Insights

Honest Insights On Elta

Elta grades B (5.5) on the New Project Scorecard — the 501-home Clementi Avenue 1 project sold 65% at launch, has crept to 82%, and just set a S$2,907 psf record. What's left is 88 units, almost all of them the big formats.

By TRIBE Editorial · 12 July 2026 · 12 min read

Elta is a 501-unit, 99-year leasehold development on Clementi Avenue 1 in District 5 — two 39-storey towers by CSC Land Group and MCL Land, the tallest residences in Clementi, with a TOP slated for 2028. It grades a B (5.5) on our New Project Scorecard (NPS), and it is a project with two stories running at once: it sold 65% — 326 of 501 units — on its February 2025 launch weekend at an average of S$2,537 psf, then spent the next sixteen months grinding to 82% sold, and on 28 June 2026 it set a fresh project record of S$2,907 psf on a developer sale. Meanwhile, 88 units remain — and 74 of them are the large four- and five-bedroom formats. This is a look at what the B rests on, why the shelf looks the way it does, and where the honest entry points sit in a leftover stack that runs from below the project's own record to well above it. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted for the project's own size, transport and schools, not a forecast.

The scorecard: what the B actually says

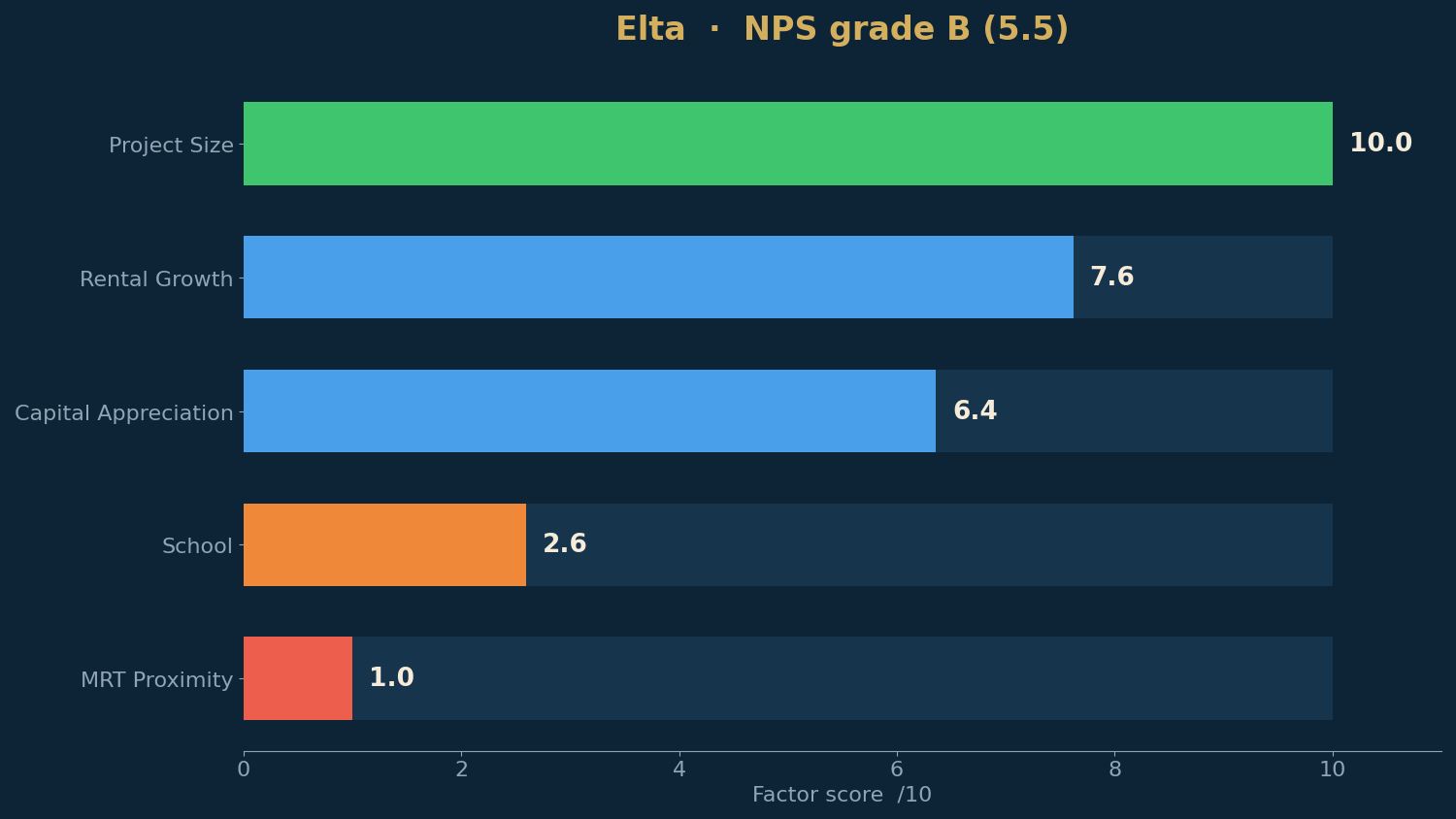

Elta's 5.5 is a barbell: perfect scale and strong rental momentum on one end, the weakest MRT score on the recent-launch board on the other.

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| Project Size | 10.0 | 501 units — ideal scale for liquidity and facilities |

| Rental Growth | 7.6 | District 5 rents grew ~7.1%/yr over the decade — strong momentum |

| Capital Appreciation | 6.4 | D5 resale grew ~3.0%/yr; lifted for the project's attributes → ~3.3%/yr |

| School | 2.6 | 2 primary schools within 1km; nearest (Pei Tong, 0.96km) undersubscribed |

| MRT Proximity | 1.0 | A 1.14km walk to Clementi MRT — the weak point |

Start with the hole, because the marketing will not. MRT scores 1.0: on OneMap's door-to-door walk, Elta is 1.14km from Clementi MRT — a real 14-to-15-minute walk, not the breezy "one stop to Jurong East" the showflat implies. Clementi Mall, the bus interchange and the MRT are a bus ride or a determined walk away. For a project that will carry Clementi's record pricing, that is the single fact a buyer should weigh most carefully, and it is the main reason a project with a 10.0 size score grades B rather than A.

The strengths are real, though. Size scores a perfect 10.0 — 501 units is the deepest liquidity pool in this review series short of a mega-project, with a full facilities deck to match. Rental growth scores 7.6: District 5 rents compounded about 7.1% a year over the decade, fed by one-north, NUS, Singapore Polytechnic and the West Coast logistics belt — Elta's projected gross yield is about 3.3%, and the tenant pool next door is structural. Capital appreciation is a 6.4: the model reads the district's resale record at roughly 3.0% a year and lifts it for Elta's scale to a projected ~3.3% a year — over the 3% bar, but only by a third of a point. That thin margin matters later. Schools score 2.6: only Pei Tong and Clementi Primary sit within a kilometre and the nearer is undersubscribed — limited ballot value in an estate otherwise famous for its school belt (Nan Hua and NUS High are just outside the ring).

The launch: a record land price meets a patient market

Elta's economics were set in November 2023, when CSC Land and MCL Land paid S$633.45 million — a then-record S$1,250 psf ppr for Clementi — against six bids, 4% above the CDL–Frasers–Sekisui consortium underneath them. That land rate made a S$2,5xx launch inevitable. The February 2025 weekend cleared 65% at an average of S$2,537 psf — a solid result, not a stampede: the two-bedders led, with almost all 179 sold at an average quantum of S$1.388 million, one-bedders averaged S$1.158 million, three-bedders S$2.198 million, and exactly one five-bedder found a buyer. The pattern was the market telling the developer something specific: the compact quantums cleared at record PSF; the big formats did not.

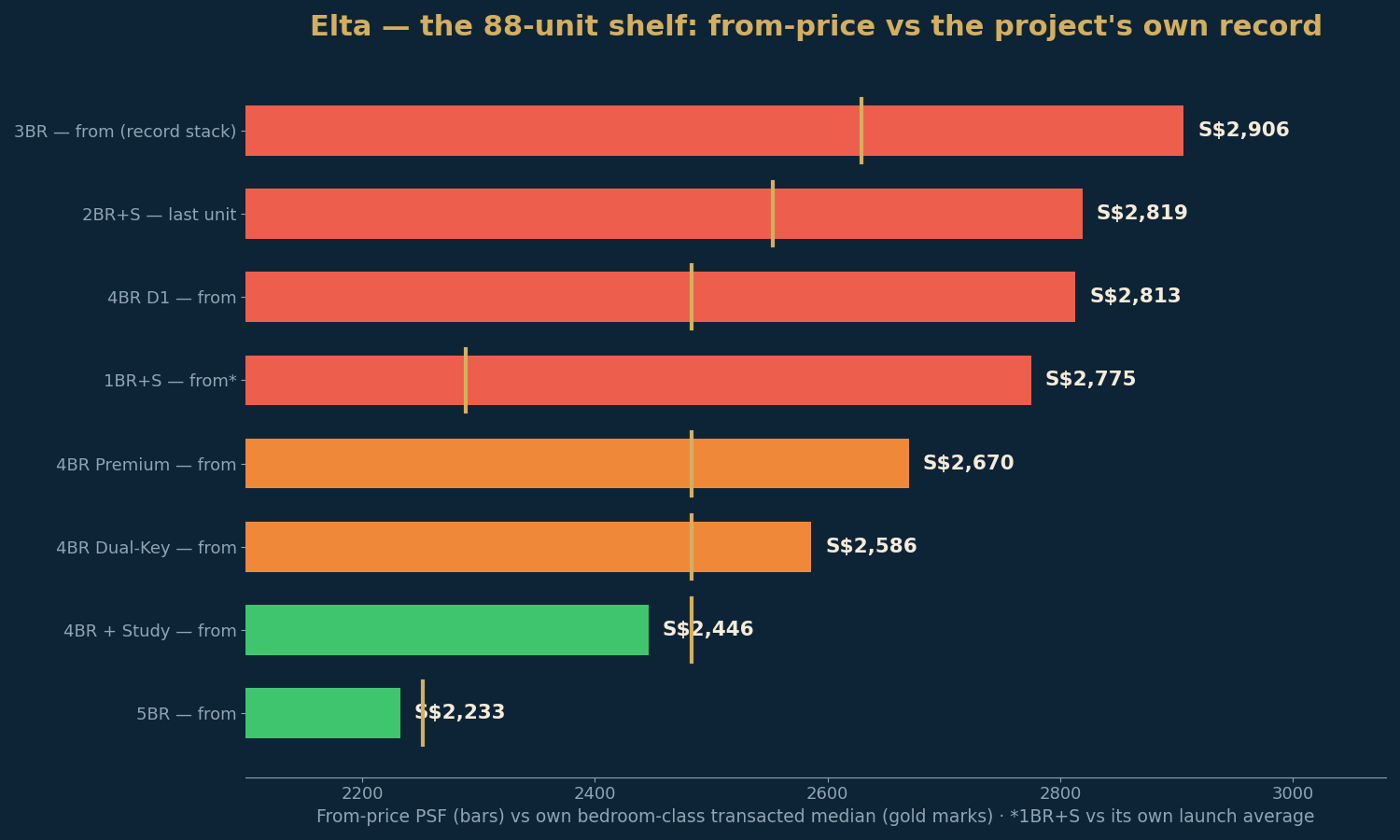

Sixteen months later the tape says the same thing. Per URA caveats as of 7 July 2026, 89 units remained unsold (82% sold); the developer's July balance chart lists 88, across eight stacks:

| What's left | Size | Units | Price from | PSF range |

|---|---|---|---|---|

| 5 Bedroom | 1,776 sqft | 26 | S$3.965m | S$2,233–2,595 |

| 4BR + Study | 1,507 sqft | 22 | S$3.686m | S$2,446–2,709 |

| 4BR Dual-Key | 1,313 sqft | 20 | S$3.396m | S$2,586–2,788 |

| 4 Bedroom | 1,184 sqft | 7 | S$3.330m | S$2,813–2,883 |

| 4BR Premium | 1,313 sqft | 6 | S$3.506m | S$2,670–2,718 |

| 1BR + Study | 506 sqft | 4 | S$1.404m | S$2,775–2,820 |

| 3 Bedroom | 926 sqft | 2 | S$2.691m | S$2,906–2,930 |

| 2BR + Study | 807 sqft | 1 | S$2.275m | S$2,819 |

Two things stand out. First, the shelf is overwhelmingly the family formats — 74 of 88 units are four- and five-bedroom types, quantums of S$3.3 million to S$4.6 million in an estate whose buyers are mostly HDB upgraders. Second, the June record was not a fluke of some penthouse: the S$2,907 psf record was a 926 sqft three-bedder sold for S$2.69 million on 28 June — exactly the stack whose last two units are now listed at S$2.691–2.713 million. The developer is not discounting the tail; it is repricing the compact formats upward while the big formats wait.

The benchmark: what the big formats are worth, adjusted

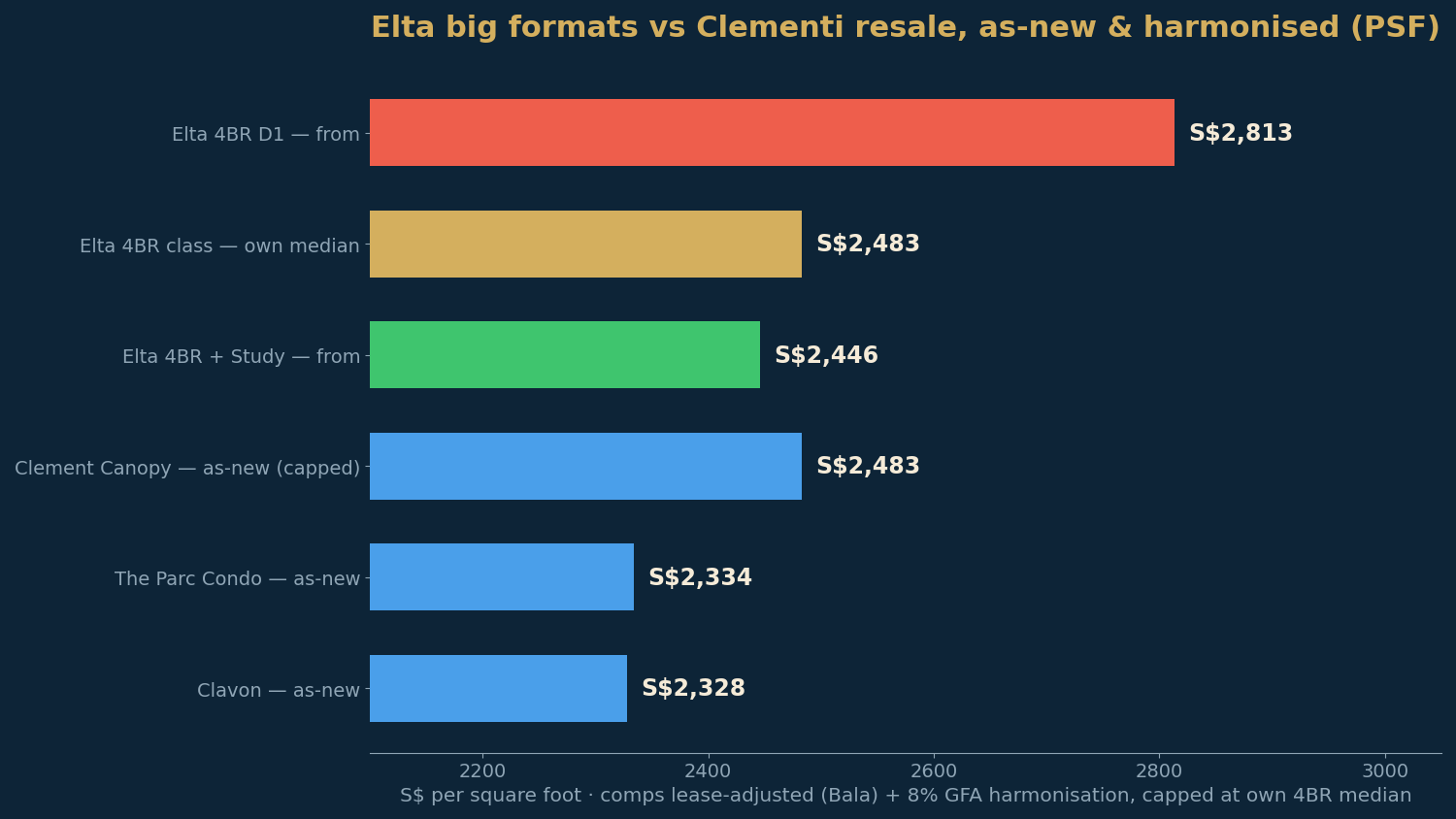

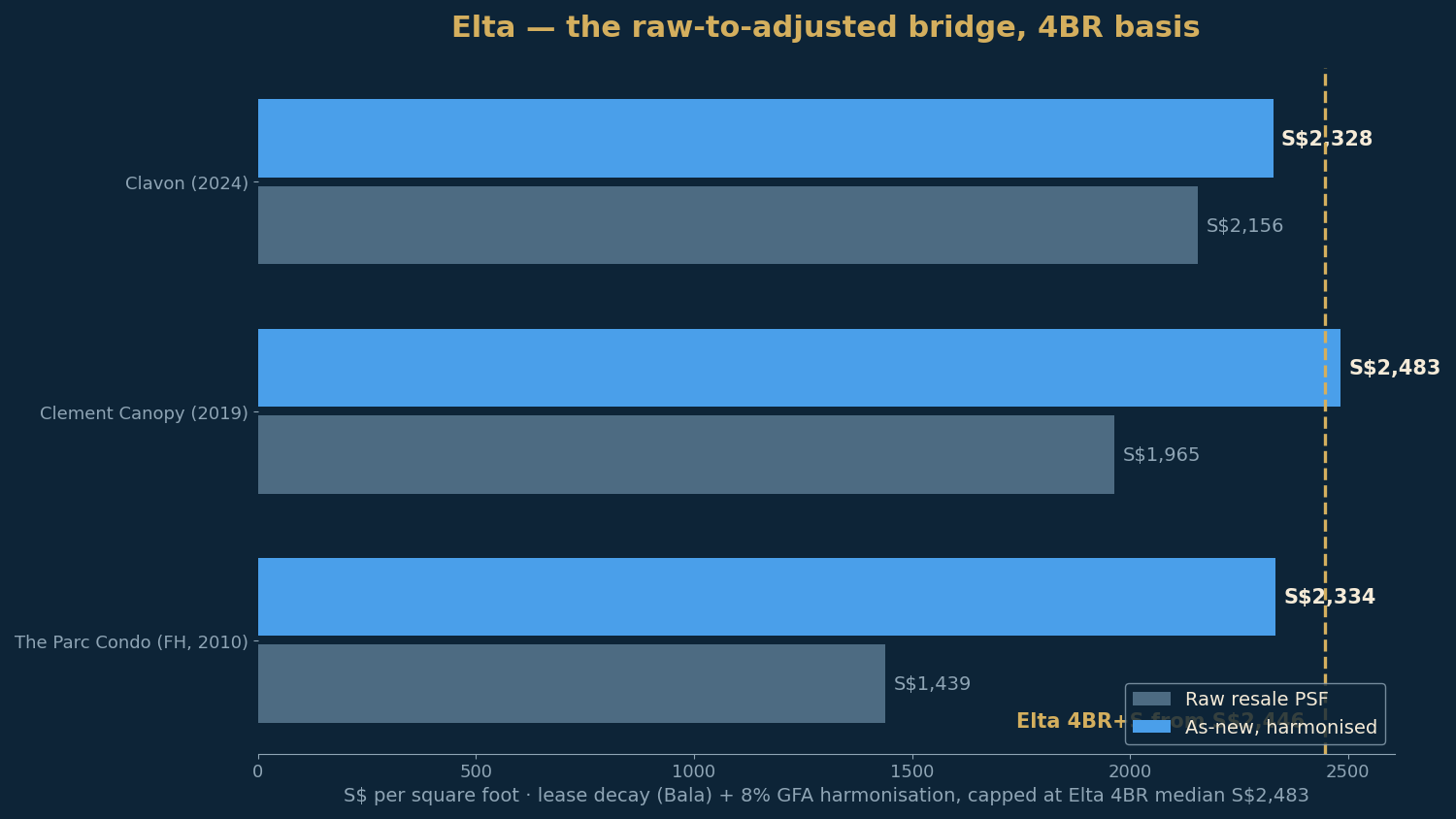

Elta's own transacted record (URA caveats via the live scorecard) prices the four-bedroom class at a S$2,483 psf median across 88 caveats, and the five-bedders at S$2,252 — meaningfully below the compact units (2BR S$2,553, 3BR S$2,629), which is normal: bigger units trade at lower PSF. The right external anchor is next door, and it has to be adjusted. Clavon (TOP 2024) and The Clement Canopy (2019) sit 0.12–0.14km away; both predate the 22 January 2023 GFA-harmonisation rules, so their strata areas still count air-conditioner ledges and voids, and their leases are two-to-seven years worn. The NPS calculator lifts each comp to a fresh-lease, as-new level and adds +8% for three-bedders and larger, capping the result at Elta's own bedroom median (a deliberately conservative floor):

| Comparable (4BR basis) | Raw recent resale | As-new, harmonised |

|---|---|---|

| Elta · 4BR+Study — from | — | S$2,446 (asking) |

| Elta · 4BR class (own median) | — | S$2,483 |

| Clavon (2024, 0.12km) | S$2,156 | ~S$2,328 |

| The Clement Canopy (2019, 0.14km) | S$1,965 | ~S$2,483 (capped) |

| The Parc Condo (FH, 2010, 0.7km) | S$1,439 | ~S$2,334 |

The read is tighter than the raw numbers suggest. Clavon — five hundred metres of walkshed better, two years old, and the natural first alternative for any Elta buyer — reprices to about S$2,328 as-new for the large formats. Elta's cheapest big-format entry, the 4BR+Study at S$2,446 psf, is about 5% above Clavon-as-new — a defensible gap for a fresh lease and a 2028 TOP. But the 4-bedroom D1 stack at S$2,813–2,883 psf is 21–24% above the same anchor, and 13% above Elta's own four-bedroom median. Same project, same month, radically different value propositions — the spread between Elta's cheapest and dearest remaining four-bedroom PSF is wider than the gap between Elta and its comps.

How long you'd likely hold

Seller's stamp duty runs for four years (16%, 12%, 8%, 4%), so no exit before year four is realistic, and the shortest tier we publish is four-to-six years. Using the NPS calculator's model — ~3.3% expected growth, a 3% target — with each bedroom class's own transacted median as the fair-value anchor, here is the estimated holding period for each remaining stack at its from-price, on price growth alone.

| Available stack | PSF | Hold (price only) |

|---|---|---|

| 5BR (from S$3.965m) | S$2,233 | 4–6 yrs |

| 4BR + Study (from S$3.686m) | S$2,446 | 4–6 yrs |

| 4BR Dual-Key (from S$3.396m) | S$2,586 | >10 yrs |

| 4BR Premium (from S$3.506m) | S$2,670 | >10 yrs |

| 4BR (from S$3.330m) | S$2,813 | Doesn't reach 3% |

| 2BR + Study (S$2.275m) | S$2,819 | >10 yrs |

| 3BR (from S$2.691m) | S$2,906 | >10 yrs |

| 1BR + Study (from S$1.404m) | S$2,775 | Doesn't reach 3%* |

The calculator has no one-bedroom caveat band for Elta; the 1BR+Study row is benchmarked against its own type's S$2,289 psf launch average — the remaining high-floor units ask 21% above it.

With growth clearing the bar by only 0.31 of a point, the model is unforgiving of premiums — this is the same pattern we flagged at Coastal Cabana, where the growth margin is thin and entry price decides everything. The two stacks that enter below the project's own transacted medians — the low-floor five-bedders (S$2,233 vs a S$2,252 median) and the low-floor 4BR+Study (S$2,446 vs a S$2,483 median) — clear in the four-to-six-year tier. Everything priced above fair value stretches brutally: the thresholds are about S$2,528 psf for the four-bedroom class and S$2,293 for the five-bedders to stay in the four-to-six-year tier, and the high floors of every stack sit far beyond them. The last compact units — the record-stack three-bedders, the lone 2BR+Study and the high-floor one-bedders — are priced 10–21% above their own medians and read more-than-ten-years to never on price alone. District 5's ~3.3% gross yield and 7%-a-year rental momentum make the big low-floor units a credible own-stay or rental hold while the price grows into itself; rent does not rescue the record-priced tail. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

Elta is a B with a barbell inside it. The scale is perfect, the D5 rental engine is real, and the project will be the newest, tallest product in an estate with structural tenant demand — but it is a 14-minute walk to the MRT, the school ring is thin, and the growth model clears the 3% bar by only a third of a point, which strips the project of any pricing forgiveness. The market has behaved accordingly for sixteen months: the compact quantums cleared and now set records; the S$3.3–4.6 million family formats sit, 74 of them, on the shelf. The honest opportunity is precisely there — the low-floor 4BR+Study from S$2,446 psf and five-bedders from S$2,233 psf enter below Elta's own transacted medians, only ~5% above Clavon adjusted as-new, and clear the model in four-to-six years with a deep rental market underneath. The honest warning is everything else: the 4BR D1 stack at S$2,813+, the record-stack three-bedders at S$2,906+, and the high-floor one-bedders at 21% over their own launch average are priced as if the growth engine were Penrith's, and it is not. Buy the bottom of the big stacks or buy elsewhere.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade (B, 5.5), the five factor scores, modelled growth and the ~3.3%/yr projected appreciation per the TRIBE New Project Scorecard (URA Data Service transacted PSF; district resale trend lifted for project size, transport and schools; figures as at July 2026). The February 2025 launch (326 of 501, 65%, average S$2,537 psf), the per-type launch averages (2BR ~S$1.388m across ~179 units; 1BR ~S$1.158m; 3BR ~S$2.198m; one 5BR) per EdgeProp and Stacked Homes, "Why This New Clementi Condo Sold 326 Units At $2,537 PSF" (March 2025). The S$2,907 psf project record (926 sqft 3BR, S$2.69m, 28 June 2026), the prior S$2,881 launch high, and the 89-units-unsold count per URA caveats as of 7 July 2026, per EdgeProp, "Developers' sale lifts Elta to new psf-price peak of $2,907" (Ashley Lo, 9 July 2026). The July 2026 balance chart (88 units across eight stacks) and per-stack from-prices and PSF ranges per the developer price list as carried by newlaunches.sg, retrieved 12 July 2026. Land rate (S$633.45 million, S$1,250 psf ppr, Clementi Avenue 1 GLS, six bids; CDL–Frasers–Sekisui second at S$1,202) per EdgeProp, "MCL Land and CSC Land JV submit highest bid of $1,250 psf ppr for Clementi Avenue 1 GLS site". Per-bedroom transacted medians (2BR S$2,553 / 3BR S$2,629 / 4BR S$2,483 / 5BR S$2,252) per URA caveats via the NPS calculator; resale comparables (Clavon, The Clement Canopy, The Parc Condo) age- and lease-adjusted per Bala's Table with a +8% (3BR+) GFA-harmonisation uplift, capped at the launch's own bedroom median, per the NPS calculator's published methodology. District 5 gross rental yield (~3.3%) estimated from URA rental and price data (Q2 2026). MRT and school distances are OneMap door-to-door walking measurements — confirm any distance claim on OneMap before relying on it. Prices and availability are as reported at the dates cited and will change; scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.