Insights

Honest Insights On Bloomsbury Residences

Bloomsbury Residences grades C (5.3) on the New Project Scorecard — the first Mediapolis launch opened at just 25.1% in April 2025, then quietly sold down to roughly 91% in fifteen months. What the C explains, and what the last two-bedders, four-bed suites and penthouses cost.

By TRIBE Editorial · 14 July 2026 · 12 min read

Bloomsbury Residences is a 358-unit, 99-year leasehold development at Media Circle in one-north, District 5 — three blocks by Qingjian Realty and Forsea Holdings, the first residential project ever launched in the Mediapolis precinct, on land bought at a GLS tender in January 2024 for S$395.29 million (S$1,191 psf ppr). It grades a C (5.3) on our New Project Scorecard (NPS), and its sales history is a study in patience: a 25.1% launch weekend in April 2025 — one of the softest major openings of that year — followed by fifteen months of steady, unglamorous selling to roughly 91% sold on the developer's July 2026 chart, with recent caveats printing above the launch average. This is a look at what the C actually flags, why the market bought the project anyway, and what the last two-bedders, four-bedroom suites and penthouses cost. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted for the project's own size, transport and schools, not a forecast.

The scorecard: what the C actually says

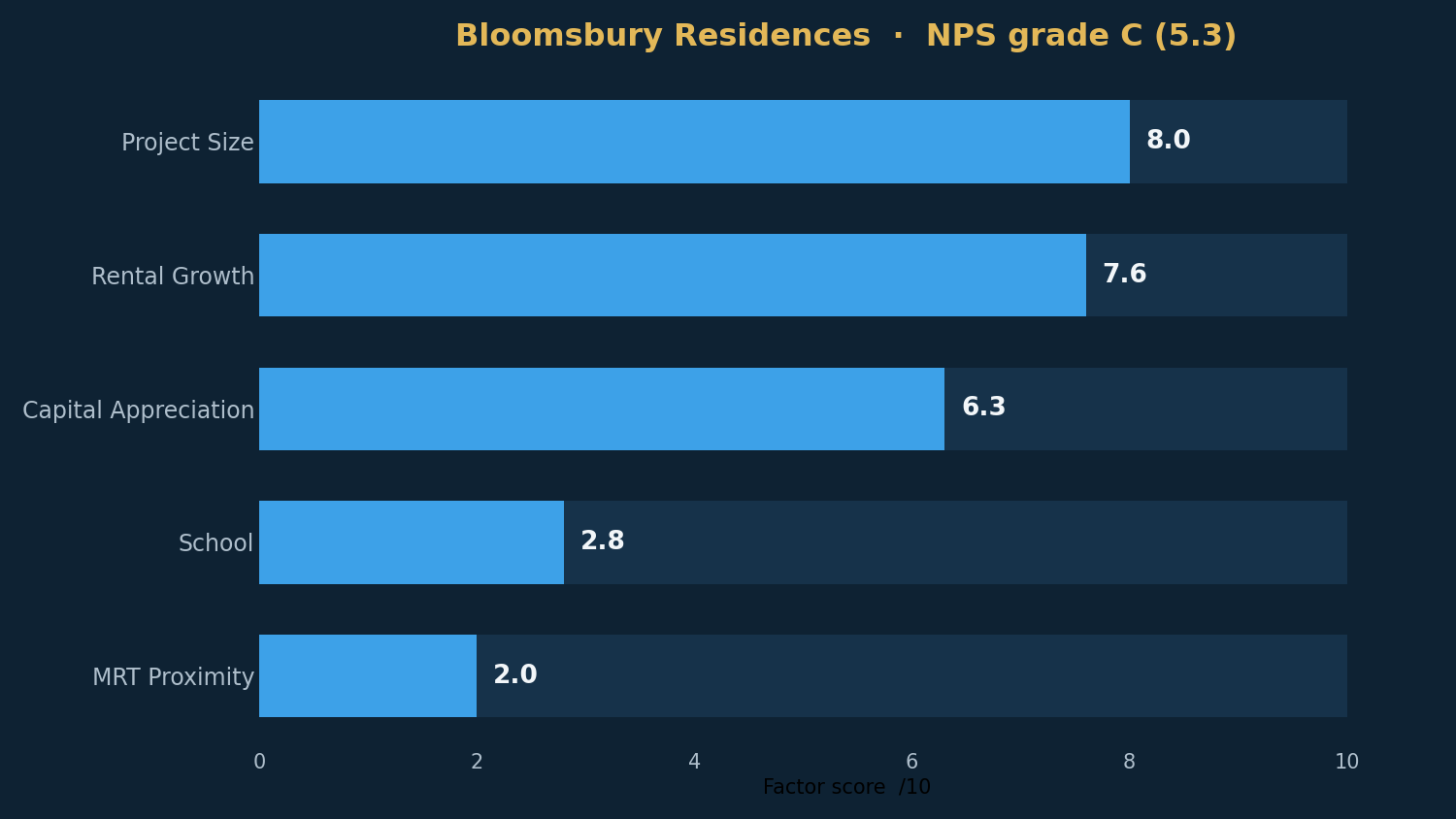

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| Project Size | 8.0 | 358 units — a mid-sized development |

| Rental Growth | 7.6 | District 5 rents grew ~7.1%/yr over the decade — the card's strength |

| Capital Appreciation | 6.3 | D5 resale grew ~3.0%/yr; lifted +0.21 → ~3.3%/yr, clearing 3% by a whisker |

| School | 2.8 | Only New Town Primary (0.80km) within 1km, undersubscribed |

| MRT Proximity | 2.0 | 0.96km to Commonwealth MRT — and the scorecard flags the walk itself |

Read the card from the bottom, because that is where the C comes from. MRT scores 2.0: the nearest station by OneMap routing is Commonwealth at 0.96km, and the scorecard's own basis note flags the walk as implausible as a daily routine — the marketing line of "a ten-minute walk to one-north MRT" crosses the Mediapolis superblocks and reads better on a brochure than on a July afternoon. School scores 2.8: one primary school inside the kilometre, undersubscribed — this is not a ballot-distance address. Those two lines are the discount the April 2025 pricing conceded.

The top of the card is what the buyers who came anyway were buying. Rental growth scores 7.6 — District 5 rents compounded about 7.1% a year over the decade, among the strongest districts on our board, fed by exactly the tenant pool outside this project's gate: Mediapolis, Biopolis, Fusionopolis, NUS and INSEAD. The modelled gross yield is 3.28%, above most of the 2025–26 launch cohort. Capital appreciation at 6.3 is the honest middle: D5 resale appreciated ~3.0% a year on a same-property basis (the model falls back to the district series here — the 1km ring around Media Circle is too thin on resale history for a local read), lifted a slim +0.21 to a projected 3.26% — clearing the 3% bar by 0.26 of a point. Hold that thin margin in mind; it does a lot of work in the holding table below.

The land, the launch, and the quiet fifteen months

The January 2024 tender told you the developers knew what they were buying: three bidders, and the Qingjian–Forsea consortium's S$395.29 million (S$1,191 psf ppr) topping the field for the precinct's first residential plot. It is still the high-water land mark at Media Circle — when the neighbouring Parcel A went to the same consortium later, it went for S$315 million, or S$1,037 psf ppr, 13% less (that site is now Hudson Place Residences). Launch pricing was, in the developer's own word, sensitive: the 12–13 April 2025 weekend moved 90 of 358 units (25.1%) at an average of S$2,474 psf — two-bedders from S$1.37 million took over 70% of sales, 88% of buyers were Singaporean, and a six-bedroom penthouse cleared at S$2,700 psf. Against Blossoms by the Park at 93% sold or One-North Eden's sell-out, 25.1% read as a verdict.

Fifteen months re-read it. With no relaunch and no headline price cut, the sold-log shows two to eight units clearing nearly every fortnight — 40-plus in the four months to mid-July 2026 alone — and URA caveats record 311 new-sale transactions by June 2026 (87% of the project), at an overall average of S$2,522 psf, trending up: June 2026 two-bedders printed S$2,482–2,566 psf against the S$2,474 launch average, and May's four-bedroom suites printed to S$2,711. The developer's 13 July 2026 unit chart shows roughly 33 units left (~91% sold) — and the composition is telling. Block 63 is finished. Every 2-bedroom, 2BR+Study, 3-bedroom and 4BR Premium+Study stack is gone except four high-floor 678 sqft 2BR Premium units (floors 19–22 of Block 61). What remains in depth is the project's most private product: about 23 of the 1,421 sqft 4-Bedroom Suite+Flexi units with private lifts (type D3) — a format that only began selling down in earnest this spring — and six of the eight penthouses (1,668–1,916 sqft five-bedders; both 2,131 sqft 6BR+Study penthouses are sold).

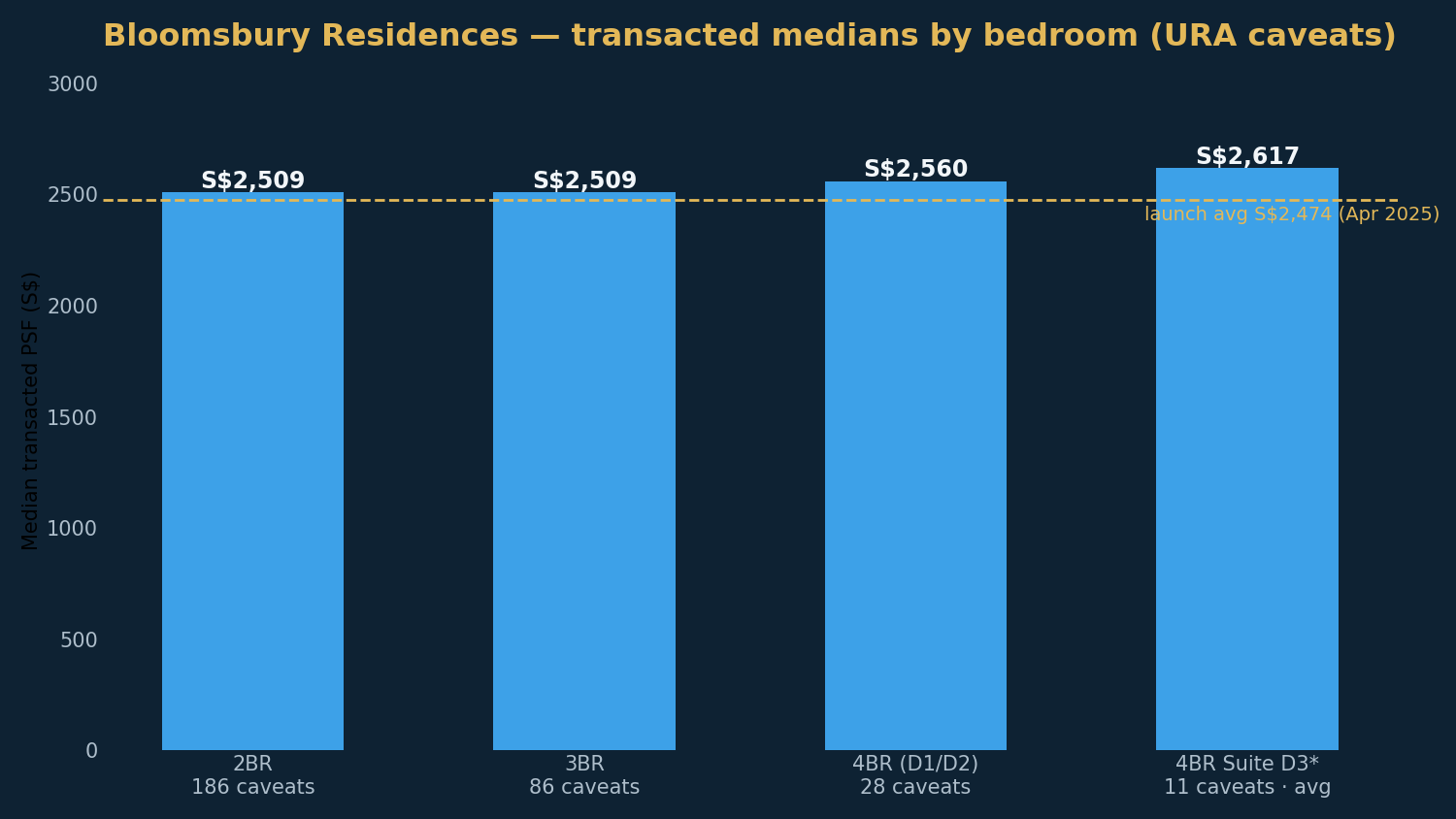

What the project has transacted at, by bedroom (URA caveats via the live scorecard, April 2025–June 2026):

| Type | Typical size | Median PSF | Caveats |

|---|---|---|---|

| 2 Bedroom | 678 sqft | S$2,509 | 186 |

| 3 Bedroom | 980 sqft | S$2,509 | 86 |

| 4 Bedroom | 1,206 sqft | S$2,560 | 28 |

One footnote on the bands: the scorecard's four-bedroom band covers the 1,173–1,206 sqft D1/D2 layouts. The remaining 1,421 sqft D3 suites sit outside it — their own eleven caveats to date average S$2,617 psf (S$3.72 million), from S$2,551 on a low floor to S$2,711 on floors 16–20. The penthouse formats still on the shelf have no transacted record at all — the only penthouse caveats are the two 6BR+Study units at about S$2,700 psf — so we benchmark what we can and say so where we can't.

The benchmark: one-north resale, adjusted honestly

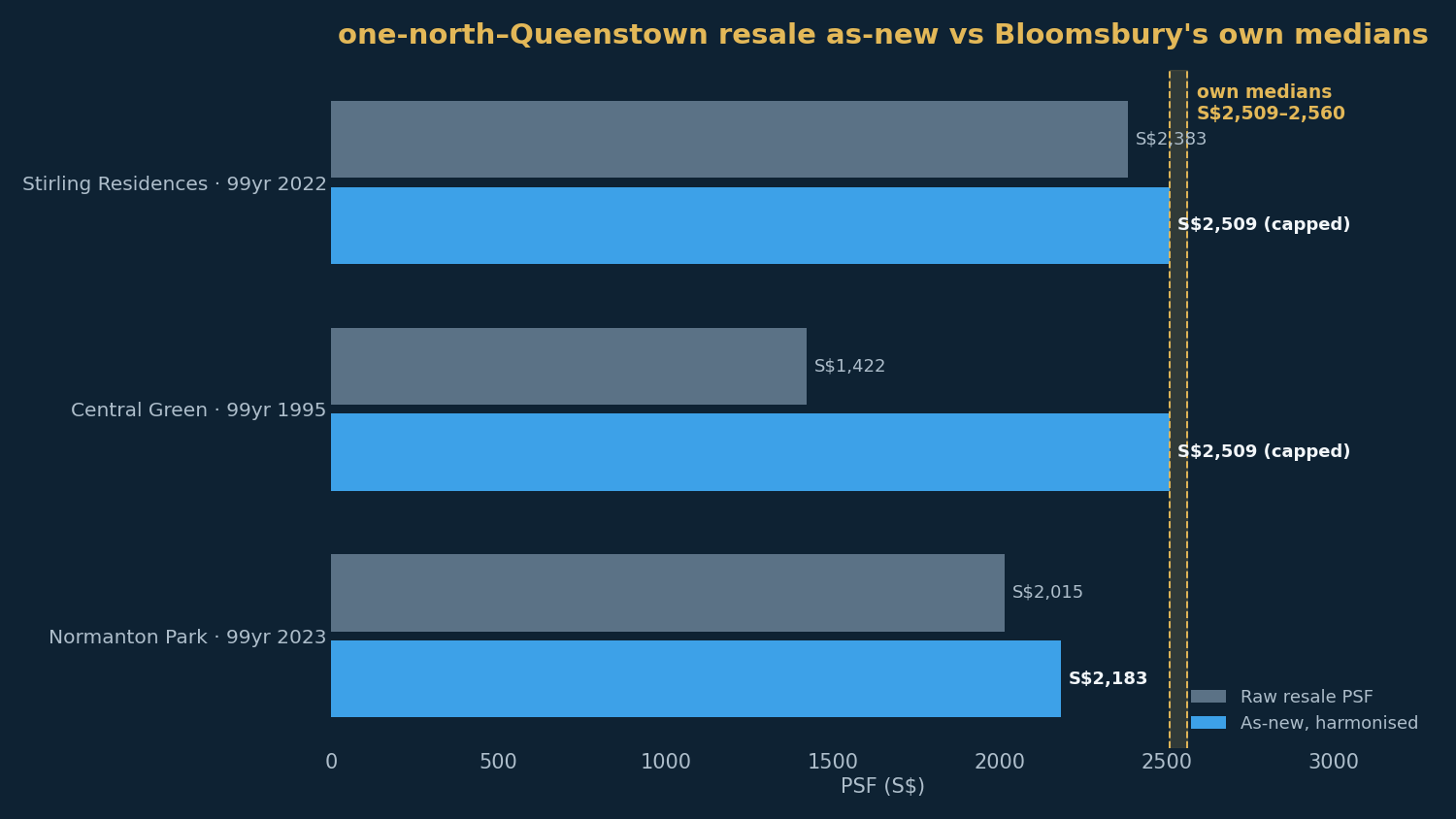

The scorecard's comparables are the established 99-year names in the Queenstown–one-north belt. We lift each to a like-for-like, as-new footing: lease/age adjustment (Bala's Table, to a fresh-99 equivalent) plus GFA harmonisation of +6% (two-bedders) or +8% (three-bedders and larger) for comps pre-dating the 22 January 2023 strata rules. The calculator caps each adjusted comp at the project's own median — a deliberately conservative floor.

| Comparable | Raw resale PSF | As-new, harmonised |

|---|---|---|

| Bloomsbury Residences · 2BR (own median) | — | S$2,509 |

| Stirling Residences (99yr, 2022, 0.67km) | S$2,383 | ~S$2,509 (capped) |

| Central Green (99yr, 1995, 0.84km) | S$1,422 | ~S$2,509 (capped) |

| Normanton Park (99yr, 2023, 0.85km) | S$2,015 | ~S$2,183 |

Two of the three comps hit the cap — Stirling Residences, four years old and a 0.67km neighbour across the district line, trades at S$2,383 raw today and restates above Bloomsbury's own S$2,509 median once lifted; thirty-one-year-old Central Green restates far above it. Normanton Park is the honest counterweight: a huge, three-year-old project at S$2,015 raw that restates to only ~S$2,183 as-new — a reminder that the belt has cheaper doors if the address itself is negotiable. The cluster's new launches frame the same range: Blossoms by the Park at S$2,444 average, Hudson Place's launch at S$2,458, LyndenWoods at ~S$2,462, The Hill at ~S$2,550. Bloomsbury's S$2,522 running average sits mid-pack — the "sensitive pricing" of April 2025 has simply become the precinct's going rate.

How long you'd likely hold

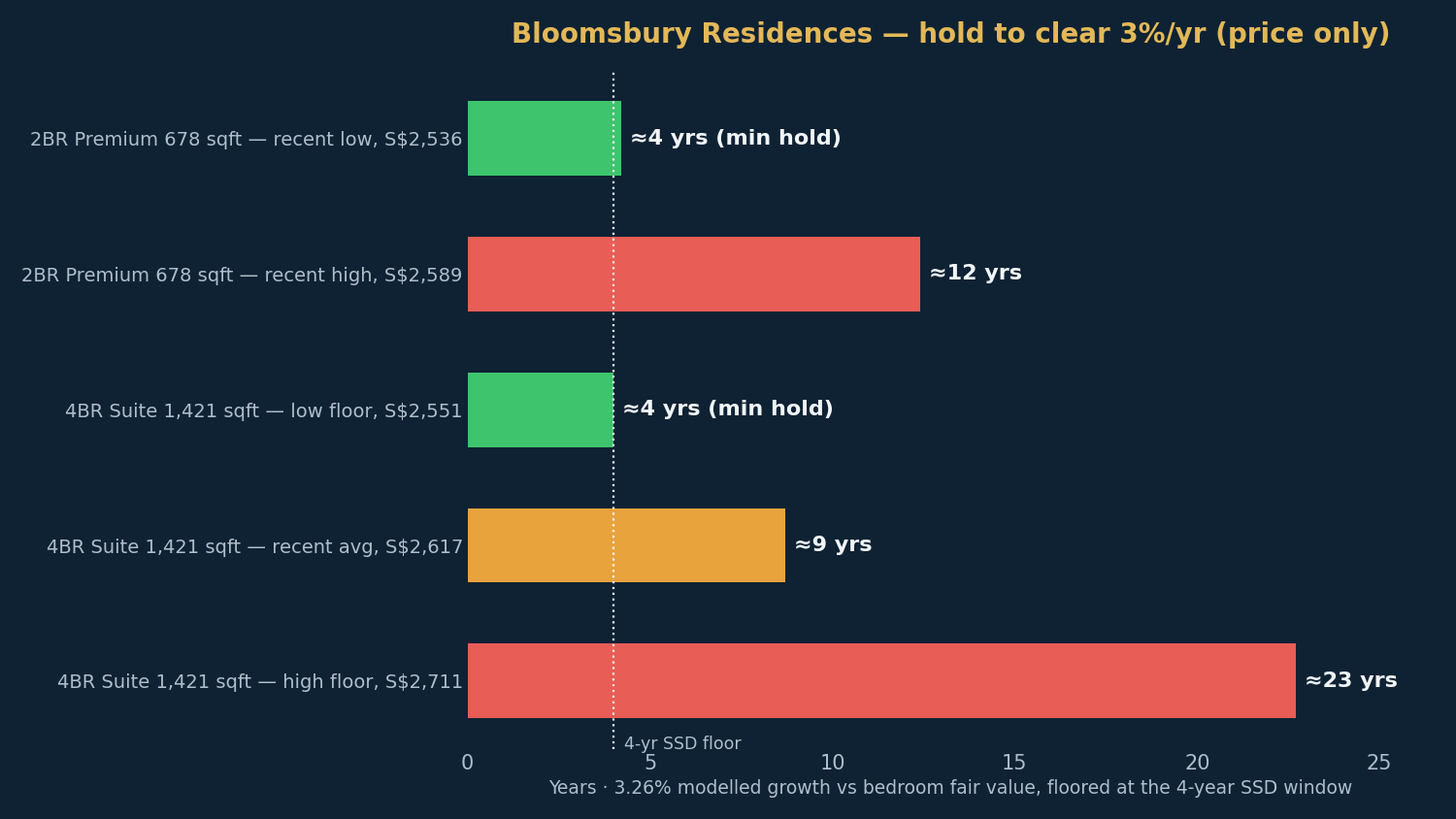

Seller's stamp duty runs for four years (16%, 12%, 8%, 4%), so no exit before year four is realistic, and the shortest tier we publish is four-to-six years. Using the NPS calculator's model — 3.26% expected growth, a 3% target — here is the estimated holding period for each remaining stack, on price growth alone, against the bedroom's own transacted median as the fair-value anchor.

| Available stack | PSF | Hold (price only) |

|---|---|---|

| 2BR Premium 678 sqft, floors 19–22 — at recent low prints | S$2,536 | 4–6 yrs |

| 2BR Premium 678 sqft, floors 19–22 — at recent high prints | S$2,589 | >10 yrs |

| 4BR Suite+Flexi 1,421 sqft — low floor (≈S$3.63m) | S$2,551 | 4–6 yrs |

| 4BR Suite+Flexi 1,421 sqft — recent average (≈S$3.72m) | S$2,617 | 6–10 yrs |

| 4BR Suite+Flexi 1,421 sqft — high floor (≈S$3.85m) | S$2,711 | >10 yrs |

The table is brutal in a way the Katong ones are not, and the reason is the growth line, not the prices: with the model clearing the 3% target by only 0.26 of a point, the four-to-six-year tier ends just S$38–39 psf above fair value (S$2,547 on the two-bedroom band, S$2,599 on the four-bedroom), and the six-to-ten tier barely S$26 further. A few dollars of floor premium swings the read by a decade — the classic thin-margin pattern we flagged at Coastal Cabana and Elta. The remaining penthouses have no fair-value anchor of their own format, so we publish none. What the price-only table cannot show is the line that actually carries this project: a 3.28% modelled yield on D5's ~7.1%-a-year rental engine, with the tenant pool across the street. Bought at the bottom of a stack, this is a rental hold that happens to clear the growth bar; bought at the top of one, it is a rental hold that doesn't — and you should price it as one. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

Bloomsbury Residences is a C that the market has spent fifteen months methodically buying, and both halves of that sentence are true. The C is real: a near-kilometre walk to a train, one undersubscribed school in the ring, and a growth model that clears its bar by a rounding error. The buying is real too: 25.1% to roughly 91% with no relaunch, caveats trending above the launch average, and the precinct's land economics — this project's S$1,191 psf ppr remains the high-water mark its own developer wouldn't repeat next door — quietly defending everyone who entered at S$2,4xx–2,5xx. The shelf that remains is entry-price-decisive to a degree that is unusual even by our standards: the same 678 sqft two-bedder is a four-to-six-year hold at S$2,536 and a ten-year-plus hold at S$2,589, and the 1,421 sqft private-lift suites swing just as hard between floors. If you are buying here, you are buying D5's rental engine at the precinct's going rate — negotiate the stack, take the low floor, and let the tenants carry it; if you need the growth story to do the work on its own, the card has been telling you since April 2025 that it can't.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade (C, 5.3), the five factor scores, modelled growth (~3.3%/yr), the 3.28% modelled yield, per-bedroom transacted medians and the adjusted comparables per the TRIBE New Project Scorecard (URA Data Service transacted PSF; district-resale trend lifted for project size, transport and schools; figures as at July 2026). Land tender (S$395.29 million, S$1,191 psf ppr, three bidders, January 2024, 114,462 sqft site at plot ratio 2.9) per EdgeProp's tender coverage and the project's sales materials; the same EdgeProp article records the neighbouring Media Circle Parcel A going to the same consortium at S$315 million (S$1,037 psf ppr). The 12–13 April 2025 launch (90 of 358, 25.1%, average S$2,474 psf, 88% Singaporean, two-bedders over 70% of sales, the S$2,700 psf six-bedroom penthouse, 199 preview cheques, and remaining units from S$1.36 million / ~S$2,386 psf) per EdgeProp, which also carries the one-north cluster status (Blossoms by the Park 93% at S$2,444 average; The Hill @ One-North ~44%; One-North Eden sold out at S$1,965). Hudson Place Residences' launch (61.5% at S$2,458 average) per our Hudson Place review. Caveat statistics (311 new-sale transactions to June 2026; overall average S$2,522 psf, range S$2,348–2,727; the June 2026 and May 2026 per-unit prints and the 1,421 sqft D3 record of ~S$2,617 average) per StackProperty, compiled from URA caveats. Remaining-unit composition (~33 units: four high-floor 678 sqft B3 units, ~23 D3 suites, six penthouses; Block 63 sold out) counted from the developer's unit distribution chart dated July 2026, read against its sold-unit log (latest sale #04-17 on 10 July 2026) — agent-carried charts are unofficial and may lag caveats. Resale comparables age- and lease-adjusted per Bala's Table with +6%/+8% GFA-harmonisation uplifts, capped at the project's own median, per the NPS calculator's published methodology. Primary 1 priority distance is measured door-to-door — confirm any school-distance claim on OneMap before relying on it. Prices and availability are as reported at the dates cited and will change; scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.