Insights

What Will I Actually Pay After Grants? An HDB First-Timer's Worked Guide

The most-searched BTO and resale question isn't the sticker price — it's the price after grants. We stack the three first-timer grants by income, citizenship and flat type, and run three real household examples down to the dollar.

By TRIBE Editorial · 16 June 2026 · 9 min read

The first number every flat-hunter chases is the price on the listing. It's almost never the number that matters. For a first-timer household, the question that actually decides affordability is the one most people only work out after they've fallen for a flat: what do I pay once the grants land? On a resale flat the grants can run into six figures — enough to move a flat from "out of reach" to "comfortable" without a single dollar changing on the price tag. This is the worked guide to that gap.

The catch is that there is no single grant. There are three for families, they stack, and how much you get swings wildly with your income, your citizenship mix, the flat size, and how close you'll live to your parents. Two couples buying the same 4-room flat next door to each other can walk away with cheques tens of thousands of dollars apart. Here's how the stack is built, and what three real-shaped households actually collect.

The three grants that stack

For a resale flat bought by a first-timer family of Singapore Citizens, three grants can layer on top of one another. Each one answers a different question.

The Family Grant rewards you for buying a resale flat as a family. It's worth S$80,000 for a 2- to 4-room flat and S$50,000 for a 5-room or larger. There's a citizenship adjustment: if one spouse is a Singapore Permanent Resident rather than a citizen (an SC+SPR couple), the grant drops by S$10,000 — to S$70,000 and S$40,000 respectively. This grant is resale-only; it does not exist for a BTO flat.

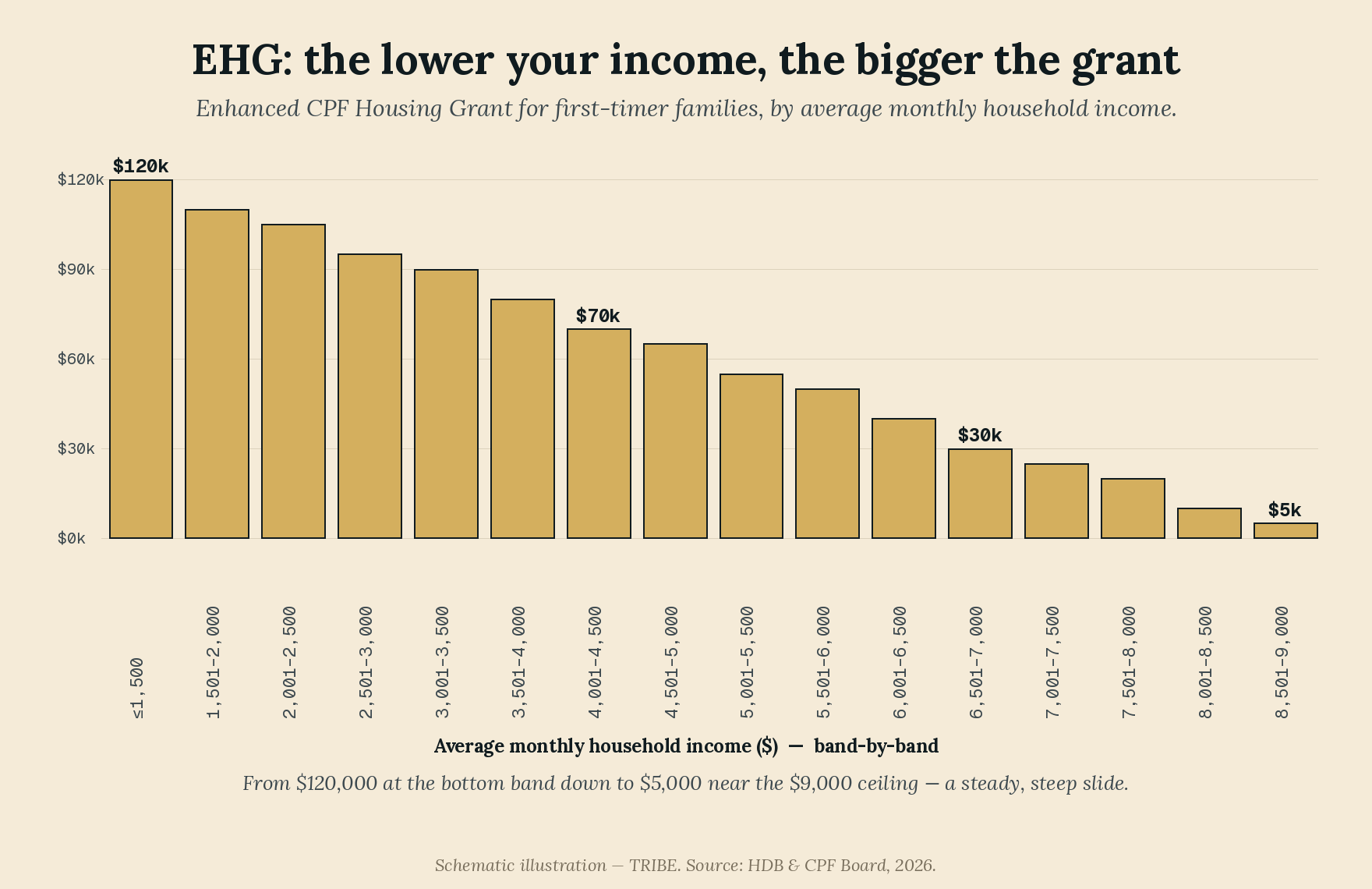

The Enhanced CPF Housing Grant (EHG) is the big, income-tested one, and it's the only grant that applies to both BTO and resale. It's worth up to S$120,000, but the exact figure slides down as your average monthly household income rises, on a tight sixteen-step ladder. The income ceiling is S$9,000 a month for two first-timers (it halves to S$4,500 if a first-timer buys with a second-timer). The ladder is the heart of the whole scheme, so it's worth seeing in full:

The shape is deliberate. The lower your income, the more help you get to buy — S$120,000 at the very bottom, melting to S$5,000 just under the ceiling. For most working couples the EHG lands somewhere in the middle of that slide, and a pay rise that nudges you into the next band genuinely costs you grant money. It's worth knowing which band you're in before you firm up the purchase.

The Proximity Housing Grant (PHG) rewards buying near family. Live with your parents or child in the flat and it's worth S$30,000; buy a flat within 4km of them and it's S$20,000. Unlike the EHG, the PHG has no income ceiling — a high earner who buys near mum and dad collects it in full. It is resale-only, like the Family Grant.

Two conditions on the EHG are worth flagging now, because they catch people. At least one applicant must have been in continuous employment for the 12 months before applying and still be working when the flat application goes in. And the flat's remaining lease must be long enough to cover the youngest buyer to age 95 — if it falls short, the EHG is pro-rated down. On an older resale flat with a shorter lease, that pro-ration can quietly shave thousands off the headline figure.

Worked examples: same scheme, very different cheques

Numbers make this concrete. Below are three households shaped like real buyers we see. The totals are computed straight off the tables above — but treat them as illustrative: your actual grants depend on HDB's HFE (HDB Flat Eligibility) assessment of your specific circumstances.

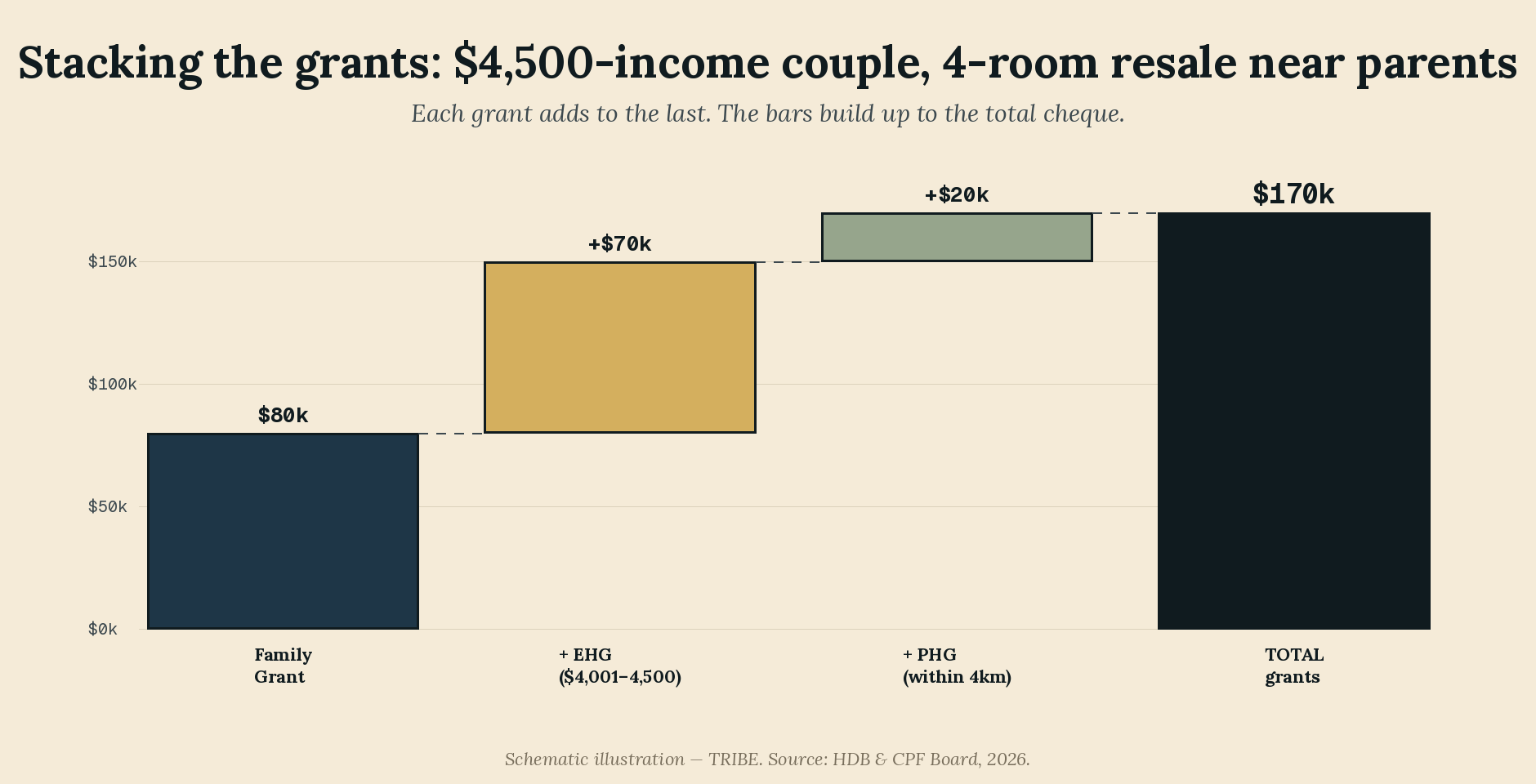

Start with the household that collects the most — a modest-income couple buying near family, where all three grants fire:

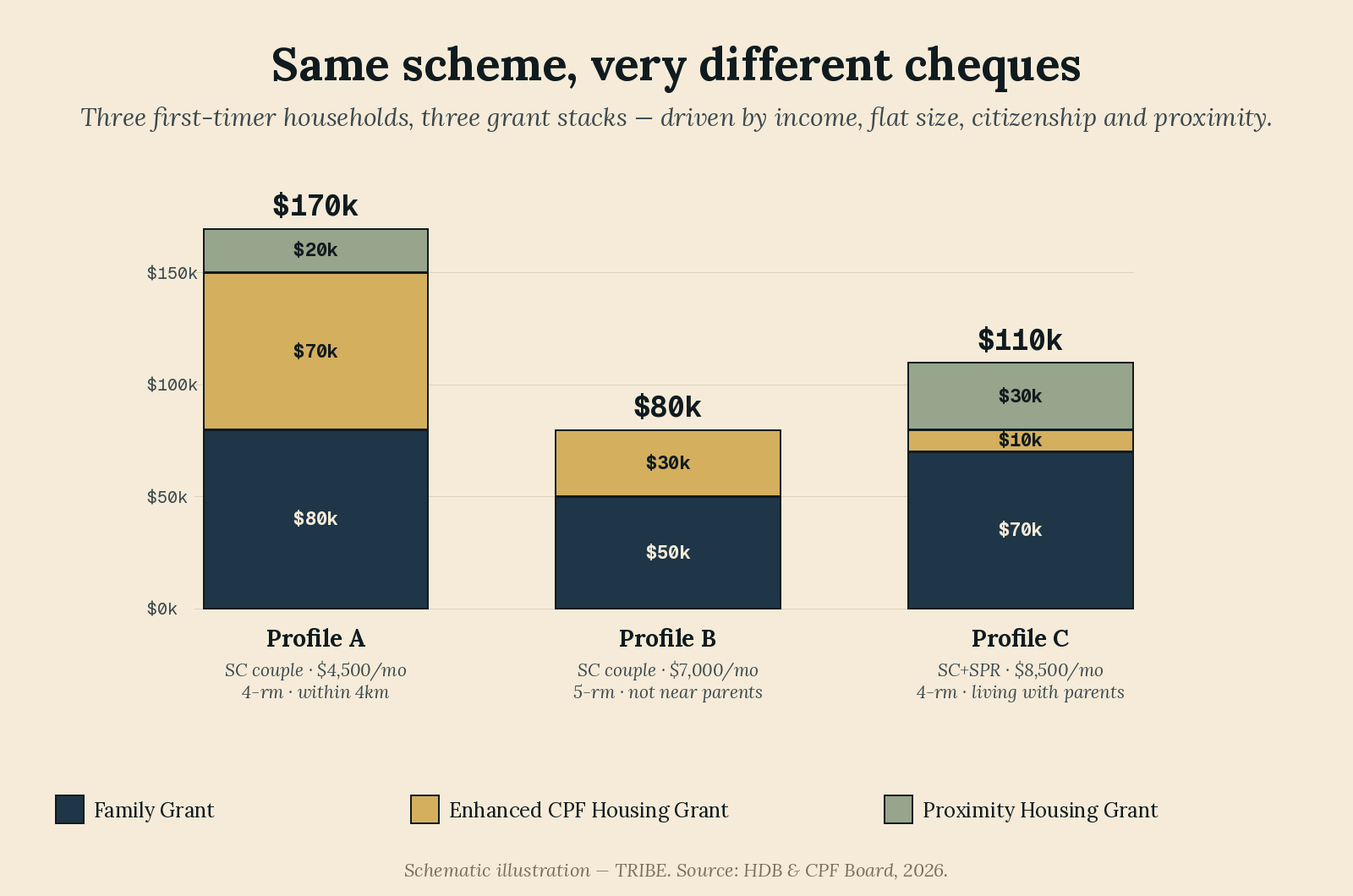

Now the same three grants across all three profiles side by side, so you can see how the stack reshuffles as income, flat size and citizenship change:

| Profile | Household | Flat | Family Grant | EHG | PHG | Total grants |

|---|---|---|---|---|---|---|

| A — first home, modest income | SC couple, $4,500/mo combined | 4-room resale, within 4km of parents | $80,000 | $70,000 (band $4,001–4,500) | $20,000 (within 4km) | $170,000 |

| B — higher income, bigger flat | SC couple, $7,000/mo combined | 5-room resale, not near parents | $50,000 (5-room) | $30,000 (band $6,501–7,000) | $0 | $80,000 |

| C — mixed citizenship, multi-gen | SC + SPR couple, $8,500/mo combined | 4-room resale, living with parents | $70,000 (SC+SPR) | $10,000 (band $8,001–8,500) | $30,000 (with parents) | $110,000 |

Three lessons fall straight out of the table. Income is the biggest lever on the EHG — Profile A's S$70,000 versus Profile B's S$30,000 is almost entirely the income band. Flat size moves the Family Grant — Profile B's 5-room choice costs S$30,000 against a 4-room, before income even enters. And proximity is free money the high earners can still get — Profile C, the highest earner here, collects the full S$30,000 PHG simply by moving in with parents, no income test applied. The household that earns the most doesn't get the least; the stack rewards different things.

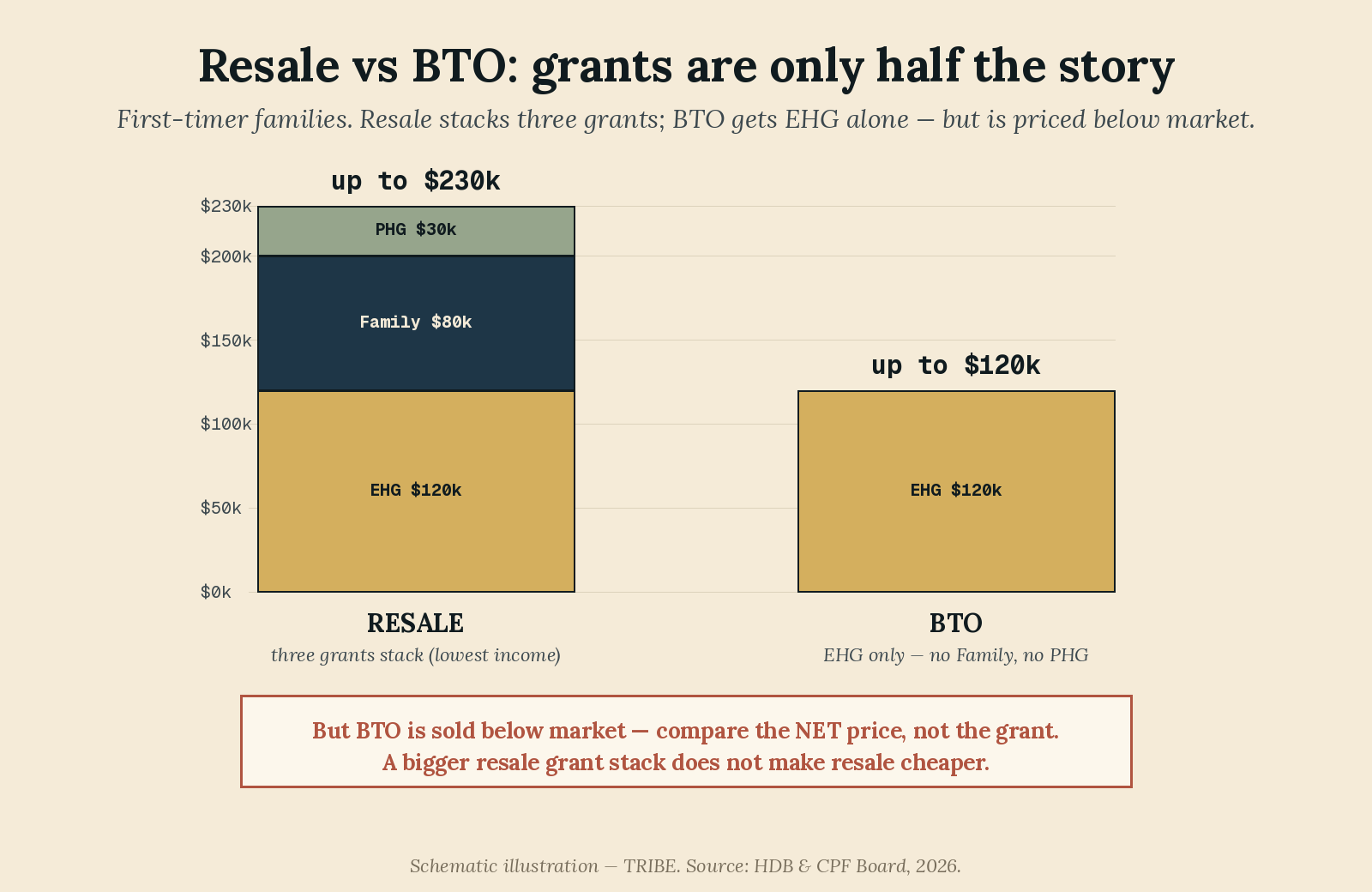

Resale vs BTO: grants are only half the story

Here's where a lot of first-timers talk themselves into the wrong conclusion. The resale grant stack is much bigger than what a BTO buyer gets — so resale must be the cheaper route, right? No. It's a trap, and it's worth drawing out.

On a BTO flat, a first-timer family gets the EHG only — no Family Grant, no Proximity Grant. So Profile A's S$4,500 couple, who collected S$170,000 buying resale, would get just the S$70,000 EHG on an equivalent 4-room BTO. At the very best case the maths is stark: resale grants can stack to S$230,000 (EHG $120k + Family $80k + PHG $30k, only at the lowest income), against a BTO ceiling of S$120,000.

But the grant is not the price. BTO flats are sold by HDB at a discount to the market; resale flats trade at full market price. The bigger resale grant is, in large part, the government topping up the gap between a market price and a subsidised one. The honest comparison is the net cash you part with — purchase price minus every grant — not the size of the grant cheque. A BTO with a smaller grant can easily land cheaper net than a resale with a bigger one. Run both nets before you let the grant headline decide.

The catch: the grant is a loan to your future self

Two more things to internalise before you bank on these numbers.

First, the grants are not a gift you keep free and clear. They're paid into your CPF Ordinary Account and reduce the loan and cash you need up front — which is real, immediate help. But when you sell the flat, the grant amount plus accrued interest at 2.5% a year must be returned to your CPF OA. It's reusable for your next home, so it isn't lost; but it does mean the grant isn't spendable cash on the way out, and the 2.5% compounding quietly grows the sum you'll need to refund. Think of it as an interest-bearing loan from your future self, not a discount.

Second, the conditions are real gates, not fine print. The EHG's twelve-month continuous-employment rule means a buyer who just changed careers or took a break may not qualify the way they assume. The lease-to-95 rule means an older, shorter-lease resale flat can pro-rate the EHG down — exactly the flats that look cheap on paper. Check both against your own situation before you treat any figure here as banked.

Where to start

Don't reverse-engineer your budget from a listing and a guessed grant. Do it the other way round: apply for your HDB Flat Eligibility (HFE) letter first. The HFE assessment is what actually fixes your grant entitlement, your loan eligibility and your budget ceiling — in writing, before you commit to a flat. Walk into viewings knowing the real number you'll pay after grants, not the sticker price, and the most-searched question answers itself.

Sources: CPF Board — guide to the EHG and Proximity Grant; HDB Enhanced CPF Housing Grant (Families); 99.co — HDB resale grants 2026. Figures current as at 2026; grant amounts subject to HDB's HFE assessment.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the Resale Project Scorecard (RPS) using 236,000+ URA REALIS transactions. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Know what you can afford

Loan, stamp duty, CPF, and monthly repayments — work out your real budget before you commit. No registration required.

Plan my purchase →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.