Insights

Honest Insights On Narra Residences

Narra scores a grade B (5.8) on the New Project Scorecard — strong on size and rents, dragged down by a 0.0 MRT sub-score. With 63% of units still available, entry price is everything: buy at or below the S$2,190 psf fair value and the maths works; pay the launch premium and it doesn't.

By TRIBE Editorial · 29 June 2026 · 11 min read

Narra Residences is a 540-unit, 99-year leasehold launch at Dairy Farm Walk, completing around 2030. It grades a B (5.8) on our New Project Scorecard (NPS) — a solid suburban project, not a top-tier one — and as at mid-June 2026 about 63% of its units are still for sale. That combination is the whole story: there is no scarcity forcing your hand, the project's expected price growth sits just below a 3% target, and so the only thing that decides whether the numbers work is the price you pay for the specific unit. This is an honest look at the scorecard, the units actually left, and how long you'd likely need to hold each of them. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, schools, project size, MRT access and rental growth — from real URA transacted data. It is backward-looking by design: it tells you what the surrounding district has done, not what a future growth corridor might do. For the holding period, we use the published NPS calculator: fair value is the median transacted PSF nearby, the project grows at its modelled rate, and we report the years needed to clear a 3% annual return — gross of stamp duty, financing and selling costs.

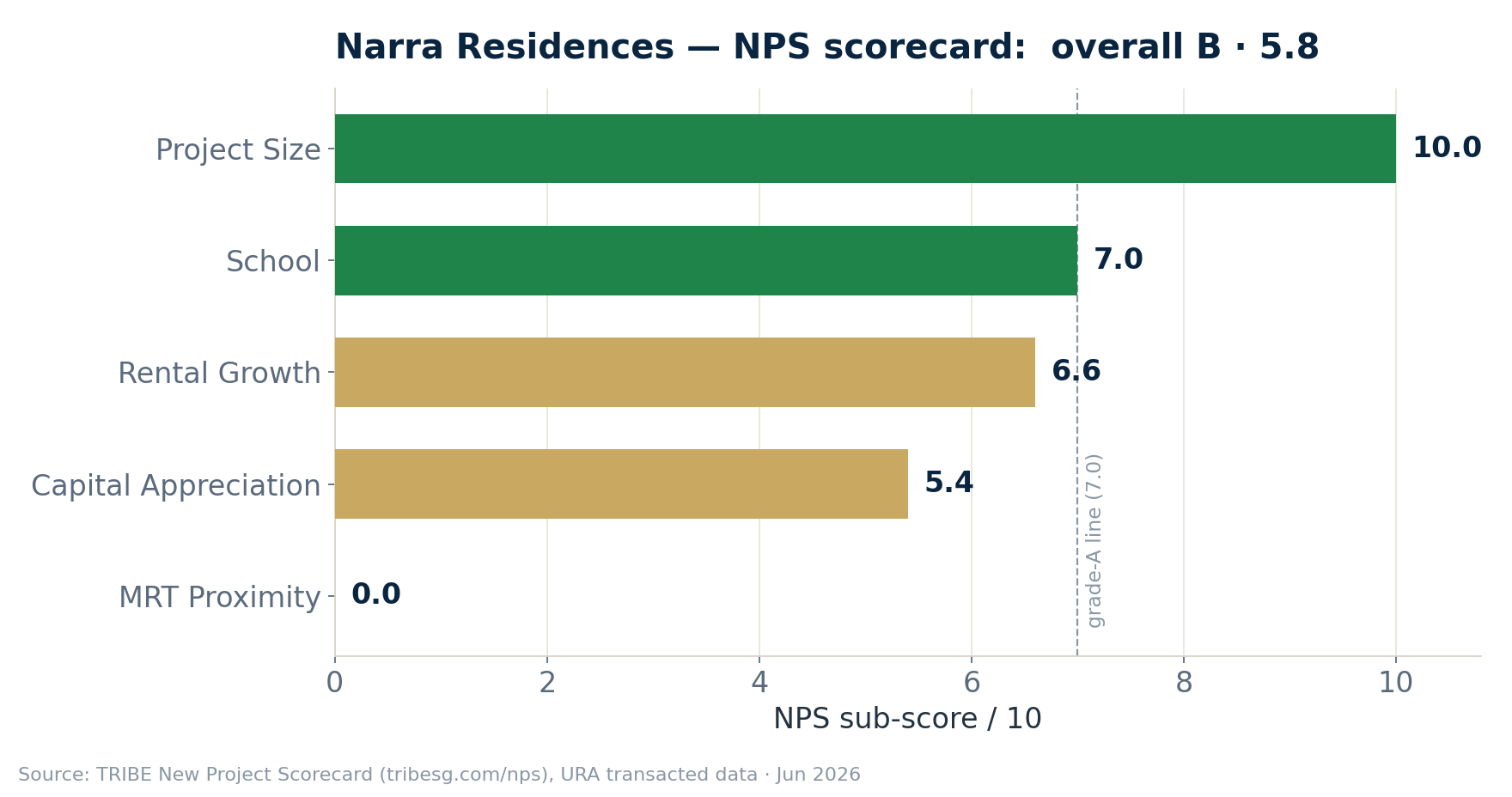

The scorecard: a B, and an honest one

Narra's 5.8 is built from five sub-scores, and they pull in opposite directions.

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| Project Size | 10.0 | 540 units — ideal scale for liquidity and facilities |

| School | 7.0 | 2 primaries within 1km; Bukit Panjang Primary 0.80km (oversubscribed) |

| Rental Growth | 6.6 | OCR rents grew ~4.65%/yr over the decade |

| Capital Appreciation | 5.4 | Nearby resale rose ~2.6%/yr (same-property basis) |

| MRT Proximity | 0.0 | 1.46km to Hillview MRT — a genuine walk |

The strengths are real: at 540 units it's large enough for a liquid resale market and full facilities, the surrounding rental market has grown steadily, and there are primary schools in range. The drag is equally real and worth stating plainly — the MRT sub-score is 0.0. Dairy Farm Walk is roughly 1.46km from Hillview MRT, which is a fifteen-to-twenty-minute walk, not a doorstep. And the capital-appreciation sub-score of 5.4 reflects that homes within 1km have appreciated about 2.6% a year over the past decade on a same-property resale basis — which strips out the price inflation that new launches themselves create. Tilted up for the project's size and schools, the scorecard's modelled expected price growth is about 2.8% a year.

That number matters because it sits below a 3% annual target. On price growth alone, Narra is a project you hold for the long run, not one that re-rates quickly. The case for it rests on two things the backward-looking score doesn't fully capture: the steady rental income, and your entry price.

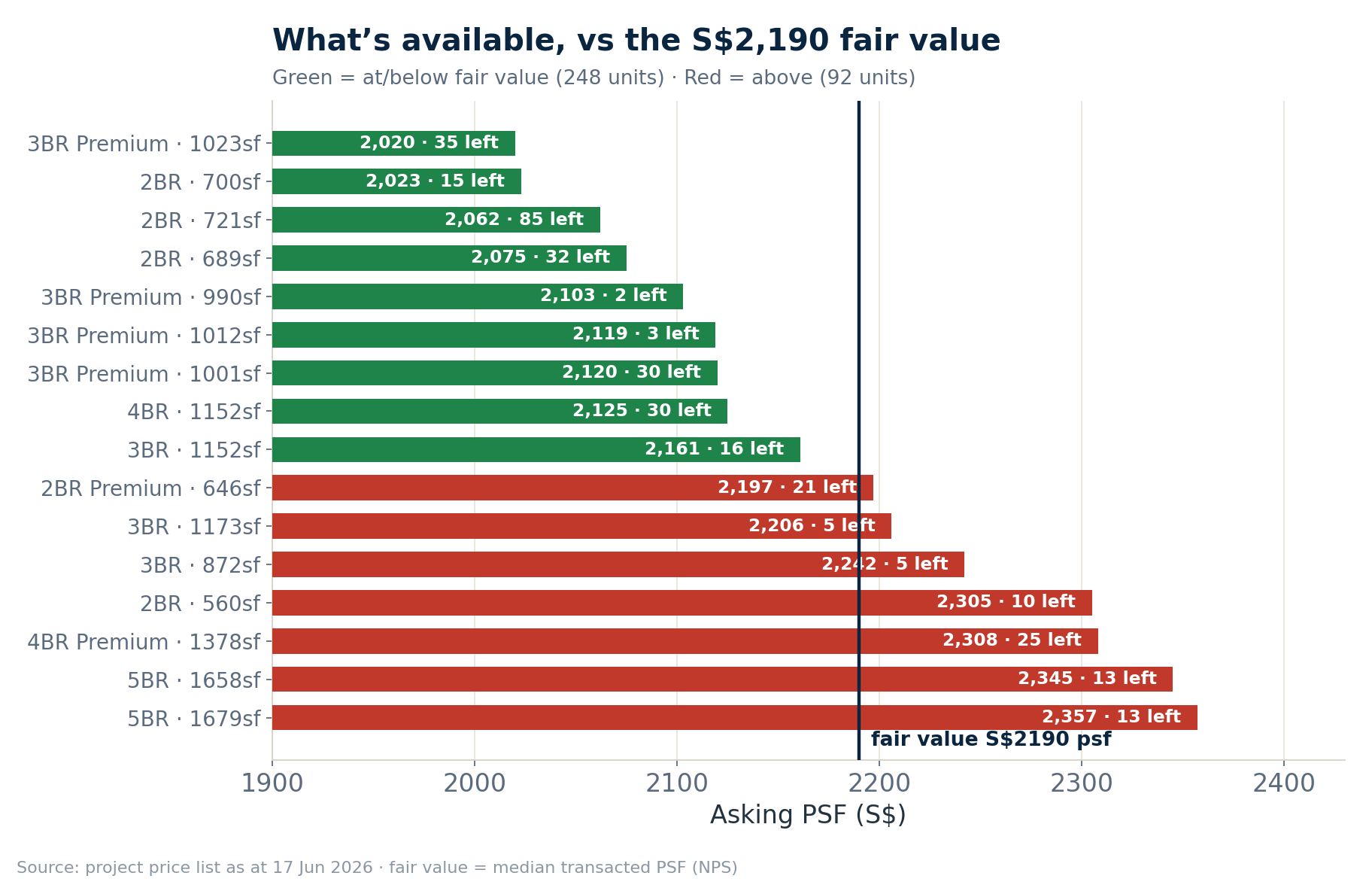

What's actually left — and what it costs

With 342 units unsold, you have real choice, and the available stacks span a wide PSF range. The line that matters is the S$2,190 psf fair value (the median transacted nearby). Buy below it and you start with a cushion; pay above it and the modelled growth has to first erase the premium before it works for you.

| Available stack | Size | Units left | PSF | vs fair value |

|---|---|---|---|---|

| 3BR Premium | 1,023 sqft | 35 | 2,020 | −7.8% |

| 2BR | 700 sqft | 15 | 2,023 | −7.6% |

| 2BR | 721 sqft | 85 | 2,062 | −5.8% |

| 2BR | 689 sqft | 32 | 2,075 | −5.3% |

| 3BR Premium | 1,001 sqft | 30 | 2,120 | −3.2% |

| 4BR | 1,152 sqft | 30 | 2,125 | −3.0% |

| 2BR Premium | 646 sqft | 21 | 2,197 | +0.3% |

| 3BR | 872 sqft | 5 | 2,242 | +2.4% |

| 2BR | 560 sqft | 10 | 2,305 | +5.3% |

| 5BR | 1,658 sqft | 13 | 2,345 | +7.1% |

Of the 342 units available, 248 are priced at or below the S$2,190 fair value and 92 are above it. The deepest, best-value pockets are the larger two-bedders (689–721 sqft, the 85-unit 721 sqft stack is the single biggest pool of inventory) and the 3-bedroom Premium layouts (1,001–1,023 sqft) — all priced 3–8% under fair value. The units carrying a premium are the small 560 sqft 2-bedder and the large-format 5-bedders, both around 5–8% above fair value.

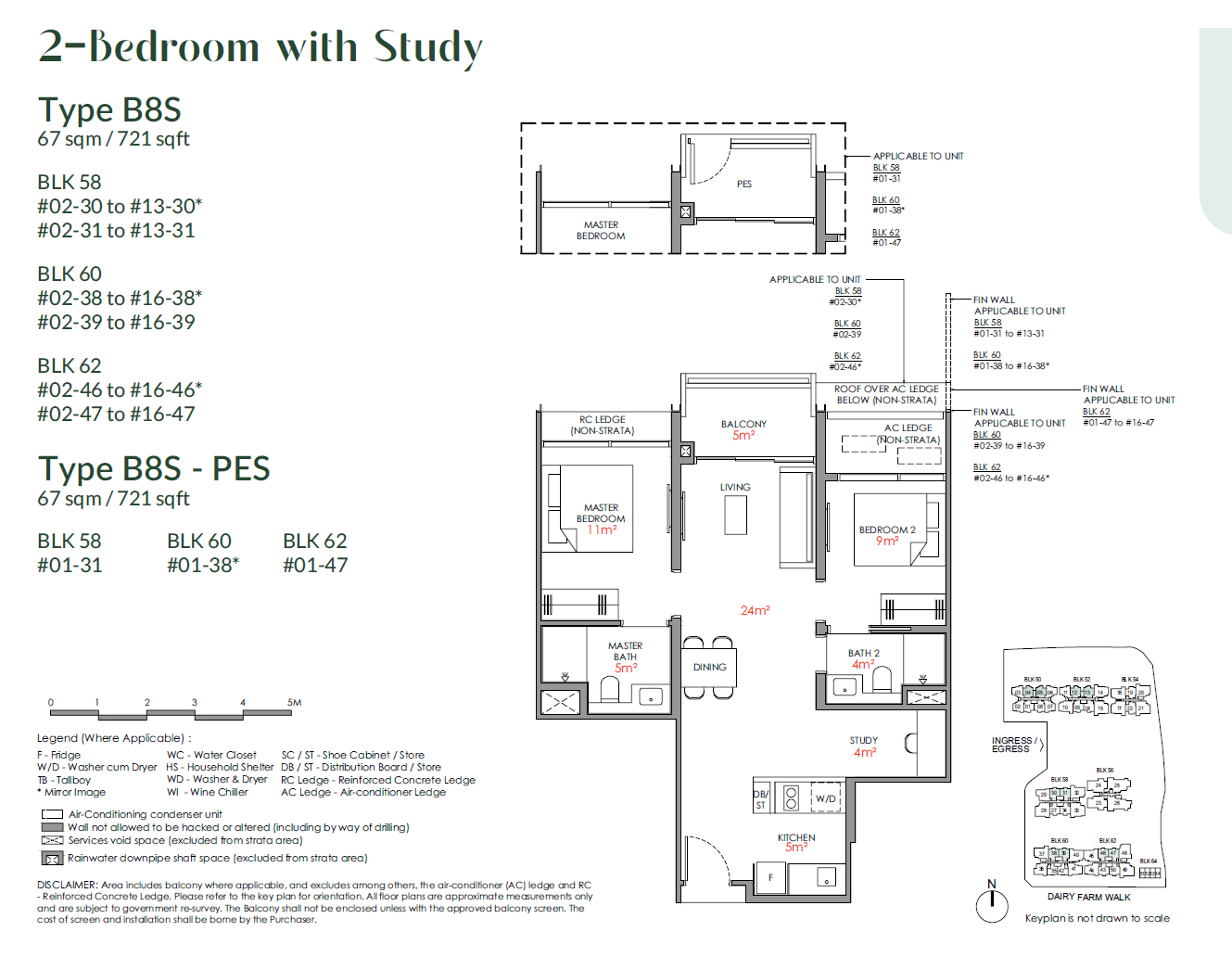

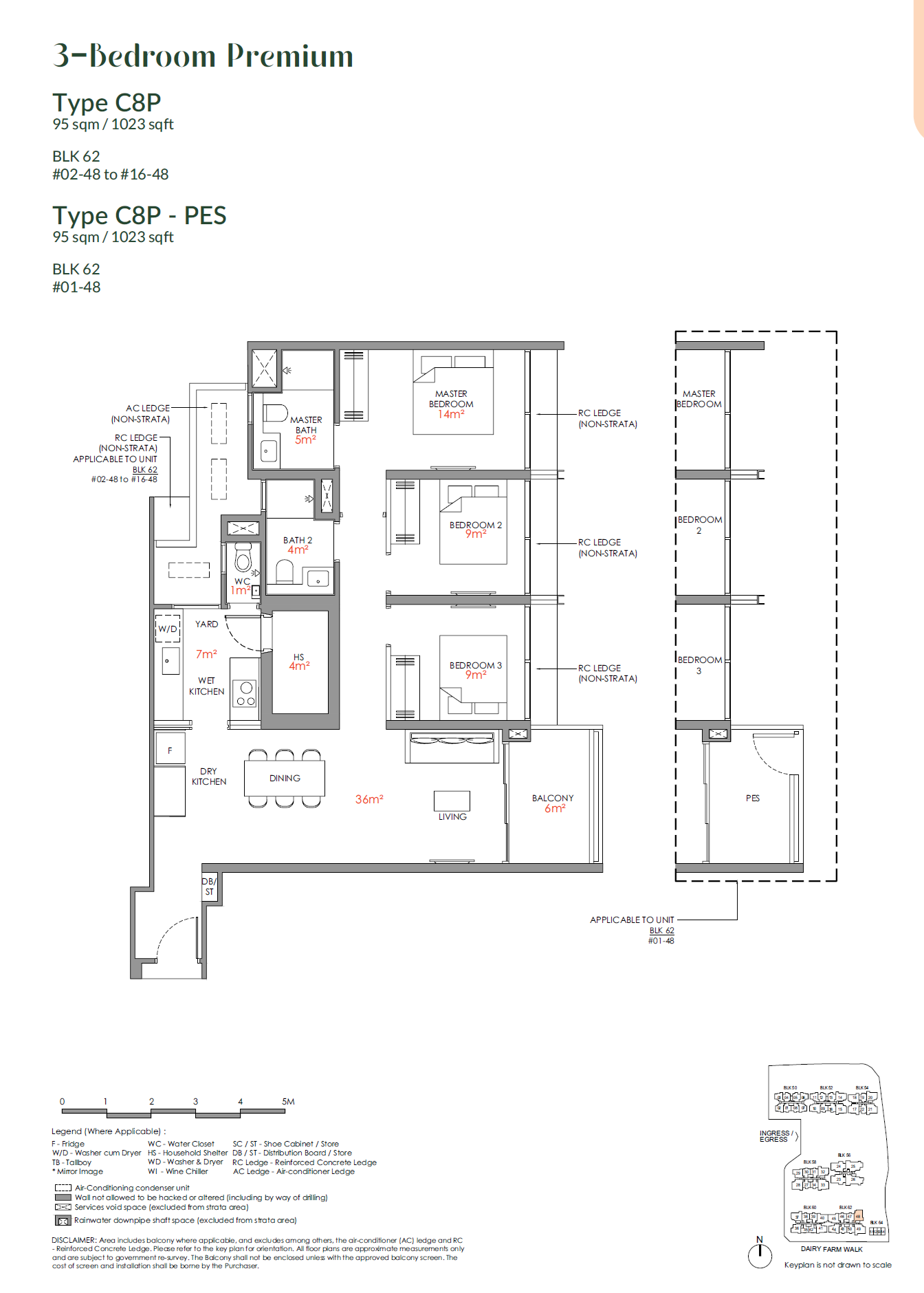

Here are the two best-value layouts still on the chart — the 721 sqft two-bedder (the largest pool of remaining stock, 85 units) and the 1,023 sqft 3-bedroom Premium (the cheapest PSF in the project):

What that S$2,190 is built on — the resale next door

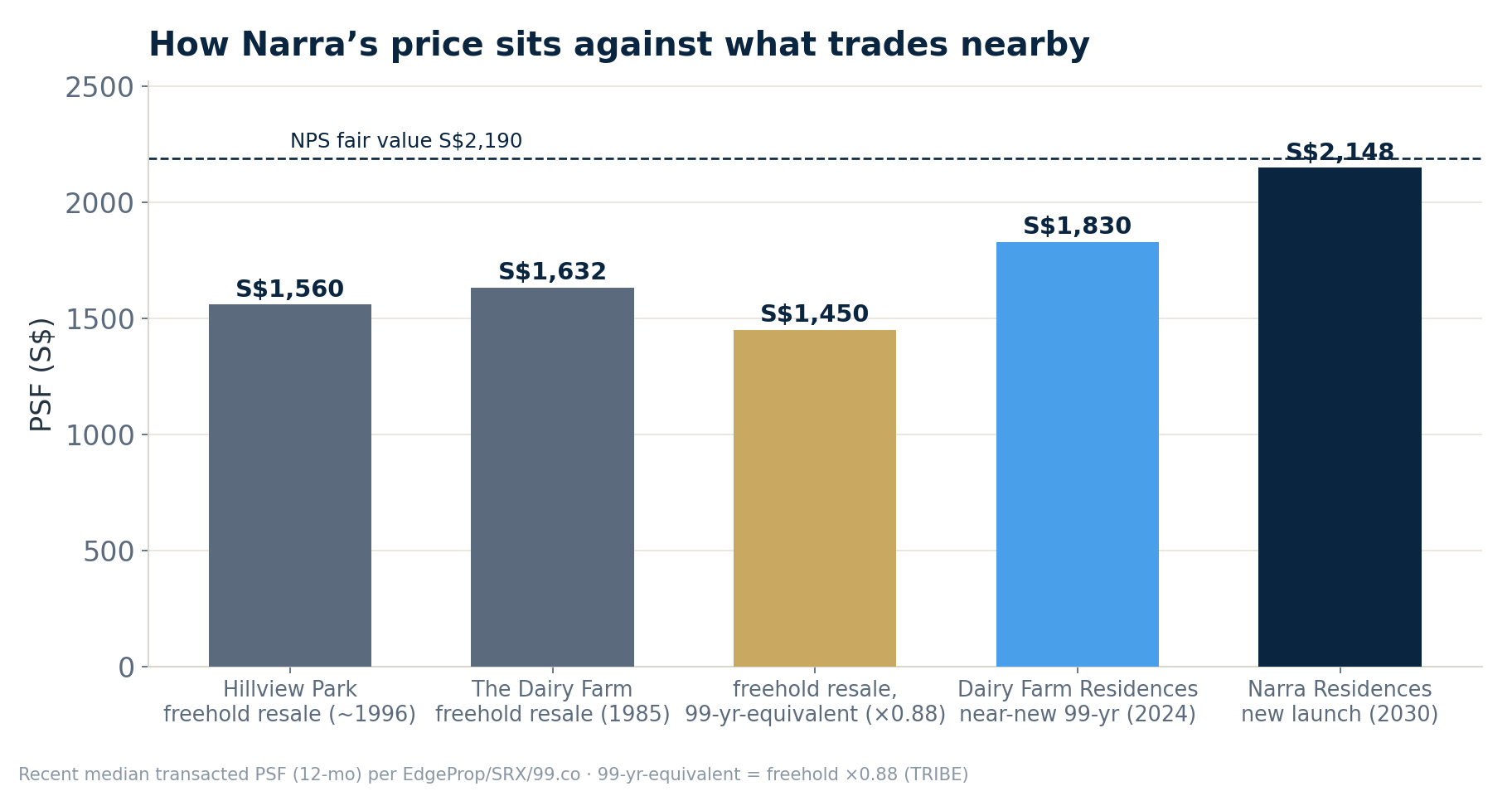

Fair value isn't an opinion; it's what comparable homes within walking distance actually trade for. Three established projects ring the Dairy Farm Walk plot, and their recent transacted prices set the floor Narra is priced against.

| Comparable | Tenure · age | Distance | Recent transacted PSF | Basis |

|---|---|---|---|---|

| The Dairy Farm | Freehold · 1985 | ~0.2 km | ~S$1,632 | 12-month resale median (range S$1,535–1,796) |

| Hillview Park | Freehold · ~1996 | ~1.0 km | ~S$1,560 | 12-month resale median |

| Dairy Farm Residences | 99-year · TOP 2024 | adjacent | ~S$1,830 | 2025 secondary median (35 deals) |

Two of the three are freehold, so to compare them like-for-like with Narra's fresh 99-year lease you have to pro-rate for tenure. A fresh 99-year leasehold typically trades at roughly a 12% discount to an equivalent freehold in this market; applying that, the mature freehold stock is worth about S$1,375–1,440 psf on a 99-year-equivalent basis. The cleanest benchmark needs no adjustment at all: Dairy Farm Residences, the near-new 99-year project on the adjacent plot, last changed hands around S$1,830 psf — a true fresh-leasehold, same-street reference.

Stack them up and the read is honest. Mature resale here runs S$1,560–1,632 psf freehold — about S$1,375–1,440 once you put it on Narra's lease terms. The only recent fresh-99-year comparable sits at ~S$1,830. And Narra is launching around S$2,148 psf (the median of 138 units sold), with the scorecard's fair value at S$2,190. So Narra asks roughly 17% above the most comparable recent leasehold and 30–40% above mature freehold resale — closer to 50% once that freehold stock is put on a like-for-like 99-year basis. That gap is what a brand-new unit, full facilities and a fresh 99-year lease cost over older stock. The fair-value line is real, but you are buying at the top of the local range, not below it — which is exactly why, on the stacks above, the entry price you negotiate decides whether the holding period works.

The holding period, both ways

Here is where "honest" earns its place. Using the NPS calculator's model — 2.8% expected price growth, a 3% annual target — we estimate the holding period for each stack two ways: on price growth alone, and with the area's ~3.3% rental yield added. We show both rather than assume you're an owner-occupier or a landlord.

| Available stack | PSF | Hold (price only) | Hold (with rent) |

|---|---|---|---|

| 3BR Premium · 1,023 sqft | 2,020 | 4–6 yrs | 4–6 yrs |

| 2BR · 700 sqft | 2,023 | 4–6 yrs | 4–6 yrs |

| 2BR · 721 sqft | 2,062 | 4–6 yrs | 4–6 yrs |

| 4BR · 1,152 sqft | 2,125 | 4–6 yrs | 4–6 yrs |

| 2BR Premium · 646 sqft | 2,197 | Doesn't reach 3% | 4–6 yrs |

| 3BR · 872 sqft | 2,242 | Doesn't reach 3% | 4–6 yrs |

| 2BR · 560 sqft | 2,305 | Doesn't reach 3% | 4–6 yrs |

| 5BR · 1,658 sqft | 2,345 | Doesn't reach 3% | 4–6 yrs |

The pattern is clean. Every stack priced at or below the S$2,190 fair value clears a 3% return in the 4–6 year tier on price growth alone. Every stack priced above it fails to reach 3% on price alone — the modelled 2.8% growth never overtakes the premium you paid plus the target — and only works once you count rental income, at which point it too lands in the 4–6 year tier. In other words, at the wrong entry price Narra becomes a rental play whether you intended it or not.

Two honest caveats sit on top of this. These figures are gross of costs — buyer's stamp duty, financing and selling costs are not netted out, so a real round trip adds time. And the seller's stamp duty makes selling in the first years punitive regardless of the model, so treat four years as a practical floor, not a target. The calculator's slider lets you test a different return target; at a 3% target, the table above is the read.

The honest verdict

Narra Residences is a competent grade-B suburban launch whose scorecard is dragged down by exactly what you'd expect from a Dairy Farm Walk address: distance from the MRT. Its expected price growth of ~2.8% a year is below a 3% bar, so this is not a quick-flip project — it is a hold-for-the-long-run home or a rental asset, and the data says so rather than dressing it up.

But the 63% of unsold inventory is an advantage for a disciplined buyer, because it means you can be choosy on price. The larger two-bedders and the 3-bedroom Premium stacks at S$2,020–2,125 psf — 3–8% under fair value — are where the maths works on price growth alone. Pay up for the small 560 sqft units or the 5-bedders at a 5–8% premium and you're relying on rent to get there. The grade is fixed; your entry price is not. On this project, the price you negotiate is the whole game.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade, sub-scores, expected growth and fair value per the TRIBE New Project Scorecard (URA Data Service transacted PSF; figures as at June 2026). Available units, sizes and PSF from the project price list as at 17 June 2026; availability changes as units sell. Holding periods computed with the published NPS calculator model (median transacted PSF fair value, modelled growth, 3% target; gross of stamp duty, financing and selling costs). Comparable resale prices (The Dairy Farm, Hillview Park, Dairy Farm Residences) are recent median transacted PSF from public caveats via EdgeProp, SRX and 99.co; the 99-year-equivalent basis applies a ~12% freehold-to-fresh-leasehold adjustment (TRIBE convention). Project rendering and unit floorplans are from the developer's marketing materials (artist's impressions; floorplans indicative, not to scale). Scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.