Insights

The Mid-2026 Mortgage Check: Reprice or Refinance? The Worked Math.

Rates are near a five-year low, but acting on that splits into two different decisions with different costs. Repricing keeps you with your bank — fast and nearly free. Refinancing moves you to a new one — cheaper rate, real fees. We run the numbers on an $800k loan and show where each one wins.

By TRIBE Editorial · 14 June 2026 · 7 min read

If your home loan was written before 2025, you are almost certainly overpaying right now. Singapore mortgage money is near a five-year low — and unlike a buyer deciding how much to borrow, an existing owner's question isn't whether the cheap rates help, but how to reach them. There are two doors, and people conflate them constantly: you can reprice (switch to a new package with your current bank) or refinance (move the loan to a different bank). They cost different things, take different amounts of time, and win in different situations. This is the mid-year check on which one is yours.

(If you're a buyer rather than an owner, the more relevant read is our companion piece on why halved rates haven't raised your borrowing power — the stress test still assumes 4%.)

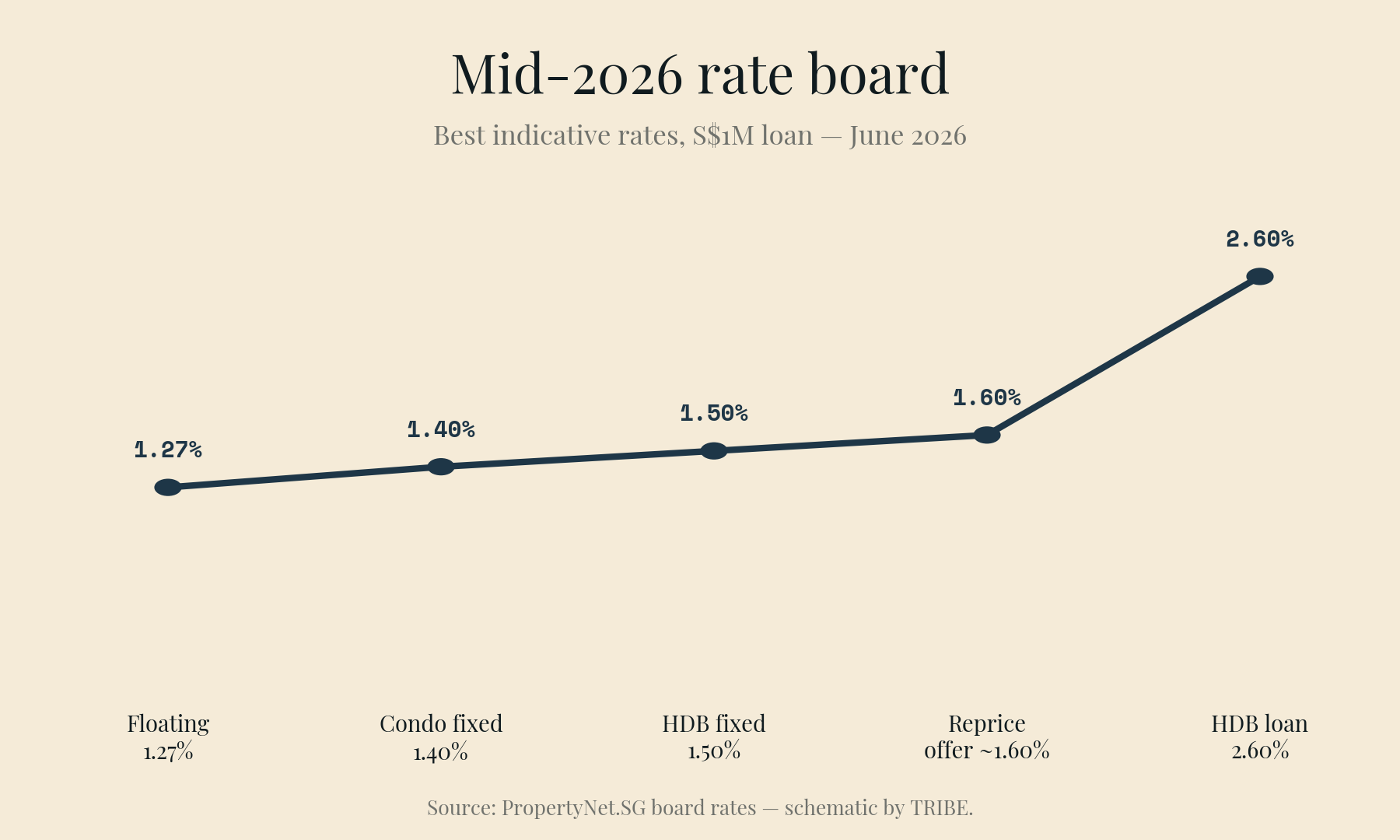

Where rates sit in mid-2026

The June 2026 board, per PropertyNet.SG's monthly tracking (indicative for a S$1M loan; your profile will vary):

| Package | Best rate | Note |

|---|---|---|

| Private condo, 2-yr fixed | 1.35–1.40% | sharpest new-customer pricing |

| Private condo, floating | 1.27% | 3M SORA + 0.20% |

| HDB, 2-yr fixed | 1.50% | |

| HDB concessionary loan | 2.60% | unchanged |

| Typical repricing offer | ~1.55–1.65% | retention rate from your existing bank |

That last row is the one most owners never see quoted, because it only appears once you ask your own bank to keep you. It is usually a notch above the sharpest refinancing rate — the bank is pricing in the friction of you leaving. Whether that notch is worth paying to avoid is the whole decision.

The two doors, side by side

Repricing is the low-friction option. You stay with your existing bank, sign a new package, and the change takes effect after roughly one month's notice. There's no fresh legal work, no new valuation, no re-assessment of your income — just an administrative or conversion fee, typically S$200–S$800. The catch is the rate: retention offers rarely match what a new bank will quote a fresh customer.

Refinancing is the higher-effort, higher-reward option. You move the loan to a new bank at its best new-customer rate, but you take on the full switching cost: legal and valuation fees of roughly S$1,800–S$2,500 (most banks subsidise these with a cash rebate on loans above ~S$500k), a three-month notice period to your existing bank, and a fresh TDSR and income-document assessment. If your income or debt profile has weakened since you first borrowed, that re-assessment is a real gate — repricing skips it.

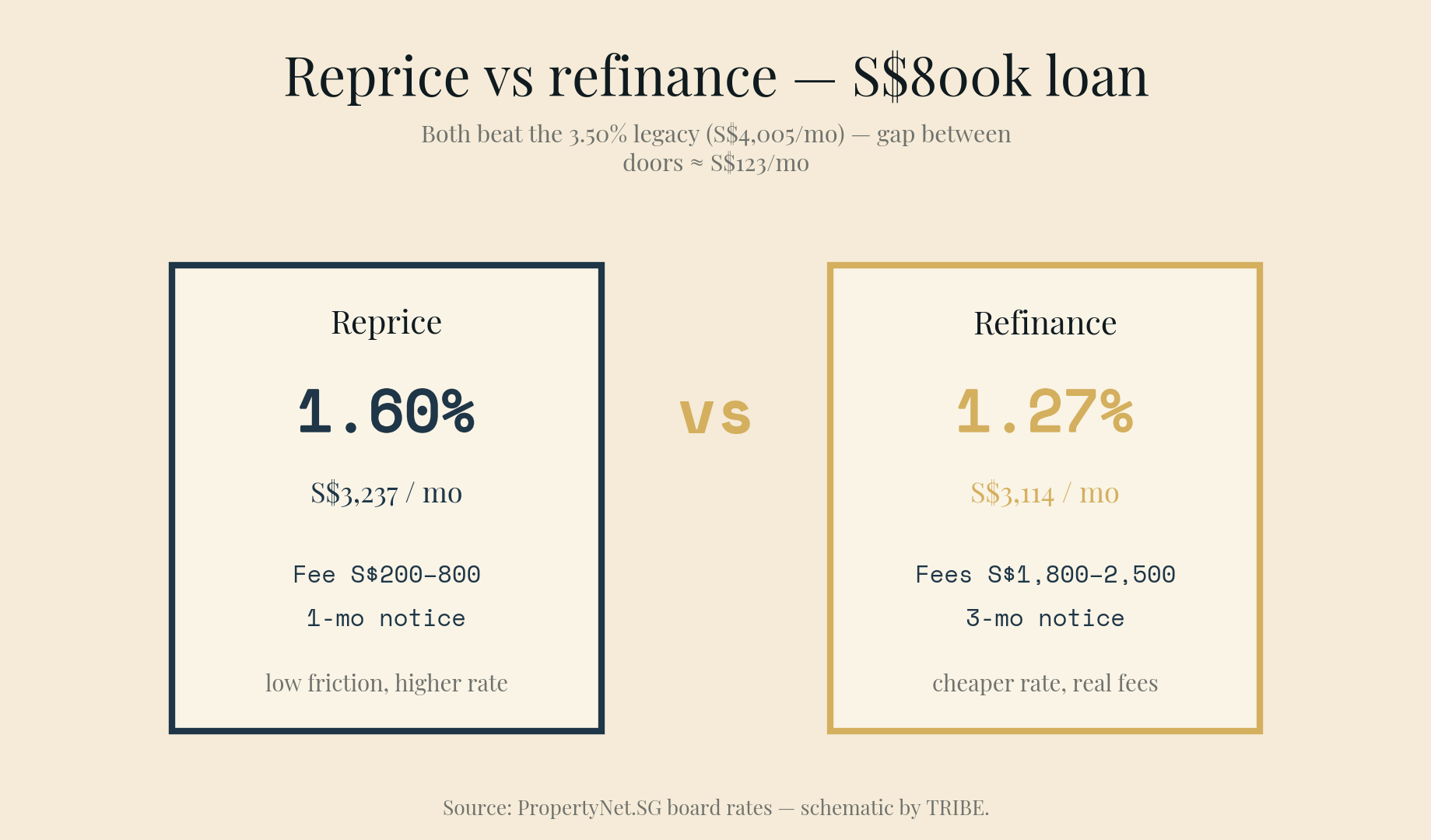

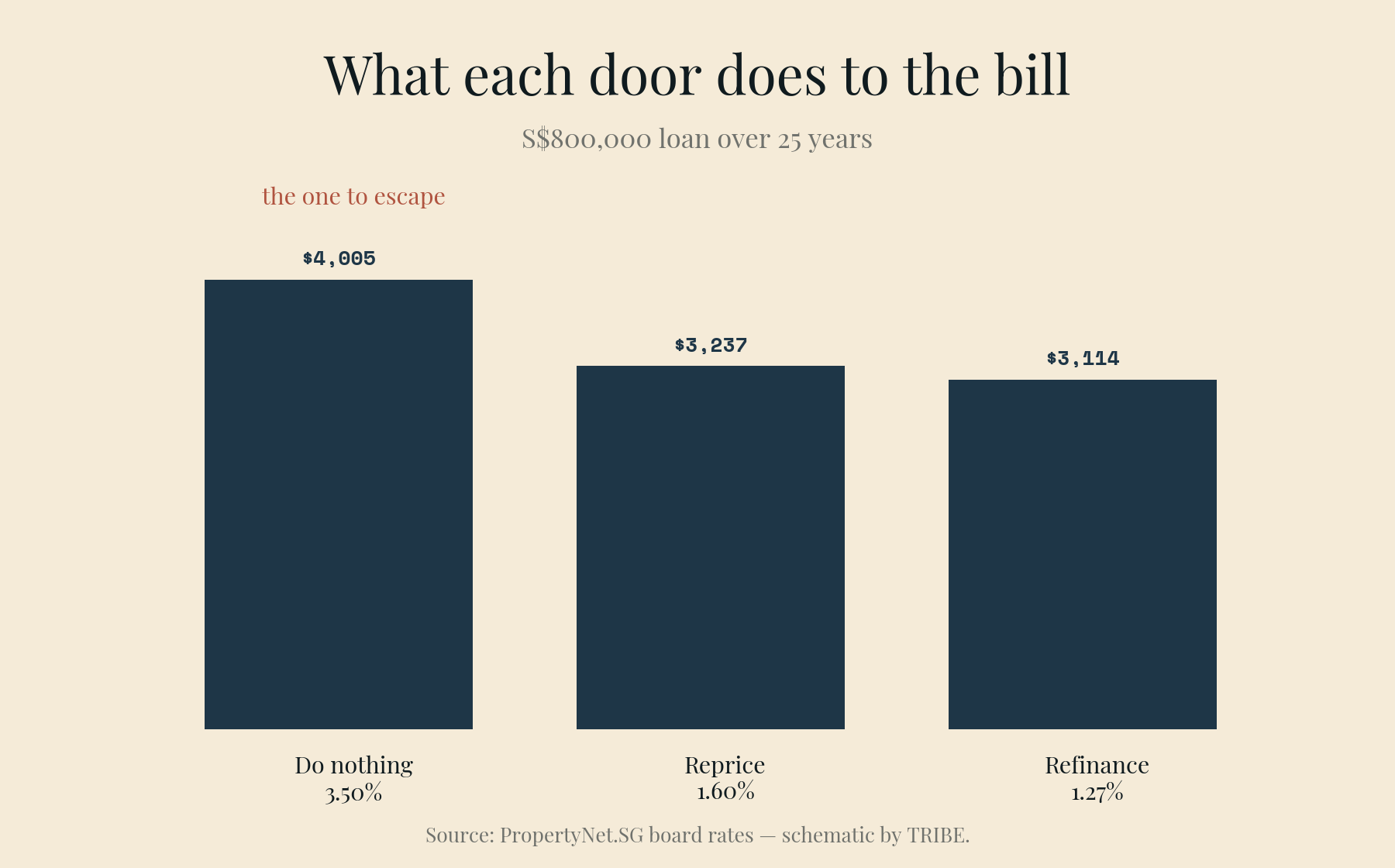

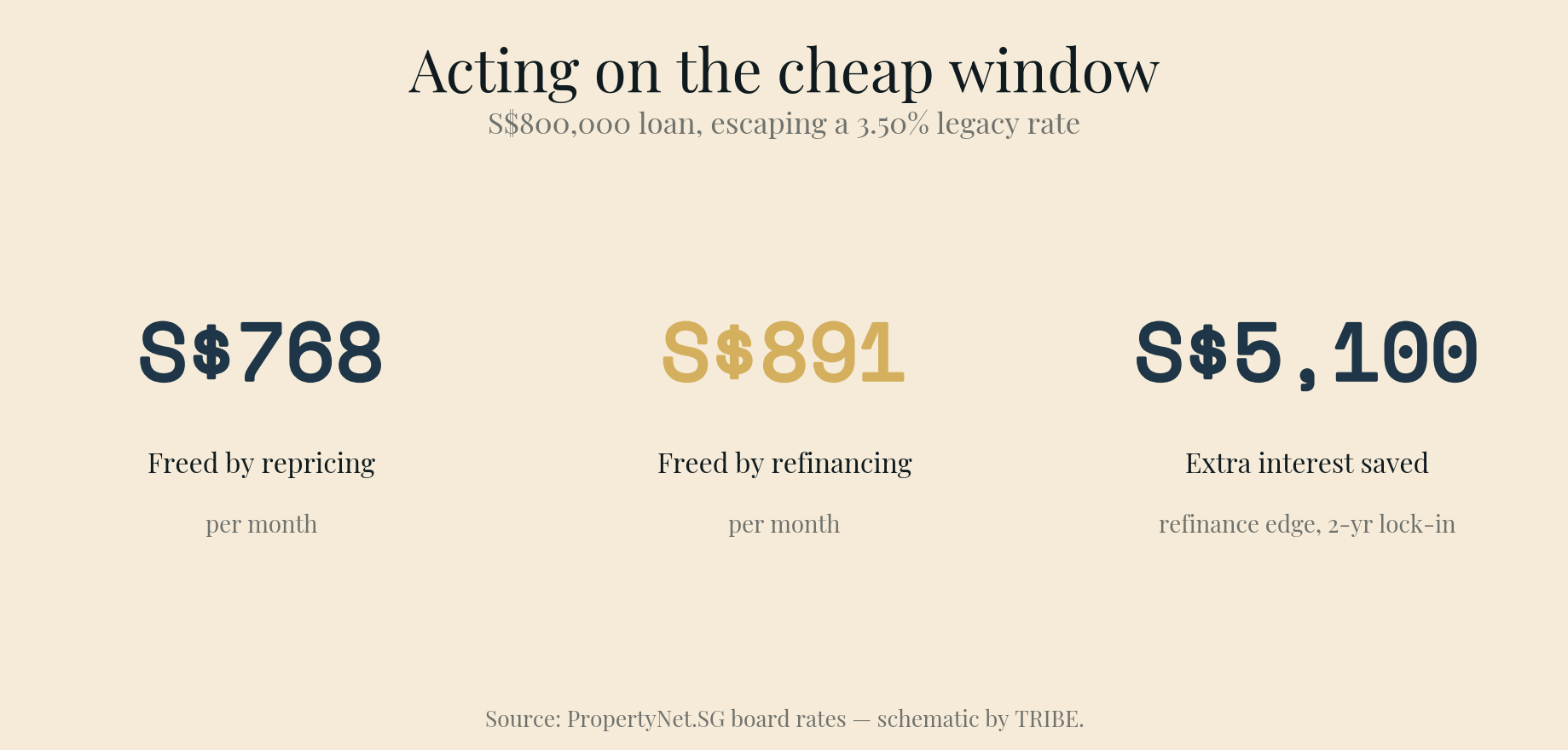

The worked math: an S$800,000 loan

Take a household carrying S$800,000 over a remaining 25-year tenure, still on a 3.50% rate from the last cycle. Here's what each door does to the monthly bill:

| Scenario | Rate | Monthly | Interest, first 2 years |

|---|---|---|---|

| Do nothing (legacy) | 3.50% | S$4,005 | ~S$54,600 |

| Reprice with current bank | 1.60% | S$3,237 | ~S$24,800 |

| Refinance to a new bank | 1.27% | S$3,114 | ~S$19,700 |

Both doors are enormous improvements over standing still — repricing alone frees about S$768 a month, refinancing about S$891. The interesting number is the gap between the two doors: roughly S$123 a month, or about S$1,480 a year, and around S$5,100 of extra interest over a two-year lock-in.

So the rule writes itself. If refinancing costs you nothing out of pocket (fees fully subsidised, no lock-in penalty to escape), the S$5,100 saving makes it the clear winner. If you'd pay S$2,000+ net to switch, that two-year edge shrinks to roughly S$3,000 — still positive, but now you're weighing it against three months of paperwork and a fresh income check. And if your current bank's retention desk sharpens its offer to within ~10bps of the market — which it often will once it knows you have a refinancing quote in hand — the gap can close to almost nothing, and repricing wins on effort alone.

Fixed versus floating, right now

For the new package itself, the live question is 1.40% fixed versus 1.27% floating. On an S$1M loan over 25 years that 13-basis-point gap is about S$60 a month — you are being charged very little for two years of rate certainty at a near-cyclical low. Unless you have a firm view that SORA sits at the bottom of its forecast band (consensus has it holding 0.7%–1.2% through 2026) or you plan to sell inside the lock-in, paying ~S$60 for the floor is cheap insurance.

One technical wrinkle worth catching if you go floating: 1M SORA (1.16%) is currently above 3M SORA (1.07%) and has been ticking up, so a 3-month-reset package is the cheaper peg this month — a reversal of the usual order. Pick the peg deliberately; don't default to the one your banker mentions first.

The timing mechanics that catch people

Three details decide whether any of this is actually available to you today:

Lock-in. If you're still inside your existing package's lock-in period, breaking it triggers a penalty — typically 1.5% of the outstanding loan (about S$12,000 on S$800k). That usually wipes out the saving. Repricing mid-lock-in is sometimes allowed penalty-free at the bank's discretion; refinancing out almost never is. Check your expiry date first — it's the gating fact.

The notice clock. Refinancing needs three months' notice to your current bank; repricing usually needs one. Start the conversation when you are four to six months from lock-in expiry, not after — retention offers improve precisely when the bank can see you're free to leave.

Subsidy clawback. If you take a refinancing cash rebate to cover legal fees, most banks claw it back if you redeem or refinance again within three years. That's fine if you intend to hold the package; it's a trap if you're rate-hopping every cycle.

What we'd actually do

If you're locked in above 3% and out of (or near the end of) your lock-in: act now — the saving is four figures a year either way. Get a refinancing quote first, then take it to your existing bank and ask them to reprice to match. You often capture most of the benefit with none of the legal fees or the three-month wait.

If the refinancing fees land near zero and you have a clean income profile: take the new bank's rate. The ~S$5,000 two-year edge is real money and the paperwork is a one-time cost.

If your income has dipped, you're self-employed with lumpy statements, or you simply value speed: reprice. Skipping the fresh TDSR assessment and the three-month clock is worth giving up ~10–15bps for.

If you're still mid-lock-in: do nothing yet except diarise your expiry date minus six months. The penalty almost always beats the saving until then.

General information only, not financial advice. Rates cited are indicative board rates for a S$1M loan as of mid-June 2026 and change without notice; actual pricing depends on loan size, property type, lock-in status, and borrower profile. Repricing and refinancing terms, fees, subsidies, and clawback periods vary by bank. TDSR, LTV, and CPF rules are set by MAS, HDB, and CPF Board and can change — verify current terms with your bank and the relevant agencies before committing.

Know what you can afford

Loan, stamp duty, CPF, and monthly repayments — work out your real budget before you commit. No registration required.

Plan my purchase →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.