Insights

Honest Insights On Pinery Residences

Pinery Residences grades S (9.0) on the New Project Scorecard — the highest grade on our board. Hoi Hup and Sunway's 588-unit integrated project above Tampines West MRT sold 92.5% at launch in March 2026; 34 units remain, all of them four- and five-bedders.

By TRIBE Editorial · 16 July 2026 · 12 min read

Pinery Residences is a 588-unit, 99-year integrated development on Tampines Street 94 — six 14-storey blocks by Hoi Hup Realty and Sunway Developments above a direct underground link to Tampines West MRT on the Downtown Line and the 121,600 sqft Pinery Mall. It grades S (9.0) on our New Project Scorecard (NPS) — the highest grade on our board, above Parktown Residence's S 8.6 and The Chuan Park's S 8.9 — and the market treated it that way: 544 of 588 units (92.5%) sold on the 28–29 March 2026 launch weekend at an average of S$2,546 psf. Three and a half months later, the 14 July 2026 balance chart shows 34 units left, every one of them a four-bedroom-plus-study or five-bedder. This is a look at what a 9.0 is made of, what the launch actually proved, and whether the big-format tail is priced like a victory lap. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted for the project's own size, transport and schools, not a forecast.

The scorecard: what the S actually says

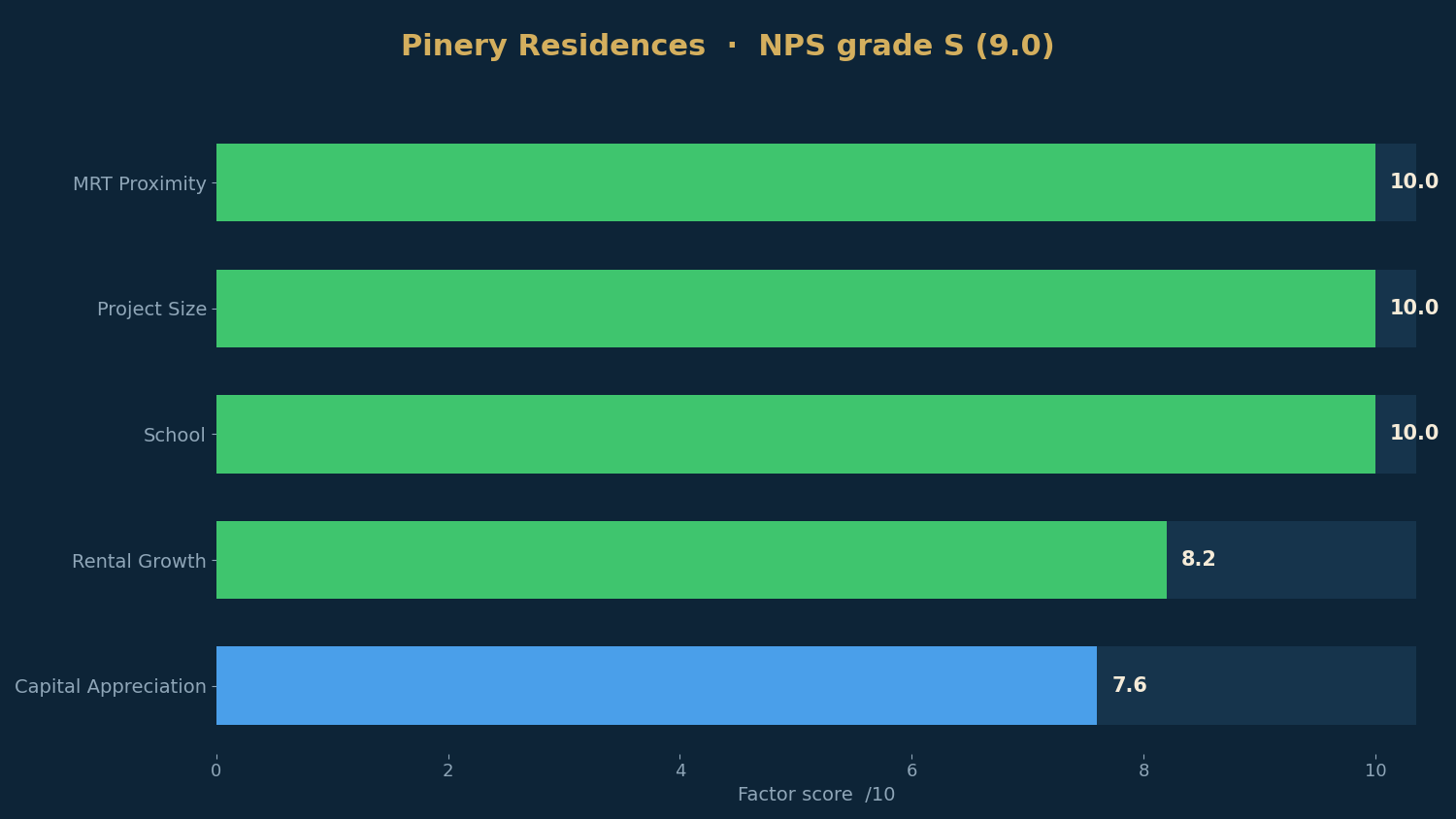

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| MRT Proximity | 10.0 | Integrated — direct underground link to Tampines West MRT (Downtown Line) |

| Project Size | 10.0 | 588 units — ideal scale for liquidity and facilities |

| School | 10.0 | 4 primaries within 1km; Junyuan (0.47km) heavily oversubscribed |

| Capital Appreciation | 7.6 | D18 resale grew ~3.1%/yr; lifted +1.45 for size, transport, schools → ~4.5%/yr |

| Rental Growth | 8.2 | District 18 rents grew ~7.4%/yr over the decade |

Three factors max out, and none of them is a technicality. MRT scores 10 as an integrated development: the underground pedestrian link puts the Downtown Line under the doorstep, one stop from the Tampines interchange. One honest boundary, though — this is the mall-and-train version of "integrated", a FairPrice, a Kopitiam food court and a childcare centre in the podium, not Parktown Residence's fuller bundle of mall, bus interchange, community club and hawker centre one town-sector north. School scores 10 with four primaries inside the kilometre and heavily-oversubscribed Junyuan Primary at 0.47km — inside the 1km priority ring, with St. Hilda's at 0.67km — a genuine ballot address, the thing Tampines buyers pay for. Size scores 10 at 588 units.

The engine behind those location scores is strong rather than spectacular. The 1km ring around Tampines Street 94 holds only three resale condo projects — too thin for a local trend — so the model falls back to the district series: D18 resale appreciated ~3.1% a year over the decade on a same-property basis, and the project's near-maximum quality tilt (+1.45 of a possible +1.5) lifts projected growth to 4.53% a year — clearing the 3% bar comfortably. Rental growth scores 8.2 on D18's ~7.4%/yr decade, among the strongest districts on our board, and the modelled gross yield is 3.59% — this is HDB-upgrader-and-tenant country, and 2026 is the year Tampines and Bedok's MOP supply jumps from 527 flats to 2,133.

The land bid that priced the launch, and the launch that cleared it

The site told you the launch price a year and a half early. The Tampines Street 94 GLS tender closed in September 2024 with six bids — the most for a non-EC private site since Clementi Avenue 1 in November 2023 — and Hoi Hup–Sunway took it at S$668.28 million, or S$1,004 psf ppr, just 1.9% over Sing Holdings' S$985. That is 13% above the S$885 psf ppr paid for the Parktown mega-site eighteen months earlier, for a smaller integrated bundle. The market shrugged: the two-week preview from 14 March 2026 drew over 8,500 visitors and roughly 1,300 cheques — more than two applicants per unit — and booking day cleared 544 of 588 units (92.5%) at an average of S$2,546 psf, from S$1.486 million for a 2-bedder to S$3.708 million for a five-bedroom. Every two-bedroom format sold out on the day; Huttons called it the best-selling integrated development launch Tampines has seen, and it was 2026's third launch to clear 90% on opening weekend, after River Modern and the Rivelle EC next door. Buyers were, per the developer, nearly all Singaporeans and PRs, with Huttons estimating about 80% owner-occupiers.

That S$2,546 average is 7.9% above Parktown's S$2,360 launch average of February 2025 — the land gap, passed through almost exactly.

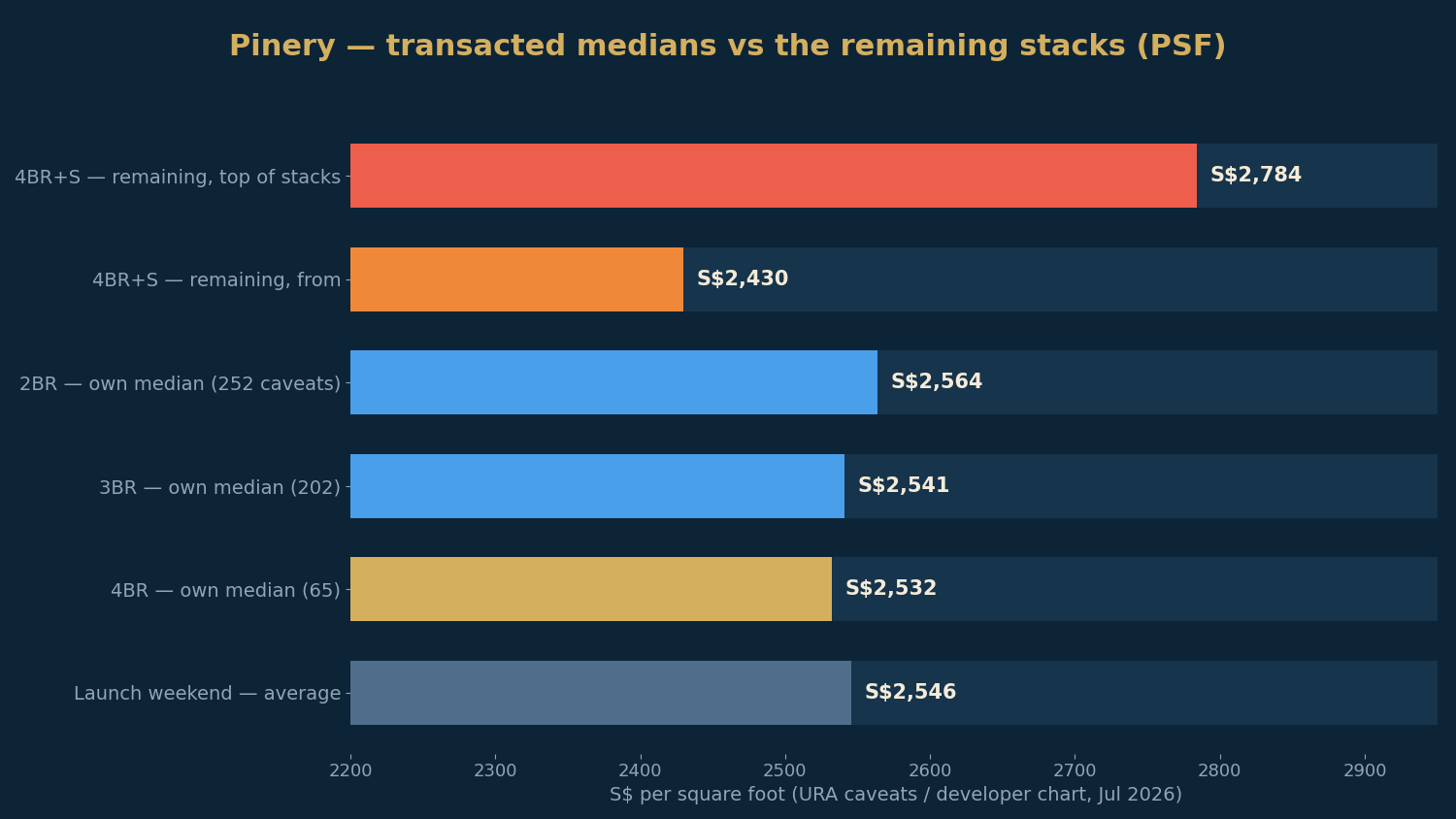

What the project has transacted at, by bedroom (URA caveats via the live scorecard, March–June 2026):

| Type | Typical size | Median PSF | Caveats |

|---|---|---|---|

| 2 Bedroom | 635 sqft | S$2,564 | 252 |

| 3 Bedroom | 990 sqft | S$2,541 | 202 |

| 4 Bedroom | 1,195 sqft | S$2,532 | 65 |

Note how flat that column is: S$2,532–2,564 across every size band. The developer priced the big units at almost no psf discount to the small ones — and the launch cleared anyway.

What's left: 34 units, all of them family-sized

Per the 14 July 2026 balance chart, the remaining 34 units are entirely four-bedroom-plus-study and five-bedroom stock: 3 of the 1,195 sqft 4BR+Study Premium (from S$2.972m, S$2,487–2,784 psf), 24 across the 1,227–1,238 sqft 4BR+Study Premium layouts (from S$3.124m, S$2,546–2,741 psf), 3 of the 1,389 sqft 4BR+Study Luxury (from S$3.375m, S$2,430–2,613 psf), and 4 of the 1,475 sqft 5BR Luxury (from S$3.579m, S$2,426 psf, topping out at S$3.904m, S$2,647 psf). Every 2- and 3-bedroom format — 456 units — is sold out.

Against the project's own record — the in-project benchmark — this tail is priced with unusual restraint. The 4BR+Study from-prices work out to S$2,430–2,546 psf against the project's S$2,532 four-bedroom median (65 caveats): the Luxury layout enters 4% below the record, the Premium layouts within ±1% of it. Only the top floors stretch to S$2,741–2,784, about 8–10% over. The five-bedders have no NPS transacted band (the 1,475 sqft layout sits outside the model's four-bedroom size range), so we benchmark them against their own launch-day from-price of S$2,378 psf: the current S$2,426 entry is 2% above it. Compare Faber Residence's tail at +6–11% over its own median or Elta's D1 stacks at +21%: like The Continuum, this shelf is asking roughly the transacted price, not a premium for being last.

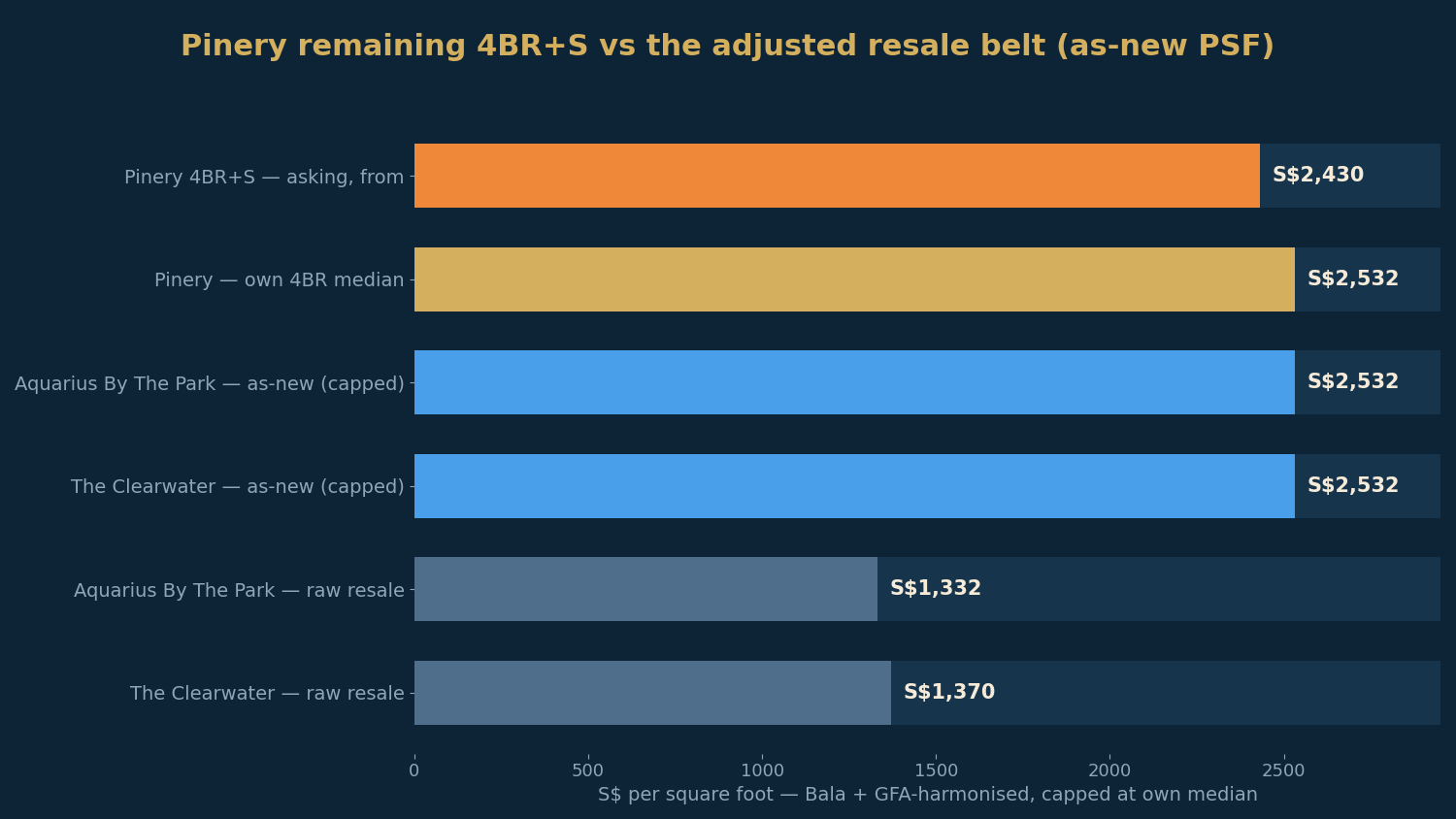

The benchmark: the resale belt across the road, adjusted honestly

Pinery's residential blocks carry Bedok Reservoir Road addresses, and its nearest resale comparables sit across the reservoir boundary in D16. Raw PSF comparisons mislead — the belt is a generation older on 99-year land — so the NPS calculator lifts each comp to a like-for-like, as-new footing: age and lease adjustment to a fresh-99 equivalent, plus +8% GFA harmonisation for these three-bedder-and-larger comparisons, since the comps pre-date the 22 January 2023 strata-area rules. Each adjusted comp is capped at the project's own median.

| Comparable | Raw resale PSF | As-new, harmonised |

|---|---|---|

| Pinery Residences · 4BR+S (remaining, from) | — | S$2,430–2,546 (asking) |

| Pinery Residences · 4BR (own median) | — | S$2,532 |

| Aquarius By The Park (99yr, 2001, 0.75km) | S$1,332 | ~S$2,532 (capped) |

| The Clearwater (99yr, 2001, 0.89km) | S$1,370 | ~S$2,532 (capped) |

| The Tapestry (99yr, 2021, Tampines St 86) | ~S$1,674 | — (context, not in comp set) |

Read plainly: the twenty-five-year-old belt across the road transacts at S$1,3xx raw — half the new price — and even lifted all the way to as-new both comps cap out at the project's own S$2,532 median. The honest statement of that table is that you are paying the full modelled as-new price for the location, with the alternative being a S$1.2–1.4m discount for a 2001 building and a 74-year lease. The uncapped arithmetic (S$2,714–2,744 as-new) says the asks are not above the adjusted belt — but nobody should pretend there is a bargain gap either. The nearest modern comp, The Tapestry (2021), last transacted around S$1,674 psf raw — the premium over it is the integrated podium, the ballot ring, and five years of land inflation.

How long you'd likely hold

Seller's stamp duty runs for four years (16%, 12%, 8%, 4%), so no exit before year four is realistic, and the shortest tier we publish is four-to-six years. Using the NPS calculator's model — 4.53% expected growth, a 3% target — here is the estimated holding period for each remaining stack, on price growth alone, against the bedroom's own transacted median as the fair-value anchor.

| Available stack | PSF | Hold (price only) |

|---|---|---|

| 4BR+S Premium 1,195 sqft — from S$2.972m | S$2,487 | 4–6 yrs |

| 4BR+S Premium 1,195 sqft — top of stack | S$2,784 | 6–10 yrs |

| 4BR+S Premium 1,227–1,238 sqft — from S$3.124m | S$2,546 | 4–6 yrs |

| 4BR+S Premium 1,227–1,238 sqft — top of stack | S$2,741 | 4–6 yrs |

| 4BR+S Luxury 1,389 sqft — from S$3.375m | S$2,430 | 4–6 yrs |

| 4BR+S Luxury 1,389 sqft — top of stack | S$2,613 | 4–6 yrs |

| 5BR Luxury 1,475 sqft — from S$3.579m | S$2,426 | 4–6 yrs |

| 5BR Luxury 1,475 sqft — top ask, S$3.904m | S$2,647 | 6–10 yrs |

With a 4.53% growth engine — the strongest we have modelled on a 2026 launch — the four-to-six-year tier stretches all the way to S$2,766 psf on the four-bedroom band (about S$3.39 million on the 1,227 sqft layout), and almost everything left is inside it. Only two reads stretch longer: the very top of the 1,195 sqft stack at S$2,784, and the highest-floor five-bedder at S$2,647 — the five-bedroom rows lean on the launch from-price rather than a transacted band (only 12 such units exist), so read them loosely. The quantum, not the psf, is the real filter: everything left costs S$2.97–3.9 million, and at that cheque the buyer is a family holding through the 2029 TOP anyway. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

Pinery Residences is what the top of the scorecard looks like: a triple-perfect location card — doorstep Downtown Line, a four-school ballot ring with Junyuan and St. Hilda's, ideal scale — on top of D18's strong rental decade and a near-maximum quality tilt that models 4.5%/yr growth. The market agreed violently: 92.5% in a weekend at a S$1,004 psf ppr land price passed through at S$2,546. What's left is a 34-unit family shelf priced at, and in places below, the project's own transacted record — on the holding model, nearly all of it a four-to-six-year read. The honest caveats are exactly two. You are paying the full as-new price in a belt where the resale alternative is half the psf — the S is a quality grade, not a discount flag. And the "integrated" here is mall-and-MRT, not Parktown's civic bundle — if you want the interchange, the hawker centre and the community club, that project graded S 8.6 and launched S$186 psf cheaper a year earlier. If you want the best card our model has ever printed and a S$3m+ four-bedder in the Junyuan ring, this is it, priced like it knows it.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade (S, 9.0), the five factor scores, modelled growth (4.53%/yr), the 3.59% modelled yield, per-bedroom transacted medians and the adjusted comparables per the TRIBE New Project Scorecard (URA Data Service transacted PSF; district resale trend — the 1km ring holds only three resale projects — lifted for project size, transport and schools; figures as at July 2026). GLS tender result (S$668.28 million / S$1,004 psf ppr, six bids, Sing Holdings second at S$985 psf ppr, awarded 10 October 2024) per EdgeProp and the HDB tender record; site and integrated-use parameters (252,989 sqft site, retail cap, childcare) per the same EdgeProp report. Launch result (544 of 588, 92.5%, average S$2,546 psf, 28–29 March 2026; 8,500 preview visitors; ~1,300 cheques; price range S$1.486–3.708 million; buyer profile) per EdgeProp via Yahoo and Stacked Homes; preview pricing from S$2,340 psf per The Business Times. The 34-unit balance, per-stack availability and current asking prices (chart dated 14 July 2026) per newlaunches.sg — agent-carried charts are unofficial and may lag caveats. Parktown Residence launch comparison per our Parktown review; Tampines/Bedok MOP supply figures (527 → 2,133 flats) per Stacked Homes. Unit mix, tenure start (99 years from 7 January 2025) and estimated TOP (Q4 2029) per PropertyReviewSG. Resale comparables age- and lease-adjusted per Bala's Table with a +8% (3BR+) GFA-harmonisation uplift, capped at the project's own median, per the NPS calculator's published methodology; The Tapestry raw median per EdgeProp's GLS coverage. Primary 1 priority distance is measured door-to-door — confirm any school-distance claim on OneMap before relying on it. Prices and availability are as reported at the dates cited and will change; scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.