Insights

Honest Insights On The Orie

The Orie grades A (8.0) on the New Project Scorecard — Toa Payoh's first private launch in eight years, a 777-unit CDL–Frasers–Sekisui development. It sold 86% at its January 2025 debut and is now about 95% sold, down to a slim tail.

By TRIBE Editorial · 8 July 2026 · 9 min read

The Orie is a 777-unit, 99-year leasehold development on Lorong 1 Toa Payoh in District 12 — twin 40-storey towers built by CDL, Frasers Property and Sekisui House, a 0.46km walk to Braddell MRT on the North-South Line, with completion due around 2030. It grades an A (8.0) on our New Project Scorecard (NPS) — one of the stronger cards we have run — and it arrived carrying real weight: it was Toa Payoh's first private residential launch in eight years, since Gem Residences in 2016. The estate answered immediately, taking 668 of 777 units — 86% — on its January 2025 opening weekend at an average of S$2,704 psf, and it has since sold down to roughly 95%. This is an honest look at what the A rests on, what a record price for the postcode actually buys, and what the slim tail is priced at. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted for the project's own size, transport and schools, not a forecast. For the holding period, we use the published NPS calculator: fair value is the transacted PSF, the project grows at its modelled rate, and we report the years needed to clear a 3% annual return — gross of stamp duty, financing and selling costs.

The scorecard: what an A actually says

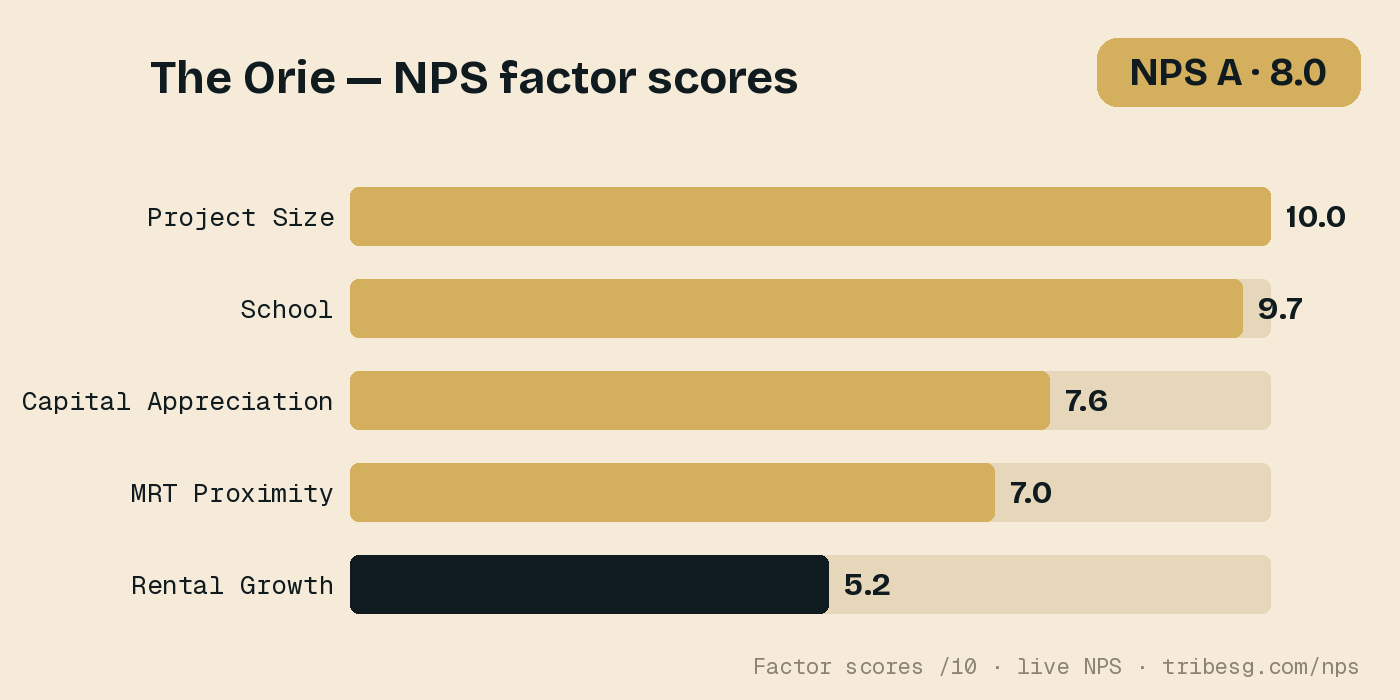

The Orie's 8.0 is a rare card with no real weak leg — four strong factors and one that is merely good.

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| Project Size | 10.0 | 777 units — ideal scale for liquidity and full facilities |

| School | 9.7 | Three primary schools within 1km; Kheng Cheng (0.42km, heavily oversubscribed) |

| Capital Appreciation | 7.6 | 1km resale grew ~3.3%/yr; lifted +1.30 for size, transport, schools → ~4.6%/yr |

| MRT Proximity | 7.0 | A 0.46km walk to Braddell MRT (North-South Line) |

| Rental Growth | 5.2 | District 12 rents grew ~5.6%/yr over the decade — healthy, not top-tier |

What makes this an A is the absence of a hole. A 777-unit project scores a full 10 on size — deep enough for a liquid resale market and a full facilities deck without feeling like a small town — and the school factor is a near-perfect 9.7, with three primary schools inside a kilometre and Kheng Cheng School a 0.42km walk away, heavily oversubscribed and a genuine draw for young families. The capital-appreciation factor is the quiet strength at 7.6: resale homes within 1km of the site grew about 3.3% a year over the past decade, and after the model's +1.30 lift for The Orie's scale, transport and schools, projected growth runs to roughly 4.6% a year — comfortably clear of the 3% bar, which is unusual for a mature central estate. The two merely-good legs are transport — a genuine but not-integrated 0.46km walk to Braddell MRT — and rent: District 12 rents grew about 5.6% a year, healthy without being the standout you see in the East or Jurong. There is no soft spot to flag here; the honest caveat is about price, not the card, and that is the next section.

The launch Toa Payoh had been waiting for

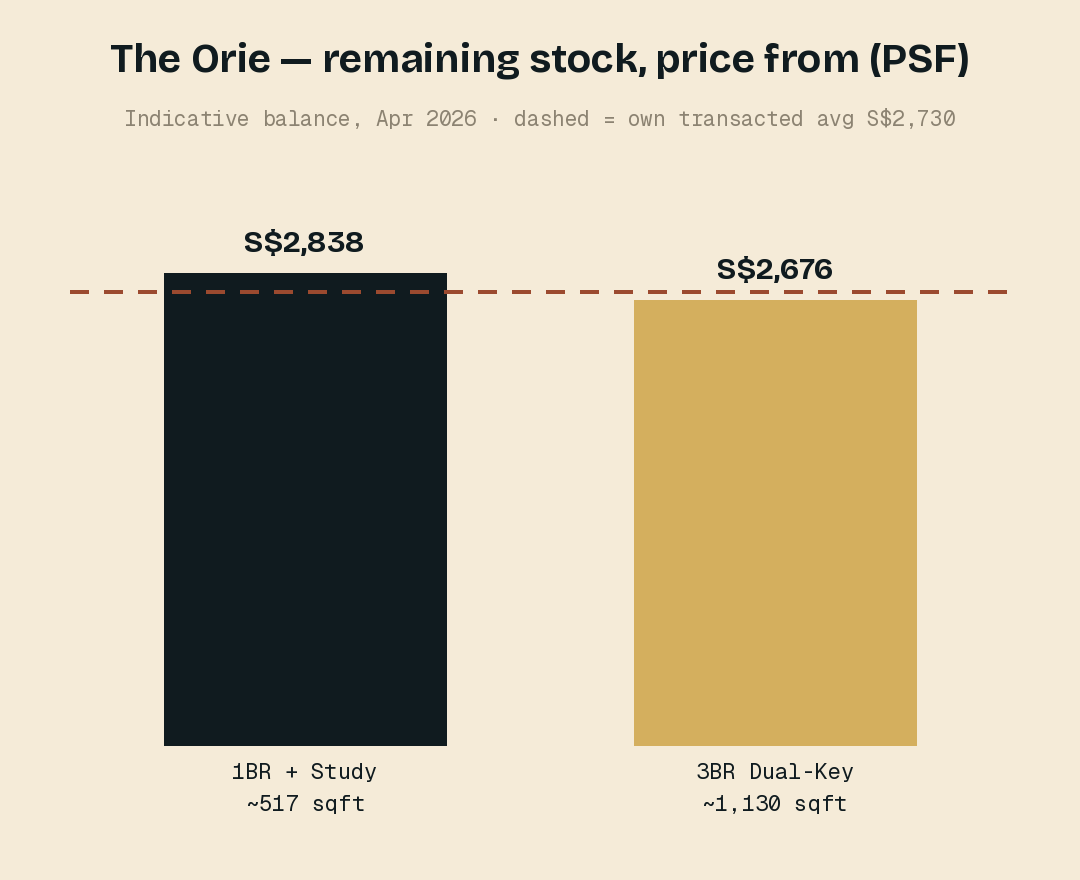

The Orie's story is a scarcity story. Toa Payoh had not seen a private launch since Gem Residences in 2016, and the site itself set a marker before a single unit was sold: CDL's consortium paid a record S$1,360 psf per plot ratio (S$968 million) for the land at the November 2023 tender, 18% above the next bid. When sales opened on 18 January 2025, the project took 668 of 777 units — 86% — at an average of S$2,704 psf, drawing about 8,000 visitors to the gallery over the preview. By March 2026 it was roughly 95% sold — around 739 units — and the remaining stock has narrowed to two rare layouts:

| Type | ~Size | Price from | PSF from |

|---|---|---|---|

| 1 Bedroom + Study | ~517 sqft | S$1.47m | S$2,838 |

| 3 Bedroom (Dual-Key) | ~1,130 sqft | S$3.02m | S$2,676 |

Against the project's own transacted record — an average of about S$2,730 psf across roughly 739 caveats since the January 2025 launch — the two remaining formats sit on either side of the line. The 1-bedroom-plus-study, from about S$2,838 psf, carries the usual small-format premium, running a touch above the project average; the 3-bedroom dual-key, from about S$2,676 psf, sits just below it, which is what you would expect of a larger, more specialised layout. Neither is a fire sale and neither is a stretch — the developer is clearing a genuine tail at close to the price the other 739 buyers paid. Note that these are indicative balance figures from the marketing agents as at April 2026; availability and pricing move as the last units sell.

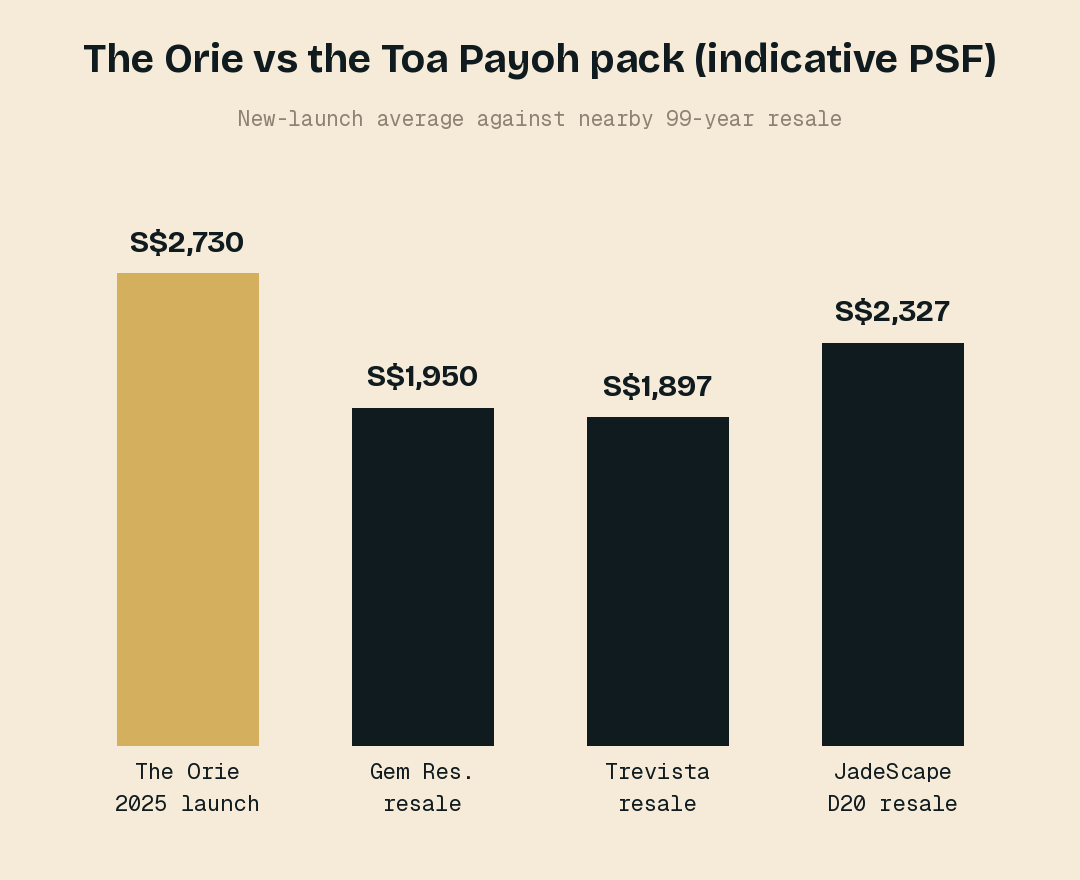

The second benchmark: a record price for the postcode

The Orie's honest caveat is not the scorecard — it is what you pay for the address. The clearest way to see it is against Toa Payoh's own resale.

| Comparable | What it is | Indicative PSF |

|---|---|---|

| The Orie | 99-yr, Lorong 1 Toa Payoh, 2025 launch | ~S$2,730 (own average) |

| JadeScape | 99-yr, Marymount (D20), resale | ~S$2,327 |

| Gem Residences | 99-yr, Toa Payoh, 2016 launch | ~S$1,950 (resale) |

| Trevista | 99-yr, Toa Payoh, resale | ~S$1,897 |

The Orie's ~S$2,730 psf runs roughly 40% above the best nearby 99-year resale — Gem Residences at about S$1,950 psf and Trevista near S$1,897 — and about 17% above JadeScape (~S$2,327), the nearest large modern leasehold comparable one district over. That gap is the new-launch premium: a fresh 99-year lease, current-spec layouts after the GFA-harmonisation rules shrank bay windows and planter voids, and the scarcity of any new supply in the estate. It is not mispriced — the 86% opening weekend and the 95% sell-through say the market accepted it — but a buyer should be clear-eyed that the entry price already reflects the A-grade fundamentals rather than sitting below them. You are paying today for the postcode, the schools and the scale; the return has to come from growth on top of a full price.

How long you'd likely hold

Using the NPS calculator's model — ~4.6% expected growth, a 3% target — here is the estimated holding period for each remaining stack, on price growth alone and with the area's ~3.2% rental yield added.

| Available stack | PSF | Hold (price only) | Hold (with rent) |

|---|---|---|---|

| 1 Bedroom + Study · ~517 sqft | S$2,838 | 4–6 yrs | 3–5 yrs |

| 3 Bedroom Dual-Key · ~1,130 sqft | S$2,676 | 3–5 yrs | 3–5 yrs |

Because the modelled ~4.6% growth clears the 3% bar with room to spare, both remaining formats exit relatively quickly. The 3-bedroom dual-key, priced just below the project's own average, clears fastest — in the three-to-five-year tier on price growth alone, and rent does not change that. The 1-bedroom-plus-study, at its small-format premium above the average, lands in the four-to-six-year tier on price alone, and the ~3.2% rent pulls it into the three-to-five-year range. Read plainly, this is the profile of a strong A near sell-out: there is no long, stranded stack here, because the growth engine is doing real work rather than leaning on rent. The honest qualifier is the entry price in the section above — the model's clean exits assume you bought at the project's established level, not above it. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

The Orie is what an A looks like when scale, schools and a credible growth engine all line up and nothing on the card is broken. A full-10 777-unit development, three primaries within a kilometre led by an oversubscribed Kheng Cheng, a 0.46km walk to Braddell MRT, and projected growth near 4.6% a year — those carry the grade, and the 86% opening weekend and 95% sell-through validate them. The one honest caveat is price: at ~S$2,730 psf the project sits about 40% above Toa Payoh resale, a record for the estate, so the A-grade fundamentals are already in the entry price rather than waiting to be discovered. For a family that wants the schools, the scale and a fresh lease in a mature, well-connected estate — and is buying one of the last two formats at close to what everyone else paid — The Orie is a deserved A. For a pure value hunter, the discount is not here; the quality is.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade, the five factor scores, modelled growth and rental yield per the TRIBE New Project Scorecard (URA Data Service transacted PSF; 1km resale trend lifted for project size, transport and schools; figures as at July 2026). January 2025 launch take-up (668 units, 86%, average S$2,704 psf) and the "first Toa Payoh private launch since 2016" per CDL and EdgeProp; the record S$1,360 psf ppr land bid per EdgeProp. Cumulative ~95% sell-through (March 2026), the project's ~S$2,730 psf transacted average and the remaining-stock pricing per EdgeProp, Stacked Homes and marketing-agent balance lists; availability changes as units sell. Comparable indicative PSF for Gem Residences, Trevista and JadeScape per EdgeProp / SRX / 99.co transaction data; District 12 gross rental yield (~3.2%) per public District 12 rental data. Scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.