Insights

Honest Insights On J'den

J'den grades A (7.6) on the New Project Scorecard — CapitaLand's 368-unit integrated tower on the former JCube site at Jurong East MRT, the best-selling launch of 2023, now 97% sold. Just 10 large-format units remain, from S$2,523 psf.

By TRIBE Editorial · 4 July 2026 · 8 min read

J'den is a 368-unit, 99-year leasehold development rising on the site of the former JCube mall in District 22, directly above Jurong East MRT — the East-West and North-South interchange at the heart of Jurong Lake District — built by CapitaLand Development with completion due in 2028. It grades an A (7.6) on our New Project Scorecard (NPS), and the market did not wait for the grade: J'den launched in November 2023 and sold 323 of 368 units — 88% — on its first day at an average of S$2,451 psf, the best-selling new launch of that year. By June 2026 it was 97% sold, with just 10 units left. Every one- and two-bedroom is gone; only large three- and four-bedders remain. This is an honest look at what the A rests on, what a near-sell-out proves, and who the leftover stock is actually for. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted for the project's own size, transport and schools, not a forecast.

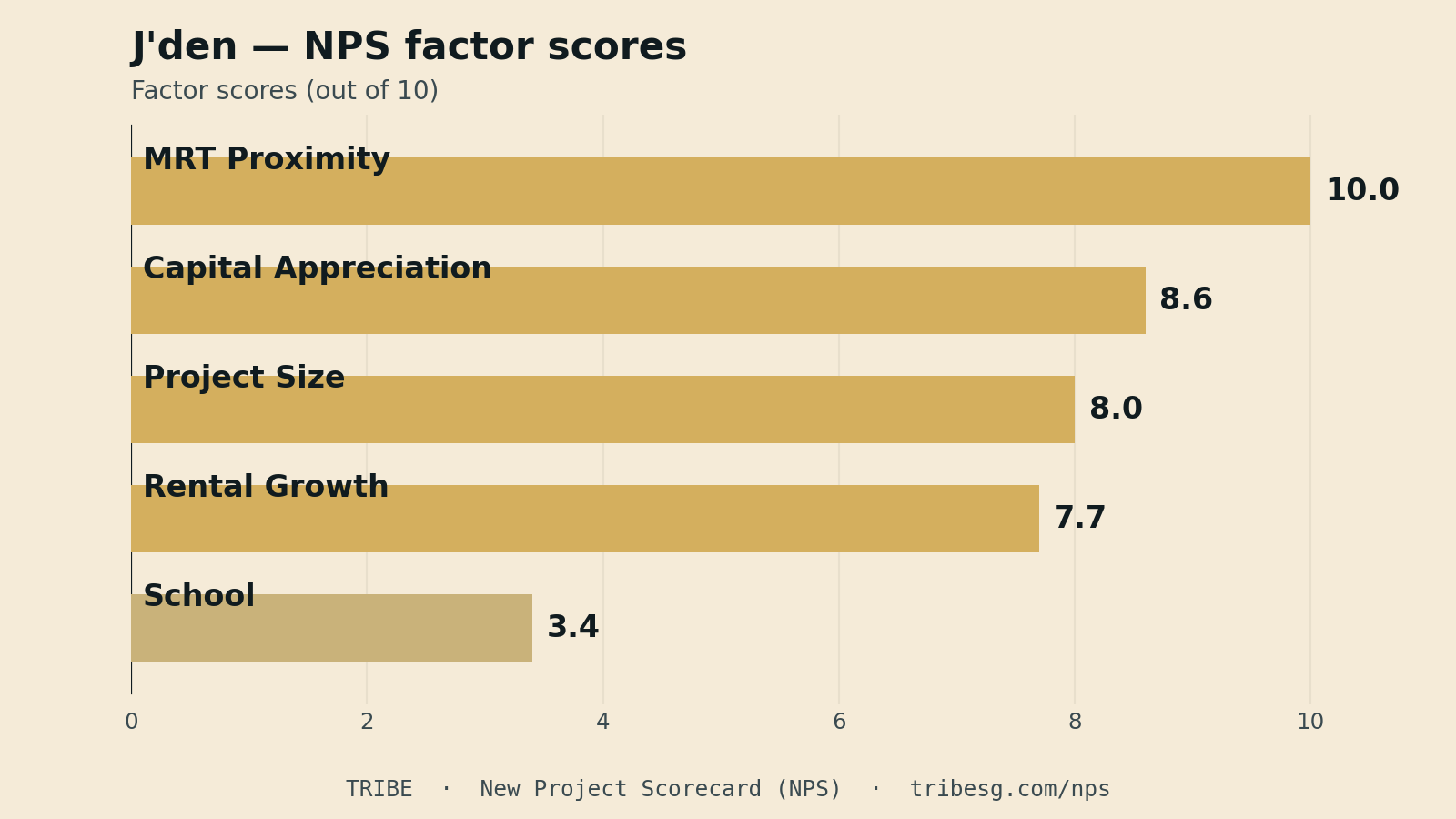

The scorecard: what an A actually says

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| MRT Proximity | 10.0 | Integrated development — direct access to Jurong East MRT (EW24/NS1 interchange) |

| Capital Appreciation | 8.6 | District 22 resale grew ~3.7%/yr over the decade; lifted ~1.2 for size, transport, schools → ~4.9%/yr |

| Rental Growth | 7.7 | District 22 rents grew ~7.1%/yr over the decade — strong rental momentum |

| Project Size | 8.0 | 368 units — scale for facilities and resale liquidity |

| School | 3.4 | 2 primaries within 1km; best is Fuhua Primary (0.57km, undersubscribed) |

The A is built on transport and growth, not on a broad sweep of every factor. The MRT score is the maximum: J'den is an integrated development sitting directly on Jurong East station, the East-West and North-South Line interchange, with the future Jurong Region Line and covered links to Westgate, JEM, IMM and the bus interchange — this is the transport core of Jurong Lake District, the second CBD the government has spent a decade planning. The capital-appreciation factor is the strongest we have scored in this series: District 22 resale homes grew about 3.7% a year over the past decade — a same-property resale basis that strips out new-launch inflation — and after the model's +1.2 tilt for J'den's integrated transport, size and schools, the projected growth is about 4.9% a year, clearing the 3% bar with real room to spare. District 22 rents grew about 7.1% a year, near the top of the scale. The one honest soft spot is schools: two primaries sit within a kilometre, but the nearest, Fuhua Primary, is undersubscribed, so the model reads school pull as limited. On this card, the district's transport and transacted history do the heavy lifting.

Sold down to the large units

J'den's own record is the clearest evidence the grade is not theoretical. It launched on 11 November 2023 and moved 323 units — 88% of the project — on day one at an average of S$2,451 psf, making it CapitaLand's best-selling launch of the year; over 99% of buyers were Singaporeans and permanent residents. By the developer's June 2026 balance list, only 10 units remained — a 97% sell-through.

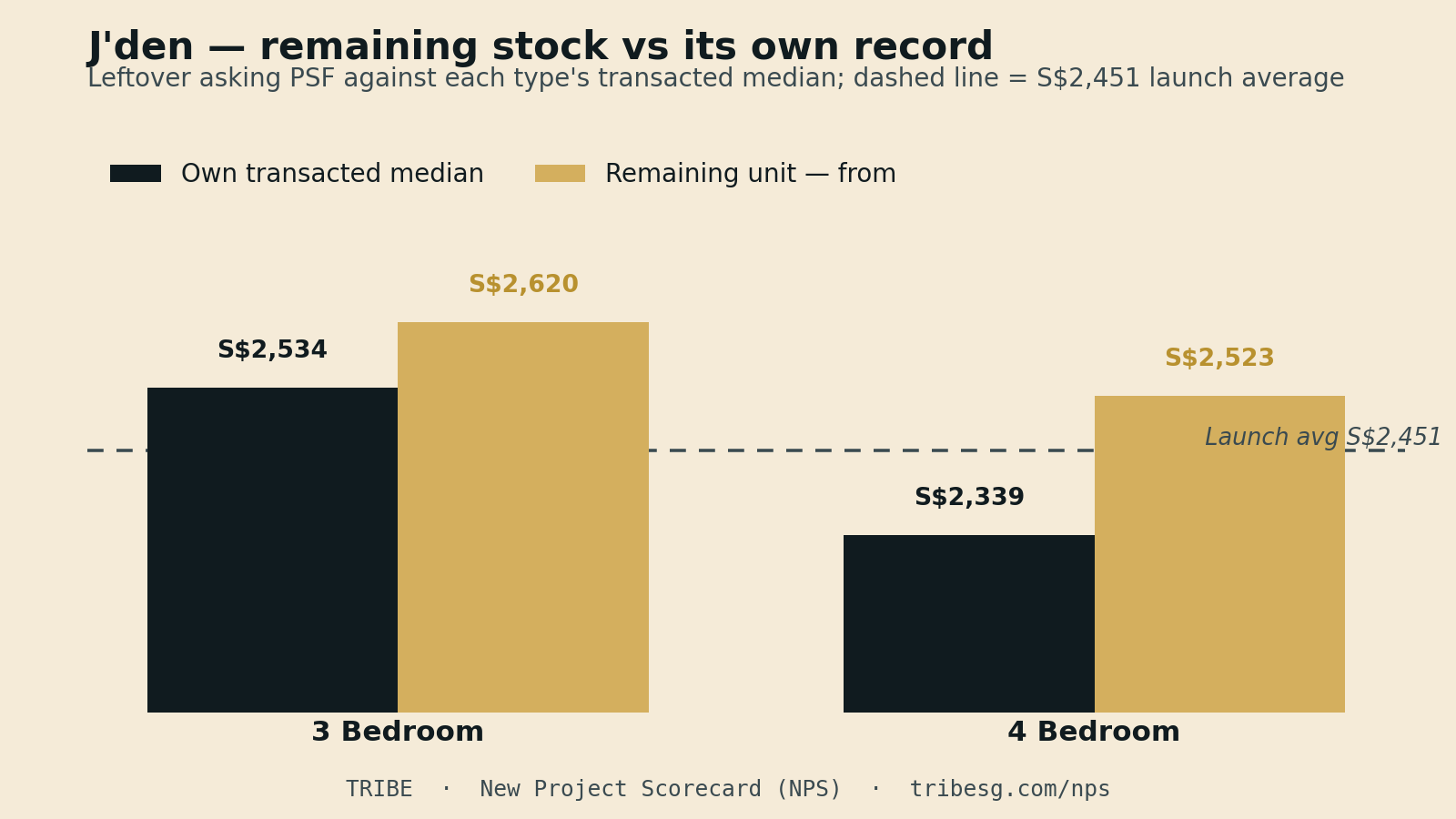

What is left is entirely the large-format tail. The one- and two-bedroom stock — 74 and 148 units respectively — is fully sold; the remaining 10 units are all three- and four-bedders.

| Type | Units left | Indicative from | ~PSF from |

|---|---|---|---|

| 3 Bedroom | 2 of 109 | S$3.102m | S$2,620 |

| 4 Bedroom | 8 of 37 | S$3.747m | S$2,523 |

The leftover stock is not a discount. The remaining four-bedders start at S$2,523 psf — about 3% above the S$2,451 launch-day average — and the two three-bedders at S$2,620 psf sit roughly 7% above it. These are the last, best-facing units in a near-sold-out project, and they are priced accordingly. The quantum is the real gate: entry is S$3.102m for a three-bedroom and S$3.747m for a four-bedroom. The affordable formats sold on day one; the family-sized units, at S$3.1m-plus cheques, are the deliberate remainder.

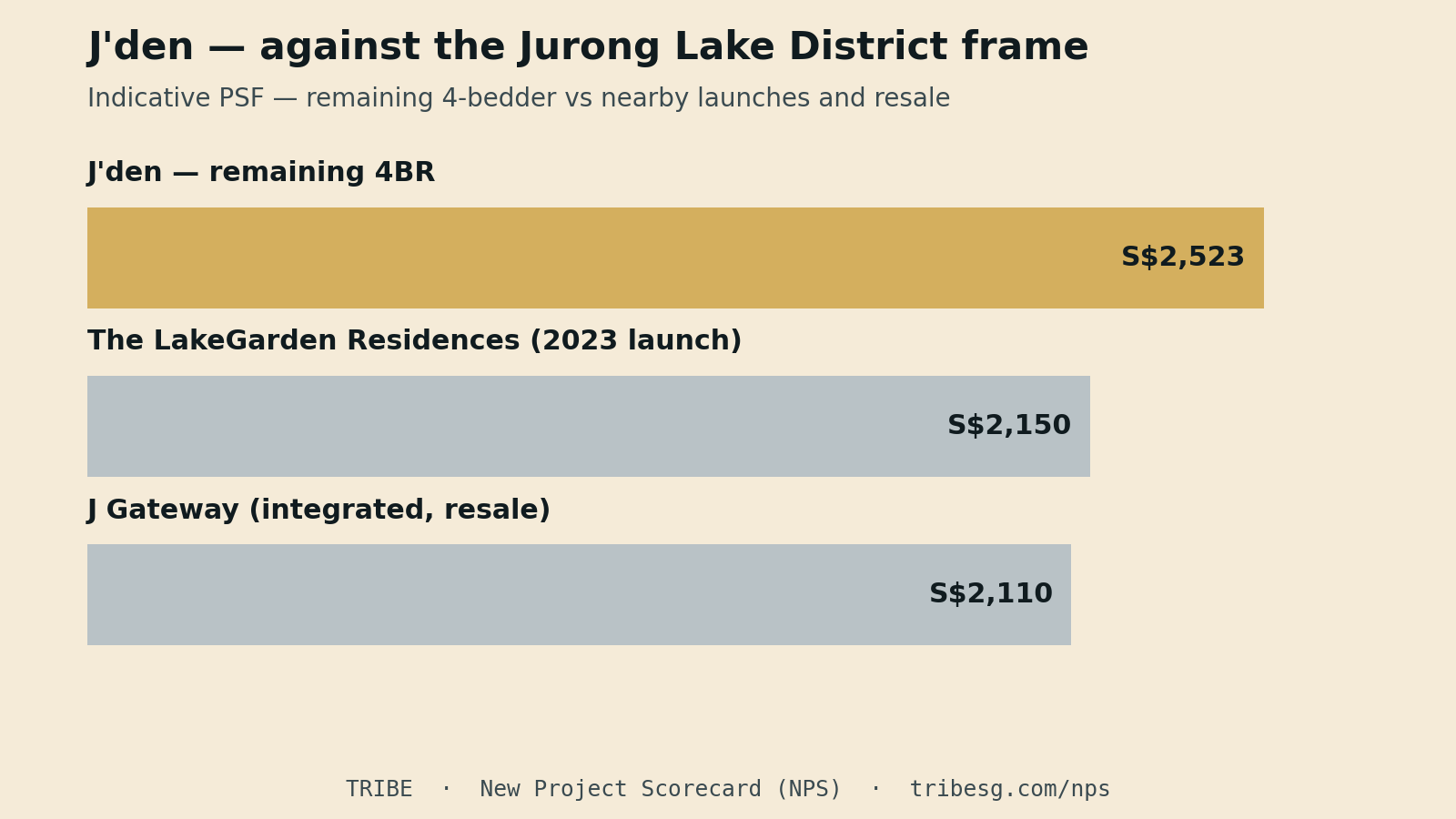

The second benchmark: the Jurong Lake District frame

Against its neighbours, J'den's pricing carries a clear integrated-development premium — and it is worth seeing exactly how large that premium is.

| Comparable | What it is | Indicative PSF |

|---|---|---|

| J'den (remaining 4BR) | 99-yr, integrated, 2023 launch | S$2,523 |

| The LakeGarden Residences | 99-yr, Yuan Ching Road, 2023 launch | ~S$2,150 (12-mo average) |

| J Gateway | 99-yr, integrated, 2016, resale | ~S$2,110 (12-mo average) |

J Gateway is the cleanest like-for-like: the other integrated development at Jurong East, completed 2016, now transacting on resale at about S$2,110 psf. J'den's remaining four-bedders at S$2,523 psf sit roughly 20% above that, and about 17% above The LakeGarden Residences (~S$2,150), the nearest recent 99-year launch by the lake. Some of that gap is fair — J'den is brand new, on a fresh 99-year lease, and directly plugged into the interchange in a way LakeGarden is not — and some of it is the premium a buyer pays for being last through the door on the district's headline project. Set against the project's own record, the read is the same: at S$2,523–2,620 psf the leftover stock is priced 3–7% above where the 323 launch-day buyers came in. You are buying conviction in Jurong Lake District at the top of J'den's own range, not finding value beneath it.

How long you'd likely hold

Using the NPS calculator's model — 4.9% expected growth, a 3% target — here is the estimated holding period for each remaining stack, on price growth alone and with the area's ~3.5% rental yield added.

| Available stack | PSF | Hold (price only) | Hold (with rent) |

|---|---|---|---|

| 3 Bedroom · from 1,184 sqft | S$2,620 | 4–6 yrs | 4–6 yrs |

| 4 Bedroom · from 1,485 sqft | S$2,523 | 4–6 yrs | 4–6 yrs |

This is the rare card where the scorecard and the sales chart agree. Because modelled growth of 4.9% clears the 3% bar comfortably, both remaining stacks reach a 3% annual return in the four-to-six-year tier on price growth alone, even entering a few percent above the project's own launch average — the district's ~3.7%/yr resale history and the integrated-MRT premium absorb the entry price. Rent only shortens the margin, not the tier. The practical caveat is timing, not returns: completion is around 2028, so the holding clock starts at keys, not at booking. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

J'den is what an A-grade integrated launch looks like when the market agrees with the scorecard before the scorecard is even written. The card is carried by the maximum transport score, the strongest capital-appreciation history in this series (~4.9%/yr projected, clearing the bar), and strong District 22 rents — the fundamentals of Jurong Lake District, priced into a tower you can walk from platform to lift lobby. The honest caveat is not quality; it is access and price discipline. What is left is a 10-unit large-format tail from S$2,523 psf but S$3.1m upward in quantum, priced 3–7% above what launch-day buyers paid, which suits one specific buyer — someone who wants a three- or four-bedroom at the heart of the second CBD and has the S$3m-plus cheque and the holding power to 2028 — and no one else. If that is you, the scarcity is the story. If it isn't, the affordable J'den sold out eighteen months ago.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade, the five factor scores and projected growth per the TRIBE New Project Scorecard (URA Data Service transacted PSF; district resale trend lifted for project size, transport and schools; figures as at July 2026). November 2023 launch take-up (323 units, 88%, average S$2,451 psf, best-selling launch of 2023) per CapitaLand newsroom and EdgeProp. Comparable indicative PSF for J Gateway and The LakeGarden Residences per 99.co / PropertyGuru transaction data. Indicative pricing and balance units from the project price list (updated June 2026); availability changes as units sell. Scores are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.