Insights

Rents Have Stopped Falling. Yields Still Haven't Recovered.

Private rents ticked up 0.3% in Q1 2026 — the bottom is in. But prices rose faster, so the gross yield on a typical condo is stuck near 3%, and the net yield, after tax and maintenance, is closer to 2.3%.

By TRIBE Editorial · 20 June 2026 · 7 min read

For two years the story in Singapore's rental market was the same: a wave of new completions handed tenants the bargaining power, and rents drifted down off their 2023 peak. That chapter has closed. URA's Q1 2026 data shows the private residential rental index up 0.3% quarter-on-quarter to 161.4, partly clawing back the 0.5% dip of the previous quarter, and up 1.8% year-on-year. The bottom is in. What has not arrived is the thing landlords actually wanted from a recovery — a meaningful rebound in yield. Prices kept climbing while rents merely stopped falling, so the gap between what you pay for a condo and what it earns is about as wide as it has been. Here is what the data says, and what it does to the only number a landlord should care about.

The recovery is real, but it is mild and uneven

Three things stand out in the Q1 2026 rental numbers. First, the recovery is modest — a 0.3% quarterly rise is a flattening, not a surge, and at 161.4 the index sits below where it peaked. Second, it is led by the suburbs: the Outside Central Region (OCR) posted the strongest growth, up 1.0% q/q to 169.5, while the Core Central Region (CCR) rose 0.5% to 151.1 and the Rest of Central Region (RCR) actually slipped 0.2% to 172.3. Prime-district rents — the ones most exposed to the expat-package pullback of the last two years — remain the soft spot. Third, leasing is active: 21,765 rental contracts were signed across landed, non-landed, and EC homes in the quarter, so this is a functioning market finding a floor, not a frozen one.

The non-landed segment, where most condo investors actually play, did the heavy lifting on the annual figure: up 2.2% year-on-year, against just 0.2% for landed. So if you own a condo to rent out, your gross rent is probably a little higher than a year ago. The problem is what happened to the denominator.

Why a rent recovery didn't lift the yield

Yield is rent divided by price, and in Q1 2026 the price side rose faster than the rent side. URA's overall private property price index climbed 0.9% in the same quarter, on top of steady gains through 2025. When prices grow faster than rents — even with rents recovering — the yield compresses. A landlord can collect more rent than last year and still earn a lower percentage return on today's market value of the flat. That is the trap of a price-led market: the asset gets more expensive faster than it gets more productive.

The cleanest way to see it is to price a few realistic 2026 condos at current market rents.

| Condo (illustrative) | Price | Monthly rent | Annual rent | Gross yield |

|---|---|---|---|---|

| OCR 2-bed | $1.30m | $3,600 | $43,200 | 3.32% |

| OCR/RCR 3-bed | $1.60m | $4,200 | $50,400 | 3.15% |

| CCR 3-bed | $2.20m | $5,200 | $62,400 | 2.84% |

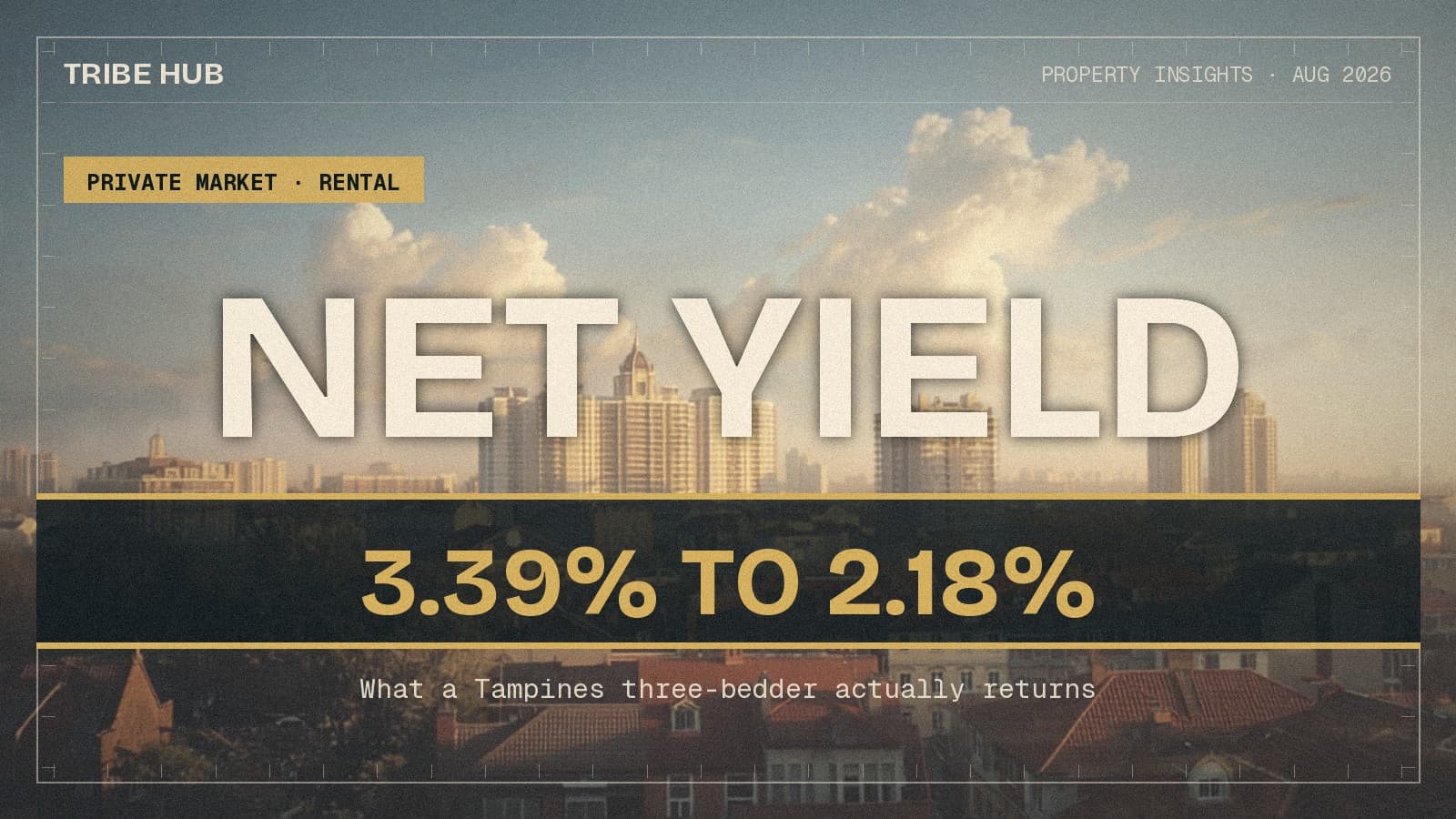

Even the best of these clears 3% only barely, and the prime-district unit — where rents are weakest and prices highest — sits under it. A 3% gross yield is not a disaster, but it is thin, and it is the number that flatters the picture, because it ignores every cost of actually being a landlord.

Gross is the brochure. Net is the cheque.

The yield that matters is what lands in your account after the costs the rent has to cover first. Three bite hardest in 2026, and none of them is the mortgage.

The largest is property tax, which for a rented-out home is charged at the non-owner-occupier rates — a progressive schedule running from 12% on the first $30,000 of annual value up to 36% at the top. On the $1.6m unit, the annual value works out near $45,000, which produces a tax bill of roughly $6,700 a year. Then there is maintenance — call it $400 a month, or $4,800 a year, for a typical condo — and a realistic vacancy and re-letting allowance of about two weeks a year plus agent costs, roughly $2,000. Run those through the same three flats:

| Condo | Gross yield | Property tax | Maint. | Vacancy | Net yield |

|---|---|---|---|---|---|

| $1.30m @ $3,600 | 3.32% | ~$5,400 | $4,800 | ~$1,700 | 2.41% |

| $1.60m @ $4,200 | 3.15% | ~$6,700 | $4,800 | ~$2,000 | 2.31% |

| $2.20m @ $5,200 | 2.84% | ~$9,700 | $4,800 | ~$2,500 | 2.06% |

The net yield on a typical 2026 condo is roughly 2.0% to 2.4% — and that is before a single dollar of mortgage interest. A landlord who borrowed to buy is, at today's prices and rents, very often running the property at a cash cost in the early years and relying entirely on capital appreciation to make the investment work. That is a legitimate strategy. It is also a completely different bet from "the rent covers the loan," which is the assumption a lot of buyers still carry into a viewing.

What it means for a buyer in mid-2026

The honest read of the rental recovery is that it changes the mood more than the math. Rents have found a floor, so the downside risk that haunted 2024–25 landlords has eased — but the recovery is too mild, and prices too firm, to have rebuilt the income case. A few things follow.

If you are buying to rent, underwrite to the net yield, not the gross. A 3.1% brochure number is a 2.3% reality, and if you are borrowing, your real cash return in the first years may be negative — fine if you are buying for appreciation and can fund the gap, dangerous if you assumed the tenant would. If income is the priority, the data points to the suburbs and to lower quantum: OCR rents are growing fastest and smaller units carry higher gross yields, while prime-district stock combines the weakest rents with the highest prices. And whatever you buy, the yield factor is exactly why a scorecard separates a good address from a good investment — a freehold flat next to a brand-name school can be a superb place to live and a mediocre place to park rental capital, and the only way to tell the difference is to run the net number before you fall for the flat.

Rents have stopped falling. That is genuinely good news for anyone who already owns. It is not, on its own, a reason to expect the income side of a Singapore condo to start paying its way again.

Sources: URA — Q1 2026 private residential rental statistics (rental index, regional breakdown, contract volume); ERA — 1Q 2026 Rental Report; CBRE — commentary on the Q1 2026 price index. Property-tax bands are the 2024-onward non-owner-occupier residential rates; yield figures are computed for the stated illustrative prices and rents.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the Resale Project Scorecard (RPS) using 236,000+ URA REALIS transactions. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.