Insights

Honest Insights On The Continuum

The Continuum grades B (6.5) on the New Project Scorecard — Hoi Hup and Sunway's 816-unit freehold Katong project sold just 26.5% at launch in May 2023, but sits at 95% three years later, with a 42-unit big-format tail priced below its own record.

By TRIBE Editorial · 14 July 2026 · 12 min read

The Continuum is an 816-unit freehold development on Thiam Siew Avenue in Katong, District 15 — a twin-plot project by Hoi Hup Realty and Sunway Developments, linked by a sky bridge, on land the pair bought for S$815 million (about S$1,488 psf ppr) in November 2021. It grades a B (6.5) on our New Project Scorecard (NPS), and its sales history is the inverse of a launch-weekend story: a 26.5% opening in May 2023 that the market read as a stumble, followed by three years of steady sell-through to 95% sold — 42 units left on the 14 July 2026 balance chart, with June 2026 caveats printing as high as S$3,019 psf. This is a look at what the B is made of, what the slow-burn sell-down actually proved, and how a tail of S$4.5–5.9 million family units prices against the project's own record. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted for the project's own size, transport and schools, not a forecast.

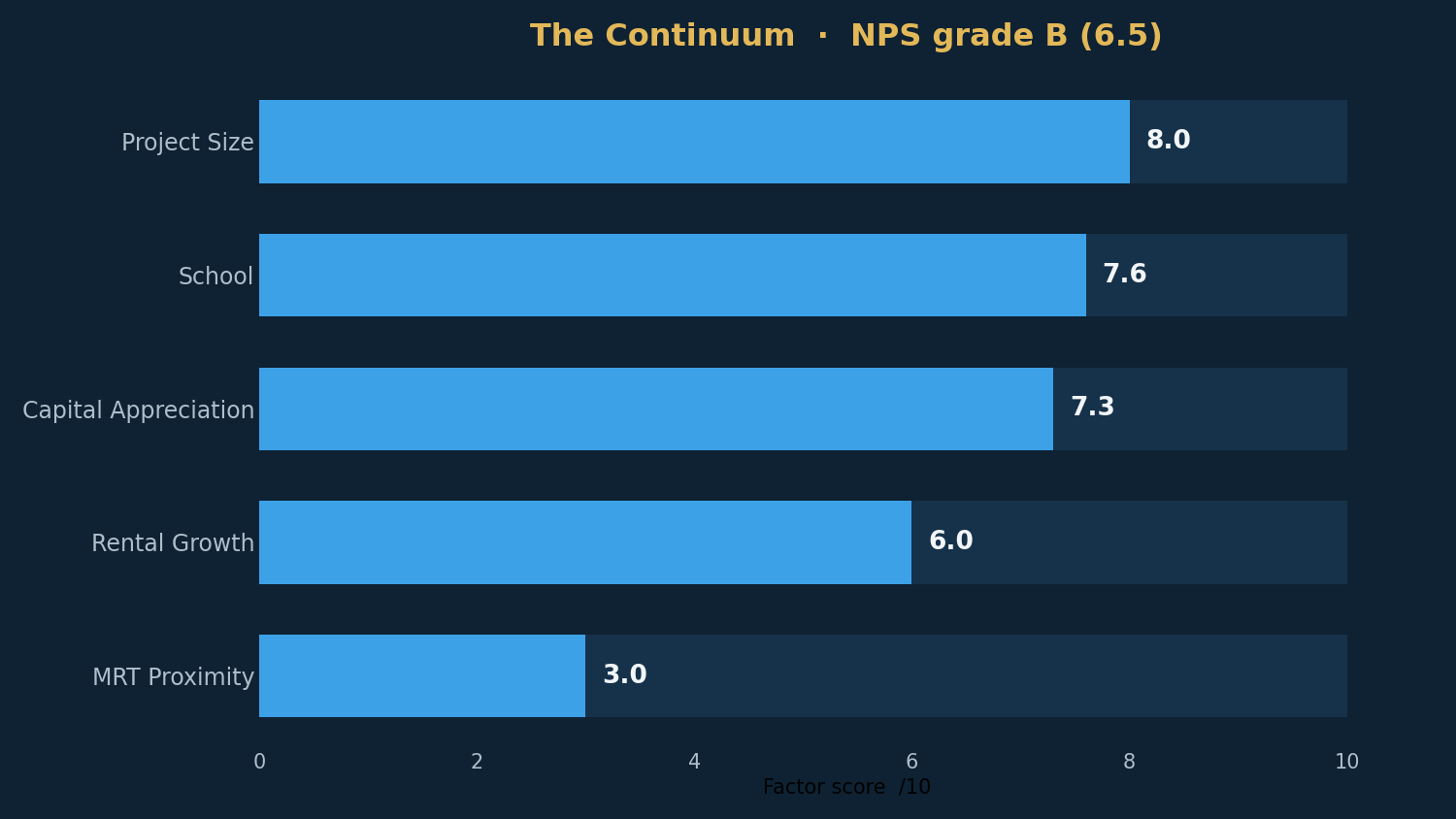

The scorecard: what the B actually says

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| Project Size | 8.0 | 816 units — ideal scale for liquidity and facilities |

| School | 7.6 | 3 primaries within 1km; Haig Girls' (0.81km) heavily oversubscribed |

| Capital Appreciation | 7.3 | 1km resale grew ~3.5%/yr; lifted for size, transport, schools → ~3.8%/yr |

| Rental Growth | 6.0 | District 15 rents grew ~6.1%/yr over the decade |

| MRT Proximity | 3.0 | A 0.89km walk to Dakota MRT (Circle Line) — the card's hole |

The engine is honest rather than spectacular. Resale homes within a kilometre of Thiam Siew Avenue — and there are 158 resale projects inside that ring, one of the densest comp sets on our board — appreciated about 3.5% a year over the past decade on a same-property basis, and the model lifts that +0.31 for the project's size, transport and schools, to a projected ~3.8% a year — clearing the 3% bar with a workable margin. Size scores 8.0 at 816 units, and schools score 7.6, with heavily-oversubscribed Haig Girls' at 0.81km and Tanjong Katong Primary and Kong Hwa also inside the kilometre — a real family card, though not the sub-0.5km ballot lock its neighbour Tembusu Grand carries.

The two honest caveats sit at the bottom of the card. Rental growth at 6.0 is D15's story — healthy at ~6.1% a year but a tier below the 7%-plus districts — and the modelled gross yield is 3.02%, thinned by East Coast pricing. And MRT scores 3.0: the OneMap walk to Dakota on the Circle Line is 0.89km, and unlike Tembusu Grand's Thomson-East Coast Line story, no new station is coming closer. Buyers here paid for freehold and the school ring, not the train.

The launch that looked like a stumble, and wasn't

Context matters for the land price: the S$815 million Thiam Siew Avenue acquisition was one of the largest freehold residential land deals Singapore had seen in years, done by private treaty in November 2021 at roughly S$1,488 psf ppr — struck before the GLS records that repriced Katong (Tembusu Grand's S$1,302 psf ppr in January 2022, Grand Dunman's S$1,350 that May, both for 99-year land). The launch weekend of 6–7 May 2023 moved 216 of 816 units (26.5%) at an average of S$2,732 psf — a soft opening for the year's biggest freehold launch, read at the time as buyers balking at the freehold premium.

The next three years re-read that verdict. By December 2024, EdgeProp's caveat analysis named The Continuum the top beneficiary of Emerald of Katong's sell-out spillover, transacting at an average of about S$2,788 psf. The developer's chart hit ~83% by December 2025, and the sell-down never stopped: the official sold-log shows five to ten units clearing in most fortnights of 2026, and URA caveats record 529 transactions in the 36 months to June 2026 alone, at an average of S$2,819 psf (range S$2,390–3,121) — with June 2026 units printing up to S$3,019 psf. By the 14 July 2026 balance chart, 42 units remain: 95% sold, without a completed building to show — the developer's stated outside date for TOP is 17 November 2027.

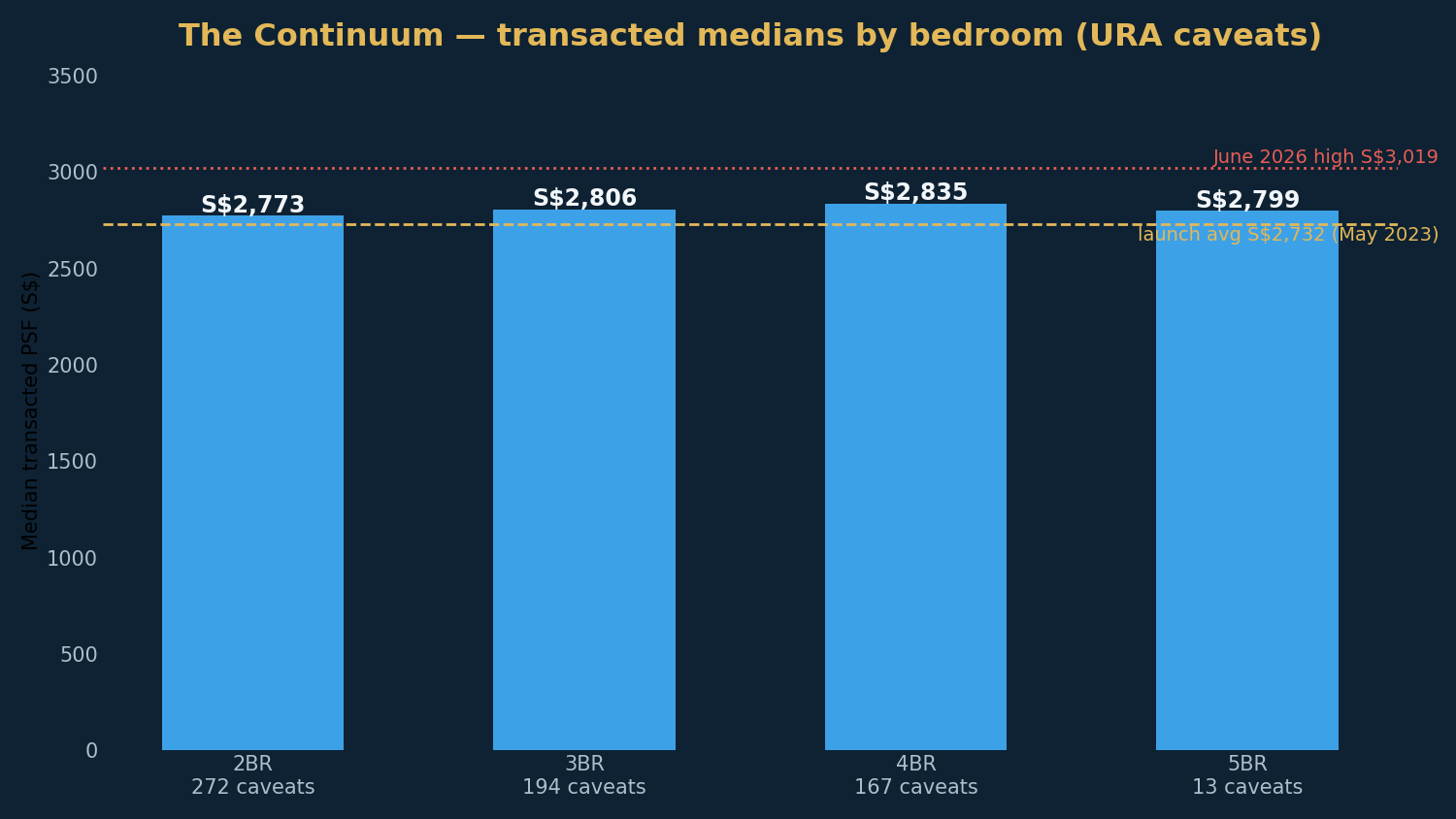

What the project has transacted at, by bedroom (URA caveats via the live scorecard, May 2023–June 2026):

| Type | Typical size | Median PSF | Caveats |

|---|---|---|---|

| 2 Bedroom | 700 sqft | S$2,773 | 272 |

| 3 Bedroom | 1,066 sqft | S$2,806 | 194 |

| 4 Bedroom | 1,249 sqft | S$2,835 | 167 |

| 5 Bedroom | 1,905 sqft | S$2,799 | 13 |

What's left: a big-family shelf, priced below its own record

Per the developer's price table (14 July 2026), the 42 remaining units are heavily weighted to the largest formats — 11 of 32 4-Bedroom Premier units (1,700–2,067 sqft, S$4.481–5.799 million) and 23 of 32 5-Bedroom units (1,905–2,282 sqft, S$5.087–5.871 million) — plus a thin scatter: two 560 sqft 1BR+Study at S$1.48 million (S$2,643 psf), one 3-Bedroom at S$2.959 million, one 3-Bedroom Premier at S$3.165 million, three 3-Bedroom+Study from S$3.502 million, and one 4-Bedroom at S$4.103 million. Every 2-bedroom format — 306 units across three types — is fully sold.

Against the project's own record — the in-project benchmark — this tail is unusual in the same way Tembusu Grand's was: it is not priced above the record. The 4BR Premier entry works out to about S$2,636 psf on the smallest 1,700 sqft layout — 7% below the project's S$2,835 four-bedroom median (167 caveats), and recent 4BR Premier caveats have printed S$2,672–3,007 psf. The 5-Bedroom entry is about S$2,670 psf on 1,905 sqft — 5% below the S$2,799 five-bedroom median (13 caveats — a thin band, read it loosely), with June 2026 five-bedders transacting at S$2,690–2,798 psf. Even the two remaining one-bedders at S$1.48 million are priced at exactly the level the last three 560 sqft caveats cleared (S$2,644 psf). Compare Faber Residence's tail at +6–11% over its own median, or Elta's D1 stacks at +21%: this shelf is asking the transacted price, not a premium for being last.

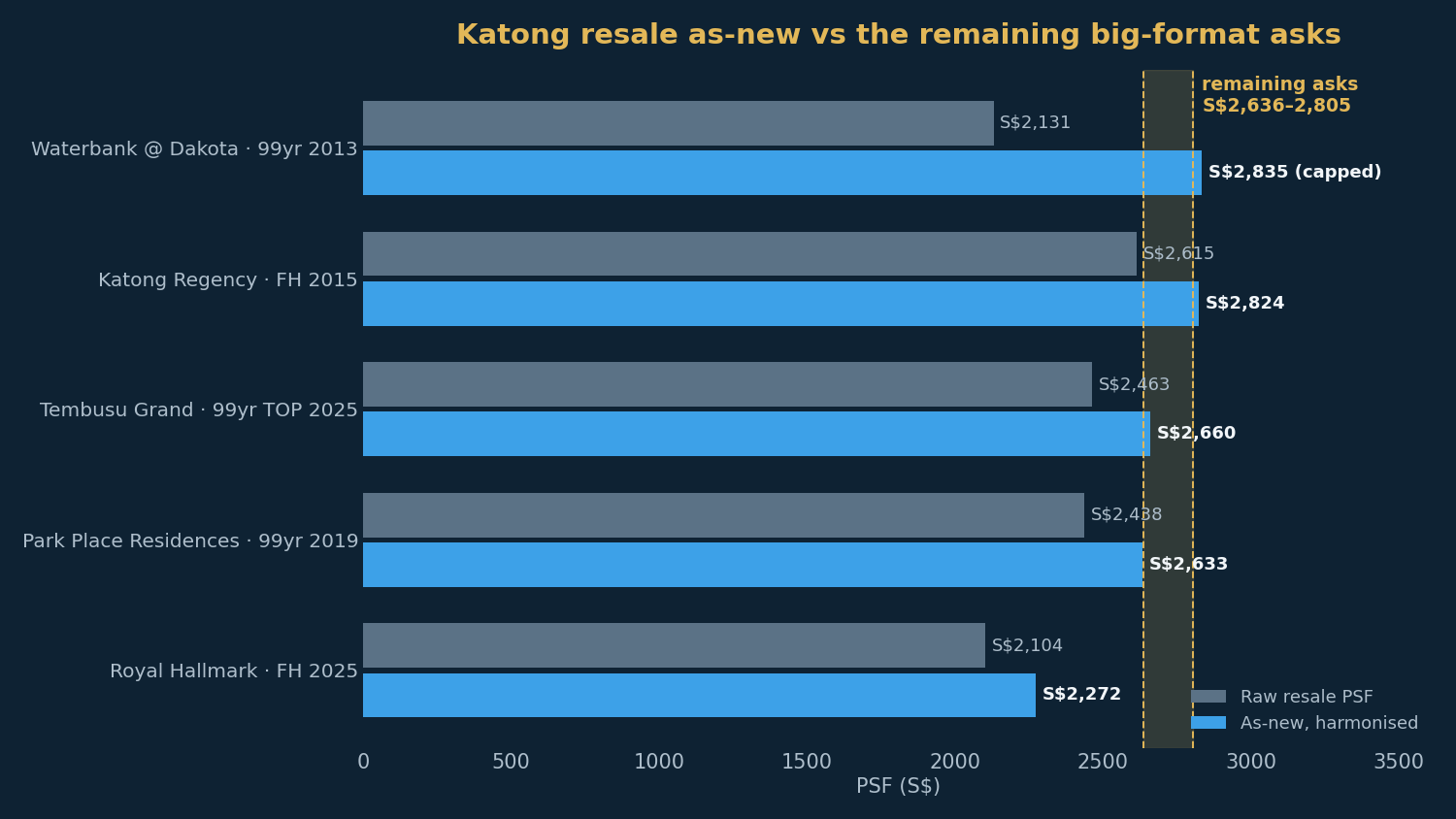

The benchmark: Katong resale, adjusted honestly

Raw PSF comparisons mislead here in both directions, so we lift each comparable to a like-for-like, as-new footing: lease/age adjustment (Bala's Table, converting leasehold comps to a fresh-99 equivalent) plus +8% GFA harmonisation for three-bedders and larger, since these comps pre-date the 22 January 2023 strata-area rules (The Continuum itself, with planning permission before that line, is also non-harmonised — so this bridge, which lifts only the comps, is conservative against the project). The NPS calculator caps each adjusted comp at the project's own median.

| Comparable | Raw resale PSF | As-new, harmonised |

|---|---|---|

| The Continuum · 4BR Premier (remaining) | — | S$2,636–2,805 (asking) |

| The Continuum · 4BR (own median) | — | S$2,835 |

| Waterbank @ Dakota (99yr, 2013, 0.94km) | S$2,131 | ~S$2,835 (capped) |

| Katong Regency (freehold, 2015, 0.40km) | S$2,615 | ~S$2,824 |

| Tembusu Grand (99yr, TOP 2025, 0.63km) | S$2,463 | ~S$2,660 |

| Park Place Residences (99yr, 2019, 0.63km) | S$2,438 | ~S$2,633 |

| Royal Hallmark (freehold, 2025, 0.36km) | S$2,104 | ~S$2,272 |

Read plainly: the adjusted belt runs S$2,272–2,835, and the remaining asks (S$2,636–2,805 psf) sit inside it — level with the mature-99-year names lifted to as-new, below the capped Waterbank and the freehold Katong Regency. The cluster tells the same story at raw prices: Tembusu Grand's 2026 sub-sales have printed to S$2,881 psf on 99-year land, Emerald of Katong launched at S$2,621 average, and this project's own June 2026 caveats reached S$3,019. A freehold asking S$2,6xx–2,8xx in that fabric is not stretching; the stretch is the quantum, to which we now turn.

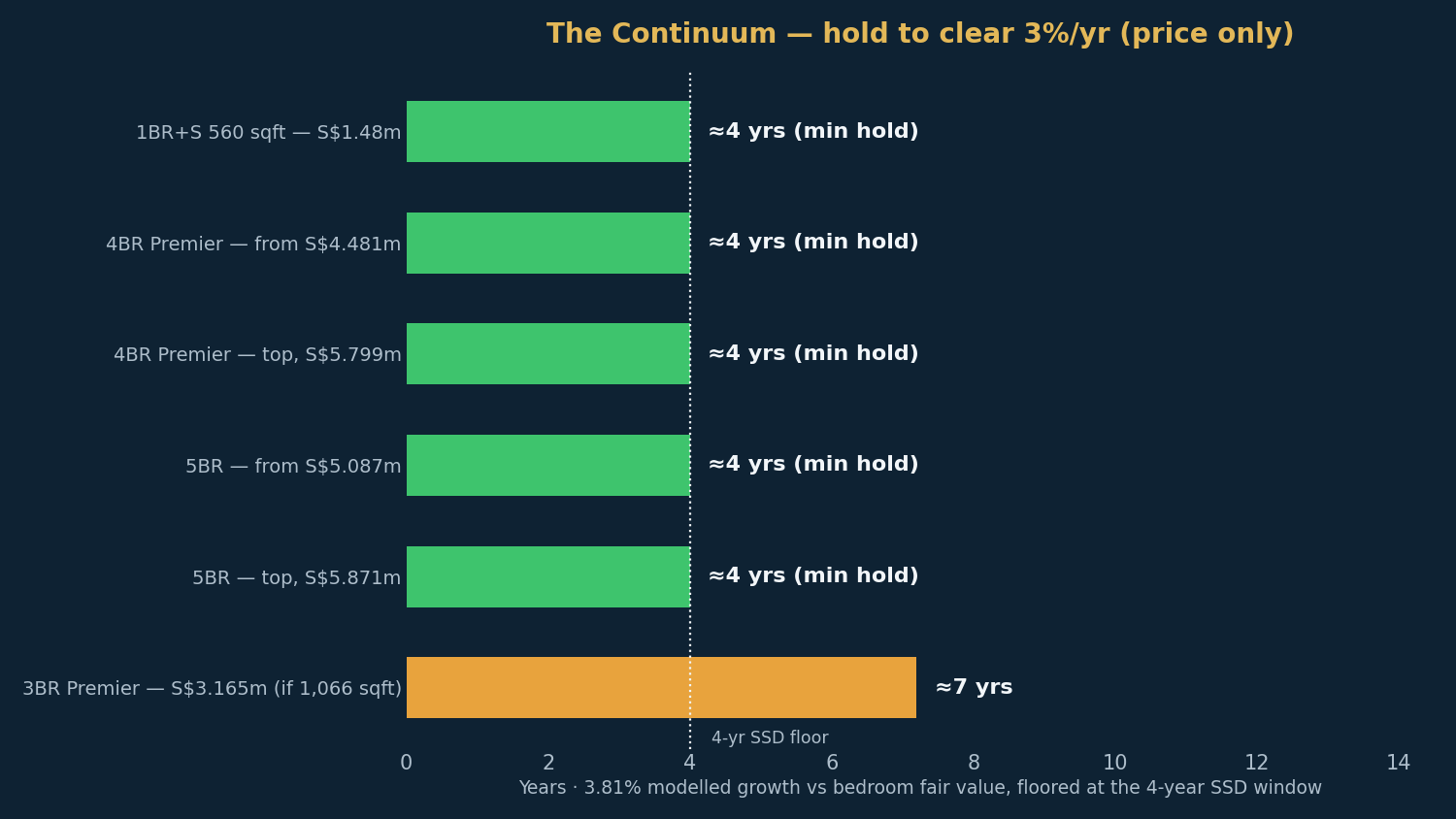

How long you'd likely hold

Seller's stamp duty runs for four years (16%, 12%, 8%, 4%), so no exit before year four is realistic, and the shortest tier we publish is four-to-six years. Using the NPS calculator's model — 3.81% expected growth, a 3% target — here is the estimated holding period for each remaining stack, on price growth alone, against the bedroom's own transacted median as the fair-value anchor.

| Available stack | PSF | Hold (price only) |

|---|---|---|

| 1BR+Study 560 sqft — S$1.48m (2 units) | S$2,643 | 4–6 yrs |

| 3BR / 3BR+Study singles — S$2.959–4.15m | S$2,593–2,854 | 4–6 yrs |

| 3BR Premier — S$3.165m (if the 1,066 sqft layout) | S$2,969 | 6–10 yrs |

| 4BR Premier — from S$4.481m | S$2,636 | 4–6 yrs |

| 4BR Premier — top of range, S$5.799m | S$2,805 | 4–6 yrs |

| 5BR — from S$5.087m | S$2,670 | 4–6 yrs |

| 5BR — top of range, S$5.871m | S$2,573 | 4–6 yrs |

With a 3.81% growth engine and entries at or below the fair-value anchors, almost the whole shelf clears the 3% bar inside the minimum realistic hold: the four-to-six-year tier stretches to S$2,971 psf on the four-bedroom band and S$2,934 on the five-bedroom band, comfortably above every current ask. The one exception is the single 3-Bedroom Premier if it is the compact 1,066 sqft layout (S$2,969 psf — a six-to-ten-year read); on its larger 1,302 sqft layout the same S$3.165 million is S$2,431 psf and clears easily — ask which unit it is before reading the table. Two caveats belong in prose rather than a column: the five-bedroom fair-value anchor rests on only 13 caveats, and at S$5–5.9 million quantums the buyer pool is owner-occupiers, not exit-optimisers — the 3.02% modelled yield won't carry a unit this size the way a one-bedder's rent does. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

The Continuum is what a B looks like when the market takes three years to agree with the price. The card is genuinely mid-tier — a ~3.5%/yr 1km engine with a modest lift, a real school ring, D15's second-tier rental growth, and a 0.89km walk to a Circle Line station that is the permanent weak line. But the 2023 verdict that freehold Katong at S$2,732 was overpriced has been unwound caveat by caveat: 95% sold, a last-three-years average of S$2,819, June 2026 prints at S$3,019, and a next-door 99-year neighbour sub-selling at S$2,881. What remains is a big-family shelf asking at or below the project's own transacted medians — on the holding model, nearly everything left is a four-to-six-year read — where the true gate is the S$4.5–5.9 million quantum, not the psf. If you need a freehold four- or five-bedder in the Katong school ring and can carry that cheque, this is one of the few honestly-priced large-format tails on the board; if you need a train at the door or a rental engine to carry the wait, the card itself tells you to look elsewhere.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade (B, 6.5), the five factor scores, modelled growth (~3.8%/yr), the 3.02% modelled yield, per-bedroom transacted medians and the adjusted comparables per the TRIBE New Project Scorecard (URA Data Service transacted PSF; 1km resale trend lifted for project size, transport and schools; figures as at July 2026). Land acquisition (S$815 million for the two Thiam Siew Avenue freehold plots, November 2021, ~S$1,488 psf ppr) per the developer consortium's project materials and contemporaneous reporting. Launch-weekend result (216 of 816, 26.5%, average S$2,732 psf, 6–7 May 2023) per EdgeProp and the developer's sold-log; the December 2024 ~S$2,788 average and Emerald-spillover finding per the same EdgeProp analysis. Sell-down status: ~83% as at 20 December 2025 per the-continuum-at-thiam-siew-avenue.com; the 42-unit balance and per-type price table (14 July 2026) per the official sales site, which also lists the expected TOP of 17 November 2027 — agent-carried charts are unofficial and may lag caveats. Last-three-years caveat statistics (529 transactions to June 2026; PSF low S$2,390 / average S$2,819 / high S$3,121; June 2026 transactions including S$3,019 psf on 1,249 sqft) per StackProperty, compiled from URA caveats. Tembusu Grand sub-sale record and cluster figures per our Tembusu Grand review and our Grand Dunman review. Resale comparables age- and lease-adjusted per Bala's Table with a +8% (3BR+) GFA-harmonisation uplift, capped at the project's own median, per the NPS calculator's published methodology. Primary 1 priority distance is measured door-to-door — confirm any school-distance claim on OneMap before relying on it. Prices and availability are as reported at the dates cited and will change; scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.