Insights

Honest Insights On Arina East Residences

Arina East Residences grades B (5.6) on the New Project Scorecard — the first freehold launch in Tanjong Rhu in over a decade, a three-minute walk from Katong Park MRT. Strong on tenure and transport, but with no school within 1km and price growth that clears 3% by a whisker.

By TRIBE Editorial · 4 July 2026 · 8 min read

Arina East Residences is a 107-unit, freehold development on Tanjong Rhu Road in District 15, a three-minute walk from Katong Park MRT on the Thomson–East Coast Line, built by ZACD Group and FRX Capital with completion around 2028. It is the first new condo launch in Tanjong Rhu in over a decade, and it grades a B (5.6) on our New Project Scorecard (NPS) — a middling card with a very clear split. The freehold tenure and the walk-to-the-platform MRT are real strengths; a missing school catchment and a thin growth engine are the offset. This is an honest look at what the B rests on, what the remaining units cost, and how long you would likely need to hold each. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design. For the holding period, we use the published NPS calculator: fair value is the median transacted PSF for each bedroom type, the project grows at its modelled rate, and we report the years needed to clear a 3% annual return — gross of stamp duty, financing and selling costs.

The scorecard: a card that splits

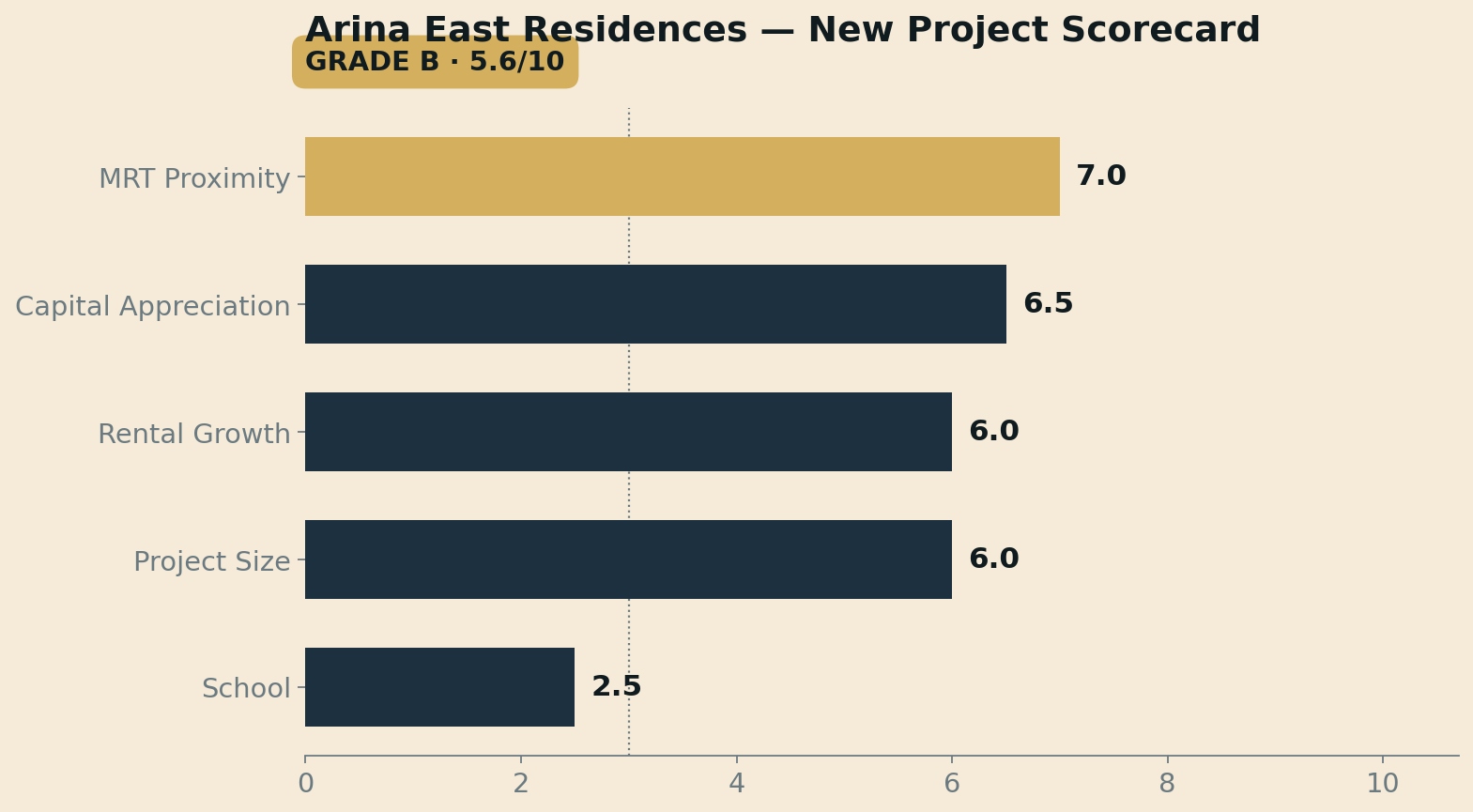

Arina East's 5.6 is the average of two clear halves — a strong top, a weak floor.

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| MRT Proximity | 7.0 | A 0.42km, three-minute walk to Katong Park MRT (Thomson–East Coast Line) |

| Capital Appreciation | 6.5 | 1km resale grew ~3.2%/yr over the decade; barely lifted for a boutique 107 units |

| Rental Growth | 6.0 | District 15 rents grew ~6.1%/yr over the decade |

| Project Size | 6.0 | 107 units — a boutique development |

| School | 2.5 | No primary school within 1km — the card's clear weak spot |

The strengths are genuine. Freehold tenure in a district that is mostly leasehold, and a Thomson–East Coast Line platform three minutes from the door, are exactly the durable traits the scorecard rewards — hence the 7.0 on transport. But two things hold the grade to a B. The first is the 2.5 on schools: there is no primary school within a kilometre, which the model reads as weaker family demand. The second is subtler and matters more for returns: the growth engine is thin. Resale homes within 1km appreciated about 3.2% a year over the past decade — a same-property resale basis — and because Arina East is a boutique 107-unit project, the model's quality lift is almost nil (+0.02). The projected growth lands at about 3.2% a year — it clears the 3% bar, but by a whisker. That single fact shapes the whole holding-period read below.

What's left — and what it costs

Arina East launched quietly. It was previewed on 31 May 2025 and opened for sale on 7 June 2025 by private placement — 10 of 107 units, 9.3%, at an average of S$3,008 psf — a deliberately low-key release over the school holidays rather than a full launch. Sales have compounded since: by the latest data the project has transacted 82 units at a median of S$2,812 psf (June 2025–May 2026), leaving roughly 25 units, about a quarter of the project, still available, with availability changing as units sell.

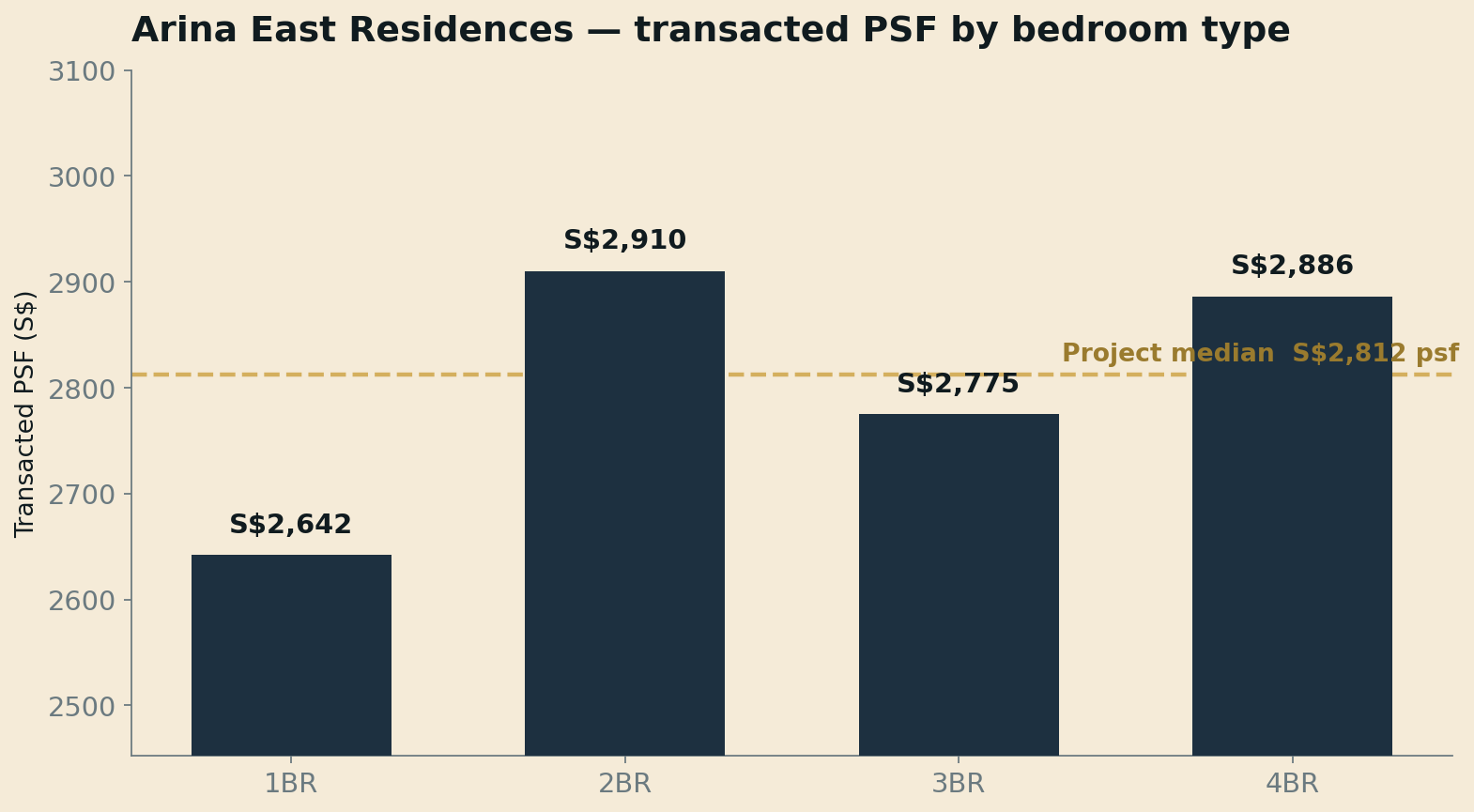

Here is what each format has been transacting at, from the project's own URA caveats:

| Type | ~Size | Transacted PSF |

|---|---|---|

| 1 Bedroom | 495 sqft | S$2,642 |

| 2 Bedroom | 797 sqft | S$2,910 |

| 3 Bedroom | 1,087 sqft | S$2,775 |

| 4 Bedroom | 1,389 sqft | S$2,886 |

The pattern is the usual boutique one: the two-bedders carry the highest psf (S$2,910, the efficient investor format), the one-bedders the lowest quantum (S$2,642 psf but the smallest cheque), and the three- and four-bedders sit around the S$2,812 psf project median. There is no deep value stack here and no fire-sale tail — this is a small freehold project selling steadily at a consistent level, and the remaining quarter is priced in line with what has already sold.

The second benchmark: freehold scarcity against the launch pack

Against nearby transactions, Arina East's level reflects two premiums stacked together — freehold, and the first new launch Tanjong Rhu has seen in over a decade.

| Comparable | Tenure · what | Distance | Recent PSF |

|---|---|---|---|

| Arina East Residences | Freehold, 2025 launch | — | ~S$2,812 (own median) |

| Grand Dunman | 99-yr, 2023 launch | ~1.2 km | ~S$2,524 (median) |

| Riveredge | 99-yr resale, 2008 | 0.71 km | ~S$1,901 |

| Pebble Bay | 99-yr resale, 1997 | 0.48 km | ~S$1,846 |

| Parkshore | Freehold resale, 1995 | 0.67 km | ~S$1,585 |

Arina East's ~S$2,812 psf runs about 11% above Grand Dunman — the nearest recent 99-year launch — and well above the ageing leasehold resale that surrounds it, which trades in the S$1,585–1,901 range. Part of that gap is the new-launch premium every fresh project carries; part is genuinely the freehold. The honest question for a buyer is whether the freehold and the scarcity are worth roughly a tenth more than a strong 99-year launch a kilometre away — a fair trade for a long-hold owner-occupier, a closer call for an investor whose return leans on a growth number that only just clears the bar.

How long you'd likely hold

Using the NPS calculator's model — ~3.2% expected growth, a 3% target — here is the estimated holding period for each remaining stack, on price growth alone and with the area's ~3.0% rental yield added.

| Available stack | PSF | Hold (price only) | Hold (with rent) |

|---|---|---|---|

| 1 Bedroom · 495 sqft | S$2,642 | 4–6 yrs | 4–6 yrs |

| 2 Bedroom · 797 sqft | S$2,910 | 4–6 yrs | 4–6 yrs |

| 3 Bedroom · 1,087 sqft | S$2,775 | 4–6 yrs | 4–6 yrs |

| 4 Bedroom · 1,389 sqft | S$2,886 | 4–6 yrs | 4–6 yrs |

The modelled 3.2% growth does clear the 3% bar, so on price alone every stack reaches a 3% return in the 4–6 year tier — but only just. The margin over 3% is about two-tenths of a percentage point, so price growth on its own leaves almost no cushion for stamp duty, financing and selling costs. What makes the hold comfortable is the ~3.0% rental yield: with rent counted, the same stacks clear the 4–6 year tier with real room to spare. That is the honest way to read Arina East — a freehold-and-yield hold, where the income and the tenure do the work, not a capital-growth play riding a strong district trend. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

Arina East Residences is a genuinely rare thing — a freehold launch, three minutes from an MRT, in a Tanjong Rhu enclave that has not seen a new condo in over a decade — and for the right buyer that scarcity is the whole point. But the scorecard is honest about the trade. The B (5.6) is a strong top (freehold, transport) averaged against a real weak floor (no school within 1km, and a boutique-size project whose growth engine clears 3% by a whisker). The numbers say the same thing twice: at ~S$2,812 psf you are paying a freehold premium over a stronger-graded 99-year launch nearby, and the modelled growth needs the ~3.0% rental yield to make the hold comfortable. For a long-hold owner-occupier who values freehold tenure and a walk-to-the-platform address, that is a defensible, eyes-open buy. For an investor chasing capital growth, a higher-graded launch will likely compound faster — Arina East's return is a yield-and-tenure story, and it is best bought as one.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade, the five factor scores, modelled growth and rental yield per the TRIBE New Project Scorecard (URA Data Service transacted PSF; 1km resale trend lifted for project size, transport and schools; figures as at July 2026). June 2025 private-placement launch (10 units, 9.3%, average S$3,008 psf) per EdgeProp. Arina East per-bedroom transacted PSF and the S$2,812 psf project median from URA caveats via our NPS dataset (82 caveats, June 2025–May 2026). Grand Dunman and nearby resale comparables per the TRIBE scorecard. Availability and pricing change as units sell. Scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.