Insights

Honest Insights On One Marina Gardens

One Marina Gardens scores a grade C (4.2) — and the number behind it is stark: the New Project Scorecard models price growth at just 0.28% a year. Marina South is a brand-new precinct with almost no resale track record, and the one comparable nearby has actually fallen in value. This is a yield-and-lifestyle buy, not a growth play.

By TRIBE Editorial · 29 June 2026 · 8 min read

One Marina Gardens is a 937-unit, 99-year leasehold development in Marina South, beside the Gardens by the Bay, completing around 2029. It grades a C (4.2) on our New Project Scorecard (NPS), and the headline number behind that grade deserves to be stated plainly: the scorecard models its price growth at just 0.28% a year — effectively flat. That isn't a knock on the building; it's what the data says about the location. Marina South is a brand-new precinct with almost no resale history, and the single comparable the scorecard can find within 1km has lost value over the past decade. With 296 units still available, this is a piece about reading a grade honestly: One Marina Gardens can make sense as a yield and lifestyle buy, but on capital growth, the model expects close to nothing. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, schools, project size, MRT access and rental growth — from real URA transacted data. It is backward-looking by design, and for a precinct with no history it leans on what little there is. For the holding period, we use the published NPS calculator: fair value is the median transacted PSF nearby for each bedroom type, the project grows at its modelled rate, and we report the years needed to clear a 3% annual return — gross of stamp duty, financing and selling costs.

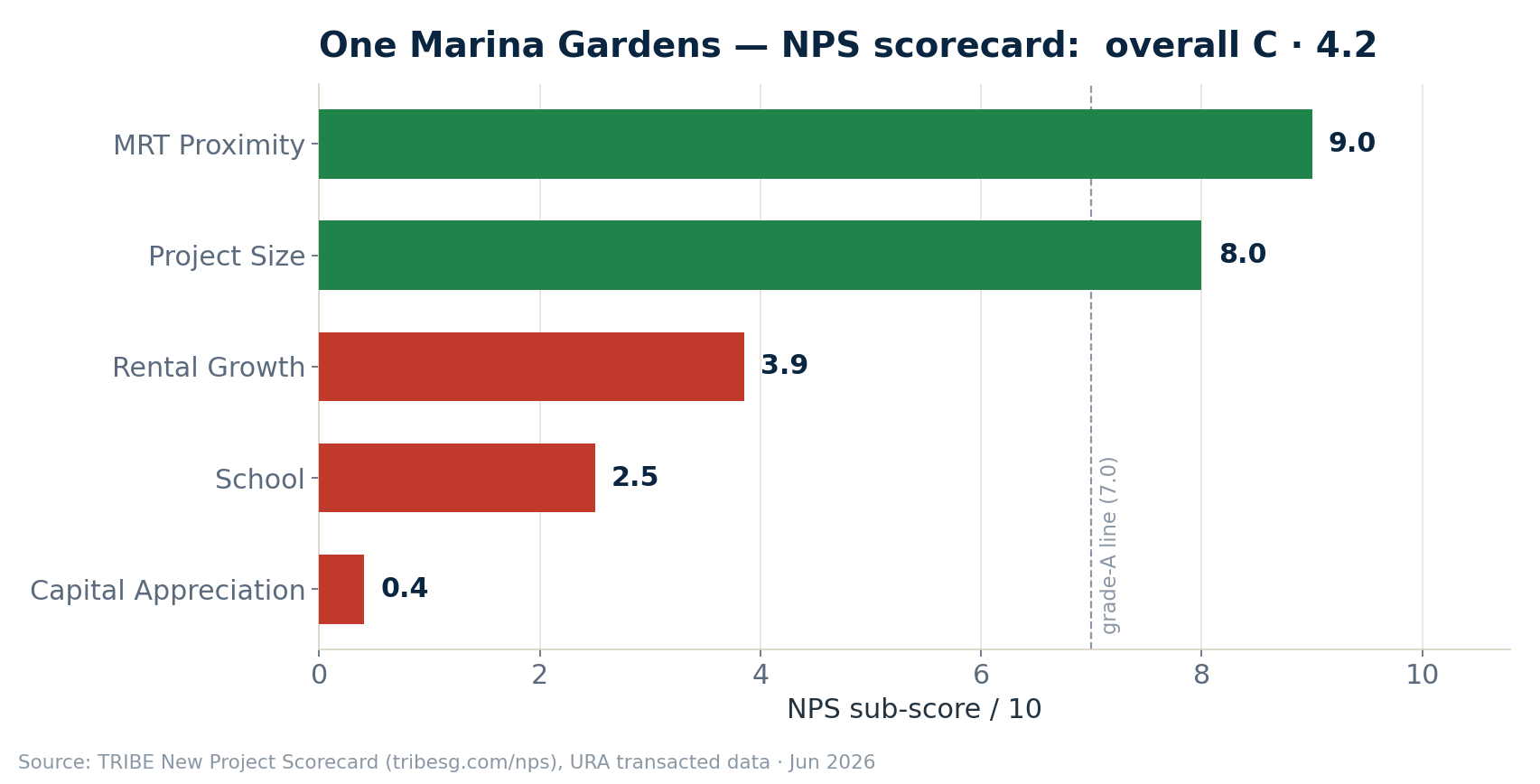

The scorecard: one strong factor, and a lot of blanks

One Marina Gardens' 4.2 comes almost entirely from a single factor; the rest of the card is thin.

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| MRT Proximity | 9.0 | Marina South MRT (Thomson-East Coast Line) at the door |

| Project Size | 8.0 | 937 units — large and liquid |

| Rental Growth | 3.9 | CCR rents grew modestly over the decade |

| School | 2.5 | Few primary schools in the downtown core |

| Capital Appreciation | 0.4 | Almost no positive resale track record nearby |

The transport score is real — a Thomson-East Coast Line station sits at the door — and the project is large. But the capital-appreciation sub-score is 0.4, because the scorecard can find almost no positive resale history to anchor to: Marina South has barely traded, and the one project within 1km (Marina Bay Residences) has appreciated at roughly −0.2% a year over the past decade. School options downtown are limited (2.5). The result is a modelled price growth of 0.28% a year — for practical purposes, flat. A buyer here should go in understanding that the model is not forecasting capital gains.

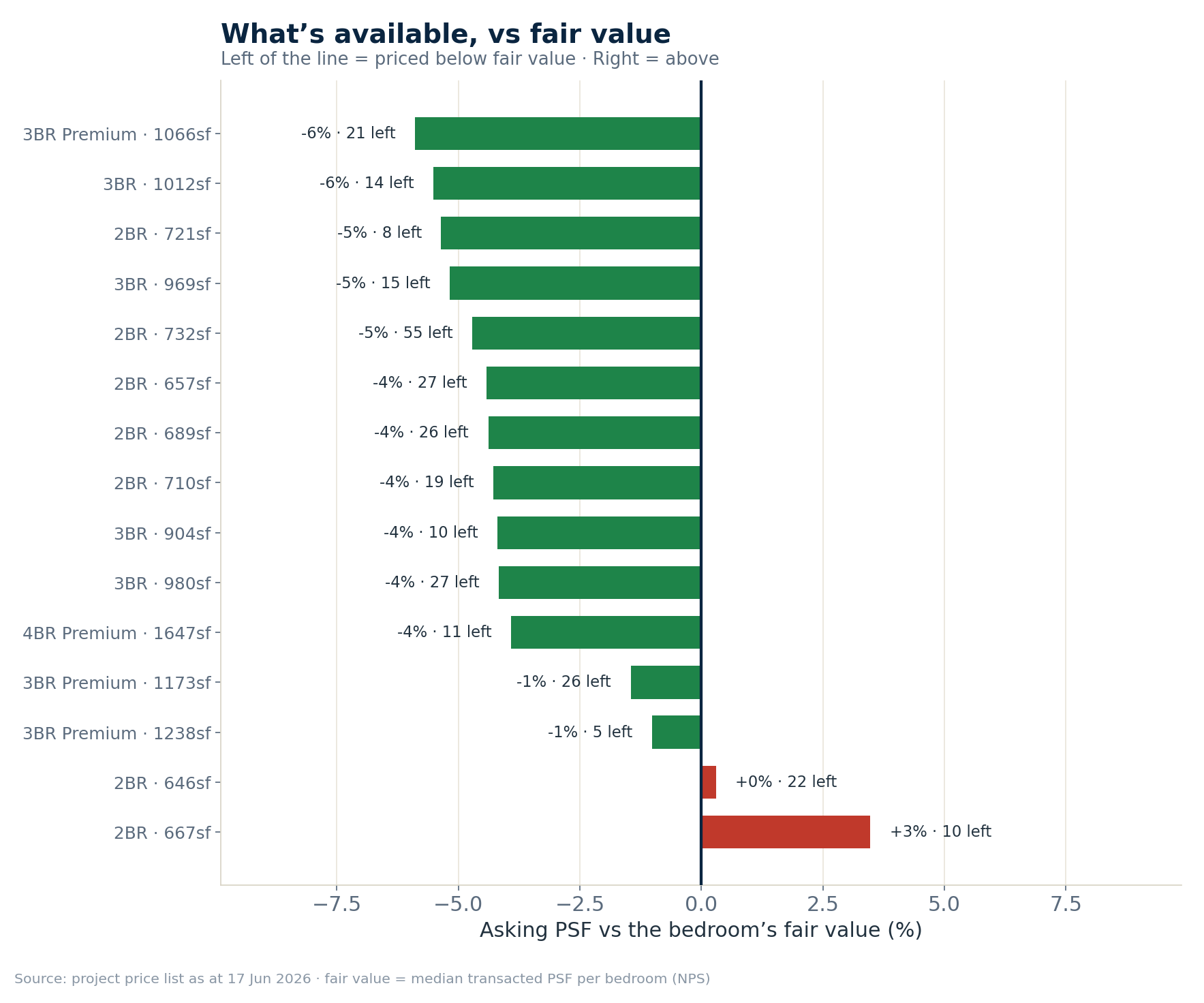

What's actually left — and what it costs

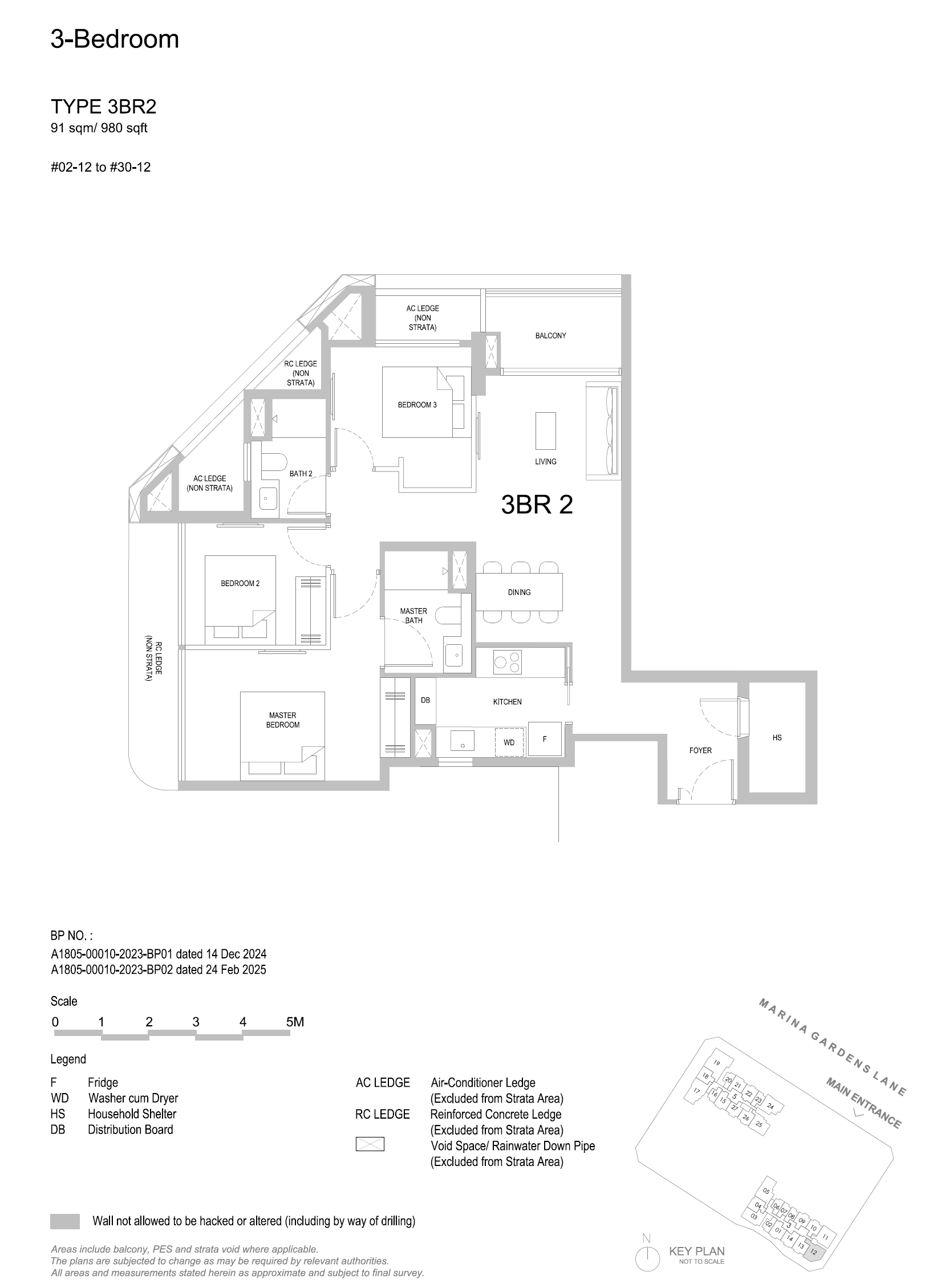

With 296 of 937 units available, there's deep choice, mostly across two- and three-bedroom layouts. Each bedroom's fair value is the median transacted PSF nearby (2BR ~S$2,988; 3BR ~S$2,955).

| Available stack | Size | Units left | PSF | vs fair value |

|---|---|---|---|---|

| 3BR Premium | 1,066 sqft | 21 | 2,781 | −5.9% |

| 3BR | 1,012 sqft | 14 | 2,792 | −5.5% |

| 2BR | 732 sqft | 55 | 2,847 | −4.7% |

| 3BR | 980 sqft | 27 | 2,832 | −4.2% |

| 2BR | 646 sqft | 22 | 2,997 | +0.3% |

| 2BR | 667 sqft | 10 | 3,092 | +3.5% |

Most of the remaining stock is priced a few percent below fair value — the 732 sqft 2BR (the deepest pool, 55 units) and the larger 3-bedders sit 4–6% under the median for their size, which is the disciplined end of the list. A couple of small 2-bedders (646 and 667 sqft) sit slightly above. Here are the deepest 2- and 3-bedroom pools:

What that fair value is built on — the (very) thin resale nearby

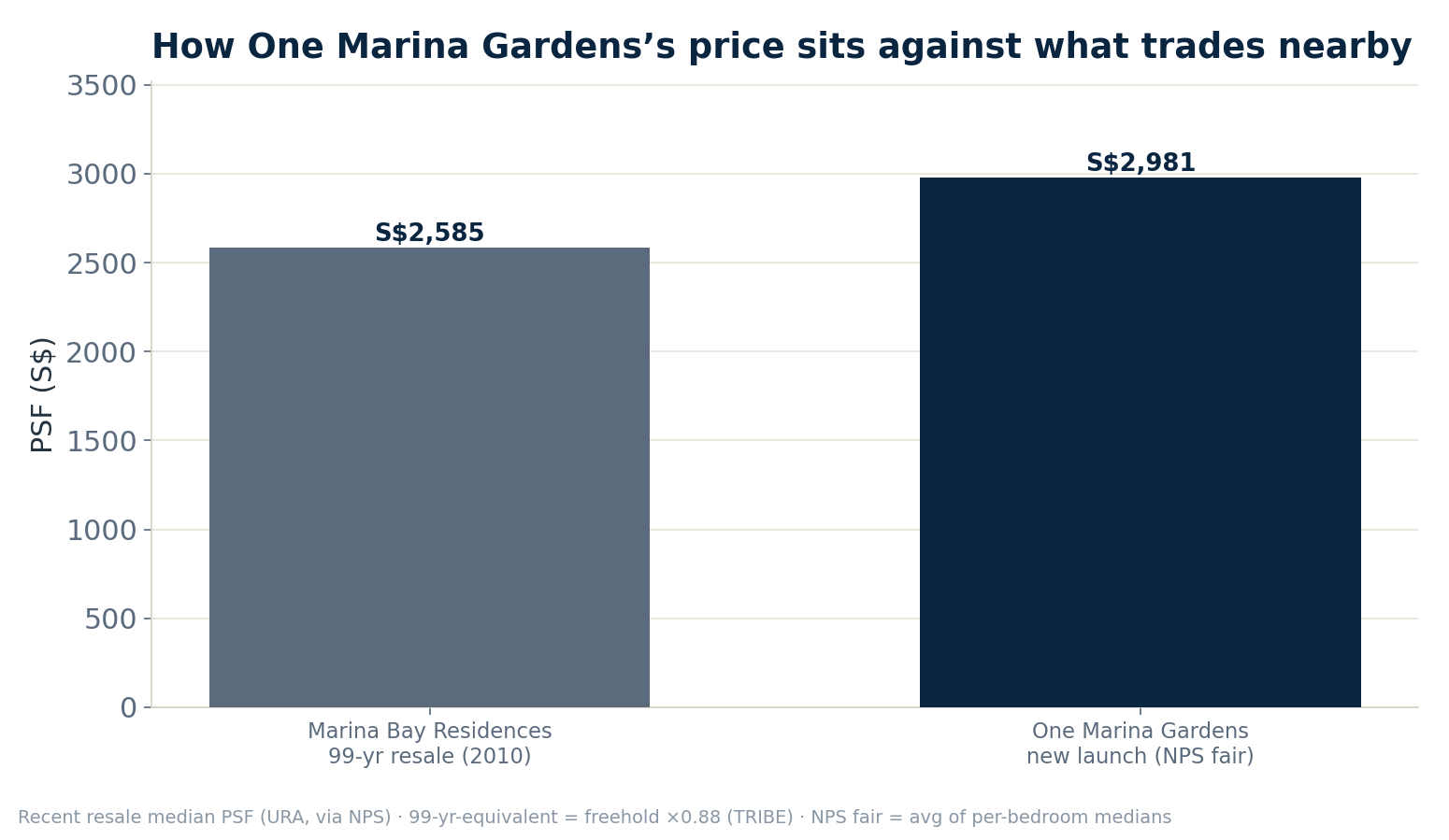

This is the heart of the honest read. The scorecard finds only one resale project within 1km: Marina Bay Residences.

| Comparable | Tenure · age | Distance | Recent resale PSF | 10-yr growth |

|---|---|---|---|---|

| Marina Bay Residences | 99-year · 2010 | 0.98 km | ~S$2,585 | ~−0.2%/yr |

With a single comparable, "fair value" rests on thin evidence — and the evidence isn't encouraging. Marina Bay Residences, the only nearby project, trades around S$2,585 psf as 16-year-old leasehold, and its capital appreciation over the past decade has been slightly negative. One Marina Gardens' blended fair value sits near S$2,973 — a new-launch premium over the one resale anchor that has itself failed to appreciate. That is the whole caution in one line: you would be paying up for a brand-new unit in a precinct whose only price history points sideways-to-down.

The holding period, both ways

Using the NPS calculator's model — 0.28% expected growth, a 3% target — the result is unusually clear-cut. On price growth alone, no stack reaches a 3% return, because the modelled growth is near zero. The only way the math lands is with the area's ~3.3% rental yield doing the work.

| Available stack | PSF | Hold (price only) | Hold (with rent) |

|---|---|---|---|

| 2BR · 732 sqft | 2,847 | Doesn't reach 3% | 4–6 yrs |

| 3BR Premium · 1,066 sqft | 2,781 | Doesn't reach 3% | 4–6 yrs |

| 3BR · 980 sqft | 2,832 | Doesn't reach 3% | 4–6 yrs |

| 2BR · 646 sqft | 2,997 | Doesn't reach 3% | 4–6 yrs |

| 2BR · 667 sqft | 3,092 | Doesn't reach 3% | >10 yrs |

The reading is unambiguous. Capital growth alone never clears 3% here — the model simply doesn't expect price appreciation. With rent counted, the below-fair stacks land in the 4–6 year tier, carried entirely by the ~3.3% yield, not by price. And the one stack priced above fair value (the 667 sqft 2BR) doesn't make it even with rent — when growth is flat, overpaying on entry can't be recovered. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

One Marina Gardens is the clearest "know what you're buying" case of this batch. It has a genuine strength — a Thomson-East Coast Line station at the door, in a marquee Marina Bay setting — and for a buyer who wants to live there, or to hold a downtown unit for rental income, those can be reason enough. But the grade is a C (4.2) for sound reasons: a 0.28% modelled growth rate, a 0.4 capital-appreciation score, a single nearby comparable that has lost value, and limited schools. The model is not forecasting capital gains, and we won't dress that up.

If you do buy here, the discipline is doubled: take only the stacks priced below fair value — the deeper 2- and 3-bedroom pools at 4–6% under the median — because when expected growth is flat, the entry price is the entire margin of safety. Treat it as a yield-and-lifestyle asset that the rental return can make work over 4–6 years, not as a project that will re-rate. On the numbers, that is the honest frame.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade, sub-scores, expected growth, fair value and the nearby resale comparable per the TRIBE New Project Scorecard (URA Data Service transacted PSF; figures as at June 2026). Available units, sizes and PSF from the project price list as at 17 June 2026; availability changes as units sell. Holding periods computed with the published NPS calculator model (median transacted PSF fair value, modelled growth, 3% target; gross of stamp duty, financing and selling costs). Project rendering and unit floorplans are from the developer's marketing materials (artist's impressions; floorplans indicative, not to scale). Scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.