Insights

Honest Insights On Springleaf Residence

Springleaf Residence grades B (6.9) on the New Project Scorecard — GuocoLand and Hong Leong's 941-home flagship on the doorstep of Springleaf MRT, 92% sold at launch from S$2,175 psf, carried by transport and rental momentum but held back by schools.

By TRIBE Editorial · 11 July 2026 · 12 min read

Springleaf Residence is a 941-unit, 99-year leasehold development at Upper Thomson in District 26 — a large GuocoLand and Hong Leong Holdings project sitting a 0.16km, roughly two-minute walk from Springleaf MRT on the Thomson-East Coast Line. It grades a B (6.9) on our New Project Scorecard (NPS), and its launch record is one of the strongest of the past year: 870 of 941 units, about 92%, sold over its 15–16 August 2025 opening at an average of S$2,175 psf. This is a look at what the B rests on, why the market moved so fast on it, what the pricing means against the neighbours that actually compete, and where the honest caveats sit. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted for the project's own size, transport and schools, not a forecast.

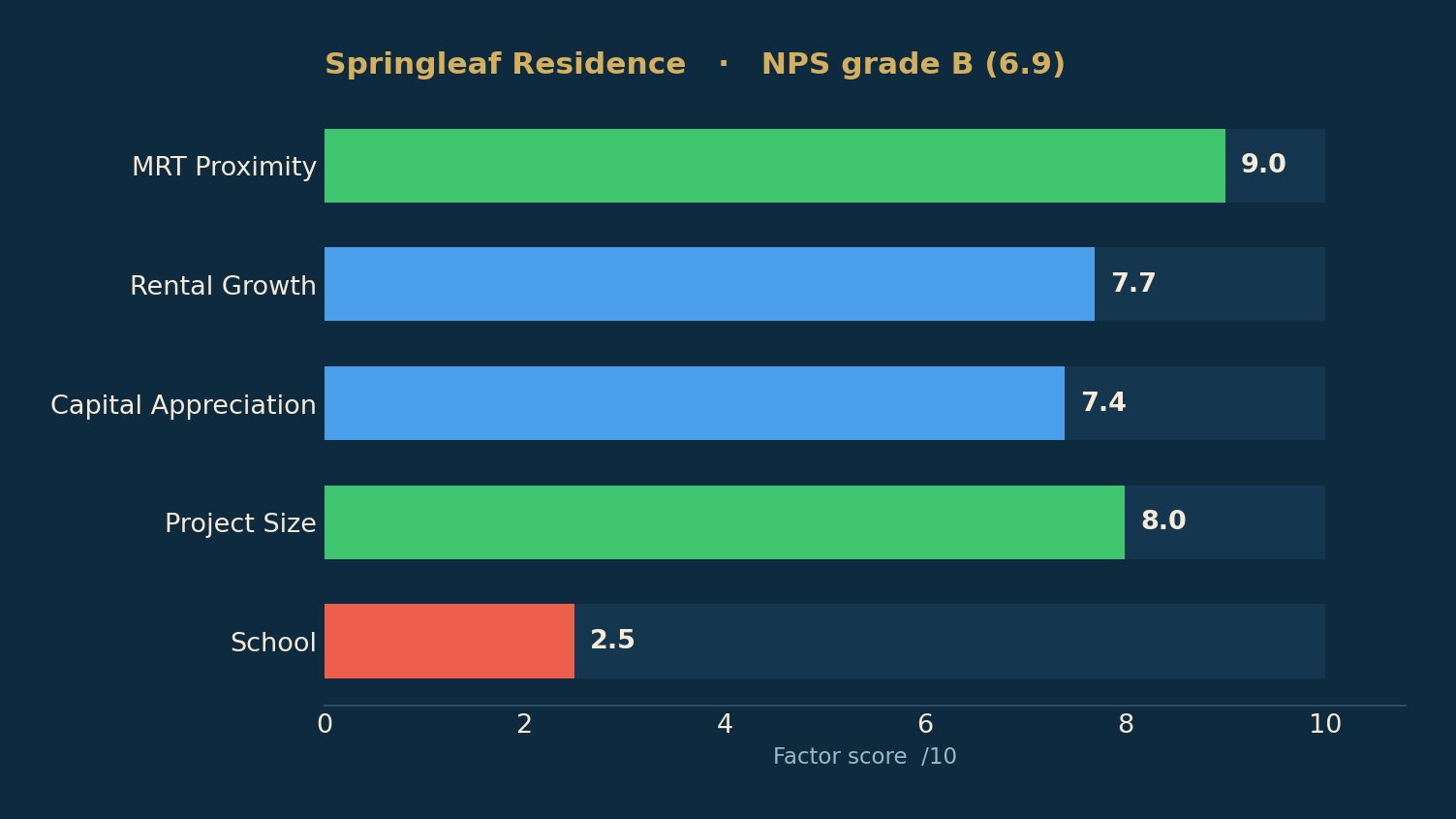

The scorecard: what a B actually says

Springleaf Residence's 6.9 is a tale of two halves — a near-perfect top of the card on transport, rental momentum and scale, and a genuine hole on schools.

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| MRT Proximity | 9.0 | A 0.16km (two-minute) walk to Springleaf MRT (Thomson-East Coast Line) |

| Project Size | 8.0 | 941 units — full facilities and a deep, liquid resale pool |

| Rental Growth | 7.7 | District 26 rents grew ~7.1%/yr over the decade — strong momentum |

| Capital Appreciation | 7.4 | 1km resale grew ~3.5%/yr; lifted for size and transport → ~3.7%/yr |

| School | 2.5 | No primary school within 1km — the clear soft spot |

The transport score is the headline. At 9.0, a two-minute walk to Springleaf MRT is about as good as an Outside Central Region address gets — one stop up the Thomson-East Coast Line brings Woodlands and the future cross-border links, and the line runs straight down to the city and the East Coast. Rental growth at 7.7 reflects a District 26 where rents compounded about 7.1% a year over the decade, among the stronger rental-momentum districts in the model, and the 941-unit scale scores 8.0 — deep enough for a full facilities deck and an active resale market once the project completes in 2029.

Capital appreciation is a solid 7.4. Resale homes within a kilometre grew about 3.5% a year over the past decade on a same-property basis, and after the model's lift for the project's size and transport, projected growth runs to roughly 3.7% a year — clear of the 3% bar, though not by the margin you see in the very top-graded launches. This is a district that has re-rated as the Thomson line opened, not one riding a single event.

The one honest hole is schools. The School factor is only 2.5 — there is no primary school inside the one-kilometre Primary 1 ballot ring. For a project pitched heavily at own-stay families, that matters, and it is the single biggest reason a project with a 9.0 for transport lands at a B rather than an A. Buyers counting on a specific school should measure the door-to-door distance on OneMap before assuming access.

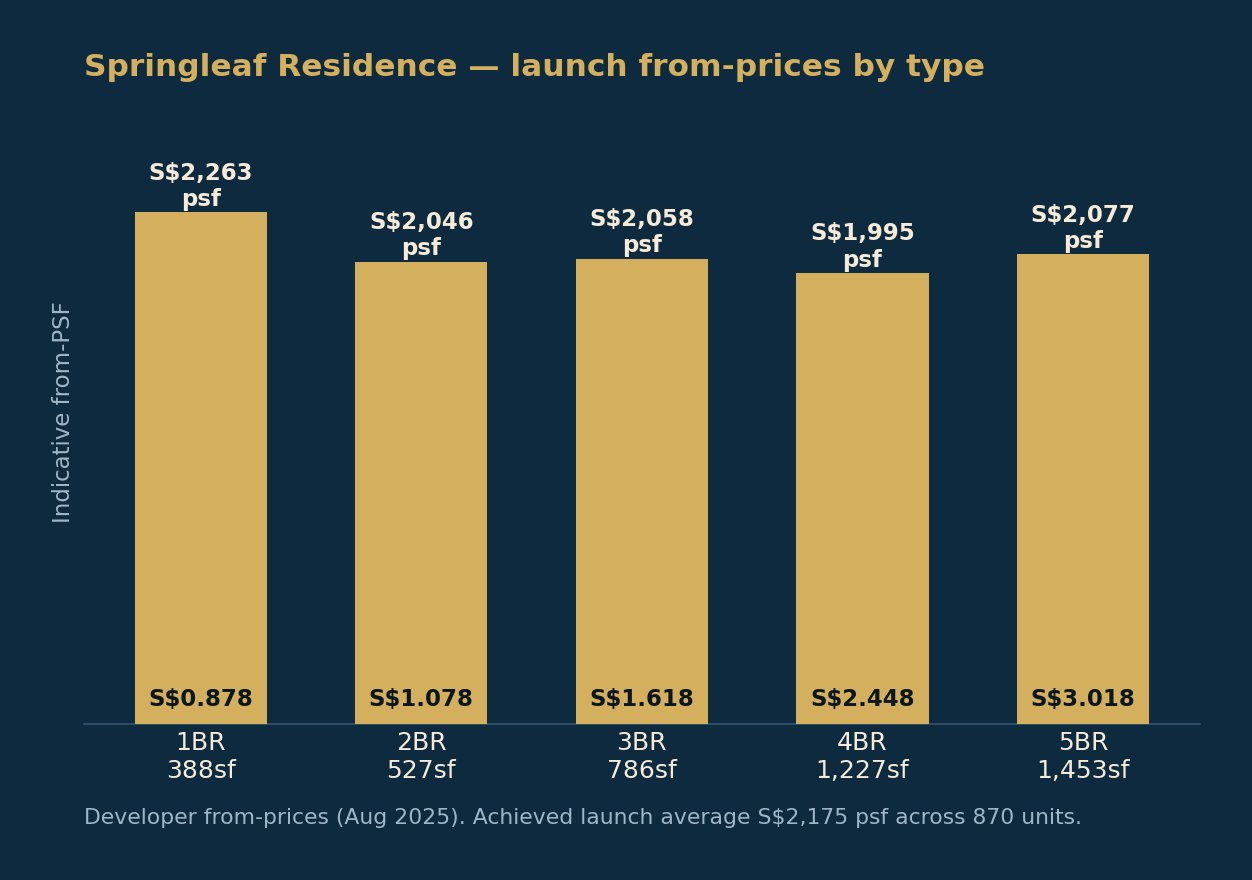

The launch: what a 92% sell-out was priced at

Springleaf Residence previewed over 1–3 August 2025 to more than 2,500 groups and booked 92% of the project on its opening weekend — a top-tier result. The developer's opening from-prices were the draw:

| Type | ~Size | Price from | PSF from |

|---|---|---|---|

| 1 Bedroom | 388 sqft | S$878,000 | S$2,263 |

| 2 Bedroom | 527 sqft | S$1.078m | S$2,046 |

| 3 Bedroom | 786 sqft | S$1.618m | S$2,058 |

| 4 Bedroom | 1,227 sqft | S$2.448m | S$1,995 |

| 5 Bedroom | 1,453 sqft | S$3.018m | S$2,077 |

Those are the best-value stacks; the average actually achieved across the 870 units sold was S$2,175 psf, as higher floors and better-facing stacks transacted up from the from-prices. What made the quantum land was harmonisation as much as headline PSF: this is a post-2023, GFA-harmonised project, so the quoted areas exclude air-conditioner ledges and void space — a genuinely usable 2-bedroom at S$1.078 million in 2025, when the typical new-launch 2-bedder had drifted toward S$1.8 million, is a real entry point. There is also a distinctive conservation block — the low-rise former Upper Thomson Secondary School building, preserved and folded into the development with 32 units, including sixteen three-bedders from about S$2.3 million.

By the project's own record, this is a near-sell-out. Almost a year on, the remaining stock is the larger and rarer stacks — the five-bedders (of which fewer than half sold at launch), a handful of four-bedders, and conservation-block units — and the largest of them have been transacting at S$2,162 psf (November 2025) up to S$2,366 psf (January 2026), at or a little above the project's own S$2,175 launch average. In other words, the cheap early stock is gone; what is left prices in line with, or slightly above, where the project itself has traded.

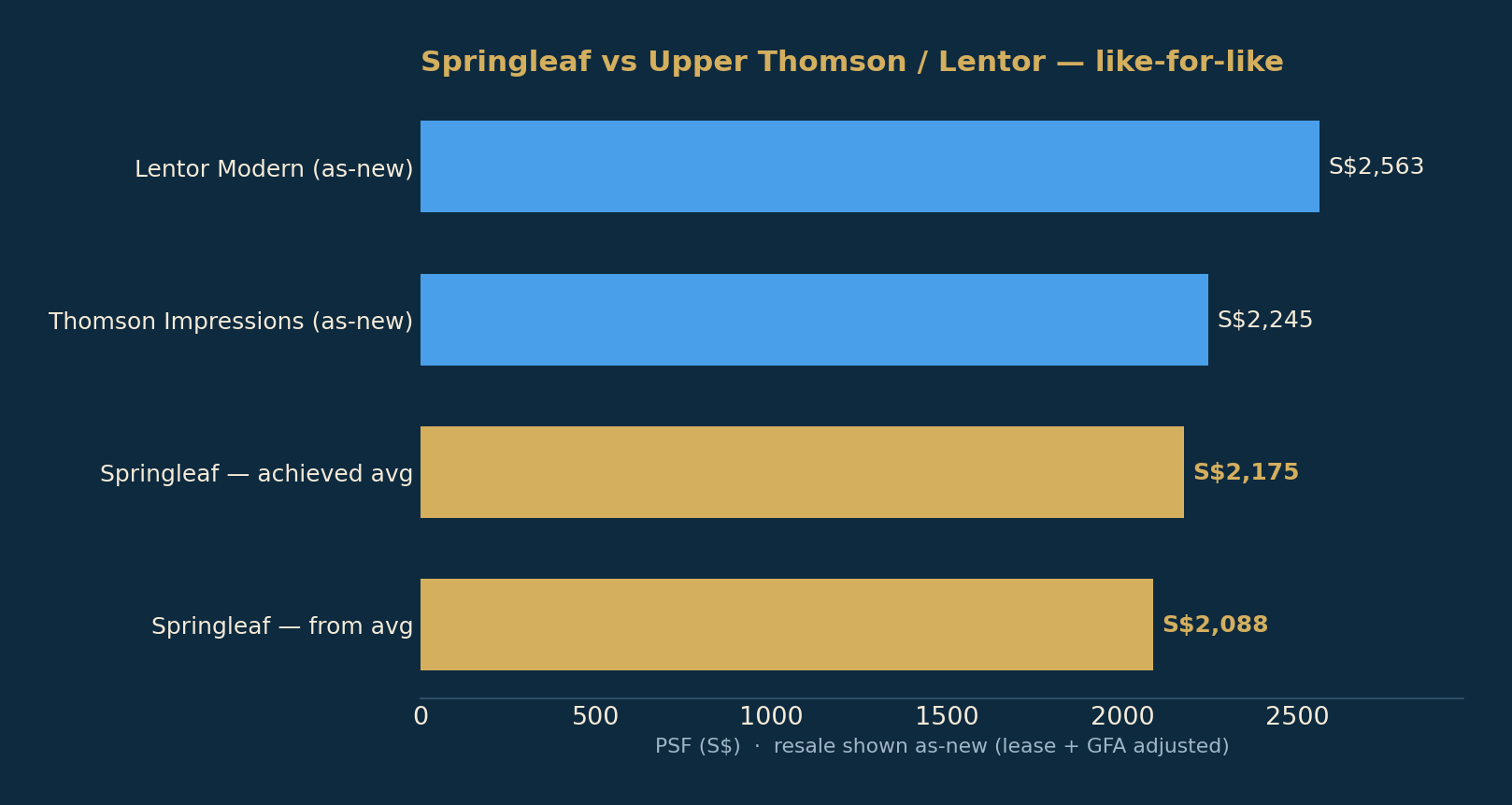

The benchmark: the neighbours, adjusted properly

The lazy comparison sets Springleaf's new-launch PSF against the raw resale PSF of older Upper Thomson and Lentor condos and calls it expensive. Do the arithmetic properly and the opposite is true. Two adjustments are needed to bring an older leasehold resale to a like-for-like, as-new footing:

- Lease decay. An older 99-year lease has fewer years left, so its PSF must be lifted to a fresh-99 equivalent on Bala's Table.

- GFA harmonisation. Resale projects whose planning approval predates 22 January 2023 still count air-conditioner ledges and void space in their strata area, so the same apartment shows more square feet and a lower PSF than a harmonised new launch. To compare like-for-like, the NPS calculator lifts a non-harmonised comp's as-new PSF by +6% for one- and two-bedders and +8% for three-bedders and larger.

Run both on the two nearest reference points — Thomson Impressions (99-year, completed 2018, the closest same-district resale) and Lentor Modern (99-year, completed 2025, the adjacent Lentor benchmark):

| Comparable | Basis | PSF |

|---|---|---|

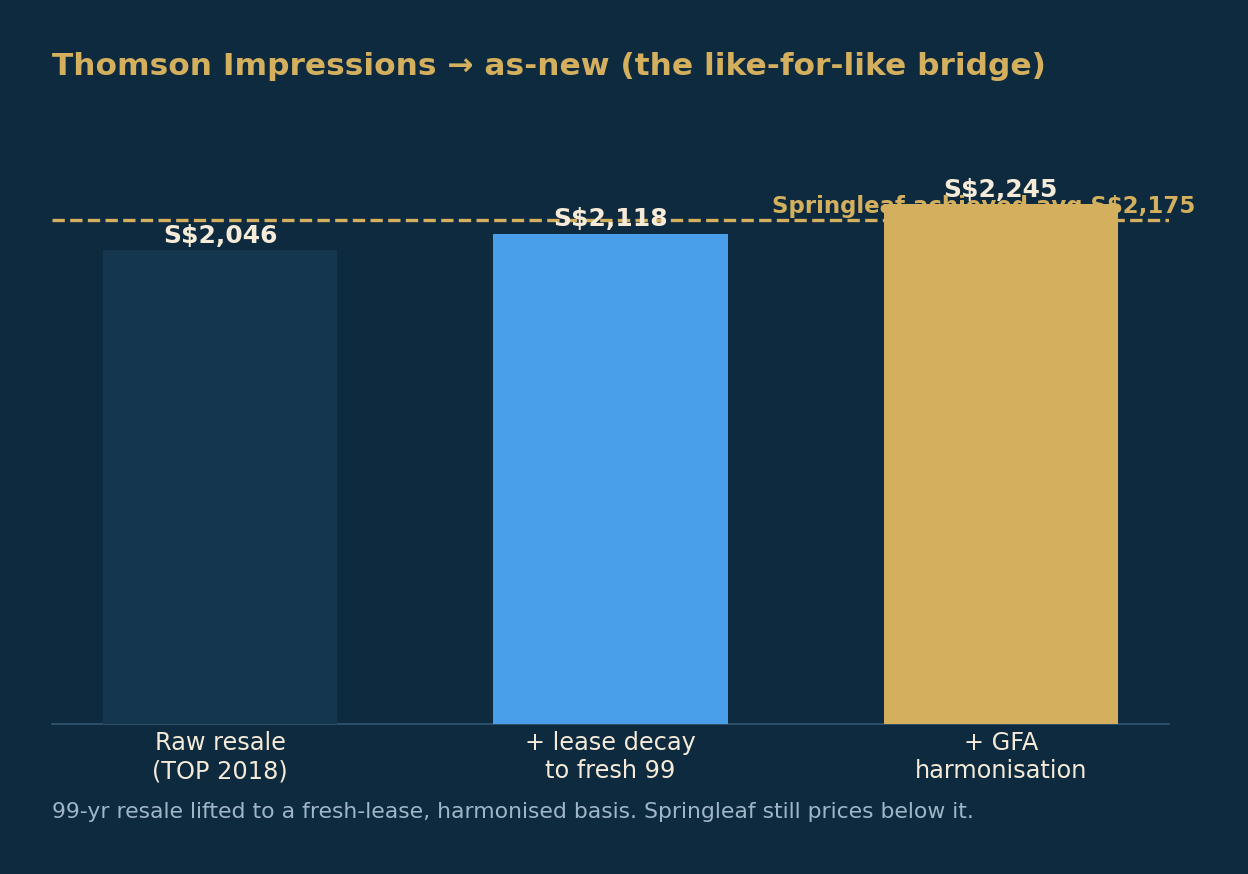

| Thomson Impressions | Raw resale (last 12 months) | S$2,046 |

| Thomson Impressions | + lease decay to fresh 99 | S$2,118 |

| Thomson Impressions | + GFA harmonisation (as-new) | S$2,245 |

| Lentor Modern | Raw subsale (2025–26) | S$2,382 |

| Lentor Modern | As-new (lease + harmonisation) | S$2,563 |

| Springleaf Residence | Achieved launch average | S$2,175 |

| Springleaf Residence | From-price average | S$2,088 |

That reframes it. Against an eight-year-old neighbour on the same stretch, Springleaf's S$2,175 average sits below an as-new Thomson Impressions (~S$2,245) — the buyer gets a brand-new building, a fresh 99-year lease and an MRT on the doorstep for less per square foot than the adjusted older block. Against Lentor Modern, the newer benchmark a few minutes north, the gap is wider still: an as-new Lentor Modern reads about S$2,563, roughly 18% above where Springleaf launched.

The honest counterweight: Thomson Impressions' raw PSF is S$2,046, so the buyer who ignores the adjustments will always be able to say Springleaf "cost more than resale." That is the point of publishing the method. On a genuine like-for-like basis, Springleaf launched at or below its adjusted neighbours — which is a large part of why 92% of it cleared in a weekend.

The location question: nature first, schools last

Springleaf's pitch is not a mall or an office node — it is the greenery. The development sits between the Central Catchment Nature Reserve, Springleaf Nature Park and Thomson Nature Park, on the low-density, landed-flavoured fringe of Upper Thomson, with the Springleaf and Upper Thomson food belts a short walk away. The Thomson-East Coast Line, fully open, is what converts that lifestyle setting into an investment case: a two-minute walk to the MRT is what lets a nature-first address also score a 9.0 on transport and a 7.1%-a-year rental record.

Two honest counterweights sit against the greenery. The first is the school gap already noted — this is not a catchment address, and families who need one should look elsewhere in the district. The second is that the nature-reserve setting caps density and height, so this is a mid-rise, lifestyle-led project, not a high-rise city-view one — a feature for its buyers, but a reason the resale pool will skew toward own-stay demand rather than pure investors. The URA Master Plan does earmark further housing along Upper Thomson Road, so competing new supply will arrive over time; first-mover pricing on the MRT is the advantage, and that supply is the price.

How long you'd likely hold

Seller's stamp duty runs for four years (16%, 12%, 8%, 4%), so no exit before year four is realistic, and the shortest tier we publish is four-to-six years. Using the NPS calculator's model — ~3.7% expected growth, a 3% target — and taking Springleaf's own S$2,175 launch average as the fair-value anchor, here is the estimated holding period for the representative remaining stacks, on price growth alone.

| Available stack | PSF | Hold (price only) |

|---|---|---|

| 3 Bedroom (conservation block) | S$2,058 | 4–6 yrs |

| 4 Bedroom · 1,227 sqft | S$1,995 | 4–6 yrs |

| 5 Bedroom · 1,453 sqft | S$2,077 | 4–6 yrs |

Because the modelled ~3.7% growth clears the 3% bar, and because the remaining larger stacks enter at or a little below the project's own S$2,175 average, every representative format clears in the same four-to-six-year tier. There is no stranded stack here — the near-sell-out did the work of clearing the marginal stock, and what is left is priced in line with the project's own record rather than at a stretch above it. Rent is a modest help rather than the story: District 26 gross yields sit near 3.4%, so the return here is a capital-appreciation-and-transport story, carried by the 3.7% growth read, not a cash-flow one. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

Springleaf Residence is what a strong B looks like: a genuinely excellent top of the card — a two-minute walk to the MRT, a 7.1%-a-year rental record, a 941-unit scale — pulled down to 6.9 by one real weakness, the absence of a primary school inside the ballot ring. The pricing is the part the market already voted on: at S$2,175 achieved, it launched below an as-new Thomson Impressions and well below an as-new Lentor Modern, and 92% of it sold in a weekend. What is left is the larger, rarer stock at or slightly above the project's own average, and on the model's ~3.7% growth every representative stack clears in the four-to-six-year window. The caveats are equally clear: this is a lifestyle-and-transport address, not a school-catchment one; the nature setting caps it at mid-rise; and Upper Thomson will see further supply over time. For an own-stay buyer or an investor who wants the line, the greenery and a fresh lease — and who does not need the school — Springleaf Residence is a credible B, and the launch numbers show the market agreed.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade (B, 6.9), the five factor scores, modelled growth and the ~3.7%/yr projected appreciation per the TRIBE New Project Scorecard (URA Data Service transacted PSF; 1km resale trend lifted for project size, transport and schools; figures as at July 2026). Land rate (S$779.6 million, S$905 psf ppr, April 2024 GLS on the 344,700 sq ft Springleaf site), the 1–3 August 2025 preview to 2,500+ groups, the 15–16 August 2025 launch and the 92% (870 of 941) take-up at an average of S$2,175 psf per EdgeProp / The Edge Singapore, "GuocoLand sells 92% of units at Springleaf Residence, with an average price of S$2,175 psf", and GuocoLand's launch releases. Per-bedroom from-prices (1BR from S$878,000/S$2,263 psf; 2BR from S$1.078m/S$2,046 psf; 3BR from S$1.618m/S$2,058 psf; 4BR from S$2.448m/S$1,995 psf; 5BR from S$3.018m/S$2,077 psf), the conservation-block detail and remaining-stock composition per Stacked Homes and developer price lists; large-format resale of S$2,162 psf (Nov 2025) to S$2,366 psf (Jan 2026) per URA caveats. Thomson Impressions (99-year, TOP 2018) 12-month resale median ~S$2,046 psf and Lentor Modern (99-year, TOP 2025) 2025–26 subsale average ~S$2,382 psf per EdgeProp / PropertyGuru / SRX transaction data; lease-decay adjustment per Bala's Table and GFA-harmonisation uplift of +6% (1–2BR) / +8% (3BR+) per the NPS calculator's published methodology. District 26 gross rental yield (~3.4%) estimated from URA rental and price data (Q2 2026). Primary 1 priority distance is measured door-to-door — confirm any school-distance claim on OneMap before relying on it. Prices and take-up are as reported at the dates cited and will change; scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.