Insights

Honest Insights On Norwood Grand

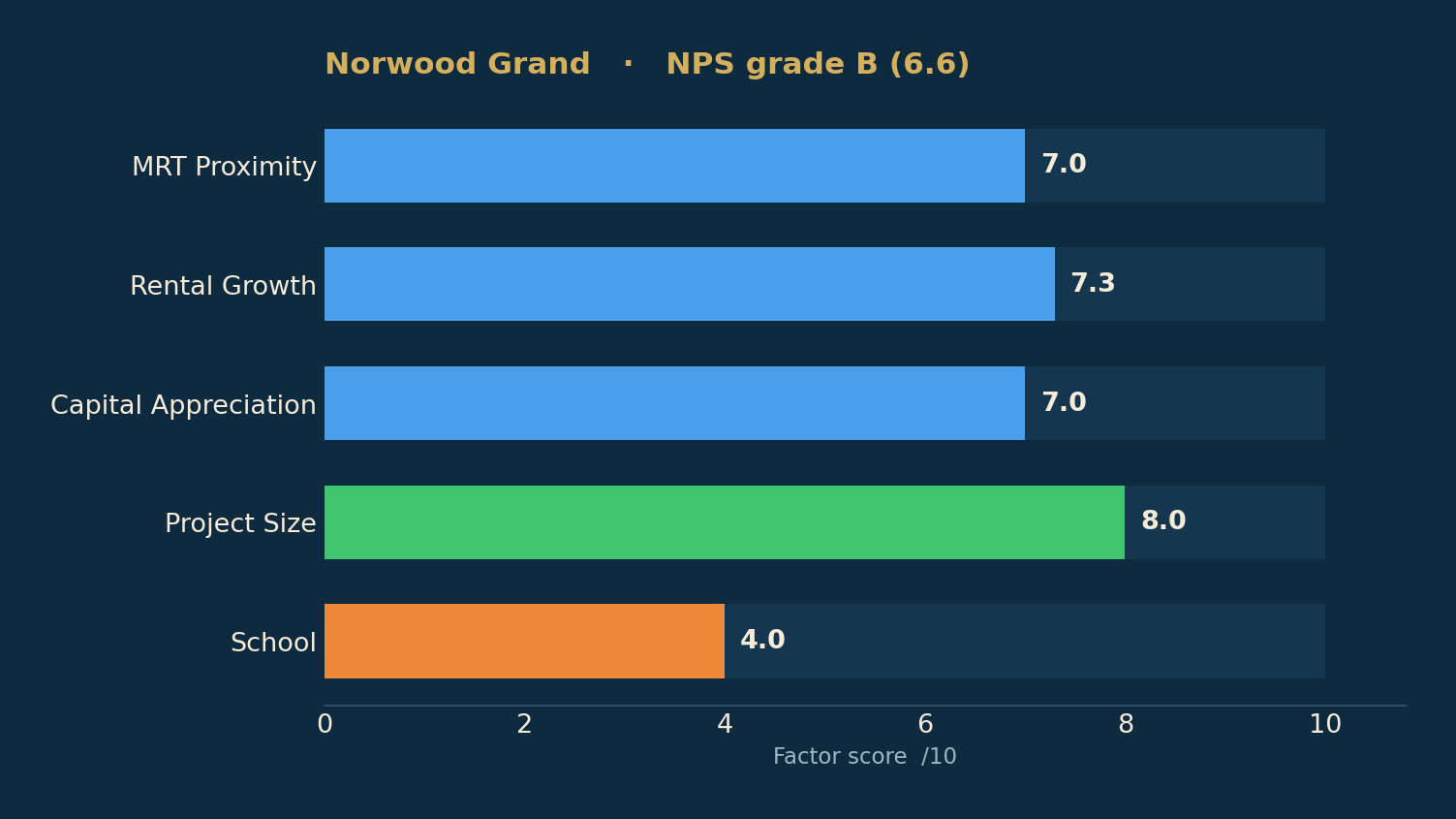

Norwood Grand grades B (6.6) on the New Project Scorecard — CDL's 348-home project on Champions Way, the first private condominium in Woodlands in over a decade, best-selling launch of 2024 at S$2,067 psf, now down to its four-bedroom tail.

By TRIBE Editorial · 11 July 2026 · 12 min read

Norwood Grand is a 348-unit, 99-year leasehold development on Champions Way in Woodlands, District 25 — a CDL project a 0.49km, four-minute walk from Woodlands South MRT on the Thomson-East Coast Line, and the first private condominium launched in Woodlands in over a decade. It grades a B (6.6) on our New Project Scorecard (NPS), and it owns a genuine record: 292 of 348 units, about 84%, sold on its 19–20 October 2024 opening weekend at an average of S$2,067 psf — the best-selling private launch of 2024, and a new price benchmark for the estate. This is a look at what the B rests on, what a Woodlands-record price means once the resale comps are adjusted honestly, and what the tail of large units still on sale is really worth. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted for the project's own size, transport and schools, not a forecast.

The scorecard: what a B actually says

Norwood Grand's 6.6 is carried by rental momentum, project scale and good-but-not-perfect transport, with schools the drag.

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| Rental Growth | 7.3 | District 25 rents grew ~6.9%/yr over the decade — strong momentum |

| Project Size | 8.0 | 348 units — a well-sized development for facilities and liquidity |

| Capital Appreciation | 7.0 | 1km resale grew ~3.0%/yr; lifted for size, transport, schools → ~3.5%/yr |

| MRT Proximity | 7.0 | A 0.49km (four-minute) walk to Woodlands South MRT (TEL) |

| School | 4.0 | 5 primary schools within 1km, but the nearest are undersubscribed — limited appeal |

The strength is income and scale. Rental growth at 7.3 reflects a District 25 where rents compounded about 6.9% a year over the decade — the Woodlands rental base is deep, anchored by the checkpoint, the industrial and business parks, and cross-border workers — and the 348-unit size scores 8.0, enough for a proper facilities deck without the resale glut of a mega-project. Transport is a solid 7.0: at four minutes to Woodlands South MRT, this is the Woodlands condo closest to a station, one stop from the Woodlands integrated hub where the Thomson-East Coast and North-South lines meet.

Capital appreciation is a respectable 7.0. Resale homes within a kilometre grew about 3.0% a year over the past decade on a same-property basis — and here the model's quality lift is doing real work: after adjusting for Norwood Grand's size, MRT access and school count, projected growth rises to roughly 3.5% a year, clear of the 3% bar. In other words, the base district record is only average, but the project's own attributes push the read over the line.

The drag is schools. The School factor is 4.0 — there are five primary schools within a kilometre, but the nearest, Innova Primary at 0.05km, is undersubscribed, so the ballot-value premium a hot school would bring is not there. It is not the empty ring some suburban launches face, but it is not a catchment selling point either.

The launch: a Woodlands record, and why it cleared

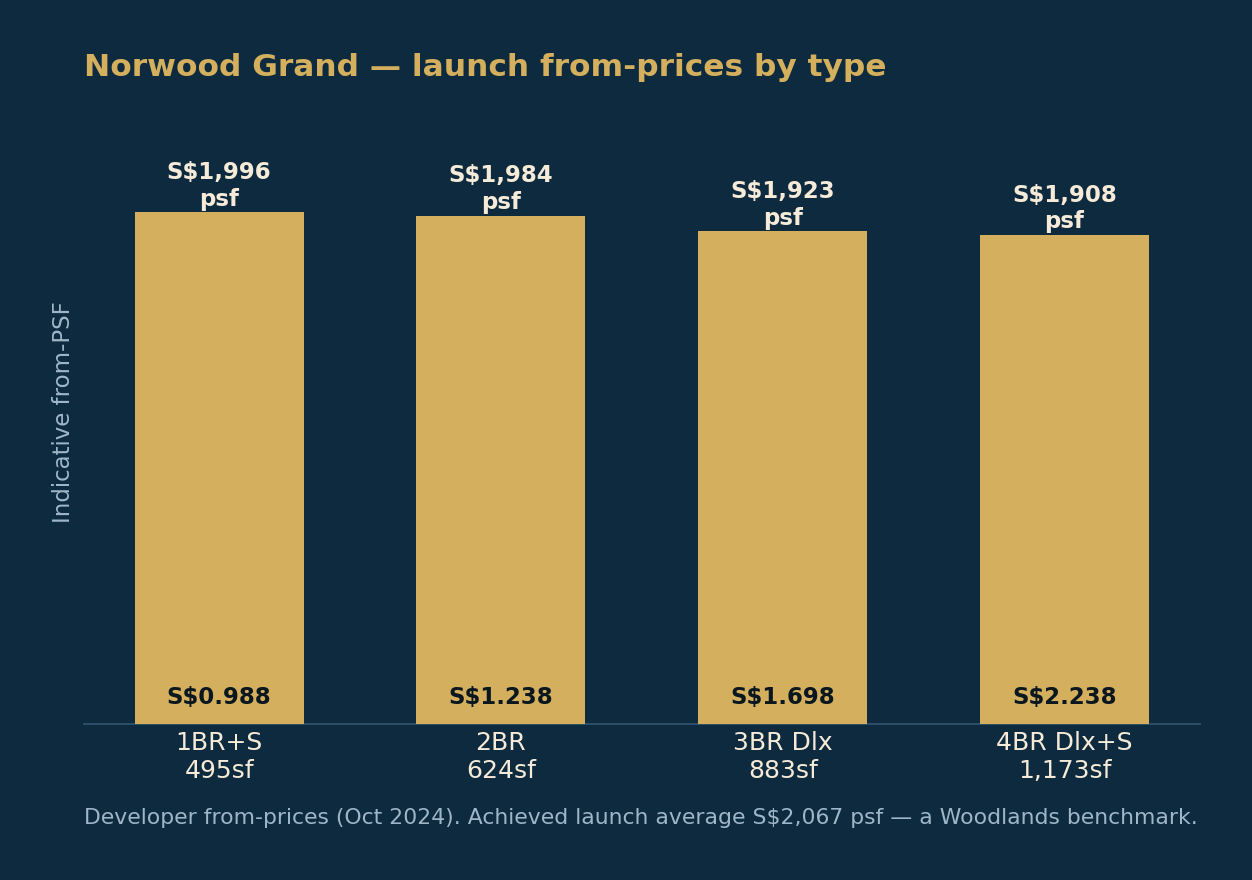

Norwood Grand was 2.8 times oversubscribed — CDL took 959 cheques ahead of a 348-unit project — and converted that into an 84% weekend at an average of S$2,067 psf, a number no Woodlands project had reached before. The from-prices show why HDB upgraders, who made up much of the crowd, moved:

| Type | ~Size | Price from | PSF from |

|---|---|---|---|

| 1 Bedroom + Study | 495 sqft | S$988,000 | S$1,996 |

| 2 Bedroom | 624 sqft | S$1.238m | S$1,984 |

| 3 Bedroom Deluxe | 883 sqft | S$1.698m | S$1,923 |

| 4 Bedroom Deluxe + Study | 1,173 sqft | S$2.238m | S$1,908 |

Most of the project sold at the "sweet spot" of S$2 million or below — a two-bedroom from S$1.238 million and a three-bedroom from S$1.698 million in an estate where four-room HDB flats were changing hands above S$700,000. Every one-, two- and three-bedroom and the four-bedroom deluxe stacks were snapped up at launch; the 56 units left over were the largest layout, the four-bedroom premium with study. Almost a year on, that tail is still the story: roughly 49 four-bedroom premium-plus-study units remain, sized about 1,313 sqft, priced from S$2.616 million to S$2.786 million, or S$1,983 to S$2,122 psf — at, and above, the project's own S$2,067 launch average.

By the project's own record, then, the leftover stock is not a discount rack. It is the priciest, largest format, and the top of that range sits above where the project itself has traded.

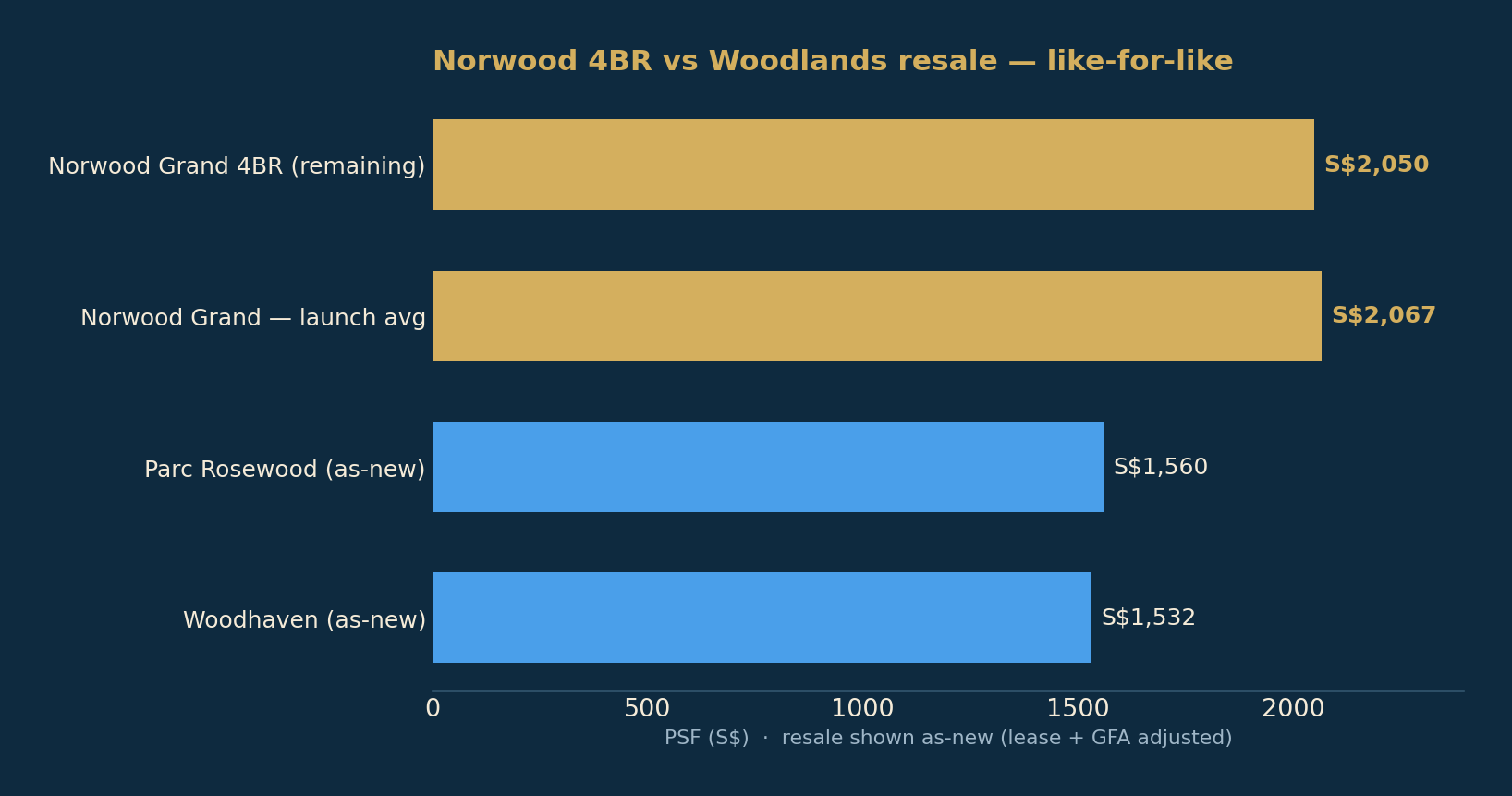

The benchmark: what a Woodlands record is worth, adjusted

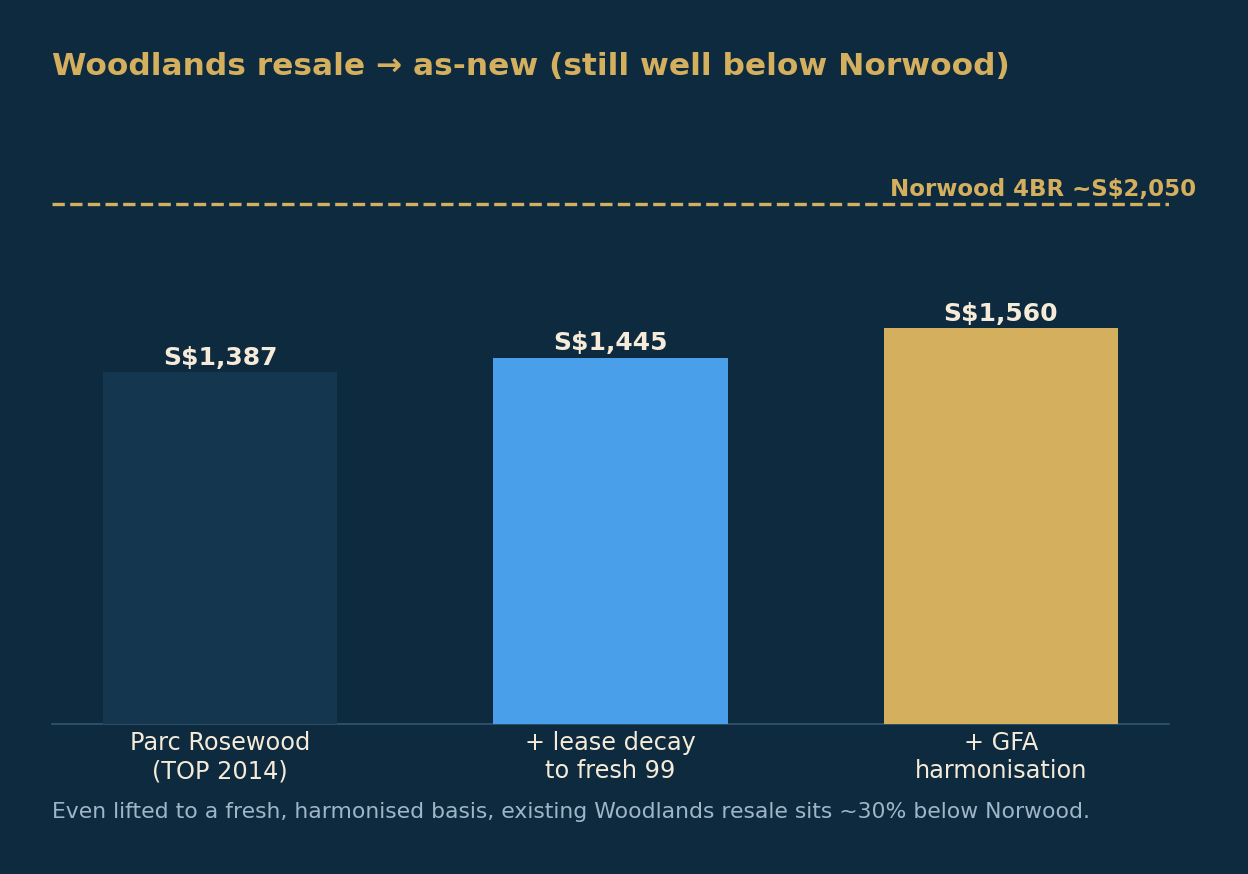

Here is the honest tension. Norwood Grand set a Woodlands price record precisely because there was no modern peer to anchor against — the last private launch here was Parc Rosewood in 2012. So the only comparison is against ageing resale, and that comparison has to be done properly. Two adjustments bring an older leasehold resale to a like-for-like, as-new footing:

- Lease decay. Parc Rosewood (completed 2014) and Woodhaven (completed 2015) have older 99-year leases, so their PSF must be lifted to a fresh-99 equivalent on Bala's Table.

- GFA harmonisation. Both predate the 22 January 2023 rules, so their strata areas still count air-conditioner ledges and void space — the same apartment shows more square feet and a lower PSF than a harmonised new launch. To compare like-for-like, the NPS calculator lifts a non-harmonised comp's as-new PSF by +8% for three-bedders and larger.

Run both against Norwood Grand's remaining four-bedroom stock at about S$2,050 psf:

| Comparable | Basis | PSF |

|---|---|---|

| Norwood Grand · 4BR (remaining) | New launch, harmonised | ~S$2,050 |

| Norwood Grand | Launch average | S$2,067 |

| Parc Rosewood | + lease decay + harmonisation (as-new) | S$1,560 |

| Woodhaven | + lease decay + harmonisation (as-new) | S$1,532 |

Even after lifting the old blocks to a fresh-lease, harmonised basis — Parc Rosewood from S$1,387 raw to ~S$1,560, Woodhaven from S$1,353 to ~S$1,532 — Norwood Grand's four-bedroom stock at ~S$2,050 sits roughly 30–34% above them. That premium is real, and a buyer should see it clearly: this is not a case, like some launches, where the adjustment closes the gap. Norwood carries a genuine new-build-and-transformation premium over everything else in Woodlands.

What the buyer is paying that premium for is the second half of the case: a fresh 99-year lease, the newest product in the estate, four minutes to the MRT, and a bet on the Woodlands transformation described below. The NPS's 3.5% growth read says that bet clears the 3% bar — but it is a bet on the region re-rating, not a discount to what is already there.

The Woodlands question: the North's re-rating

Norwood Grand's bull case is the estate around it. Woodlands is being built into the Woodlands Regional Centre — planned as the largest economic hub in the North and one of the biggest outside the city — alongside the 70-hectare Woodlands North Coast waterfront business-and-lifestyle precinct. Overlaid on that is cross-border connectivity: the Johor Bahru–Singapore Rapid Transit System (RTS) Link, due to open around end-2026, and the Johor-Singapore Special Economic Zone, both of which route their Singapore end through Woodlands. That is a genuine, funded, decade-scale transformation, and it is why the model's quality lift pushes a merely-average district record over the 3% line.

Two honest counterweights. The first is that most of that upside is a multi-year story — the regional centre and the North Coast build out over the next decade-plus, well beyond a first holding period, so a nearer-term buyer is partly underwriting patience. The second is the same premium the comparison exposed: Norwood already prices about 30% above adjusted Woodlands resale, so a good chunk of the transformation is in the price today. The upgrader demand is real — some 4,200 Woodlands HDB flats have crossed their Minimum Occupation Period since 2021 — but that demand met the record price, it did not undercut it.

How long you'd likely hold

Seller's stamp duty runs for four years (16%, 12%, 8%, 4%), so no exit before year four is realistic, and the shortest tier we publish is four-to-six years. The only stock left is the four-bedroom premium-plus-study, so we test it across its price range. Using the NPS calculator's model — ~3.5% expected growth, a 3% target — and taking Norwood Grand's own ~S$2,033 four-bedroom transacted level as the fair-value anchor, here is the estimated holding period on price growth alone.

| Available stack | PSF | Hold (price only) |

|---|---|---|

| 4BR Premium + Study — from | S$1,983 | 4–6 yrs |

| 4BR Premium + Study — mid | S$2,050 | 4–6 yrs |

| 4BR Premium + Study — top | S$2,122 | 6–10 yrs |

The read is entry-price-decisive. Because the modelled 3.5% growth clears the 3% bar, a four-bedroom bought at the bottom of the remaining range (from S$1,983 psf) — below the project's own four-bedroom level — clears in the four-to-six-year tier. But the top of the range (S$2,122 psf) sits enough above the project's own fair value that it stretches into six-to-ten years on price alone. With District 25 gross yields near 3.7%, rent is a meaningful help on a large own-stay unit, but it does not rescue an over-priced stack — the discipline is to buy the bottom of the tail, not the top. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

Norwood Grand is a clean B: strong rental momentum, a sensible 348-unit scale, four minutes to the MRT, and a district record that the market ratified by making it the best-selling launch of 2024. The grade rests on a quality lift doing real work — an average Woodlands growth record pushed over the 3% line by the project's own attributes and the funded transformation of the North. The honest caveats are the mirror image of the story: schools are undersubscribed rather than a draw; the price is a genuine ~30% premium over adjusted Woodlands resale, so the buyer is paying up for the transformation rather than into a discount; and the only stock left is the large four-bedroom tail, where the read turns entry-price-decisive — the bottom of the range clears in four-to-six years, the top stretches to six-to-ten. For an own-stay upgrader who wants the newest, best-connected home in a transforming Woodlands and buys the bottom of the remaining tail, Norwood Grand is a credible B. Pay up for the top of that tail and the same model says you wait longer.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade (B, 6.6), the five factor scores, modelled growth and the ~3.5%/yr projected appreciation per the TRIBE New Project Scorecard (URA Data Service transacted PSF; 1km resale trend lifted for project size, transport and schools; figures as at July 2026). The 19–20 October 2024 launch, the 84% (292 of 348) take-up at an average of S$2,067 psf, the 2.8x oversubscription (959 cheques), the 99.7% Singaporean/PR buyer mix, the per-bedroom from-prices (1BR+Study from S$988,000; 2BR from S$1.238m; 3BR Deluxe from S$1.698m; 4BR Deluxe+Study from S$2.238m), the "first private launch in Woodlands since Parc Rosewood in 2012" and the remaining four-bedroom premium stock per EdgeProp, "CDL's Norwood Grand achieves 84% sales at an average price of S$2,067 psf" (Cecilia Chow, 20 October 2024) and CDL's launch release; remaining-stock pricing (from S$2.616m–S$2.786m, S$1,983–S$2,122 psf) per 99.co and developer price lists. Land rate (S$294.889 million, S$904 psf ppr, September 2023 Champions Way GLS, top of six bids; TID second at S$835 psf ppr) per EdgeProp / URA. Parc Rosewood (99-year, TOP 2014) 12-month resale average ~S$1,387 psf and Woodhaven (99-year, TOP 2015) ~S$1,353 psf per PropertyGuru / PropNex transaction data; lease-decay adjustment per Bala's Table and GFA-harmonisation uplift of +8% (3BR+) per the NPS calculator's published methodology. Woodlands Regional Centre, the 70-hectare Woodlands North Coast, the Johor Bahru–Singapore RTS Link and the Johor-Singapore Special Economic Zone per URA / EdgeProp; the ~4,200 Woodlands HDB flats reaching MOP since 2021 per ERA. District 25 gross rental yield (~3.7%) estimated from URA rental and price data (Q2 2026). Primary 1 priority distance is measured door-to-door — confirm any school-distance claim on OneMap before relying on it. Prices and take-up are as reported at the dates cited and will change; scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.