's door-to-door distance on OneMap before counting on priority. Rental growth at 4.4 (D10, ~5.2%/yr) and a modelled gross yield of 2.46% — the thinnest we have reviewed, under even The Sen's 2.63% — complete the engine-room picture.

The top of the card is what 246 buyers actually bought. MRT 9.0: the tower stands at the station door — a 0.00km OneMap walk to TE13, one stop from Orchard, ION at ~500m. Size 8.0 at 301 units, split into a 270-unit Signature Collection and 31 Bespoke four-bedroom suites with private lifts and dedicated parking. It is a genuinely rare address: the only GLS land released in the Orchard/Tanglin belt in six-plus years, across the road from Park Nova's S$6,150 psf freehold new-sales.

The launch: CCR demand, measured

The February 2024 tender drew four bidders; UOL–SingLand's S$1,617 psf ppr edged Allgreen's S$1,578 by 2.5%. Eighteen months later, launch day — 19 July 2025 — moved 162 units (53.8%) at an average of S$3,350 psf, which PropNex called the strongest CCR project debut since Watten House's 57% in November 2023. The shape of the demand was telling: the 764 sqft 2BR+Study sold 60 of 67 on the day (S$2.338–2.72 million), the 1,012 sqft 3BR Premium sold 33 of 34 (S$3.269–3.781 million), while the S$7 million-plus Bespoke suites moved about 30%. Buyers were, per UOL, almost all Singaporeans and PRs — with foreigner ABSD at 60%, prime launches now clear on local demand or not at all. The macro pitch behind the launch was the compression trade: the CCR-versus-RCR new-home price gap had narrowed from 56.5% in 2018 to under 2% by the first half of 2025, and S$3,350 psf beside Orchard Boulevard MRT was priced at 99-year resale levels across the road (Cuscaden Reserve was transacting above S$3,100) rather than at freehold-new levels.

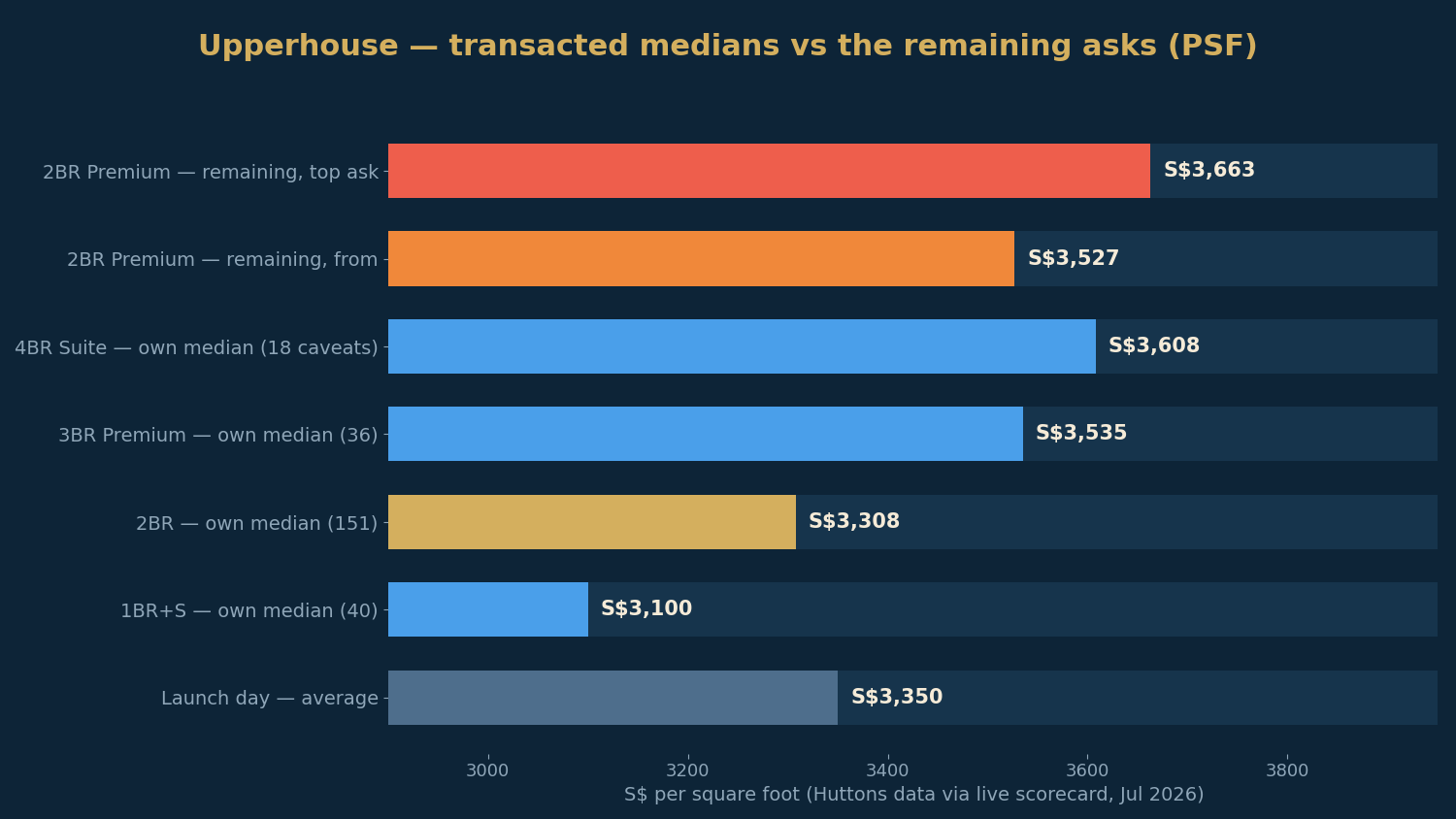

A year on, the chart reads 246 of 301 sold (81%): the 2BR+Study and 3BR Premium are fully sold, and the sell-down has been a steady grind rather than a second wave.

What the project has transacted at, by bedroom (Huttons data via the live scorecard, July 2025–July 2026):

| Type | Typical size | Median PSF | Caveats |

|---|---|---|---|

| 1BR+Study | 474 sqft | S$3,100 | 40 |

| 2BR Premium / +Study | 700–764 sqft | S$3,308 | 151 |

| 3BR Premium | 1,012 sqft | S$3,535 | 36 |

| 4BR Suite | 2,056 sqft | S$3,608 | 18 |

What's left: 55 units, asking above the record

Per the agent price guides of 6 July 2026, the remaining stock is 26 of the 474 sqft 1BR+Study (S$1.571–1.715 million, S$3,314–3,618 psf), 19 of the 700 sqft 2BR Premium (S$2.469–2.564 million, S$3,527–3,663 psf), and around 11 of the 2,056 sqft Bespoke 4BR Suites (S$7.131–8.056 million, S$3,468–3,918 psf) — the 16 July balance chart confirms 55 units across exactly these three types.

Against the project's own record, this tail — unlike Pinery's or The Continuum's — asks a premium over the transacted medians almost everywhere. The 1BR+Study enters 6.9% above its own S$3,100 median (40 caveats) and stretches to +16.7% at the top. The 2BR Premium enters 6.6% above its S$3,308 band median and reaches +10.7%. Only the Bespoke suite from-price sits below its band — S$3,468 against a S$3,608 median, though that median rests on just 18 caveats, so read it loosely. The pattern is familiar late-cycle developer pricing: the accessible formats that cleared early are repriced upward on scarcity, and the last discount lives in the biggest cheque.

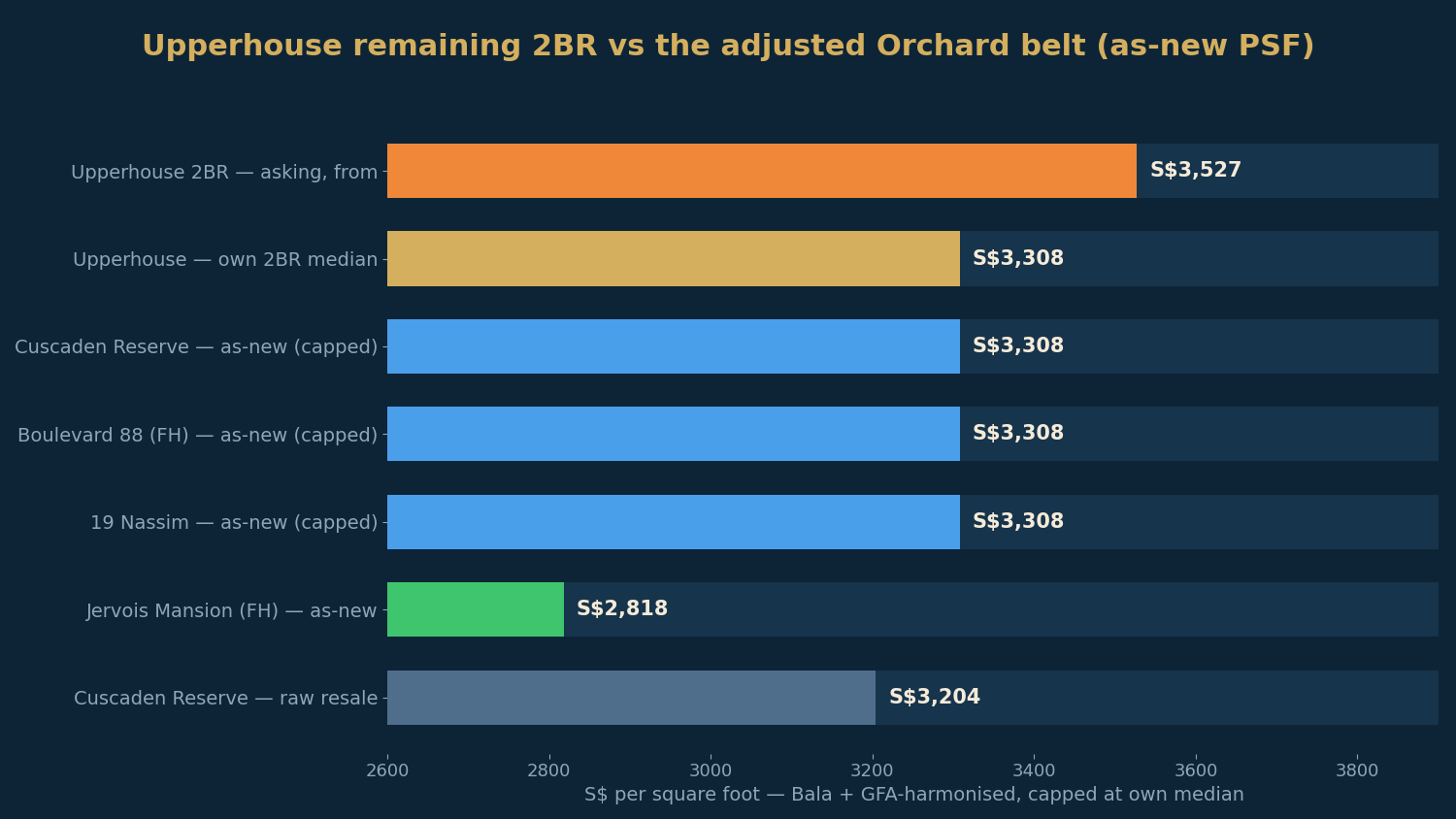

The benchmark: the Orchard belt, adjusted honestly

Raw PSF flatters nothing here — the neighbours are either older freeholds or 99-year projects that have gone sideways — so the NPS calculator lifts each comparable to a like-for-like, as-new footing: age and lease adjustment to a fresh-99 equivalent plus +6% GFA harmonisation for these one- and two-bedder comparisons (the comps pre-date the 22 January 2023 strata rules), capped at the project's own median.

| Comparable | Raw resale PSF | As-new, harmonised |

|---|---|---|

| Upperhouse · 2BR Premium (remaining) | — | S$3,527–3,663 (asking) |

| Upperhouse · 2BR (own median) | — | S$3,308 |

| Cuscaden Reserve (99yr, 2023, 0.22km) | S$3,204 | ~S$3,308 (capped) |

| Boulevard 88 (freehold, 2023, 0.52km) | S$4,041 | ~S$3,308 (capped) |

| Gramercy Park (freehold, 2016, 0.46km) | S$2,798 | ~S$3,308 (capped) |

| 19 Nassim (99yr, 2023, 0.59km) | S$3,317 | ~S$3,308 (capped) |

| Jervois Mansion (freehold, 2025, 0.96km) | S$2,578 | ~S$2,818 |

Four of the five comparables cap out at the project's own S$3,308 median — meaning Upperhouse's own transacted record already sits at the top of its adjusted belt, and the remaining 2BR asks of S$3,527–3,663 sit S$200–350 psf above every adjusted comparable, including freehold Boulevard 88 lifted to as-new. Put rawly: Cuscaden Reserve, a 2023-completed 99-year project a 3-minute walk away, transacts at S$3,204 — about 10% below what the last Upperhouse two-bedders ask. The one genuinely cheaper adjusted door is Jervois Mansion, freehold and 2025-new, at ~S$2,818 as-new a kilometre south — a different address, and the honest alternative for a buyer who wants the postcode's fabric without the station-doorstep premium. Park Nova across the road, at S$6,150 psf, is the reminder of what Orchard freehold-new costs; Upperhouse is not that product, and is not priced as it.

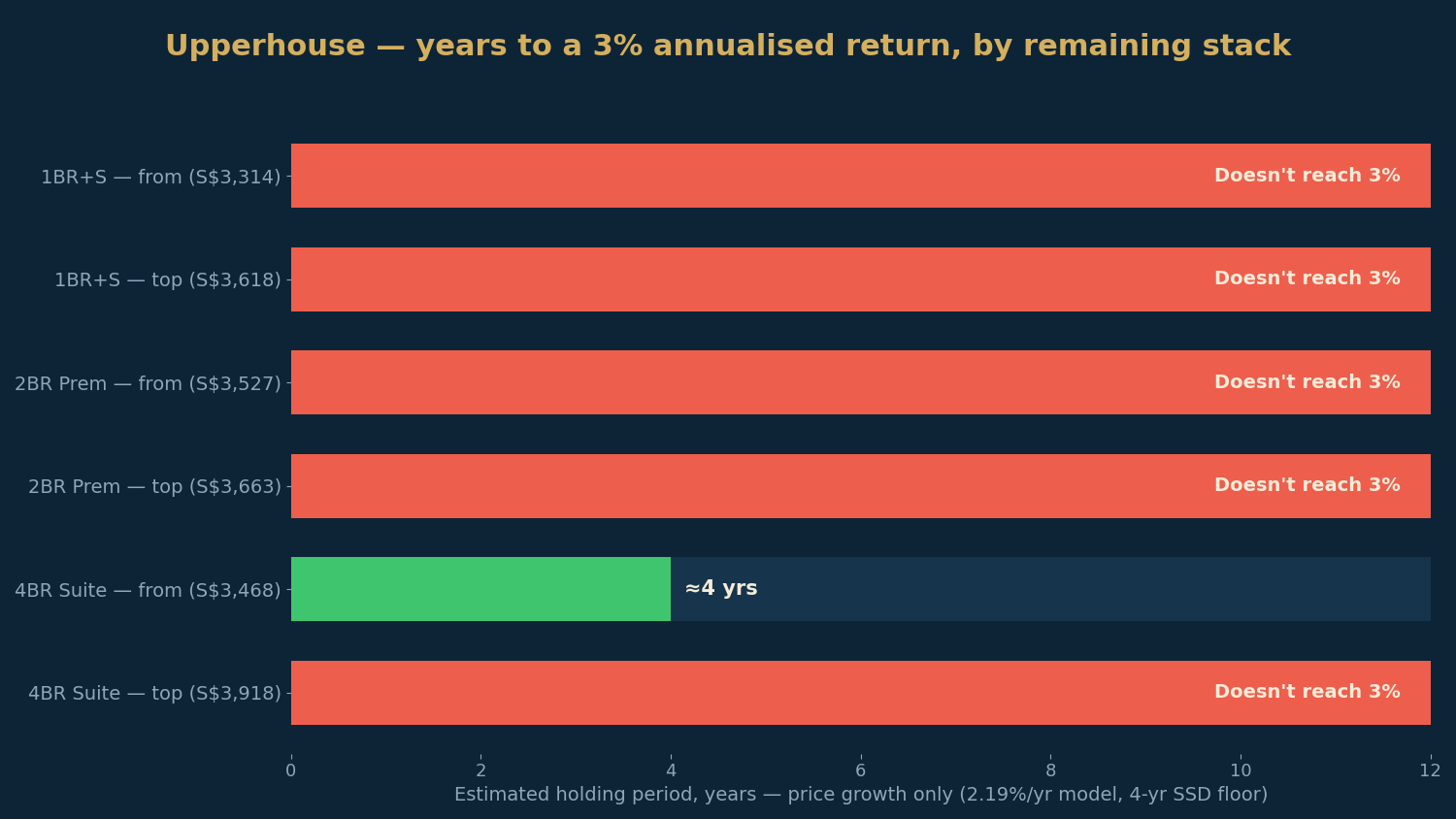

How long you'd likely hold

Seller's stamp duty runs for four years (16%, 12%, 8%, 4%), so no exit before year four is realistic, and the shortest tier we publish is four-to-six years. Using the NPS calculator's model — 2.19% expected growth, a 3% target — here is the estimated holding period for each remaining stack, on price growth alone, against the bedroom's own transacted median as the fair-value anchor. With sub-3% modelled growth, a stack clears the bar only if it enters far enough below fair value — at this growth rate, roughly 3% under — and none of the premium-priced stacks does.

| Available stack | PSF | Hold (price only) |

|---|---|---|

| 1BR+Study 474 sqft — from S$1.571m | S$3,314 | Doesn't reach 3% |

| 1BR+Study 474 sqft — top ask, S$1.715m | S$3,618 | Doesn't reach 3% |

| 2BR Premium 700 sqft — from S$2.469m | S$3,527 | Doesn't reach 3% |

| 2BR Premium 700 sqft — top ask, S$2.564m | S$3,663 | Doesn't reach 3% |

| 4BR Suite 2,056 sqft — from S$7.131m | S$3,468 | 4–6 yrs |

| 4BR Suite 2,056 sqft — top ask, S$8.056m | S$3,918 | Doesn't reach 3% |

The arithmetic is stark because the engine is: at 2.19% modelled growth, the one-bedders would need to enter below S$3,004 psf and the two-bedders below S$3,205 to clear 3% even at the four-year floor — the current asks are S$300–450 above those lines. The single stack the model endorses is the lowest-floor Bespoke suite, entering 3.9% under its own (thin, 18-caveat) fair-value anchor — and a S$7.1 million private-lift suite is an owner's purchase, not an exit trade. Nor does rent rescue the math the way it did at Kassia: the modelled yield here is 2.46%, the thinnest on our board, so even the combined price-plus-rent return runs to roughly 4.7%/yr — held up by the rent, on the biggest cheques in this review series. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

Upperhouse is the cleanest statement yet of the question every 2025–26 CCR launch asks: is a great address with no growth engine a good buy? The card is honest about both halves. The location scores are real — a station under the tower, ION up the road, the only fresh Orchard land in six years, a product split that gave 270 buyers an attainable S$1.3–3.8m entry to the postcode. The engine scores are real too: a decade of ~1.8%/yr prime resale, 2023-vintage neighbours reselling flat, a projected 2.19% that misses our bar, and the thinnest yield we have modelled. The launch proved locals will buy Orchard at 99-year-resale pricing when the gap to the RCR has nearly closed — 53.8% in a day, 81% in a year, is a strong result for a C, and it says the market is pricing the address, the compression trade and the Paterson–Orchard master-plan story, none of which the backward-looking model counts. But what remains is priced above the project's own record into that weak engine: on the model, the one- and two-bedders left don't reach 3% at any holding period. If you are buying Upperhouse now, you are buying it to live at the station door in 249628 — a legitimate purchase the scorecard can't grade — or you are underwriting the master plan yourself. What you are not buying, at S$3,527-and-up for the last two-bedders, is the model's math.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade (C, 5.4), the five factor scores, modelled growth (2.19%/yr), the 2.46% modelled yield, per-bedroom transacted medians, comp past-appreciation rates and the adjusted comparables per the TRIBE New Project Scorecard (URA Data Service transacted PSF; 1km resale trend — 106 resale projects in the ring — lifted for project size, transport and schools; figures as at July 2026). GLS tender result (S$428,280,980 / S$1,617 psf ppr, four bids, Allgreen's Valerian Residential second at S$1,578 psf ppr, awarded 21 February 2024) per EdgeProp and PropertyReviewSG's tender table. Launch result (162 of 301, 53.8%, average S$3,350 psf, 19 July 2025; per-type take-up; buyer profile; the Watten House comparison; the CCR–RCR gap narrowing from 56.5% to 1.9%; Park Nova S$6,150 / Boulevard 88 ~S$4,200 / Cuscaden Reserve >S$3,100 context) per EdgeProp's launch report. Current availability and asking prices (1BR+S last 26 from S$1.571m; 2BR Premium last 19 from S$2.469m; 4BR Suite last 11 from S$7.131m; 6 July 2026) per MySgProp's price guide; the 246-of-301 (81%) sold status (16 July 2026) per newlaunches.sg — agent-carried charts are unofficial and may lag caveats. Project facts (35 storeys, 301 units, Signature/Bespoke split, ADDP Architects, contractual vacant possession 30 June 2029 with a marketed target of H2 2028–2029) per PropertyReviewSG and the developer's factsheet. Foreigner ABSD at 60% per MAS/MOF April 2023 cooling measures. Resale comparables age- and lease-adjusted per Bala's Table with a +6% (1–2BR) GFA-harmonisation uplift, capped at the project's own median, per the NPS calculator's published methodology. The scorecard finds no primary school within 1km on OneMap door-to-door routing while launch coverage cited River Valley Primary as within 1km — verify your unit's door-to-door distance on OneMap before relying on P1 priority. Prices and availability are as reported at the dates cited and will change; scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.