Insights

Honest Insights On Faber Residence

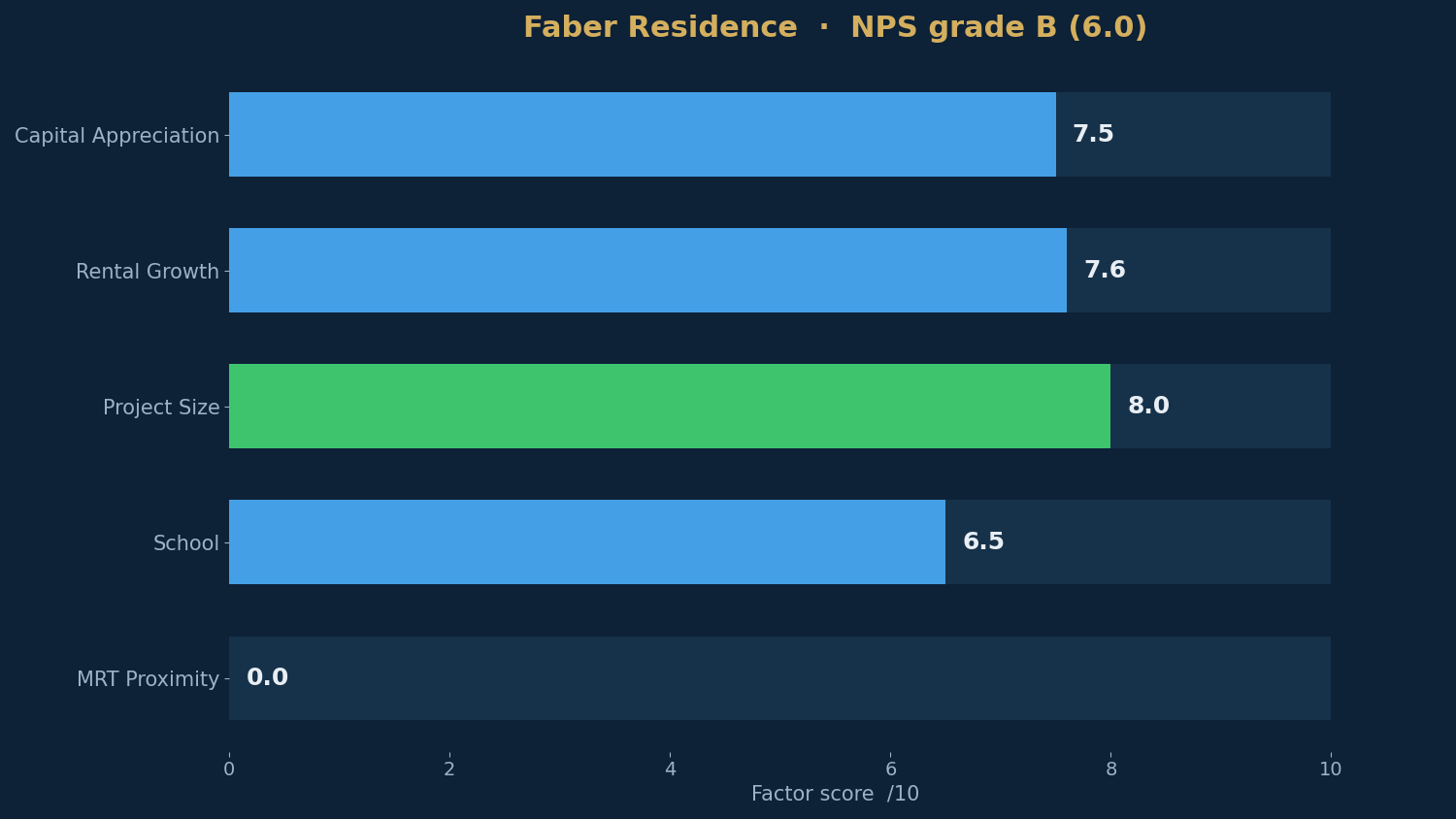

Faber Residence grades B (6.0) on the New Project Scorecard — GuocoLand and Hong Leong's 399-unit riverfront project on Faber Walk sold 86% in its October launch weekend despite scoring zero on MRT access, and is now down to its last 14 four- and five-bedders.

By TRIBE Editorial · 13 July 2026 · 12 min read

Faber Residence is a 399-unit, 99-year leasehold development on Faber Walk in District 5 — nine five-storey blocks by a GuocoLand, Hong Leong Holdings and TID joint venture, fronting Sungei Ulu Pandan in a landed enclave that had not seen a new project since 2014. It grades a B (6.0) on our New Project Scorecard (NPS), and the grade hides the most lopsided card we have reviewed this year: four factors at 6.5 or better sitting next to a zero for MRT access. The market shrugged — 344 of 399 units (86%) sold in the October 2025 launch weekend at an average of S$2,160 psf, every two- and three-bedder gone in a day. Nine months on, what is left is a 14-unit tail of four- and five-bedders priced above the project's own record. This is a look at what the B actually measures, what the river sold that the scorecard cannot see, and which of the remaining stacks still makes arithmetic sense. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted or docked for the project's own size, transport and schools, not a forecast.

The scorecard: a B with one hole in it

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| Project Size | 8.0 | 399 units — a mid-sized development |

| Rental Growth | 7.6 | District 5 rents grew ~7.1%/yr over the decade |

| Capital Appreciation | 7.5 | 1km resale grew ~3.8%/yr; docked slightly → ~3.7%/yr projected |

| School | 6.5 | Nan Hua Primary at 0.95km — heavily oversubscribed, at the edge of the ring |

| MRT Proximity | 0.0 | 1.98km walk to Clementi MRT — no station in walking distance |

The strengths are real. Capital appreciation scores 7.5: resale homes within a kilometre of Faber Walk appreciated about 3.8% a year over the past decade on a same-property basis — the West Coast condo belt across the AYE has been a quiet compounder — and the model's projection for Faber lands at ~3.7% a year, clearing the 3% bar (the project tilt here is marginally negative, one of the few on the board). Rental growth at 7.6 reflects District 5 rents compounding about 7.1% a year over the decade, fed by one-north, the NUS belt and Jurong's office base, and the project's gross yield models at 3.28%. Size scores 8.0, and schools 6.5: Nan Hua Primary — heavily oversubscribed — sits at 0.95km, inside the priority ring but close enough to its edge that any buyer banking on it should walk the door-to-door route on OneMap before relying on it.

Then the hole. MRT proximity scores 0.0 — the lowest score the model gives — because the nearest station today, Clementi on the East-West Line, is a 1.98km walk on OneMap's door-to-door routing. The marketing answer is the future Jurong Town Hall station on the Jurong Region Line, but sources put its opening anywhere from 2028 to 2030, and even then the walk is not trivial — one pre-launch review clocked it at a seven-minute drive or an eleven-minute bus ride. Faber Residence is, and will for years remain, a car-and-bus address.

The launch: what the river sold

The land market priced the hole in. The Faber Walk GLS tender closed in November 2024 with just three bids, and the winning S$349.9 million — S$900 psf ppr — was 8.9% above JBE Holdings' S$827. For context, Elta's Clementi Avenue 1 site — a 1.1km walk to Clementi MRT — had gone for a record S$1,250 psf ppr a year earlier, and 2024's Bayshore and Chuan Grove sites cleared S$1,300. At S$900, the developers bought the district's cheapest recent land and priced the launch accordingly: from S$1,995 psf, with two-bedders from S$1.28 million, three-bedders from about S$1.57 million, four-bedders from S$2.39 million and five-bedders from S$3.19 million.

The weekend of 18–19 October 2025 — the same weekend sister project Penrith sold 97% in Queenstown — Faber Residence moved 344 of 399 units (86%) at an average of S$2,160 psf, the final OCR launch of 2025. All 80 two-bedders and all 199 three-bedders sold out on day one; more than half the four- and five-bedders went with them. Buyers were overwhelmingly Singaporeans and PRs, mostly owner-occupiers — people buying a five-storey, river-fronting project in a landed estate, the first new supply in the Faber area since Waterfront @ Faber in 2014. At S$2,160 against the 2025 OCR launch average of about S$2,275 psf, it was also simply cheaper than the year's other suburban launches.

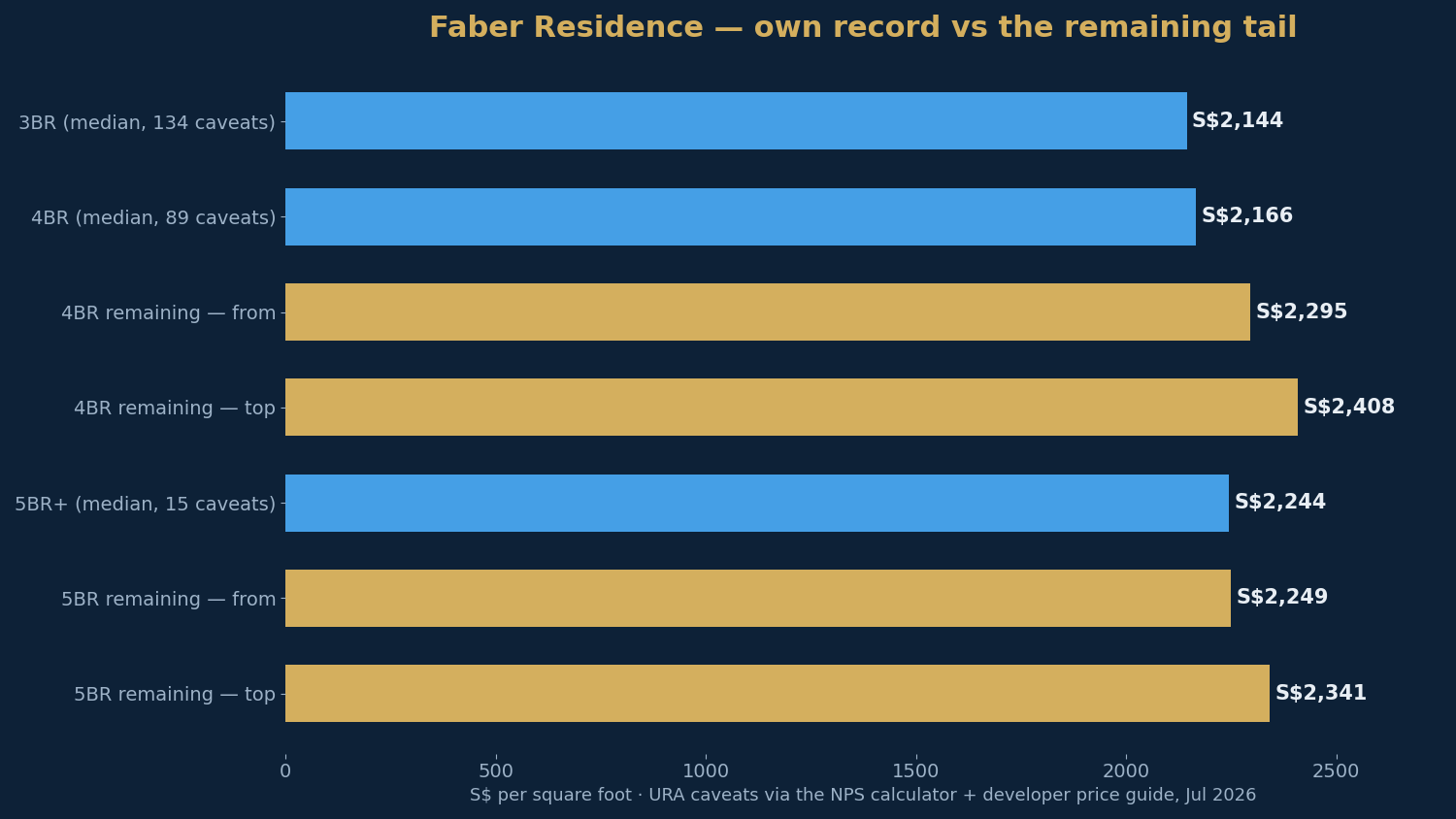

What the project has actually transacted at, by bedroom (URA caveats via the live scorecard, October 2025–June 2026):

| Type | Typical size | Median PSF | Caveats |

|---|---|---|---|

| 3 Bedroom | 861 sqft | S$2,144 | 134 |

| 4 Bedroom | 1,206 sqft | S$2,166 | 89 |

| 5 Bedroom | 1,485 sqft | S$2,244 | 15 |

What's left: a tail priced above the record

Per the developer's balance chart (12 July 2026), 384 of 399 units are sold — 96% — with 14 available (plus one unreleased): nine 1,216 sqft four-bedders at S$2.799–2.928 million (S$2,302–2,408 psf), two 1,270 sqft four-bedders at S$2.915 million (S$2,295 psf), and five 1,485 sqft five-bedders at S$3.340–3.476 million (S$2,249–2,341 psf).

Against the project's own record — the in-project benchmark — the two formats read very differently. The remaining four-bedders enter 6–11% above the project's own S$2,166 four-bedroom median (89 caveats, October 2025–June 2026). The five-bedders are the honest end of the shelf: the S$3.340 million from-price is S$2,249 psf, effectively on the project's own S$2,244 five-bedroom median, with the top of the range 4% above it.

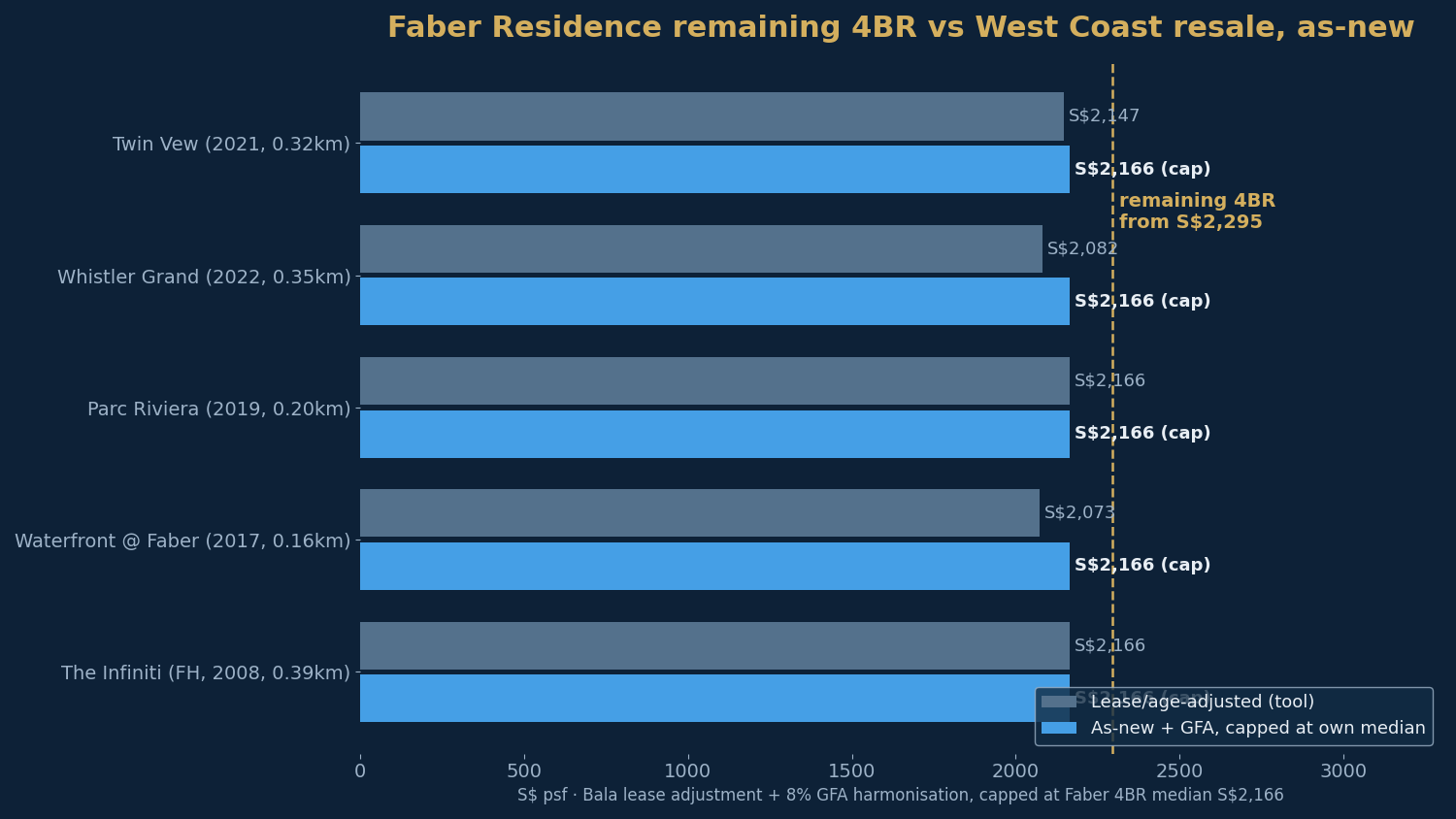

The benchmark: what the West Coast resale belt says

A raw PSF comparison against the 2017–2022 condos across the river flatters them, so we adjust each comparable to a like-for-like, as-new footing: lease decay back to a fresh 99 years on Bala's Table, and +8% GFA harmonisation for three-bedders and larger, since every comp predates the 22 January 2023 strata-area rules (their PSF is understated because their square footage still counts AC ledges and voids). The NPS calculator caps each adjusted comp at the project's own median — a deliberately conservative floor.

| Comparable | Raw resale PSF | As-new, harmonised |

|---|---|---|

| Faber Residence · 4BR (remaining) | — | S$2,295–2,408 (asking) |

| Faber Residence · 4BR (own median) | — | S$2,166 |

| Twin Vew (2021, 0.32km) | S$1,882 | ~S$2,166 (capped) |

| Whistler Grand (2022, 0.35km) | S$1,926 | ~S$2,166 (capped) |

| Parc Riviera (2019, 0.20km) | S$1,741 | ~S$2,166 (capped) |

| Waterfront @ Faber (2017, 0.16km) | S$1,548 | ~S$2,166 (capped) |

| The Infiniti (freehold, 2008, 0.39km) | S$1,672 | ~S$2,166 (capped) |

Every single comparable hits the cap: uncapped, their as-new values run S$2,239–2,772 psf, all at or above Faber's own S$2,166 median. Read plainly, that says the October launch price was fair to conservative against the estate around it on a like-for-like basis — the same defence Penrith earned, and rarer than it sounds. Both projects, incidentally, TOP around 2029, so a buyer is also paying for a wait: Twin Vew and Whistler Grand are livable today. What the adjustment does not defend is the remaining tail: at S$2,295–2,408 psf, the leftover four-bedders sit above every capped comparable and 6–11% above the project's own record.

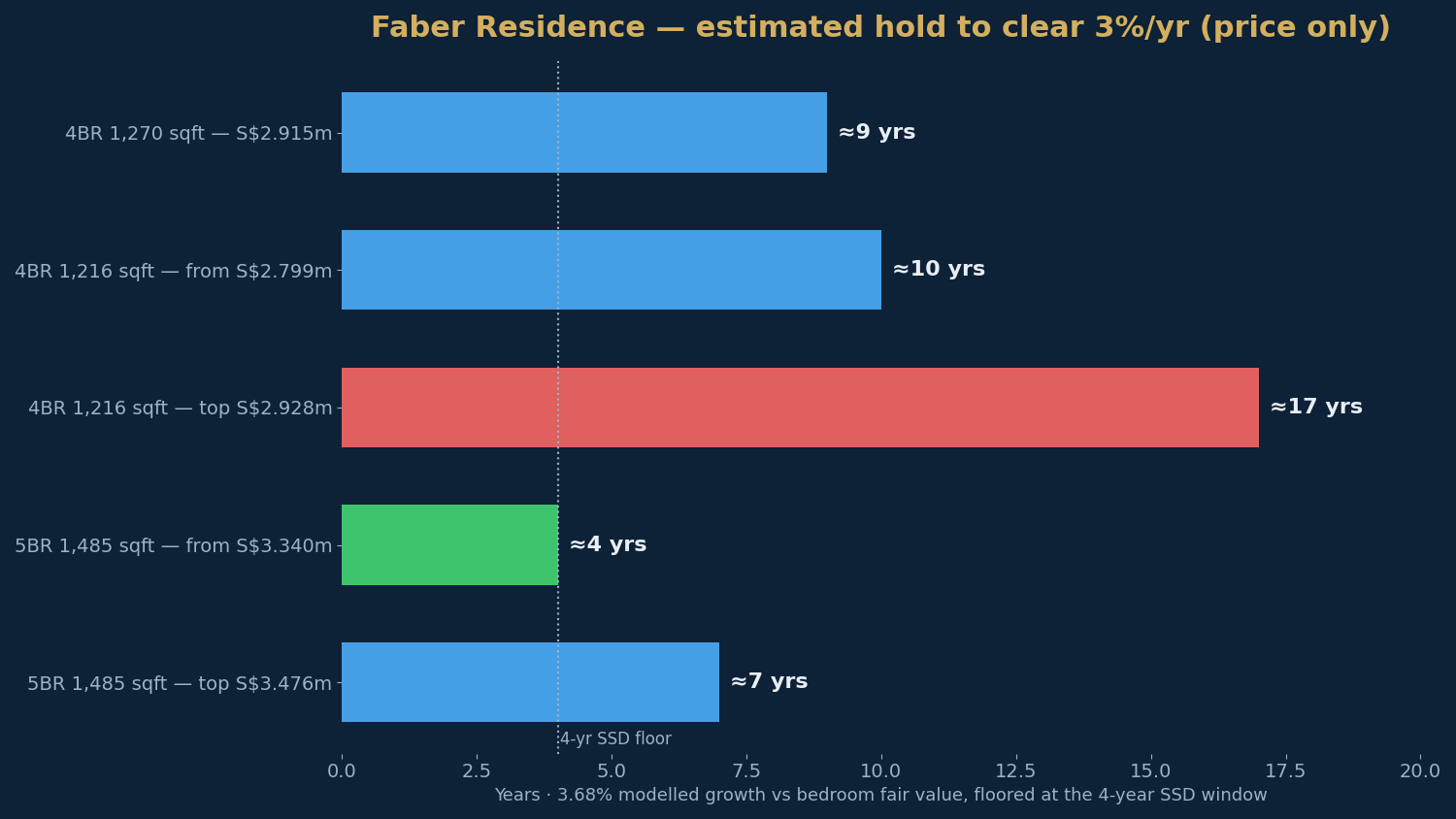

How long you'd likely hold

Seller's stamp duty runs for four years (16%, 12%, 8%, 4%), so no exit before year four is realistic, and the shortest tier we publish is four-to-six years. Using the NPS calculator's model — 3.68% expected growth, a 3% target — here is the estimated holding period for each remaining stack, on price growth alone, against each bedroom's own transacted median as the fair-value anchor.

| Available stack | PSF | Hold (price only) |

|---|---|---|

| 4BR 1,270 sqft — S$2.915m | S$2,295 | 6–10 yrs |

| 4BR 1,216 sqft — from (S$2.799m) | S$2,302 | 6–10 yrs |

| 4BR 1,216 sqft — top (S$2.928m) | S$2,408 | >10 yrs |

| 5BR 1,485 sqft — from (S$3.340m) | S$2,249 | 4–6 yrs |

| 5BR 1,485 sqft — top (S$3.476m) | S$2,341 | 6–10 yrs |

The pattern is entry-price-decisive. The five-bedroom from-price — the one stack priced on the project's own median — clears the 3% bar inside four-to-six years. The four-bedroom threshold for that tier sits at about S$2,253 psf (≈S$2.74 million at 1,216 sqft) — below the current S$2.799 million from-price — so no remaining four-bedder clears in four-to-six years; the bulk of the tail is a six-to-ten-year hold, and the top S$2,408 psf units stretch past ten. The five-bedroom four-to-six threshold is about S$2,334 psf (≈S$3.47 million), which brackets nearly the whole five-bedroom range. A 3.28% modelled yield on D5's strong rental engine carries a rented-out unit comfortably while it waits — but on a S$2.8–3.5 million family-format quantum, most buyers here will be owner-occupiers, not landlords. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

Faber Residence is a clean test of what a zero MRT score does — and does not — mean. The scorecard says transit is the worst on the board, and it is right: 1.98km to Clementi is not a walk, and the JRL rescue is years out and modest when it lands. Everything else on the card is solid: a genuine ~3.8%-a-year 1km growth record, a 7%-a-year D5 rental decade, the right project size, and an oversubscribed school at the ring's edge. The market's answer in October was that a low-rise, river-fronting project in a landed enclave at S$2,160 psf — bought on S$900 psf ppr land when neighbouring sites cleared S$1,250-plus — was cheap enough to forgive the bus ride, and the like-for-like adjustment agrees: every West Coast comparable adjusts to at or above Faber's own median. The tail is a different proposition. The remaining four-bedders ask 6–11% above the project's own record and none of them clears our four-to-six-year tier; the five-bedroom from-price, sitting exactly on the project's median, is the one honestly-priced stack left on the shelf. If the S$3.34 million quantum fits, that is the unit this article defends. If it doesn't, October's price is gone.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade (B, 6.0), the five factor scores, modelled growth (~3.7%/yr) and the 3.28% modelled yield per the TRIBE New Project Scorecard (URA Data Service transacted PSF; 1km resale trend adjusted for project size, transport and schools; figures as at July 2026). Land tender (S$349.858 million, S$900 psf ppr, three bids, JBE Holdings second at S$827 psf ppr, November 2024) per EdgeProp, "GuocoLand-led JV submits highest bid of $900 psf ppr for Faber Walk GLS site". The 18–19 October 2025 launch (344 of 399, 86%, average S$2,160 psf, all two- and three-bedders sold, final OCR launch of 2025, 2025 OCR average ~S$2,275 psf) per EdgeProp, "Faber Residence achieves 86% sales at average price of $2,160 psf". Project details, unit mix and launch price points per PLB Insights (3 October 2025) and 99.co. Remaining-stock pricing (14 available units and per-unit asks) per the developer balance chart as carried by newlaunches.sg, updated 12 July 2026; MySgProp (6 July 2026) showed 16 remaining a week earlier. Per-bedroom transacted medians (3BR S$2,144 / 4BR S$2,166 / 5BR S$2,244) per URA caveats via the NPS calculator; resale comparables (Twin Vew, Whistler Grand, Parc Riviera, Waterfront @ Faber, The Infiniti) age- and lease-adjusted per Bala's Table with a +8% (3BR+) GFA-harmonisation uplift, capped at the project's own median, per the NPS calculator's published methodology. Expected TOP is cited as Q1 2029 by newlaunches.sg while the marketing site carries a 31 December 2030 legal completion date — treat 2029 as the estimate and 2030 as the outside date. Jurong Town Hall MRT (JRL) opening dates are cited variously as 2028–2030. Primary 1 priority distance is measured door-to-door — confirm the Nan Hua distance on OneMap before relying on it. Prices and availability are as reported at the dates cited and will change; scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.