Insights

Honest Insights On Parktown Residence

Parktown Residence grades S (8.6) on the New Project Scorecard — the first mega-integrated development in Tampines North, 1,193 units by UOL, SingLand and CapitaLand. It sold 87% on its February 2025 debut and is now about 99% sold.

By TRIBE Editorial · 9 July 2026 · 10 min read

Parktown Residence is a 1,193-unit, 99-year leasehold integrated development on Tampines Avenue 11 in District 18 — the residential heart of a mixed-use complex by UOL Group, Singapore Land and CapitaLand Development that folds in a bus interchange, a hawker centre, a community club, retail and direct access to the coming Tampines North MRT station on the Cross Island Line. It grades an S (8.6) on our New Project Scorecard (NPS) — the highest card we have run on a suburban launch — and the market treated it that way, taking 1,041 of 1,193 units — 87% — on its February 2025 opening weekend. Eighteen months on it is about 99% sold. This is an honest look at what the S rests on, what the record take-up actually bought, and how the last of the stock is priced. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted for the project's own size, transport and schools, not a forecast. For the holding period, we use the published NPS calculator: fair value is the median transacted PSF for each bedroom type, the project grows at its modelled rate, and we report the years needed to clear a 3% annual return — gross of stamp duty, financing and selling costs.

The scorecard: what an S actually says

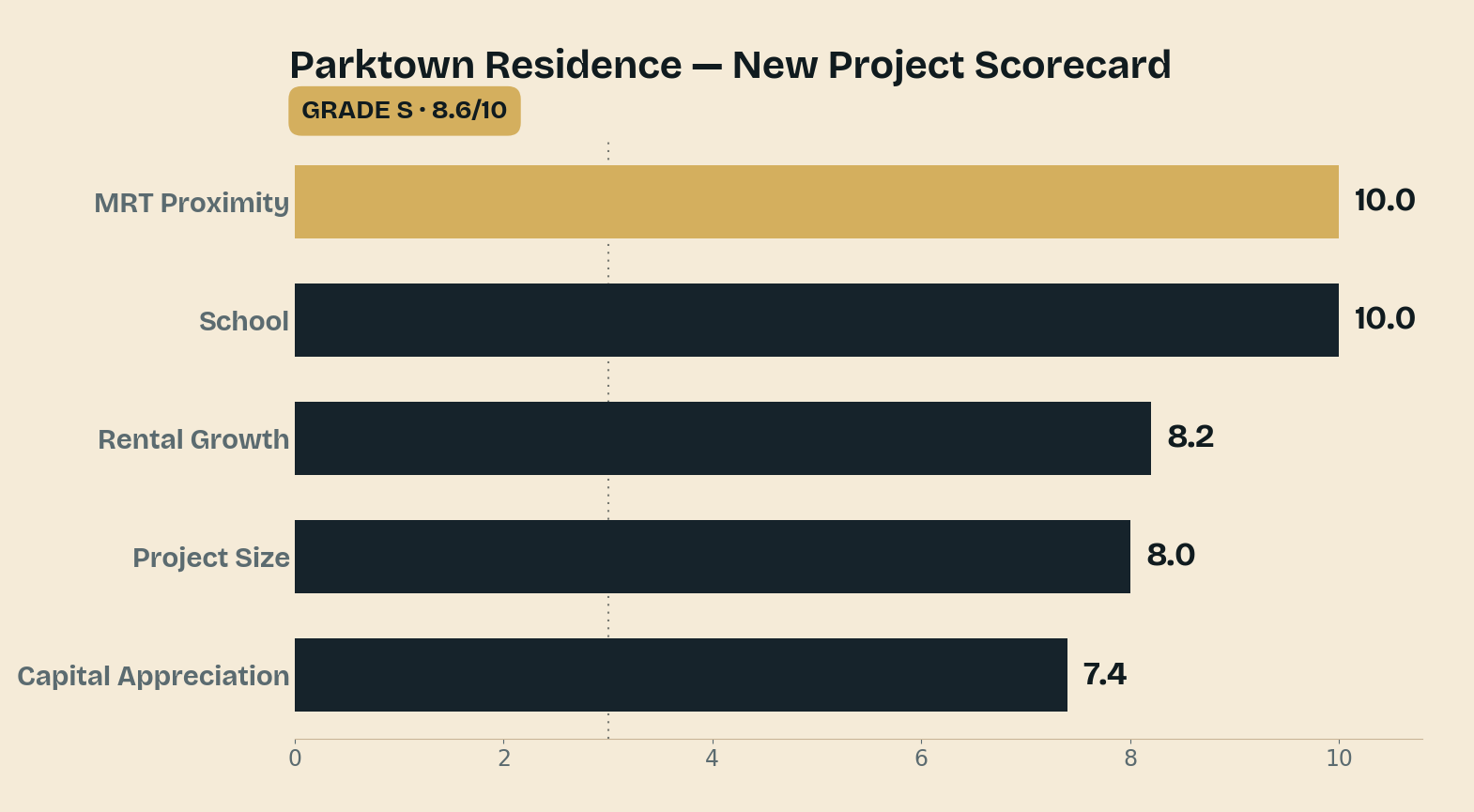

Parktown's 8.6 is the rarest kind of card — two perfect legs, and no weak one anywhere.

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| MRT Proximity | 10.0 | Integrated development — direct access to the coming Tampines North MRT (Cross Island Line) |

| School | 10.0 | Three primary schools within 1km; Angsana Primary (0.38km, heavily oversubscribed) |

| Rental Growth | 8.2 | District 18 rents grew ~7.4%/yr over the decade — strong rental momentum |

| Project Size | 8.0 | 1,193 units — deep liquidity and a full facilities deck |

| Capital Appreciation | 7.4 | 1km resale grew ~3.0%/yr; lifted ~+1.3 for scale, transport, schools → ~4.35%/yr |

What lifts this to an S is that the two things families pay most for are both maxed out. Transport scores a full 10 because Parktown is not "near" an MRT — it is built over one: the Tampines North station on the Cross Island Line sits inside the complex, alongside the bus interchange, so the connection is weatherproof and step-free. Schools also score a full 10, with three primary schools inside a kilometre led by Angsana Primary a 0.38km walk away and heavily oversubscribed. The rental factor is a genuine 8.2 — District 18 rents grew about 7.4% a year over the decade, among the stronger suburban trends — and the 1,193-unit scale earns 8.0, deep enough for a liquid resale market and a resort-sized facilities deck. The one merely-good leg is capital appreciation at 7.4: resale homes within 1km appreciated about 3.0% a year over the past decade, and after the model's lift for Parktown's integration, scale and schools, projected growth runs to roughly 4.35% a year — comfortably clear of the 3% bar. There is no soft spot to flag; the honest caveat is what you pay for a card this clean, which is the next section.

The launch Tampines had been waiting for

Tampines North was farmland-adjacent HDB frontier until this site; Parktown is its first private integrated development, and buyers answered on day one. At the 22 February 2025 opening the project took 1,041 of 1,193 units — 87% — at a benchmark average of S$2,360 psf, one of the strongest OCR launch-weekend results in years. The tail cleared steadily through 2025 and into 2026: the latest caveat lodged on 11 June 2026, and the project now stands at roughly 99% sold, with only about a dozen units left. The action has effectively moved from the showflat to the subsale and eventual resale market, so the honest picture of "what it costs" is the project's own transacted record rather than a live balance list.

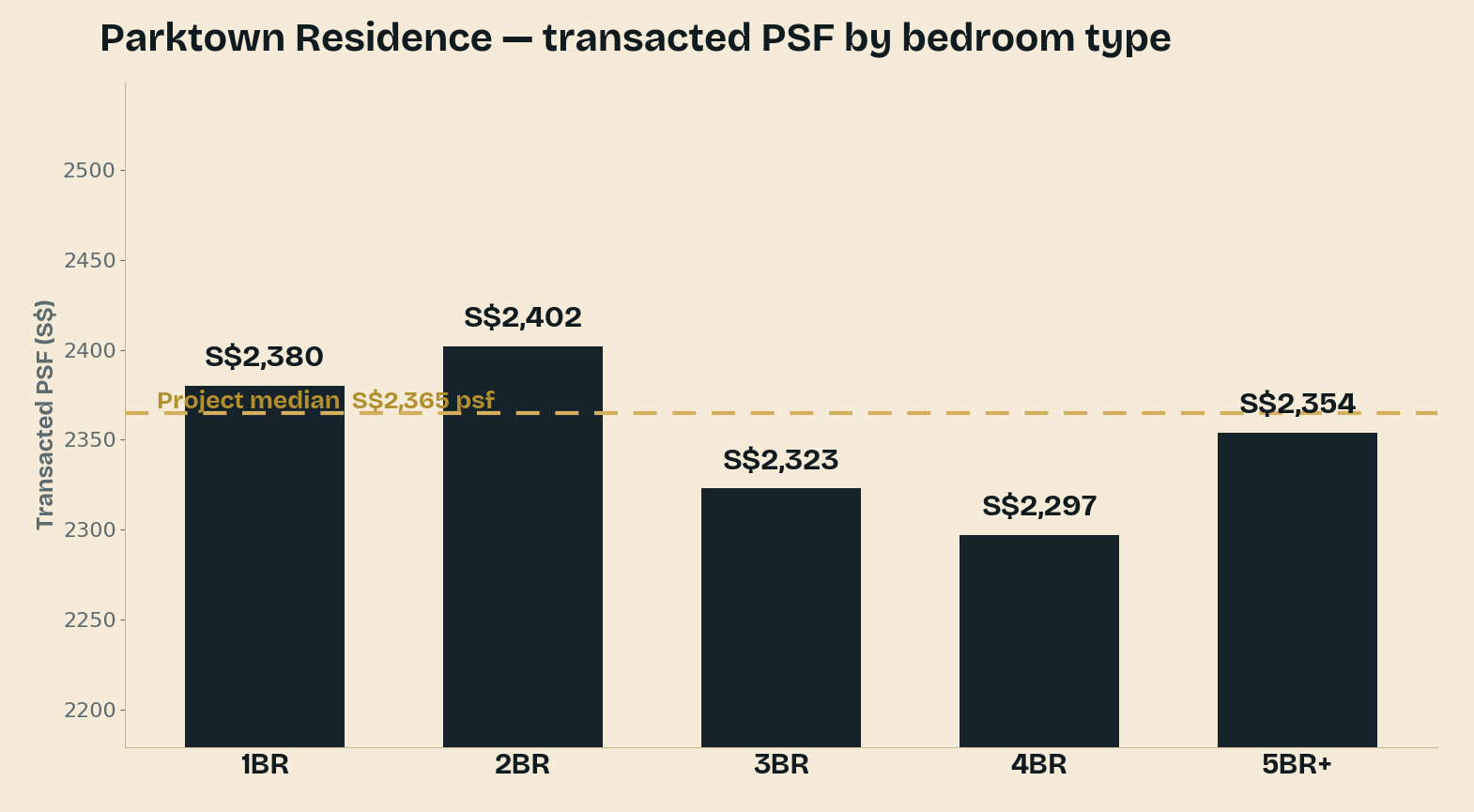

Here is what each format has transacted at, from Parktown's own URA caveats:

| Type | ~Size | Transacted PSF |

|---|---|---|

| 1 Bedroom | 463–506 sqft | S$2,380 |

| 2 Bedroom | 592–764 sqft | S$2,402 |

| 3 Bedroom | 926–1,184 sqft | S$2,323 |

| 4 Bedroom | 1,335–1,496 sqft | S$2,297 |

The pattern is the textbook integrated-launch one. The two-bedders carry the highest psf (S$2,402) — the efficient investor format with the deepest rental demand — while the larger three- and four-bedders sit lower (S$2,323 and S$2,297) on a per-foot basis, because quantum, not psf, is what stretches at that size. Across roughly 1,181 caveats the project's volume-weighted average is about S$2,365 psf. That is a remarkably tight distribution for a 1,193-unit project, which tells you the developer priced the whole stack to sell rather than holding out for premiums on the best stacks — and the 99% sell-through says the strategy worked.

The second benchmark: a new-launch premium, but roughly fair once adjusted

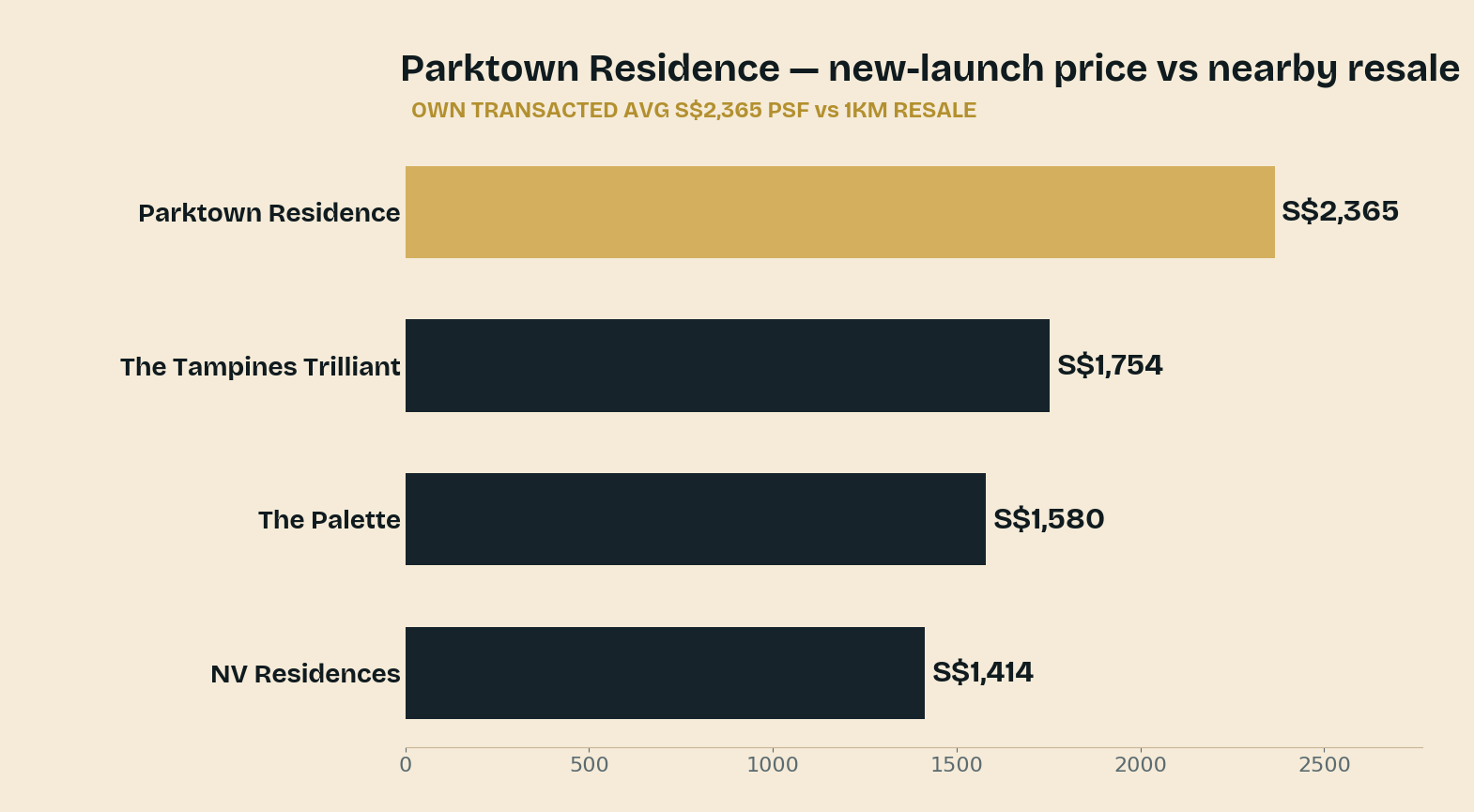

The honest question for an S-grade at a record postcode price is whether the number is a bubble over the neighbourhood or a fair premium for a new, integrated, full-lease home. The clearest test is Tampines' own leasehold resale.

| Comparable | What it is | Indicative PSF |

|---|---|---|

| Parktown Residence | 99-yr, integrated, 2025 launch | ~S$2,365 (own average) |

| The Tampines Trilliant | 99-yr, 2015, resale | ~S$1,754 |

| The Palette | 99-yr, 2015, resale | ~S$1,580 |

| NV Residences | 99-yr, 2013, resale | ~S$1,414 |

On raw psf, Parktown's ~S$2,365 runs 35% to 67% above the surrounding 99-year resale — The Tampines Trilliant near S$1,754, The Palette around S$1,580, NV Residences about S$1,414. That gap looks large until you adjust those projects for age and lease: they are decade-old buildings on shorter remaining leases, and once the scorecard normalises them to a fresh-99 equivalent, Parktown sits only a few per cent above their age-adjusted value — roughly fair, not frothy. In plain terms, you are paying a normal new-launch premium for a brand-new lease, current-spec layouts and — uniquely here — the integration, and you are not paying a bubble over what the neighbourhood is genuinely worth. That is the difference between a record price that is defensible and one that is not.

How long you'd likely hold

Using the NPS calculator's model — ~4.35% expected growth, a 3% target — here is the estimated holding period for a representative unit in each main format, at the project's own transacted median, on price growth alone and with the area's ~3.6% rental yield added.

| Available stack | PSF | Hold (price only) | Hold (with rent) |

|---|---|---|---|

| 2 Bedroom · 592–764 sqft | S$2,402 | 4–6 yrs | 4–6 yrs |

| 3 Bedroom · 926–1,184 sqft | S$2,323 | 4–6 yrs | 4–6 yrs |

| 4 Bedroom · 1,335–1,496 sqft | S$2,297 | 4–6 yrs | 4–6 yrs |

Because the modelled ~4.35% growth clears the 3% bar with real room to spare, every format exits in the same 4–6 year tier once past the four-year seller's-stamp-duty floor — there is no stranded stack here, and no format that needs rent to rescue it. What the flat table is telling you is that a buyer at the project's established median is paying fair value for the growth, so the return compounds cleanly from year four rather than waiting for a mispricing to correct. The only way to land in the faster three-to-five-year tier is to buy one of the last units below that median — a lower-floor stack in the tail — which is exactly where the final dozen units sit. With the ~3.6% District 18 yield counted, an investor's hold is comfortable across the board. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

Parktown Residence is what an S looks like when the two factors families weigh most — transport and schools — are both perfect, and nothing else on the card is broken. An MRT station and bus interchange inside the development, three primaries within a kilometre led by an oversubscribed Angsana, a strong District 18 rental trend, 1,193-unit liquidity, and projected growth near 4.35% a year: those carry the grade, and the 87% opening weekend and 99% sell-through validate them. The honest caveat is simply that a card this clean prices accordingly — at ~S$2,365 psf Parktown set a record for Tampines North — but the second benchmark shows that record is only a few per cent above the age-adjusted worth of the neighbourhood's own resale, not a bubble. For a family that wants a brand-new, full-lease home wired directly into the MRT and a top school catchment, Parktown is a deserved S. For a pure bargain hunter, the discount is gone; what is left is quality, fairly priced, and nearly sold out.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade, the five factor scores, modelled growth and rental yield per the TRIBE New Project Scorecard (URA Data Service transacted PSF; 1km resale trend lifted for project size, transport and schools; figures as at July 2026). February 2025 launch take-up (1,041 units, 87%, benchmark average S$2,360 psf) per PropertyReview and EdgeProp; integrated-development details (bus interchange, hawker centre, community club, retail, Tampines North MRT) per the developers UOL Group, Singapore Land and CapitaLand Development. Parktown per-bedroom transacted PSF and the ~S$2,365 psf project average from URA caveats via our NPS dataset (~1,181 caveats; latest 11 June 2026). The Palette, NV Residences and The Tampines Trilliant resale comparables per the TRIBE scorecard. Availability and pricing change as units sell. Scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.