Insights

Honest Insights On Penrith

Penrith grades A (7.3) on the New Project Scorecard — the Hong Leong–GuocoLand 462-home project on Margaret Drive, Queenstown's first private launch since 2018, 97% sold on day one at over S$2,800 psf, now down to its last two-bedders.

By TRIBE Editorial · 12 July 2026 · 11 min read

Penrith is a 462-unit, 99-year leasehold development on Margaret Drive in Queenstown, District 3 — twin 40-storey towers by Hong Leong Holdings, Hong Realty and GuocoLand, a 0.59km walk from Queenstown MRT on the East-West Line, and the first private residential launch in Queenstown since 2018. It grades an A (7.3) on our New Project Scorecard (NPS), and it owns the loudest sales record of 2025: 447 of 462 units — 97% — sold by 4pm on launch day, 18 October 2025, at prices from S$2,435 to S$3,088 psf and an average above S$2,800 psf. This is a look at what the A rests on, what a seven-year supply drought did to that price, and whether the last handful of two-bedders still on the shelf makes sense at the top of the stack. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted for the project's own size, transport and schools, not a forecast.

The scorecard: what the A actually says

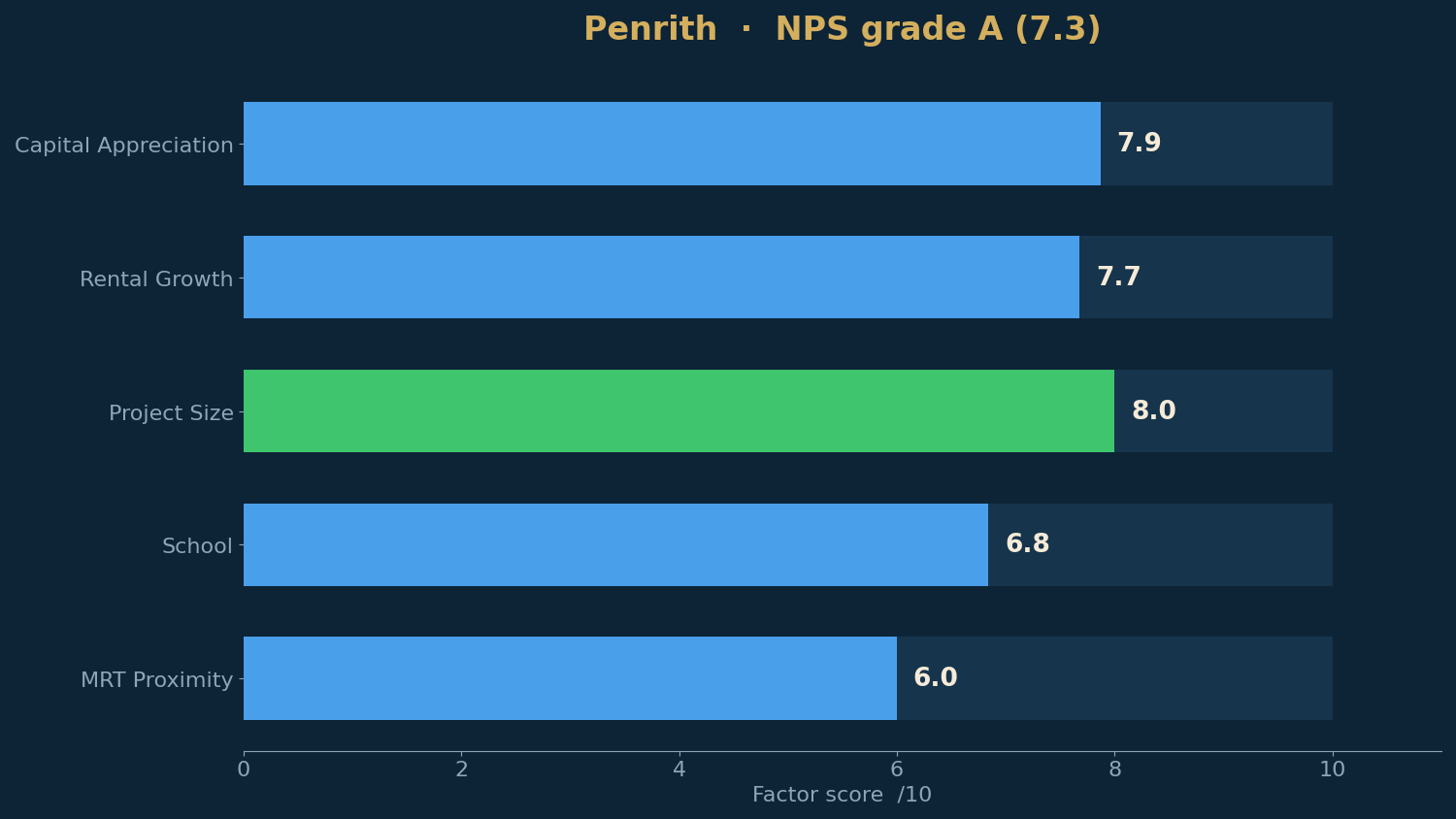

Penrith's 7.3 is unusual among recent launches for having no real hole — every factor sits at 6.0 or better.

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| Capital Appreciation | 7.9 | 1km resale grew ~3.5%/yr; lifted for size, transport, schools → ~4.4%/yr |

| Rental Growth | 7.7 | District 3 rents grew ~7.1%/yr over the decade — strong momentum |

| Project Size | 8.0 | 462 units — ideal scale for liquidity and facilities without crowding |

| School | 6.8 | Queenstown Primary at 0.13km — next door, though balanced rather than oversubscribed |

| MRT Proximity | 6.0 | A 0.59km walk to Queenstown MRT (East-West Line) |

The headline factor is growth. Capital appreciation scores 7.9 — resale homes within a kilometre of Margaret Drive appreciated about 3.5% a year over the past decade on a same-property basis, one of the stronger 1km records on the board, and the model lifts that for Penrith's own size, transport and schools to a projected ~4.4% a year — clearing the 3% bar comfortably. This is the mirror image of the prime-district launches we have reviewed, where a glamorous address sits on a weak resale growth engine: Queenstown's engine is the quiet kind that actually shows up in caveats, powered by a city-fringe location, the Dawson HDB renewal and a decade of upgrader demand.

The rest of the card is solid rather than spectacular. Rental growth at 7.7 reflects District 3 rents compounding about 7.1% a year over the decade — one-north, the CBD and the medical belt at Outram all feed tenants into Queenstown. Size scores 8.0 at 462 units, and schools score 6.8: Queenstown Primary School is 0.13km away — effectively across the road — though it is balanced rather than oversubscribed, so this is convenience more than ballot leverage. MRT is the softest line at 6.0: 0.59km on OneMap's door-to-door walk, a real seven-to-eight minutes rather than the "five minutes" in the brochures, but still comfortably walkable.

The launch: what a seven-year drought clears

Queenstown had not seen a private launch since Margaret Ville and Stirling Residences in mid-2018. Seven years of pent-up demand met a 462-unit project: the developers collected 1,905 cheques — 4.1 times the unit count — before doors opened, previewed from S$2,437 psf, and sold 97% in a single day, with Singaporeans over 90% of buyers. All three-bedders were gone by mid-afternoon; only two four-bedders were left by 4pm. It was the fifth launch of 2025 to clear 90% on its opening weekend, alongside Lentor Central Residences, LyndenWoods, Springleaf Residence and Skye at Holland — and at over S$2,800 psf, comfortably the priciest of them.

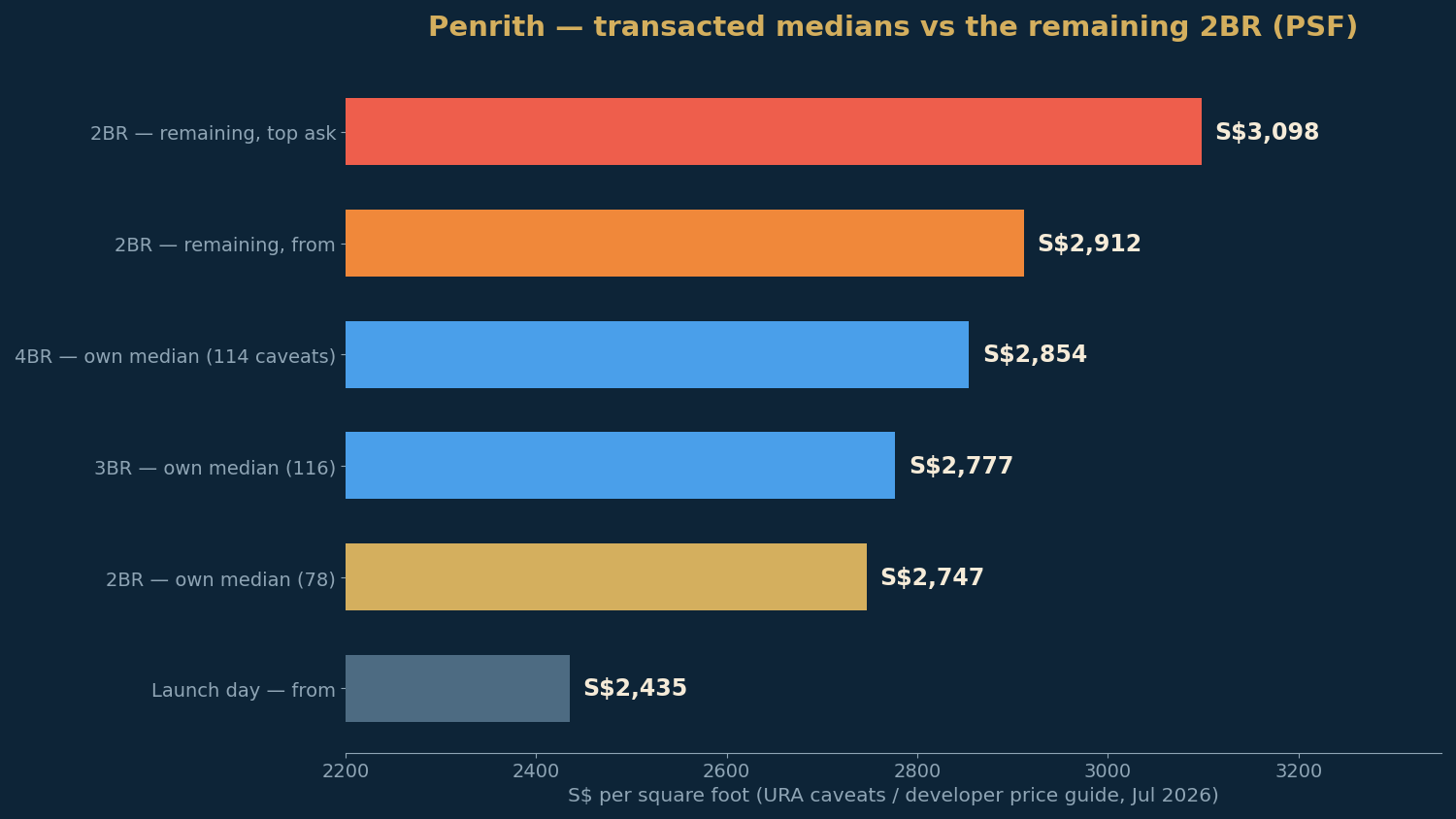

What the project has actually transacted at, by bedroom (URA caveats, per the live scorecard):

| Type | Typical size | Median PSF | Caveats |

|---|---|---|---|

| 2 Bedroom | 678 sqft | S$2,747 | 78 |

| 3 Bedroom | 850–1,066 sqft | S$2,777 | 116 |

| 4 Bedroom | 1,173–1,281 sqft | S$2,854 | 114 |

Nine months on, the shelf is nearly bare. Per the developer's price guide (July 2026), what remains is roughly the last ten units, all of one two-bedroom type — 614 sqft, priced from S$1.788 million to S$1.902 million, or S$2,912 to S$3,098 psf. Against the project's own two-bedroom median of S$2,747 psf, the leftover stock enters 6% to 13% above what the market has already paid here. These are the high floors of the stack — and unlike the discounted tails we have found at some launches, this tail is priced like the record it sits on.

The benchmark: a record price, adjusted honestly

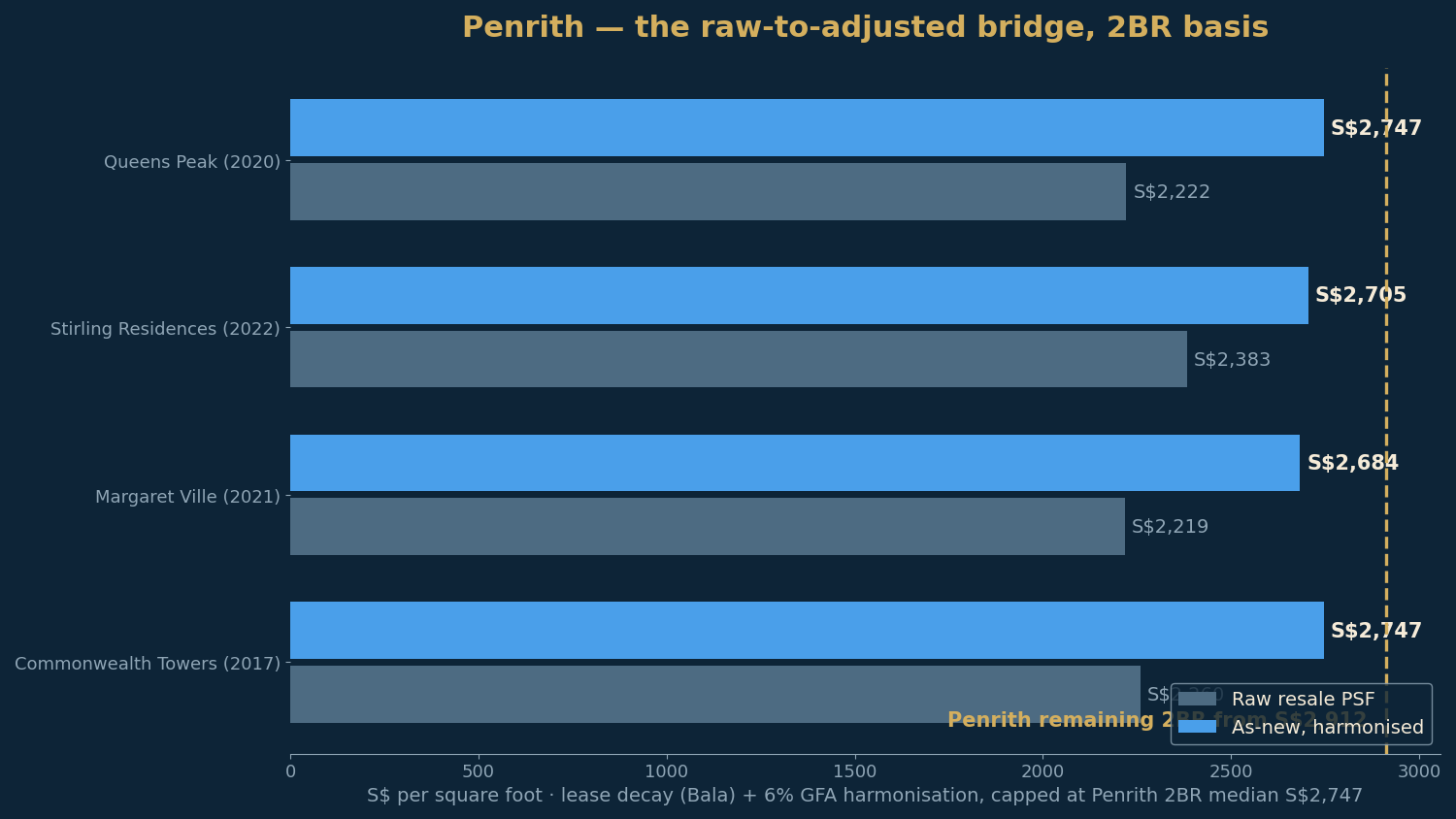

Is S$2,800-plus defensible in Queenstown? The nearest comparisons are the 2016–2022 generation next door, and a raw PSF comparison flatters them. Two adjustments bring an older leasehold resale to a like-for-like, as-new footing:

- Lease decay. Queens Peak (TOP 2020), Commonwealth Towers (2017), Margaret Ville (2021) and Stirling Residences (2022) are four to nine years into their 99-year leases, so their PSF must be lifted to a fresh-99 equivalent on Bala's Table.

- GFA harmonisation. All of them predate the 22 January 2023 rules, so their strata areas still count air-conditioner ledges and voids — the same apartment shows more square feet and a lower PSF than a harmonised new launch like Penrith. The NPS calculator lifts a non-harmonised comp's as-new PSF by +6% for one- and two-bedders (capped at the launch's own median, a deliberately conservative floor).

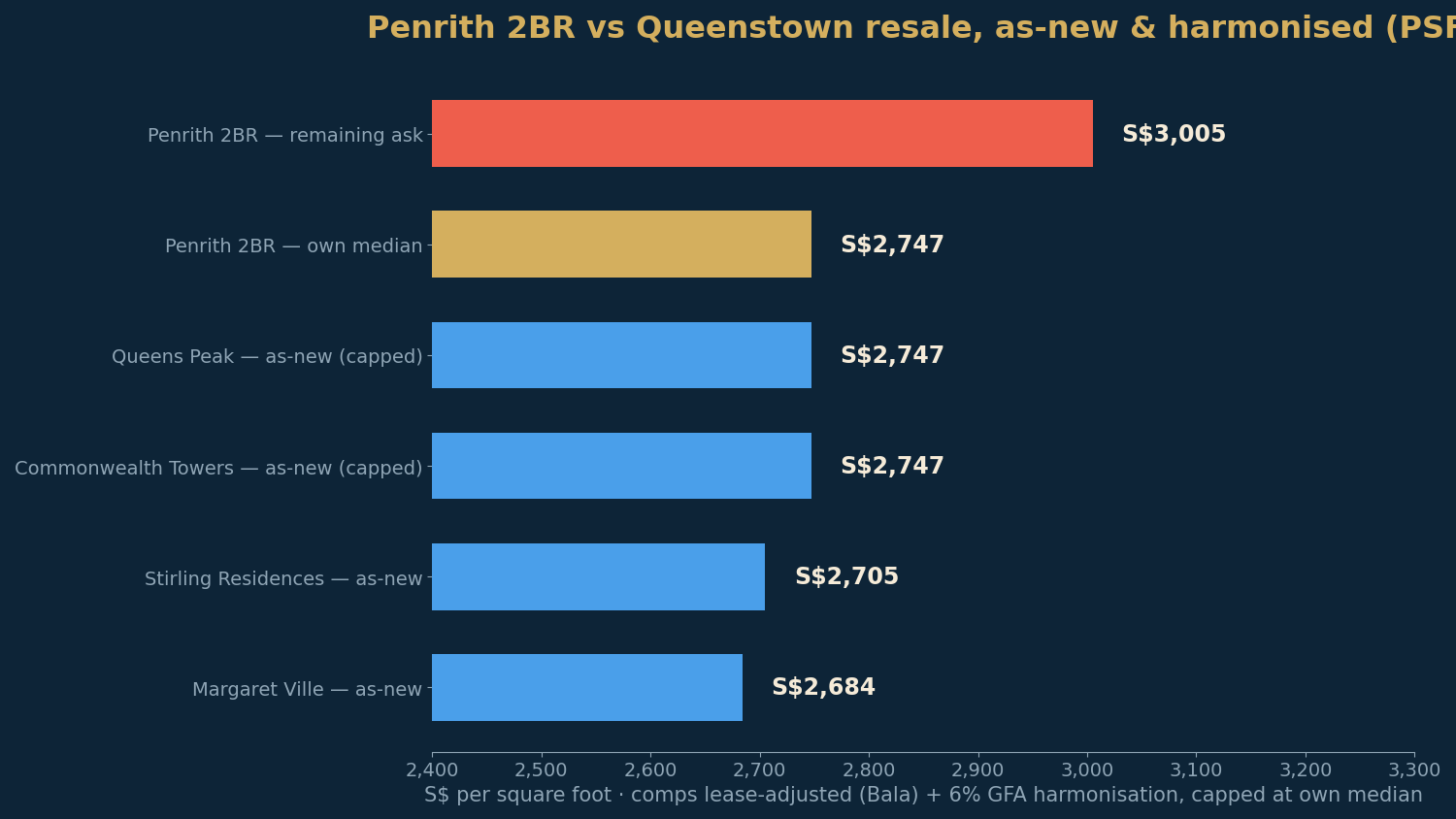

Run the two-bedroom comparison:

| Comparable | Raw resale PSF | As-new, harmonised |

|---|---|---|

| Penrith · 2BR (remaining) | — | S$2,912–3,098 (asking) |

| Penrith · 2BR (own median) | — | S$2,747 |

| Queens Peak (2020, 0.24km) | S$2,222 | ~S$2,747 (capped) |

| Stirling Residences (2022, 0.89km) | S$2,383 | ~S$2,705 |

| Margaret Ville (2021, 0.78km) | S$2,219 | ~S$2,684 |

| Commonwealth Towers (2017, 0.3km) | S$2,260 | ~S$2,747 (capped) |

The adjustment tells a two-sided story. On one side, Penrith's own median — S$2,747 for a two-bedder — is almost exactly where the adjusted comps land (S$2,684–2,747): the launch price the market paid in October was, on a like-for-like basis, roughly fair against the estate around it. That is rare among the launches we have reviewed and it is the honest core of the A grade. On the other side, the remaining stock does not get that defence: at S$2,912–3,098 psf, the last two-bedders sit 8–15% above Margaret Ville as-new and 6–13% above Penrith's own record.

The Queenstown question: what's already in the price

Penrith's bull case is hiding in plain sight: this is one of Singapore's oldest estates being systematically rebuilt — the Dawson precinct's newer HDB blocks, the hawker-and-market cluster on Margaret Drive itself, and a resale flat market where more than a hundred Queenstown HDB transactions crossed S$1 million in 2025, feeding exactly the upgrader pool that queued in October. The counterweight is the land market's own signal: the site drew only two bids in August 2024, and the S$1,154 psf ppr winning rate was 5% above the sole other offer — developers were far more cautious about this price point than launch-day buyers turned out to be. A buyer today should also note that the 3.5%-a-year 1km record already reflects a decade of renewal; the model's projection extends that record, it does not discover a new catalyst.

How long you'd likely hold

Seller's stamp duty runs for four years (16%, 12%, 8%, 4%), so no exit before year four is realistic, and the shortest tier we publish is four-to-six years. The only stock left is the 614 sqft two-bedroom type, so we test it across its asking range. Using the NPS calculator's model — ~4.4% expected growth, a 3% target — with the project's own S$2,747 two-bedroom median as the fair-value anchor, here is the estimated holding period on price growth alone.

| Available stack | PSF | Hold (price only) |

|---|---|---|

| 2BR 614 sqft — from (S$1.788m) | S$2,912 | 4–6 yrs |

| 2BR 614 sqft — mid | S$3,005 | 6–10 yrs |

| 2BR 614 sqft — top (S$1.902m) | S$3,098 | 6–10 yrs |

The strong growth engine is doing the work: even entering 6% above the project's own median, the bottom of the remaining range clears the 3% bar inside four-to-six years, because a ~4.4% modelled growth rate absorbs a premium quickly. The arithmetic threshold sits at about S$2,974 psf (≈S$1.826 million) — buy under that and you stay in the four-to-six-year tier; the mid and top of the range stretch to six-to-ten years. With District 3 gross yields around 3.4% and D3 rents on a 7%-a-year decade run, a rented-out two-bedder carries well while it waits. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

Penrith is the most complete scorecard of the 2025 launch generation: no factor below 6, a genuine ~3.5%-a-year 1km growth record lifted to ~4.4%, deep D3 rental momentum, the right project size, and a school across the road. The market ratified it — 97% in a day, at a Queenstown record — and, unusually, the like-for-like adjustment defends the launch price: Penrith's own S$2,747 two-bedroom median lands almost exactly on the adjusted value of the estate's 2017–2022 resale. The honest caveats are narrow but real: the land tender's two bids say the professionals were more cautious than the queue; the "five-minute" MRT walk is nearer eight; and the only stock left is the top of the two-bedroom stack at S$2,912–3,098 psf, 6–13% above the project's own record — priced for the growth story to keep delivering. Under S$2,974 psf the model still clears in four-to-six years, which is more forgiveness than most leftover stock earns. For an upgrader who missed October, the door is still open — but it is the top of the stack, and you are paying for it.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade (A, 7.3), the five factor scores, modelled growth and the ~4.4%/yr projected appreciation per the TRIBE New Project Scorecard (URA Data Service transacted PSF; 1km resale trend lifted for project size, transport and schools; figures as at July 2026). The 18 October 2025 launch, the 97% (447 of 462) day-one take-up at S$2,435–3,088 psf and an average above S$2,800 psf, the 1,905 cheques (4.1x subscription), the 90%+ Singaporean buyer mix, the "first Queenstown launch since 2018" and the launch-day sell-out of all three-bedders per EdgeProp, "Penrith achieves 97% sales on launch day at an average price of over $2,800 psf" (18 October 2025), "Penrith over 4.1 times subscribed ahead of weekend launch on Oct 18" and "Hong Leong Holdings previews Penrith with prices starting from $2,437 psf". Land rate (S$497 million, S$1,154 psf ppr, August 2024 Margaret Drive GLS; two bids, Sing Holdings–Cedar second at S$1,100 psf ppr) per EdgeProp, "GuocoLand-Hong Leong JV submits top bid of $1,154 psf ppr for Margaret Drive GLS site". Remaining-stock pricing (last ~10 units, 2BR 614 sqft, S$1,788,000–S$1,902,000) per the developer's price guide as carried by Huttons marketing (MySgProp), updated 6 July 2026. Per-bedroom transacted medians (2BR S$2,747 / 3BR S$2,777 / 4BR S$2,854) per URA caveats via the NPS calculator; resale comparables (Queens Peak, Commonwealth Towers, Margaret Ville, Alexis, Stirling Residences) age- and lease-adjusted per Bala's Table with a +6% (1–2BR) GFA-harmonisation uplift, capped at the launch's own median, per the NPS calculator's published methodology. District 3 gross rental yield (~3.4%) estimated from URA rental and price data (Q2 2026). Primary 1 priority distance is measured door-to-door — confirm any school-distance claim on OneMap before relying on it. Prices and availability are as reported at the dates cited and will change; scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.