Insights

Honest Insights On Tembusu Grand

Tembusu Grand grades A (7.6) on the New Project Scorecard — CDL and MCL Land's 638-unit Katong project received its TOP in December 2025, is 99% sold, set a S$2,881 psf sub-sale record in May, and is down to five one-bedders and two penthouses.

By TRIBE Editorial · 13 July 2026 · 12 min read

Tembusu Grand is a 638-unit, 99-year leasehold development on Jalan Tembusu in Katong, District 15 — four 20-to-21-storey towers by CDL and MCL Land that opened the Katong GLS generation when the site drew eight bids and a S$1,302 psf ppr record in January 2022. It grades an A (7.6) on our New Project Scorecard (NPS), and it is that rare thing among the projects we review: a completed story. The building received its TOP in December 2025, the shelf is 99% sold, sub-sales set a S$2,881 psf record in May 2026 — 17% above the S$2,465 launch average — and what remains is exactly five one-bedders and two S$7.888 million penthouses. This is a look at what the A is made of, what three years of sell-through proved about the price, and how the last seven doors stack up. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted for the project's own size, transport and schools, not a forecast.

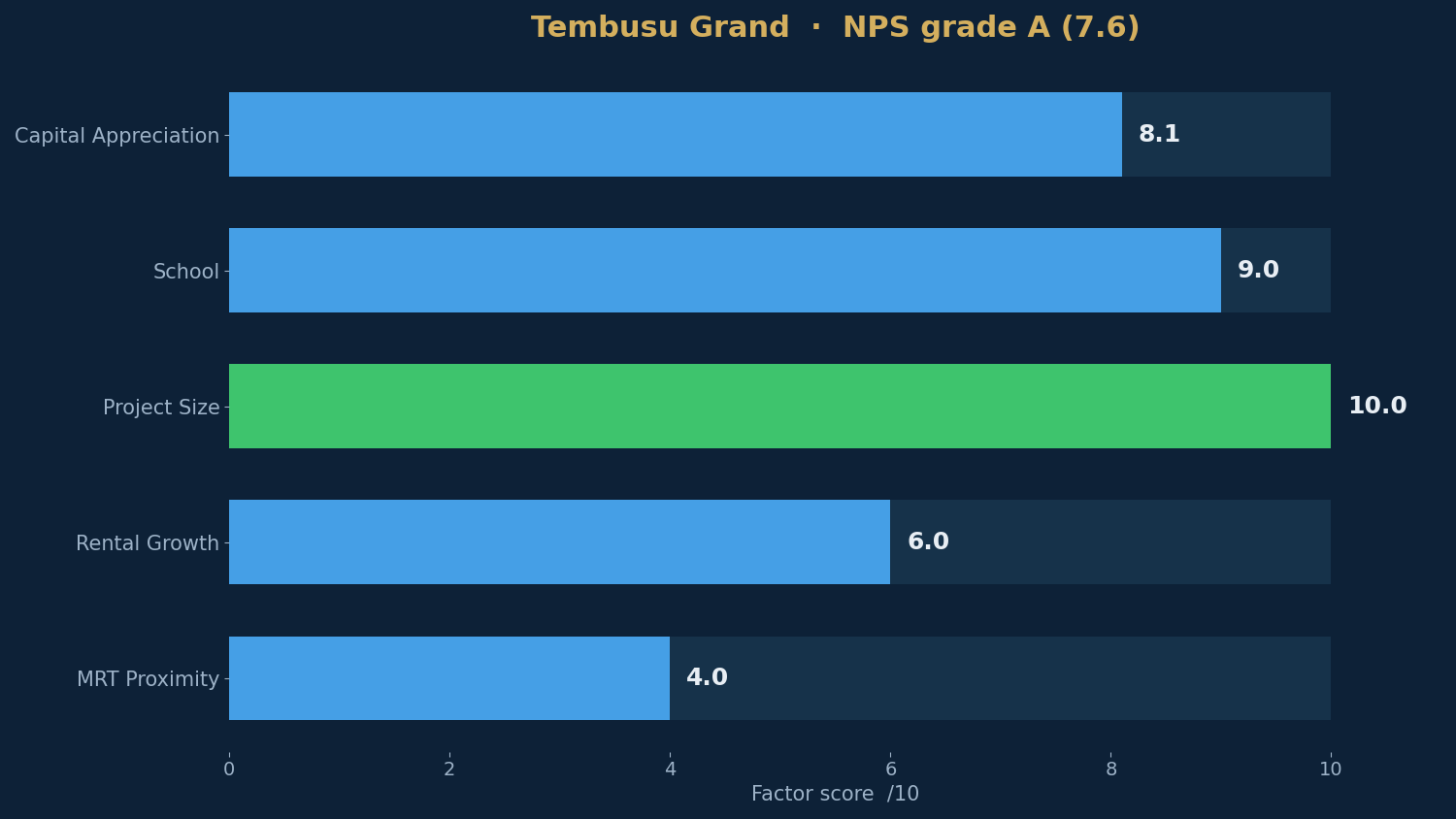

The scorecard: what the A actually says

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| Project Size | 10.0 | 638 units — ideal scale for liquidity and facilities |

| School | 9.0 | Tanjong Katong Primary at 0.38km, oversubscribed; Haig Girls' within 1km |

| Capital Appreciation | 8.1 | 1km resale grew ~3.6%/yr; lifted for size, transport, schools → ~4.5%/yr |

| Rental Growth | 6.0 | District 15 rents grew ~6.1%/yr over the decade |

| MRT Proximity | 4.0 | A 0.76km walk to Tanjong Katong MRT (TEL, opened June 2024) |

The engine is capital appreciation. Resale homes within a kilometre of Jalan Tembusu appreciated about 3.6% a year over the past decade on a same-property basis, and the model applies one of the larger quality lifts on the board — +0.87 points for the project's size, transport and schools — to a projected ~4.5% a year, clearing the 3% bar with room to spare. The lift is earned mechanically: size scores a perfect 10.0 at 638 units, and schools score 9.0, with oversubscribed Tanjong Katong Primary a 0.38km walk and Haig Girls' also inside the kilometre — a genuine ballot-distance card in a district where school access drives family demand.

The two quieter lines are worth reading honestly. Rental growth at 6.0 reflects D15 rents compounding ~6.1% a year — healthy, but a tier below the 7%-plus districts — and the modelled gross yield is 3.02%, thinned by East Coast pricing. MRT scores 4.0: Tanjong Katong station on the Thomson-East Coast Line opened in June 2024, and the 0.76km OneMap walk is real — nearer ten minutes than the brochure's eight — though it turned a bus-dependent pocket into a one-train ride to the CBD, something the launch buyers of April 2023 paid for on faith.

The launch, and the three years that ratified it

CDL's S$768 million (S$1,302 psf ppr) bid in January 2022 — eight bidders deep, with a Hong Leong consortium second at roughly S$1,208 — was the record that repriced Katong land and set up everything that followed: Grand Dunman at S$1,350 ppr that May, Emerald of Katong next door in 2023. The April 2023 launch weekend moved 340 of 638 units (53%) at an average of S$2,465 psf — one-bedders-with-study from S$1.248 million, two-bedders from S$1.548 million, three-bedders from S$2.278 million — with about 90% Singaporean buyers. It was a solid rather than spectacular opening, and the sell-through that followed is the more telling record: 91% by November 2024 (52 units in that month alone, as Emerald of Katong's 99% launch sent overflow next door), effectively sold out by mid-2026 — five unsold units by URA caveats as at 2 June 2026, seven on the developer's mid-July balance chart.

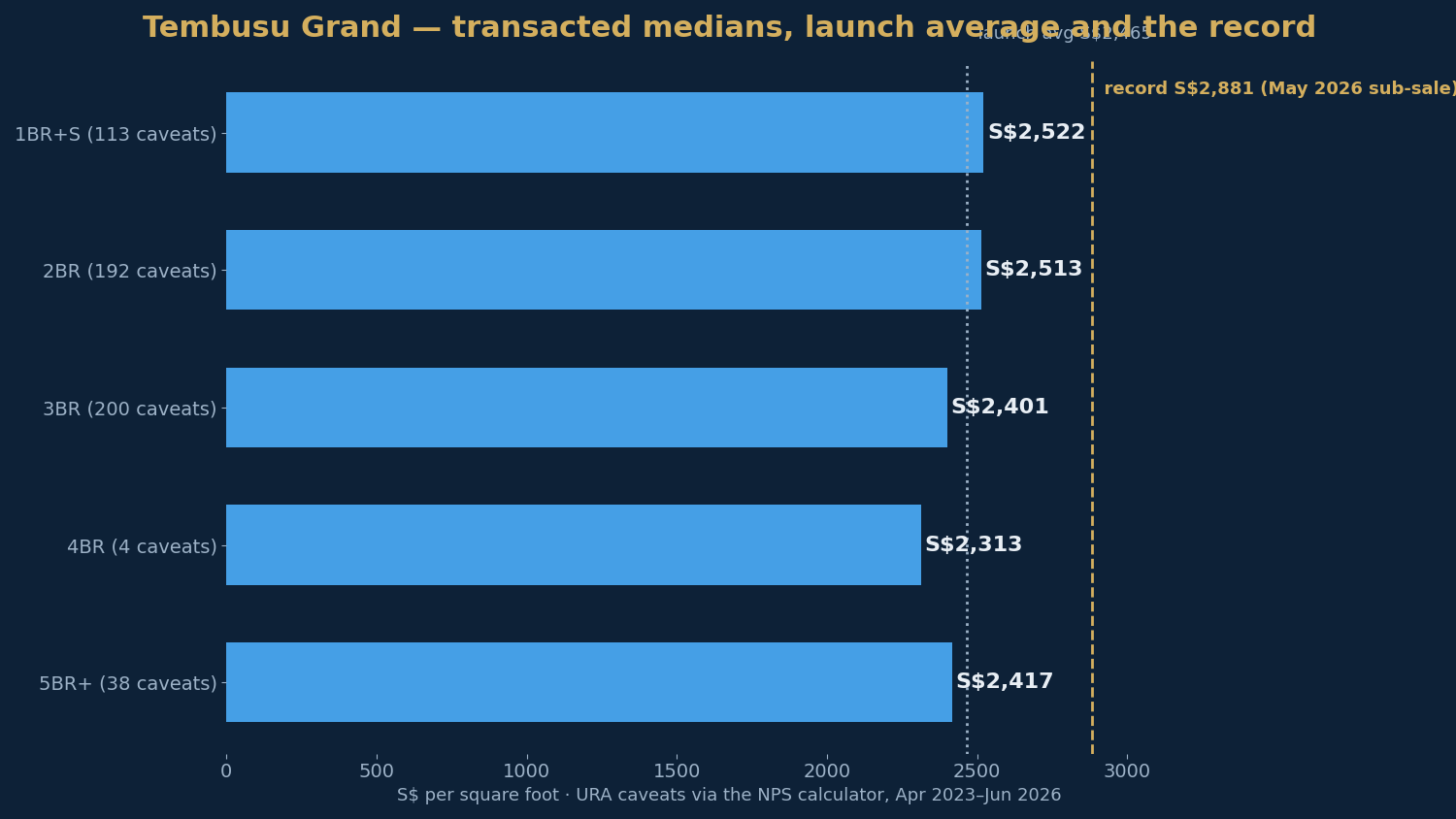

What the project has transacted at, by bedroom (URA caveats via the live scorecard, April 2023–June 2026):

| Type | Typical size | Median PSF | Caveats |

|---|---|---|---|

| 1BR + Study | 527 sqft | S$2,522 | 113 |

| 2 Bedroom | 743 sqft | S$2,513 | 192 |

| 3 Bedroom | 1,173 sqft | S$2,401 | 200 |

| 4 Bedroom | 1,604 sqft | S$2,313 | 4 |

| 5 Bedroom | 1,711 sqft | S$2,417 | 38 |

The May 2026 sub-sale market put a number on what completion did to the price: a 1,173 sqft three-bedder changed hands at S$3.38 million — S$2,881 psf, a project record — four days after a 990 sqft unit set the previous mark at S$2,878, with seven further 2026 sub-sales between S$2,693 and S$2,850 psf. Against the S$2,465 launch average, the record is a 17% mark-up in three years — on a physically complete building, not a promise.

What's left: seven doors, two different conversations

Per the developer's balance chart (13 July 2026), the shelf is down to five 1BR+Study units (527–646 sqft) at S$1.409–1.546 million nett — roughly S$2,393–2,674 psf across the size range — and the two 2,691 sqft five-bedroom penthouses at S$7.888 million (S$2,931 psf) each. Every other bedroom type is fully sold.

Against the project's own record — the in-project benchmark — the one-bedders are priced with unusual restraint: the ask range straddles the project's own S$2,522 one-bedroom median (113 caveats over three years), from 5% below to 6% above it. Leftover stock priced at the record rather than above it is something we have rarely found on these shelves — compare Faber Residence's tail at +6–11% or Penrith's at +6–13%. The penthouses are another conversation: at S$2,931 psf they ask 21% above the S$2,417 five-bedroom-band median, which is trophy pricing, not scorecard pricing.

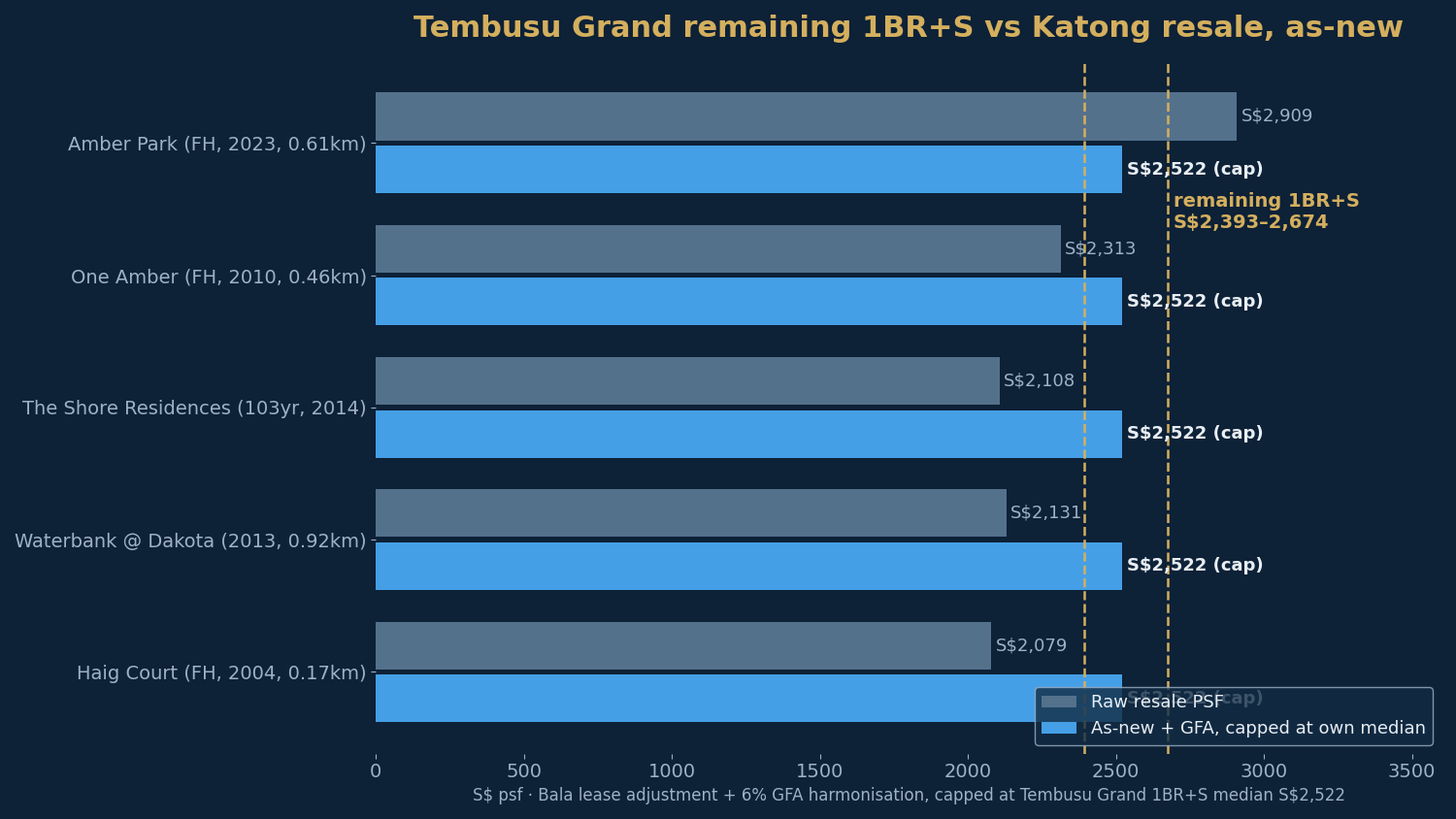

The benchmark: Katong resale, adjusted honestly

Katong's resale belt is largely freehold and older, so raw PSF comparisons mislead in both directions. We lift each comparable to a like-for-like, as-new footing: lease/age adjustment (Bala's Table, converting to a fresh-99 equivalent) plus +6% GFA harmonisation for one- and two-bedders, since every comp predates the 22 January 2023 strata-area rules. The NPS calculator caps each adjusted comp at the project's own median — a deliberately conservative floor.

| Comparable | Raw resale PSF | As-new, harmonised |

|---|---|---|

| Tembusu Grand · 1BR+S (remaining) | — | S$2,393–2,674 (asking) |

| Tembusu Grand · 1BR+S (own median) | — | S$2,522 |

| Amber Park (freehold, 2023, 0.61km) | S$2,909 | ~S$2,522 (capped) |

| One Amber (freehold, 2010, 0.46km) | S$2,313 | ~S$2,522 (capped) |

| The Shore Residences (103yr, 2014, 0.55km) | S$2,108 | ~S$2,522 (capped) |

| Waterbank @ Dakota (99yr, 2013, 0.92km) | S$2,131 | ~S$2,522 (capped) |

| Haig Court (freehold, 2004, 0.17km) | S$2,079 | ~S$2,522 (capped) |

Every comparable hits the cap — uncapped, their as-new values run S$2,554–2,562, and Amber Park trades at S$2,909 raw today as a freehold 2023 building. Read plainly: on a like-for-like basis the estate around Tembusu Grand values at or above the project's own S$2,522 median, which is why the sub-sale market has been able to print S$2,693–2,881 without leaving the neighbourhood's gravity. The cluster agrees — Emerald of Katong launched at S$2,621 average in November 2024, Grand Dunman's 911 caveats median S$2,524, and the freehold Continuum was averaging S$2,788 by late 2024. The remaining one-bedders, asking S$2,393–2,674, sit inside that fabric, not above it.

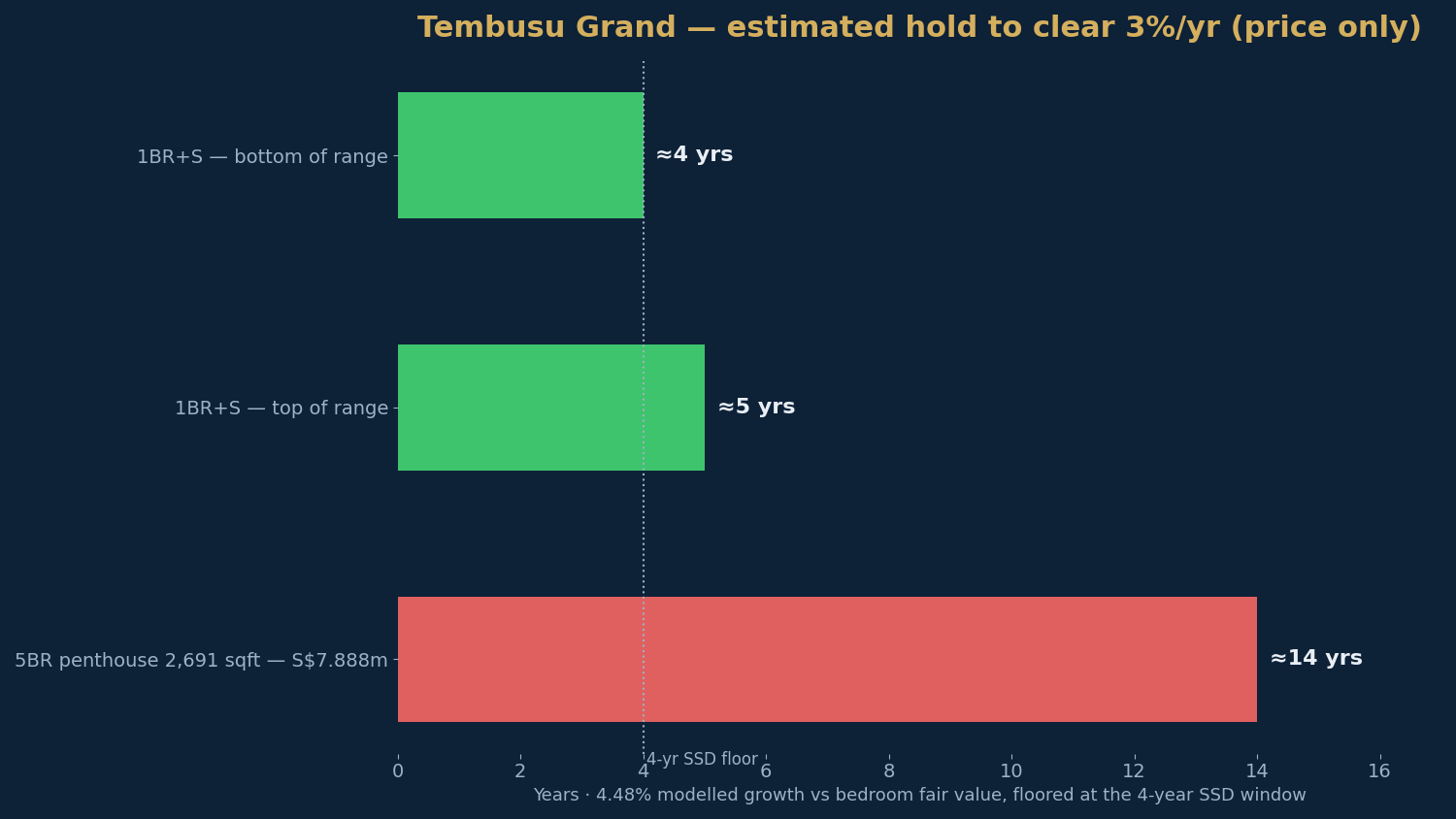

How long you'd likely hold

Seller's stamp duty runs for four years (16%, 12%, 8%, 4%), so no exit before year four is realistic, and the shortest tier we publish is four-to-six years. Using the NPS calculator's model — 4.48% expected growth, a 3% target — here is the estimated holding period for each remaining stack, on price growth alone, against the bedroom's own transacted median as the fair-value anchor.

| Available stack | PSF | Hold (price only) |

|---|---|---|

| 1BR+S 527–646 sqft — bottom of range (S$1.409m–1.546m) | S$2,393 | 4–6 yrs |

| 1BR+S 527–646 sqft — top of range | S$2,674 | 4–6 yrs |

| 5BR penthouse 2,691 sqft — S$7.888m | S$2,931 | >10 yrs |

The one-bedders clear cleanly: with a ~4.5% modelled growth engine, even the top of the ask range clears the 3% bar by year five, and the four-to-six-year tier stretches all the way to a S$2,747 psf entry — comfortably above anything on the shelf. They are also the one format where the 3.02% yield line understates the case: a completed, TOP-obtained 527 sqft unit a ten-minute walk from a TEL station is rentable now, at the quantum D15's tenant pool actually pays, so the wait is carried rather than endured. The penthouses are the mirror image: benchmarked against the project's five-bedroom band, a 21% premium at 4.48% growth needs roughly 14 years to annualise past 3% on price alone (the four-to-six tier would require about S$2,633 psf, or roughly S$7.1 million), and no realistic rent on a S$7.888 million penthouse changes that read materially. Trophy floors are bought for other reasons. One note on the anchor: the scorecard also publishes a small separate "penthouse-format" band (eight caveats, median S$2,366) for compact top-floor units; we benchmark the big penthouses against the 1,711 sqft five-bedroom band instead, as the closer product. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

Tembusu Grand is what an A looks like after the market has finished voting. The scorecard's engine — a ~3.6%-a-year 1km record lifted to ~4.5% by a perfect size score and a genuine ballot-distance school card — has been ratified in caveats: 99% sold, a 17% sub-sale mark-up over launch in three years, and a completed building collecting keys rather than promises. The honest caveats are the card's own quiet lines: D15 rental growth is a tier below the strongest districts, the yield models at 3.02%, and the 0.76km TEL walk is real but not doorstep. What is left on the shelf splits cleanly. The five one-bedders are, unusually, priced inside the project's own record — the whole range holds a four-to-six-year read with a live rental market underneath it — and are the last new-launch entry into this postcode under S$1.6 million. The penthouses, at 21% over the big-format band, are priced for a buyer who is not reading holding-period tables. If a completed Katong one-bedder fits your case, this is one of the few honestly-priced tails of 2026; if you need the growth story cheap, that window closed in April 2023.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade (A, 7.6), the five factor scores, modelled growth (~4.5%/yr) and the 3.02% modelled yield per the TRIBE New Project Scorecard (URA Data Service transacted PSF; 1km resale trend lifted for project size, transport and schools; figures as at July 2026). Land tender (S$768 million, ~S$1,302 psf ppr, eight bids, January 2022; Hong Leong consortium second at S$712.6 million) per the URA tender results as reproduced by PropertyReviewSG and EdgeProp/Yahoo Finance. The 8–9 April 2023 launch (340 of 638, 53%, average S$2,465 psf, per-bedroom entry prices, ~90% Singaporean buyers) per the CDL–MCL Land joint press release (9 April 2023) and EdgeProp. The 91%-by-November-2024 milestone and the D15 cluster figures (Emerald of Katong 99% at S$2,621 average; The Continuum ~S$2,788) per EdgeProp, "Emerald of Katong boosts District 15 new home sales" (December 2024); Grand Dunman's S$2,524 median (911 caveats) per our Grand Dunman review. TOP obtained December 2025, the S$2,881 psf sub-sale record (18 May 2026, 1,173 sqft, S$3.38 million), the prior S$2,878 record, the seven other 2026 sub-sales at S$2,693–2,850 psf and the five-units-unsold caveat position (2 June 2026) per EdgeProp, "New record high of $2,881 psf at Tembusu Grand condo sub-sale" (4 June 2026). Remaining-stock pricing (five 1BR+S at S$1.409–1.546 million nett; two 2,691 sqft penthouses at S$7.888 million) per the developer balance chart as carried by tembusugrand-condo.sg, updated 13 July 2026 — agent-carried charts are unofficial and may lag caveats. Per-bedroom transacted medians per URA caveats via the NPS calculator; resale comparables (Amber Park, One Amber, The Shore Residences, Waterbank @ Dakota, Haig Court) age- and lease-adjusted per Bala's Table with a +6% (1–2BR) GFA-harmonisation uplift, capped at the project's own median, per the NPS calculator's published methodology. Tanjong Katong MRT (TE25) opened 23 June 2024 per LTA. Primary 1 priority distance is measured door-to-door — confirm any school-distance claim on OneMap before relying on it. Prices and availability are as reported at the dates cited and will change; scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.