Insights

Honest Insights On Kassia

Kassia grades C (5.1) on the New Project Scorecard — a 268-unit freehold on Flora Drive by TID, with strong District 17 rents but a flat ~2.6%/yr growth history and no MRT within walking distance. Entry from S$1,989 psf; 40 units left.

By TRIBE Editorial · 4 July 2026 · 8 min read

Kassia is a 268-unit freehold development at 31 Flora Drive, in the Loyang and Upper Changi pocket of District 17 on the eastern edge of Pasir Ris, built by TID — the Hong Leong–Mitsui joint venture — with completion due in 2027. It grades a C (5.1) on our New Project Scorecard (NPS), and the grade is a clean lesson in what freehold tenure does and does not buy. The card has one real strength — District 17's rental momentum — and two structural drags: a flat ~2.6% a year capital-growth history and no MRT within walking distance. It has sold roughly 85% of its units and lists the rest from S$1,989 psf. This is an honest look at what the C reflects, and who a sub-S$2m freehold this far from a train actually suits. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted for the project's own size, transport and schools, not a forecast.

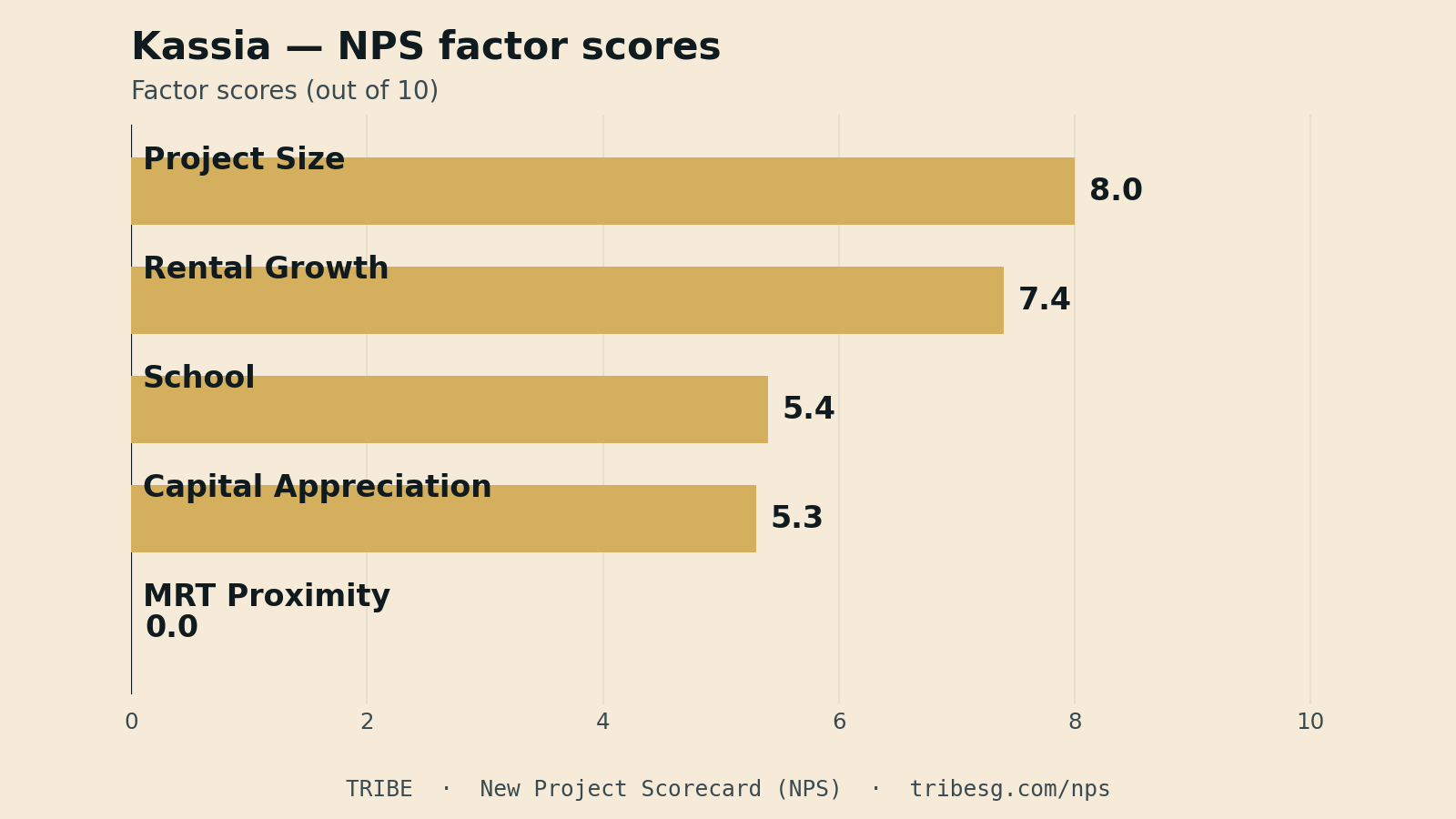

The scorecard: what a C actually says

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| Project Size | 8.0 | 268 units — scale for facilities and resale liquidity |

| Rental Growth | 7.4 | District 17 rents grew ~7.0%/yr over the decade — strong rental momentum |

| School | 5.4 | 2 primaries within 1km; East Spring Primary 0.65km (balanced) |

| Capital Appreciation | 5.3 | District 17 resale grew ~2.6%/yr over the decade → projected ~2.7%/yr |

| MRT Proximity | 0.0 | Tampines East MRT is a ~2km walk (~1.2km straight-line) |

The one genuinely strong factor is rental growth: District 17 rents have grown about 7.0% a year over the decade, near the top of the absolute scale, and the eastern rental catchment — Changi, the airport and business park, Loyang's industrial estates — is real tenant demand. Project size is comfortable at 268 units, and schools are decent, with East Spring Primary a 0.65km walk. The two drags are the ones freehold cannot fix. Resale homes across District 17 appreciated only about 2.6% a year over the past decade — a same-property resale basis that strips out new-launch inflation — and after a marginal tilt the projected growth is roughly 2.7% a year, under the 3% bar. And the MRT factor is a zero: the nearest station, Tampines East on the Downtown Line, is close to a two-kilometre walk. Freehold tenure protects against lease decay; it does not manufacture the growth history the district never had, or move a train closer.

Still a third to sell

Kassia launched in July 2024 and moved just over half its units on its opening weekend at S$1,821 to S$2,177 psf. Two years on it is roughly 85% sold, with 40 of 268 units still on the balance list — a slower, steadier sell-down than the near-sell-outs in the prime and integrated launches, which is what you would expect from a freehold priced ahead of its leasehold neighbours in a location the MRT map skips.

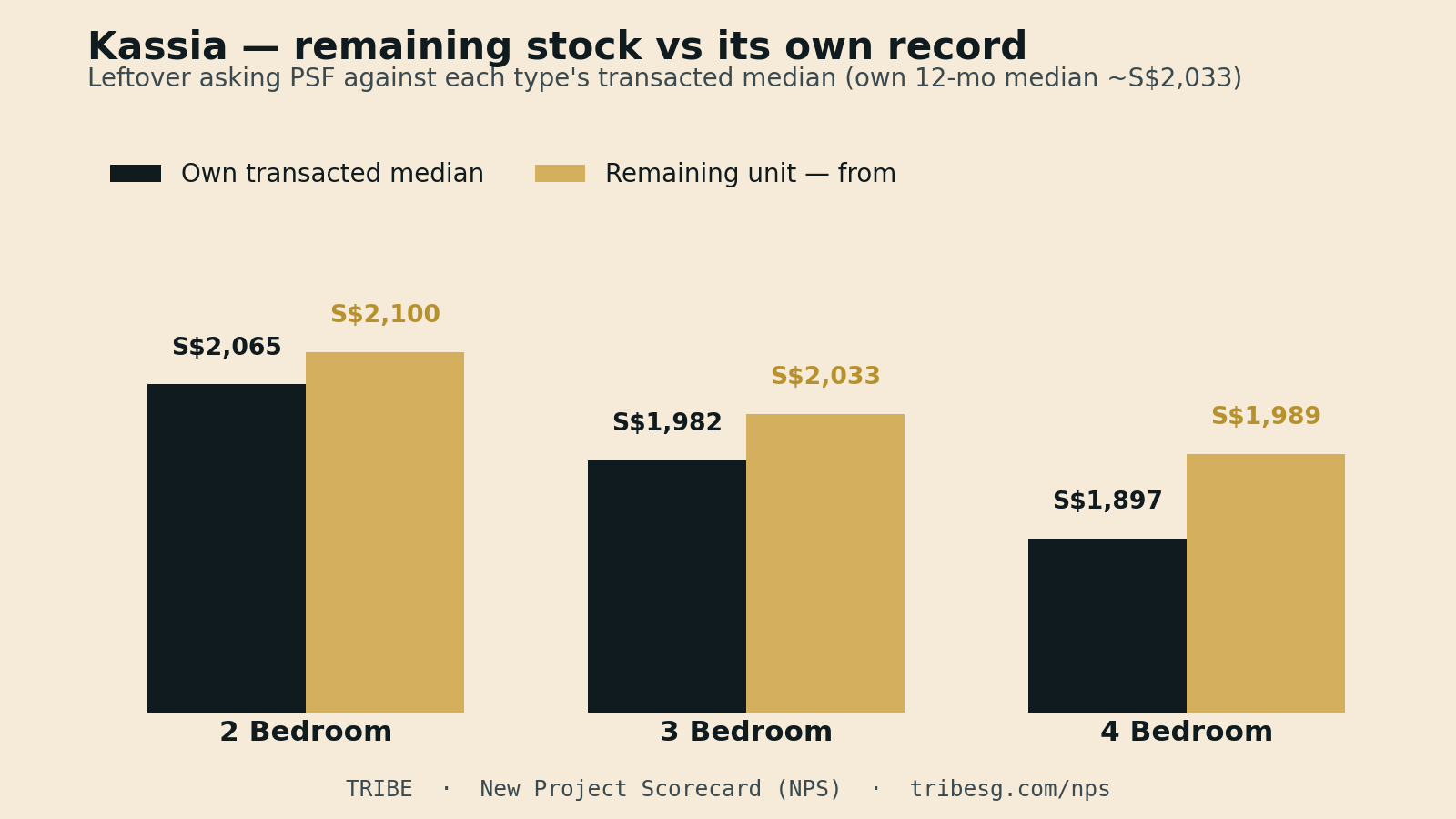

The one-bedroom stock is gone; what remains spans two- to four-bedders, and the larger the unit, the lower the psf:

| Type | Units left | Indicative from | ~PSF from |

|---|---|---|---|

| 2 Bedroom | 6 of 108 | S$1.581m | S$2,100 |

| 3 Bedroom | 19 of 56 | S$2.145m | S$2,033 |

| 4 Bedroom | 15 of 24 | S$2.675m | S$1,989 |

Against its own record, the leftover stock is priced a shade above where the project has been transacting. Kassia's own transacted record runs to about 226 caveats over the year to April 2026 at a median near S$2,033 psf; by bedroom, the medians sit around S$2,065 (2BR), S$1,982 (3BR) and S$1,897 (4BR). The remaining units start a touch above each of those — the 2-bedders about 1.7% over their own median, the 3-bedders 2.6%, the 4-bedders 4.8% — the normal pattern of a developer holding firm on its last, best-facing stacks. The accessible part is the quantum: a two-bedroom from S$1.581m, or the lowest-psf way in, a four-bedroom from S$1.989m — a freehold family unit under S$2m, which is genuinely scarce.

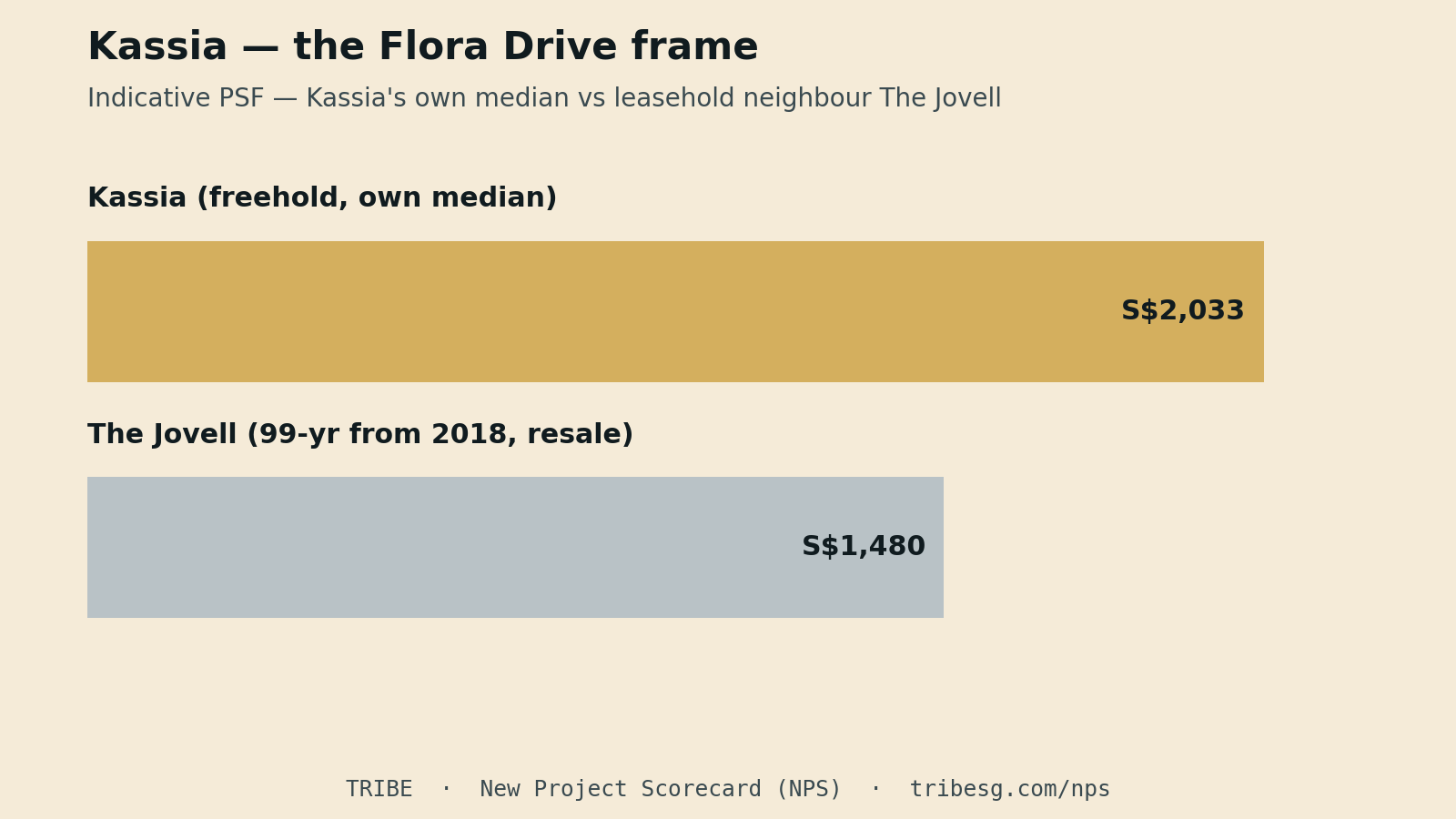

The second benchmark: the Flora Drive frame

The most revealing comparison is next door — and it is a leasehold one, because there is no directly comparable freehold new launch in this pocket, which itself tells you something about the location.

| Comparable | What it is | Indicative PSF |

|---|---|---|

| Kassia (own median) | Freehold, 2024 launch | ~S$2,033 (own transacted median) |

| The Jovell | 99-yr from 2018, Flora Drive, resale | ~S$1,480 (12-mo average) |

The Jovell — a 428-unit 99-year leasehold completed in 2022, a few doors down on the same Flora Drive — trades on resale at about S$1,480 psf. Kassia's ~S$2,033 psf own median sits roughly 37% above that. Most of that gap is exactly what you would expect a freehold, brand-new launch to command over an older leasehold neighbour — fresh tenure, new build, developer pricing — but the size of it is the honest flag: you are paying a full freehold-and-new premium in a location whose 99-year stock trades in the low-S$1,000s, and the scorecard's ~2.6%/yr growth history says the district has not historically re-rated that premium upward. The absence of any freehold new-launch comparable nearby is not a scarcity bonus here; it reflects a pocket the market treats as a leasehold, MRT-light suburb.

How long you'd likely hold

Using the NPS calculator's model — 2.7% expected growth, a 3% target — here is the estimated holding period for each remaining stack, on price growth alone and with the area's ~3.3% rental yield added.

| Available stack | PSF | Hold (price only) | Hold (with rent) |

|---|---|---|---|

| 2 Bedroom · from 657 sqft | S$2,100 | Doesn't reach 3% | 4–6 yrs |

| 3 Bedroom · from 904 sqft | S$2,033 | Doesn't reach 3% | 4–6 yrs |

| 4 Bedroom · from 1,346 sqft | S$1,989 | Doesn't reach 3% | 4–6 yrs |

The table is blunt, and it is meant to be. Because modelled growth of 2.7% sits below the 3% bar, and every remaining stack is priced at or above the project's own transacted median, no stack reaches a 3% annual return on price growth alone — the district's flat resale history gives no basis to buy Kassia primarily for appreciation. What makes the maths work is income: add District 17's ~3.3% rental yield and every stack clears in the four-to-six-year tier, carried by rent rather than price. Kassia is coherent as a freehold rental or own-stay hold — strong tenant catchment, no lease decay, a sub-S$2m entry — but the returns lean on the yield, not the capital. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

Kassia is a clean example of why freehold is a feature, not a thesis. The C (5.1) is not a verdict on the building; it is the scorecard reporting that this pocket of District 17 has strong rents but a soft ~2.6%/yr growth decade, and that the nearest MRT is a two-kilometre walk — neither of which freehold tenure changes. Priced from S$1,989 psf, it offers something genuinely scarce: a brand-new freehold family unit under S$2m, with a real eastern rental catchment behind it. If you are a landlord or own-stayer who values freehold tenure and the Changi–Loyang rental demand, and you are clear-eyed that the model has price growth under the 3% bar and rent doing the work, it fits. If you are buying for appreciation, the scorecard is telling you plainly to look at the district's history first — because freehold will not supply the growth the last decade didn't, and the MRT will not get any closer.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade, the five factor scores and projected growth per the TRIBE New Project Scorecard (URA Data Service transacted PSF; district resale trend lifted for project size, transport and schools; figures as at July 2026). Kassia's own transacted record (~226 caveats to April 2026, median ~S$2,033 psf) and July 2024 launch pricing (S$1,821–S$2,177 psf) per PropertyGuru and 99.co. Comparable indicative PSF for The Jovell per 99.co / EdgeProp transaction data. Indicative pricing and balance units from the project price list (updated June 2026); availability changes as units sell. Scores are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.