Insights

Honest Insights On Meyer Blue

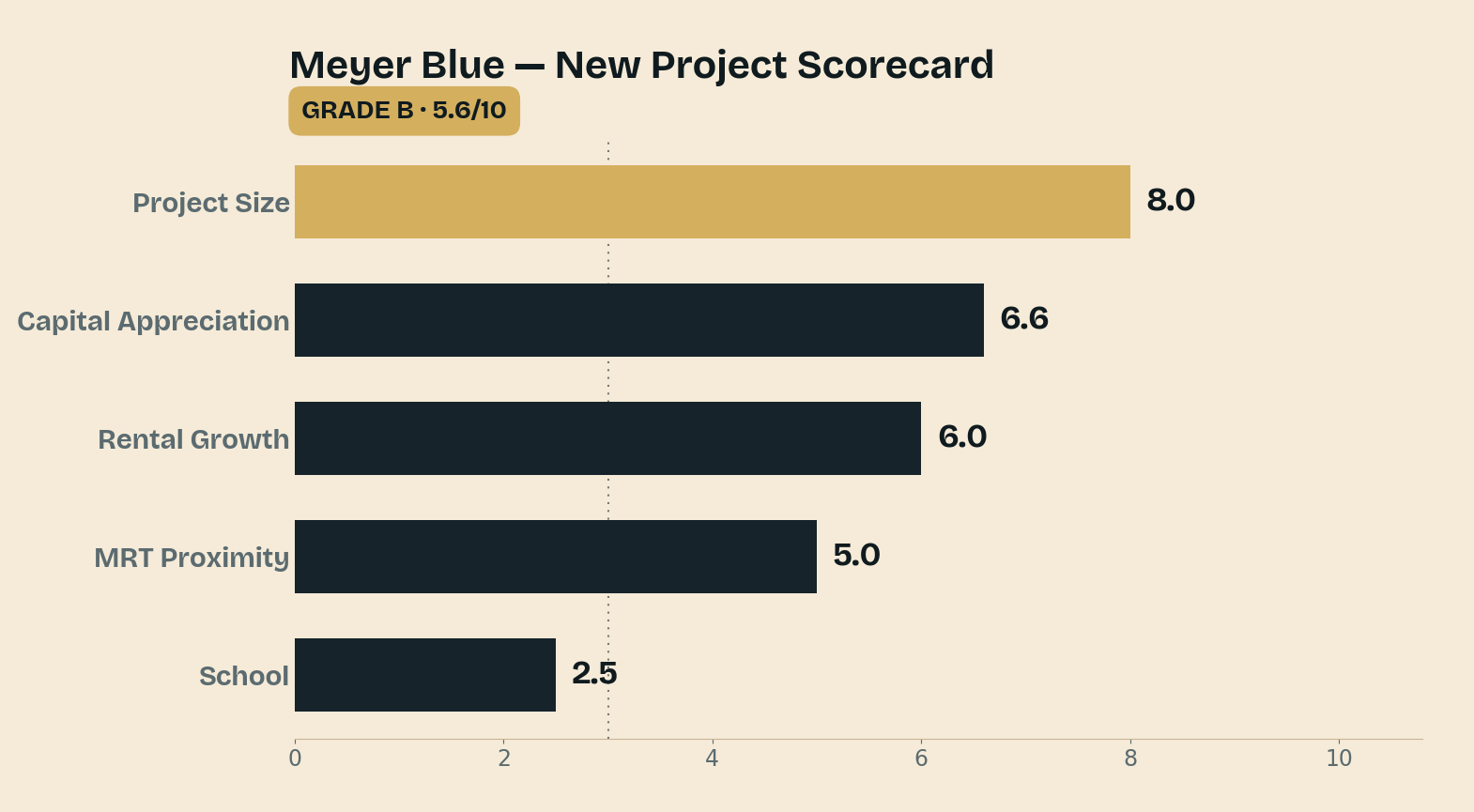

Meyer Blue grades B (5.6) on the New Project Scorecard — a 226-unit freehold tower on Meyer Road by UOL and SingLand. Strong on tenure and scale, held back by no school within 1km and price growth that clears 3% by a hair.

By TRIBE Editorial · 9 July 2026 · 9 min read

Meyer Blue is a 226-unit, freehold development at 81 Meyer Road in District 15 — a single 26-storey tower by UOL Group and Singapore Land, a 0.61km walk to Katong Park MRT on the Thomson–East Coast Line, with completion due December 2028. It grades a B (5.6) on our New Project Scorecard (NPS) — a middling card with a clear split. Freehold tenure on the Meyer Road ridge and a full-sized 226-unit development are the strengths; a missing school catchment and a growth engine that only just clears 3% are the offset. This is an honest look at what the B rests on, what the larger-format tail costs, and how long you would likely need to hold each. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design. For the holding period, we use the published NPS calculator: fair value is the median transacted PSF for each bedroom type, the project grows at its modelled rate, and we report the years needed to clear a 3% annual return — gross of stamp duty, financing and selling costs.

The scorecard: a card that splits

Meyer Blue's 5.6 is the average of a solid top and a weak floor.

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| Project Size | 8.0 | 226 units — a full-sized development with proper facilities |

| Capital Appreciation | 6.6 | 1km resale grew ~3.3%/yr over the decade; barely lifted (+0.02) |

| Rental Growth | 6.0 | District 15 rents grew ~6.1%/yr over the decade |

| MRT Proximity | 5.0 | A 0.61km walk to Katong Park MRT (Thomson–East Coast Line) |

| School | 2.5 | No primary school within 1km — the card's clear weak spot |

The strengths are real and durable. Freehold tenure on the Meyer Road ridge — a district that is mostly leasehold near the coast — is exactly the trait the scorecard rewards over a long hold, and at 226 units the project earns a full 8.0 on scale, deep enough for a proper facilities deck and a liquid resale pool. But two things hold the grade to a B. The first is the 2.5 on schools: there is no primary school within a kilometre, which the model reads as weaker family demand. The second matters more for returns: the growth engine is thin. Resale homes within 1km appreciated about 3.3% a year over the past decade — a same-property resale basis that strips out new-launch inflation — and because Meyer Blue is a mid-sized project with no standout scale or transport edge, the model's quality lift is essentially nil (+0.02). Projected growth lands at about 3.29% a year — it clears the 3% bar, but by a hair. That single fact shapes the whole holding-period read below.

What's left — and what it costs

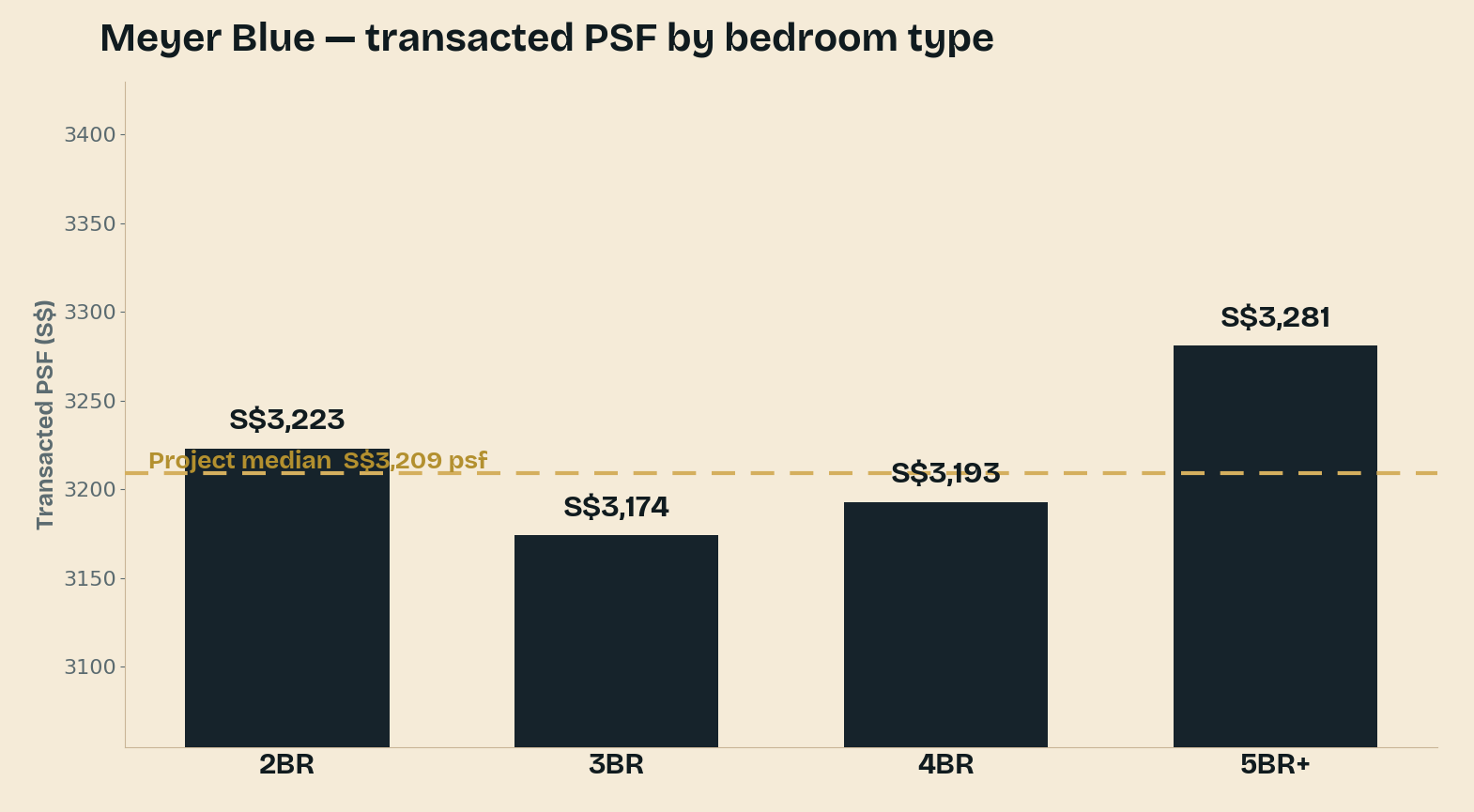

Meyer Blue launched in October 2024, selling over 50% of its 226 units on opening weekend at an average of S$3,260 psf, with two penthouses going for S$10.08 million (S$3,418 psf) and S$10.28 million (S$3,436 psf). Sales have compounded steadily since: as at 15 June 2026 the project is 177 of 226 units sold — 78% — leaving roughly 49 units, and those are now weighted to the larger formats. The entry-level compact stock is gone; what remains is three-, four- and five-bedroom apartments, from about S$3.0 million for a three-bedder to around S$6.0 million for a five-bedroom suite, with availability changing as units sell.

Here is what each format has transacted at, from the project's own URA caveats:

| Type | ~Size | Transacted PSF |

|---|---|---|

| 2 Bedroom | 667–710 sqft | S$3,223 |

| 3 Bedroom | 990–1,141 sqft | S$3,174 |

| 4 Bedroom | 1,518–1,733 sqft | S$3,193 |

| 5 Bedroom+ | 1,905–2,992 sqft | S$3,281 |

The distribution is unusually flat — every format clusters within about 3% of the project's ~S$3,209 psf average, from the two-bedders at S$3,223 to the five-bedders at S$3,281. That tells you Meyer Blue is priced by the ridge and the freehold, not by format arbitrage: you pay roughly the same per foot whichever door you take, so the choice among the remaining larger units is a quantum-and-space decision, not a value one. There is no deep-discount stack in the tail — the leftover stock is priced in line with everything that has already sold.

The second benchmark: the newest of the Amber Road freeholds

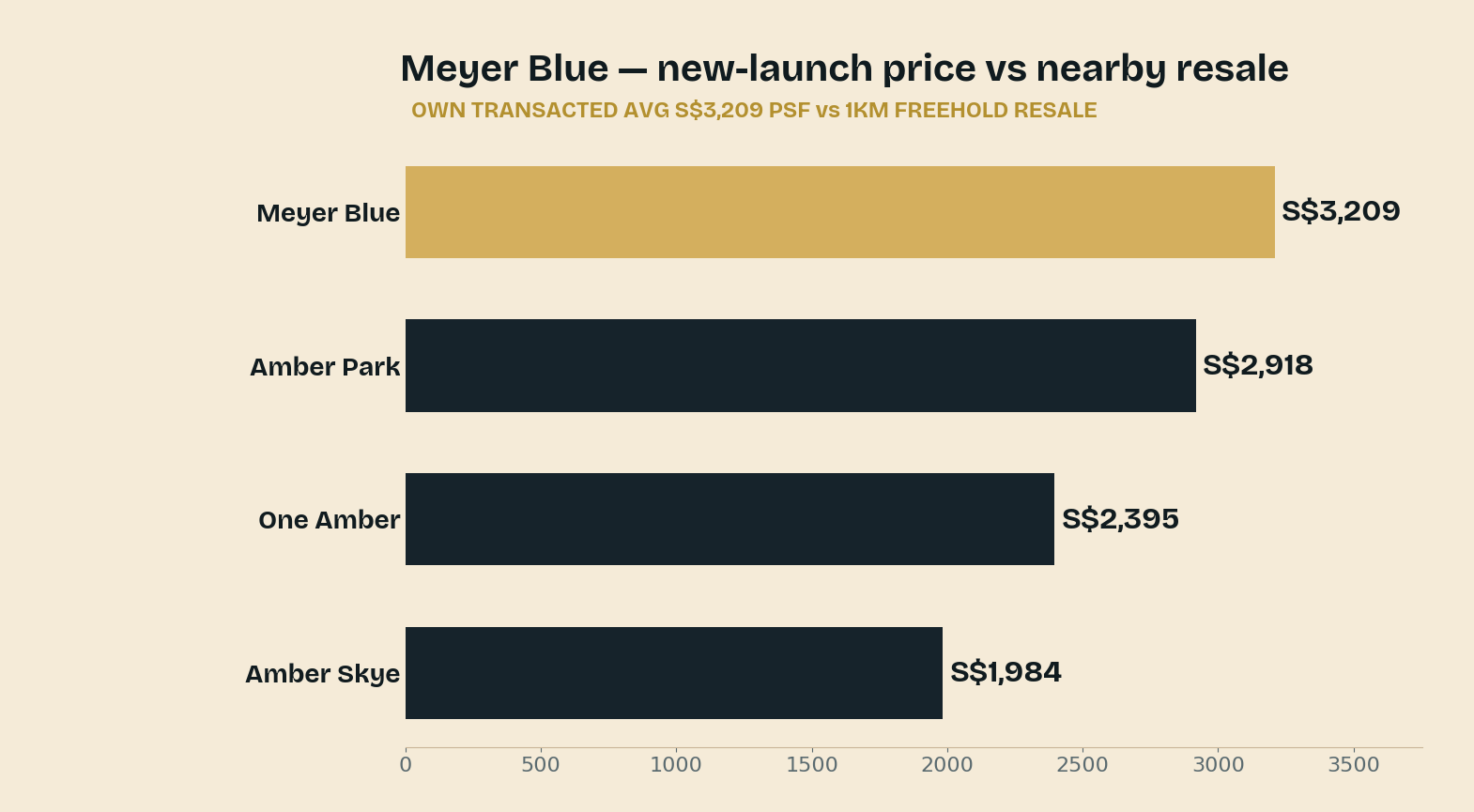

Against nearby transactions, Meyer Blue's level reflects a new-launch premium stacked on genuine freehold scarcity — and the fairest yardstick is the freehold pack it sits among.

| Comparable | Tenure · what | Distance | Recent PSF |

|---|---|---|---|

| Meyer Blue | Freehold, 2024 launch | — | ~S$3,209 (own median) |

| Amber Park | Freehold, 2023 | 0.94 km | ~S$2,918 |

| One Amber | Freehold, 2010 | 0.90 km | ~S$2,395 |

| Amber Skye | Freehold, 2017 | 0.79 km | ~S$1,984 |

Meyer Blue's ~S$3,209 psf runs about 10% above Amber Park — the newest freehold comparable, a 2023 completion — and further above the older freehold stock, One Amber near S$2,395 and Amber Skye around S$1,984. Read honestly, that ~10% over Amber Park is the ordinary new-launch premium: a fresh building, current-spec layouts and no renovation drag. The wider gaps to One Amber and Amber Skye are mostly age — those are 2010 and 2017 buildings that would price much closer to Meyer Blue if they were new today. So the buyer's real question is narrow and answerable: is a brand-new freehold worth roughly a tenth more than a two-year-old freehold a few streets away? For a long-hold owner it usually is; for an investor it tightens an already-thin return.

How long you'd likely hold

Using the NPS calculator's model — ~3.29% expected growth, a 3% target — here is the estimated holding period for each remaining stack, on price growth alone and with the area's ~3.0% rental yield added.

| Available stack | PSF | Hold (price only) | Hold (with rent) |

|---|---|---|---|

| 3 Bedroom · 990–1,141 sqft | S$3,174 | 4–6 yrs | 4–6 yrs |

| 4 Bedroom · 1,518–1,733 sqft | S$3,193 | 4–6 yrs | 4–6 yrs |

| 5 Bedroom+ · 1,905–2,992 sqft | S$3,281 | 4–6 yrs | 4–6 yrs |

The modelled 3.29% growth does clear the 3% bar, so on price alone every remaining format reaches a 3% return in the 4–6 year tier past the seller's-stamp-duty floor — but only just. The margin over 3% is about three-tenths of a percentage point, so price growth on its own leaves almost no cushion for stamp duty, financing and selling costs. What makes the hold comfortable is the ~3.0% rental yield: with rent counted, the same stacks clear the 4–6 year tier with real room to spare. That is the honest way to read Meyer Blue — a freehold-and-yield hold, where the tenure and the income do the work, not a capital-growth play riding a strong district trend. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

Meyer Blue is a clean freehold on one of the East Coast's best-known addresses, and for a long-hold owner that tenure is the whole case. But the scorecard is honest about the trade. The B (5.6) is a solid top — freehold, 226-unit scale, a healthy District 15 rental trend — averaged against a real weak floor: no primary school within a kilometre, a middling walk to the MRT, and a growth engine that clears 3% by a hair. The numbers say the same thing twice: at ~S$3,209 psf you are paying a normal new-launch premium over the newest freehold nearby, and the modelled growth needs the ~3.0% rental yield to make the hold comfortable. For an owner-occupier who values freehold on Meyer Road and is buying space rather than a bargain, that is a defensible, eyes-open purchase. For an investor chasing capital growth, a higher-graded launch will likely compound faster — Meyer Blue's return is a tenure-and-yield story, and it is best bought as one.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade, the five factor scores, modelled growth and rental yield per the TRIBE New Project Scorecard (URA Data Service transacted PSF; 1km resale trend lifted for project size, transport and schools; figures as at July 2026). October 2024 launch take-up (over 50% of 226 units, average S$3,260 psf, two penthouses at S$10.08m and S$10.28m) per EdgeProp. The 78%-sold balance (177 of 226, ~49 units) as at 15 June 2026 and remaining larger-format pricing per 99.co and marketing-agent balance lists; availability changes as units sell. Meyer Blue per-bedroom transacted PSF and the ~S$3,209 psf project median from URA caveats via our NPS dataset (~178 caveats). Amber Park, One Amber and Amber Skye freehold resale comparables per the TRIBE scorecard. Scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.