Insights

Mortgage Rates Have Halved. Your Borrowing Power Hasn't. Here's the Worked Math.

Two-year fixed packages now start at 1.40% and 3M SORA sits at 1.07% — down from a ~3% peak in early 2025. But the bank still stress-tests you at 4%, so cheap money cuts your monthly bill, not your maximum loan. We run the actual numbers on a $1M loan, the HDB 2.6% question, and refinancing.

By TRIBE Editorial · 11 June 2026 · 7 min read

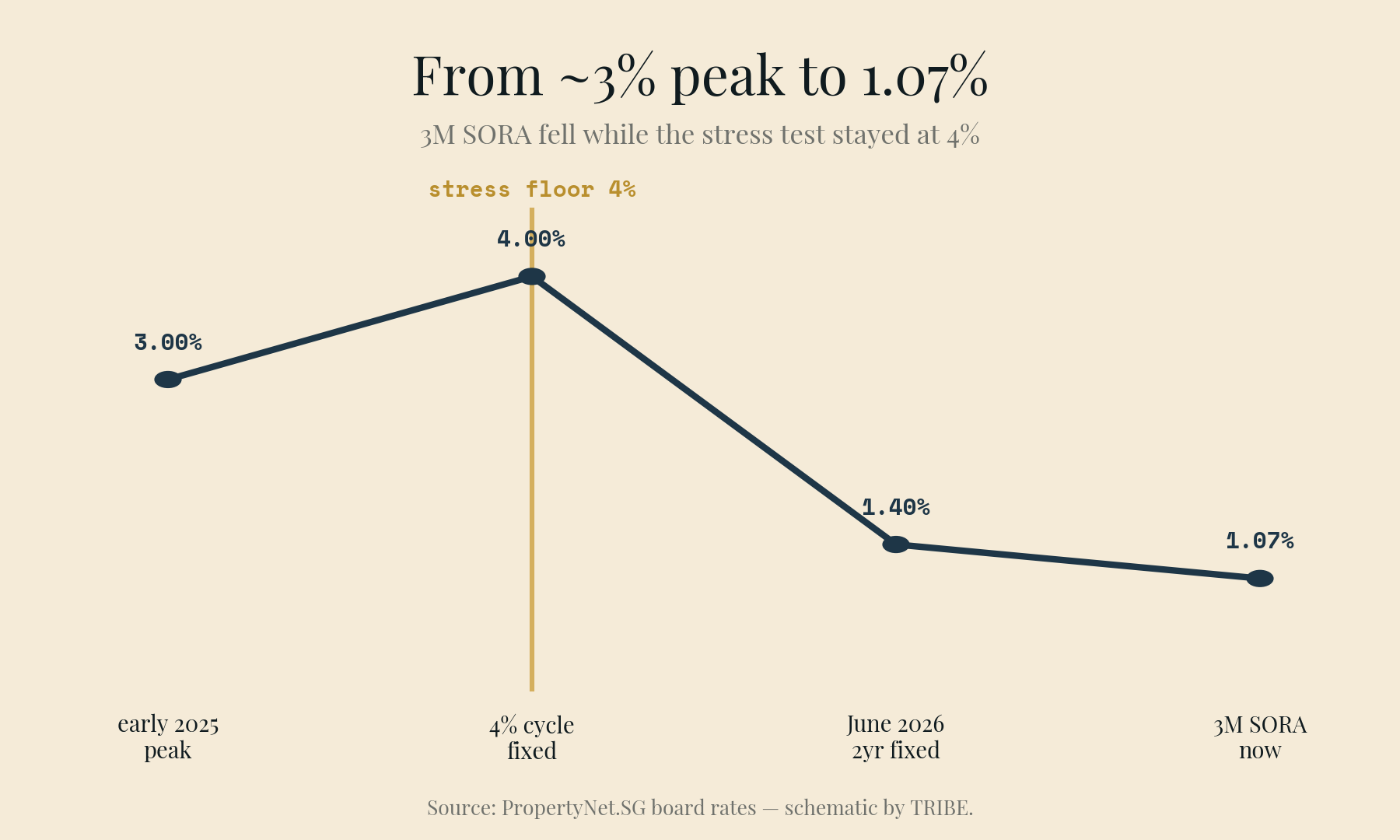

Singapore mortgage money is the cheapest it has been in roughly five years. As of June 2026, two-year fixed packages for completed private property start at 1.40%, the best floating packages price at 3M SORA + 0.20% — an all-in 1.27% — and 3M compounded SORA itself sits at 1.07%, down from a peak of around 3% in early 2025.

Halved rates change two numbers most people conflate: what a loan costs you each month, and how much the bank will lend you. The first has improved dramatically. The second has barely moved — because the TDSR stress test never followed rates down. Understanding that split is the difference between using this window well and letting it talk you into a bigger purchase than the rules will approve.

Where rates actually are

The June 2026 board, per PropertyNet.SG's monthly tracking (indicative for a S$1M loan; your profile will vary):

| Package | Best rate | Who |

|---|---|---|

| Private condo, 2-yr fixed | 1.40% | HSBC (Citi, DBS, Maybank at 1.45%) |

| Private condo, floating | 1.27% | HSBC / Maybank (3M SORA + 0.20%) |

| HDB, 2-yr fixed | 1.50% | HSBC / DBS |

| HDB, floating | 1.32% | OCBC (3M SORA + 0.25%) |

| HDB concessionary loan | 2.60% | HDB (unchanged) |

Two benchmark details worth noticing. 1M SORA (1.16%) is now above 3M SORA (1.07%) and rising faster — so quarterly-repricing packages are the cheaper peg this month, a reversal of the usual pattern. And the consensus forecast has SORA holding in a 0.7%–1.2% band for the rest of 2026. Forecasts are forecasts; the floor under them is that nobody credible is projecting a return to 3%+ this year.

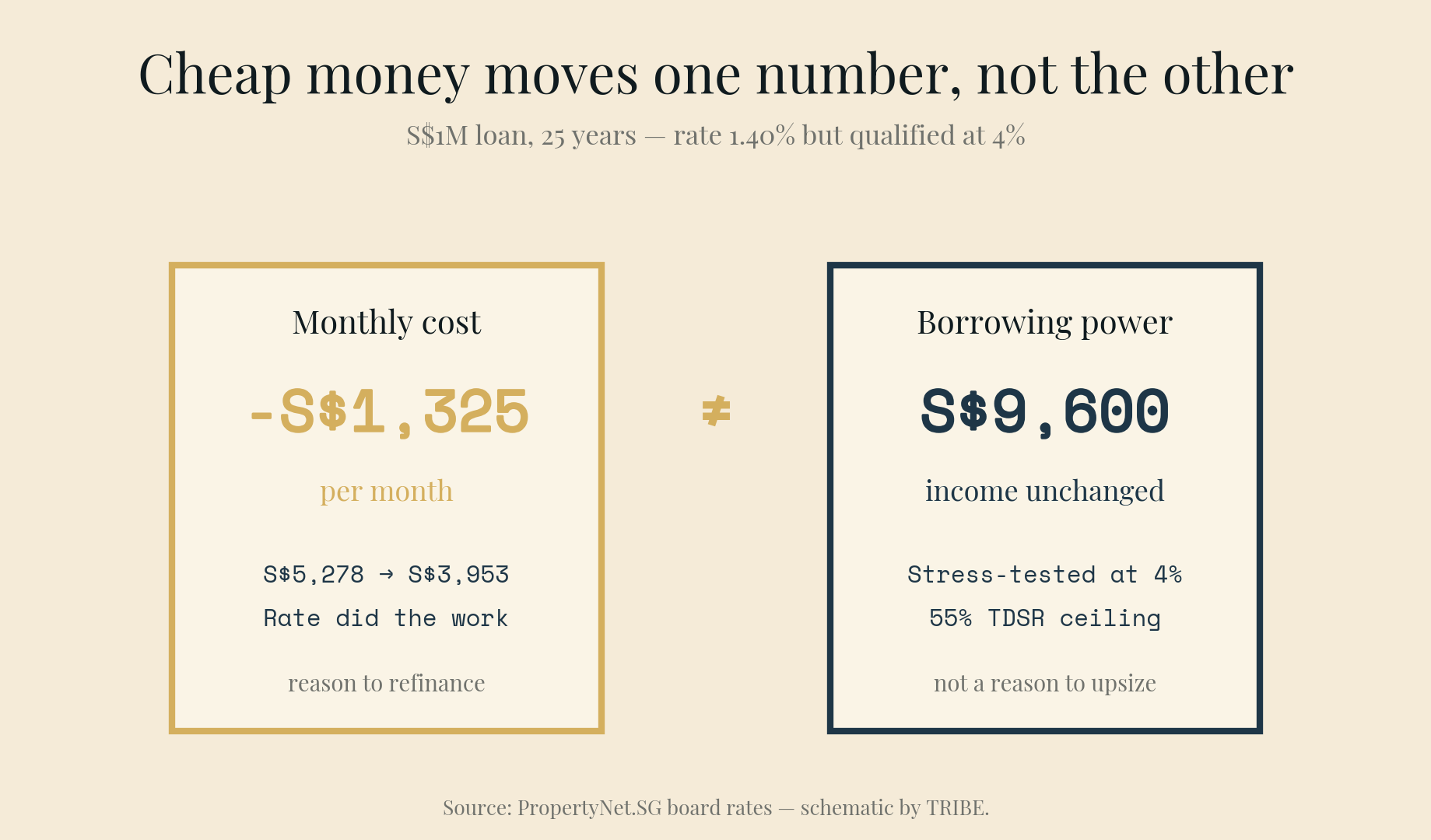

What halving the rate does to a $1M loan

Take a S$1 million loan over 25 years — a standard upgrader-sized mortgage. The monthly repayment:

- At 4.0% — roughly where fixed packages sat in the 2023–2024 cycle: S$5,278/month

- At 1.40% — today's best 2-year fixed: S$3,953/month

That's S$1,325 a month, every month. Framed as interest rather than payment: over just the first two years, the 4% loan charges about S$78,000 in interest; the 1.40% loan charges about S$27,000. Same property, same principal — a S$51,000 difference in pure cost, inside a single lock-in period.

This is why the refinancing queue is real. A household carrying S$800,000 at 3.5% from the last cycle pays about S$4,005/month over a 25-year tenure; the same loan rewritten at 1.27% costs about S$3,114 — roughly S$890/month freed up. Against typical legal-and-valuation fees of around S$1,800 (often bank-subsidised above S$500K), break-even arrives in the first months. The only genuine blockers are an unexpired lock-in (typically a 1.5% penalty) — and inertia.

The number that didn't move

Now the half everyone skips. Under MAS's Total Debt Servicing Ratio framework, banks don't assess your loan at the rate you'll actually pay. They stress-test it at a medium-term floor rate — 4% for residential loans — and your total debt repayments at that stressed rate must stay within 55% of gross income.

Run the S$1M loan through that filter. At the 4% stress rate the assessed repayment is S$5,278/month, which means you need roughly S$9,600/month in gross income to clear TDSR — whether your actual contracted rate is 1.40%, 1.27%, or anything else. The rate halved; the qualifying income required for the loan did not change by a single dollar.

This is deliberate, and it's worth defending rather than resenting. The stress test is the regulator assuming today's 1.07% SORA is the anomaly and 4% is the world you must survive. Anyone who took a floating loan at 0.2% SORA spreads in 2021 and lived through 3.7% in 2023 knows that assumption isn't theoretical — that round trip happened within one lock-in cycle.

The practical translation: cheap money is a reason to refinance, not a reason to upsize. Your maximum purchase is set by the 4% world; your monthly comfort is set by the 1.4% one. Buy in the first, enjoy the second.

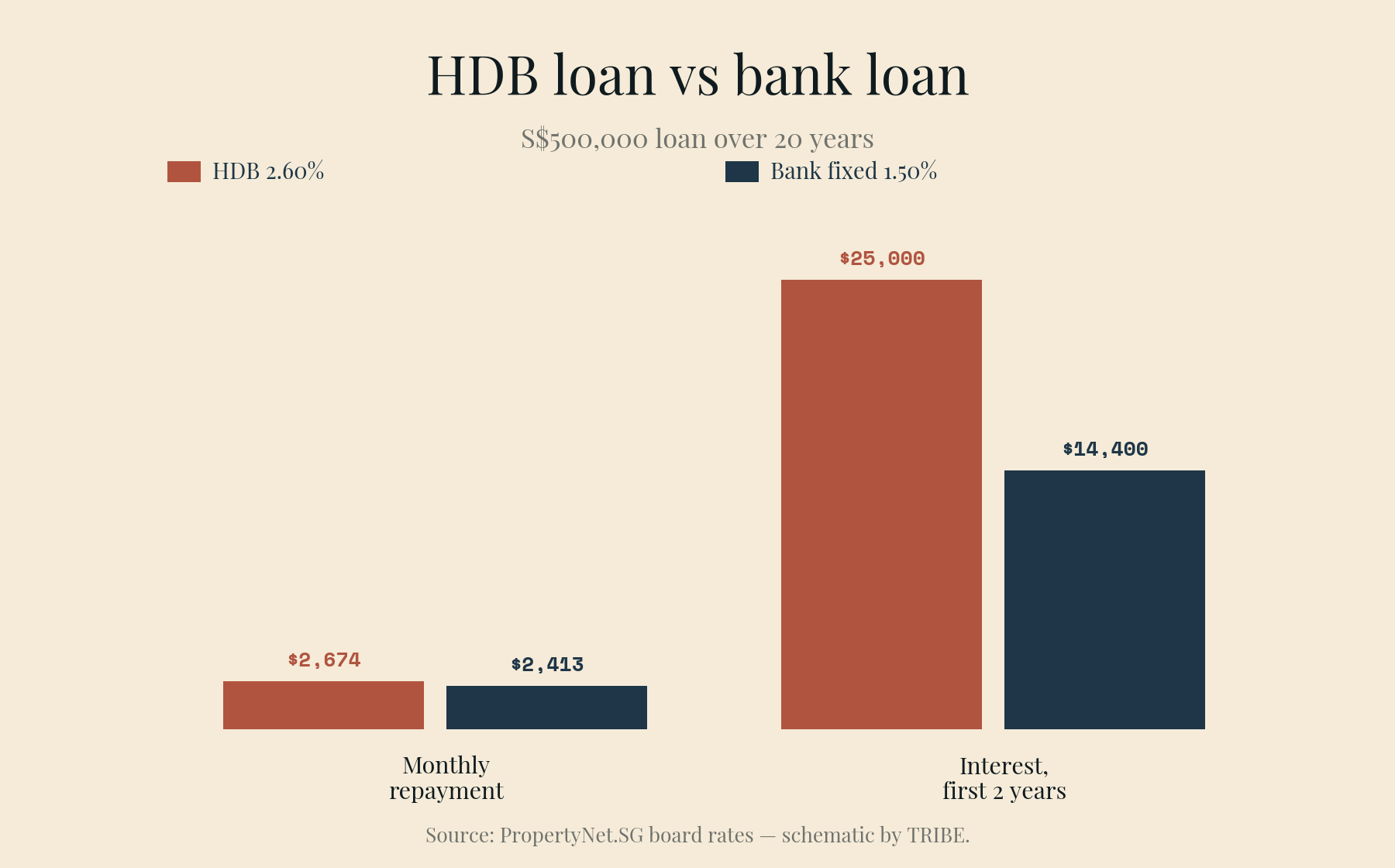

The HDB loan question, finally interesting again

For years the HDB concessionary loan at 2.60% versus a bank loan was a close call decided by temperament. At June 2026 pricing the gap is wide enough to put real numbers on. A S$500,000 loan over 20 years:

| HDB 2.60% | Bank fixed 1.50% | |

|---|---|---|

| Monthly repayment | S$2,674 | S$2,413 |

| Interest, first 2 years | ~S$25,000 | ~S$14,400 |

About S$260/month and S$10,600 of interest inside one two-year window. Floating at 1.32% widens it further.

The catch is structural, and it's a one-way door: you can refinance from HDB to bank, but never back. The HDB loan's value was never its rate — it's the option-rich terms: no penalty for early repayment in any amount, a downpayment that can be fully funded from CPF, and a historically more forbearing counterparty if your income hits trouble. Giving that up for ~S$130/month after-tax equivalent is a real trade, not a free lunch. Households with stable dual incomes and a buffer tend to take it; households whose income is lumpy or fragile often shouldn't, at any spread.

One more second-order effect of sub-2% money: CPF Ordinary Account balances earn 2.5%. For the first time in years, a private-property mortgage can cost less than what your OA earns. The default reflex — empty the OA into the property to shrink the loan — quietly stopped being free arbitrage. At 1.4% against 2.5%, every CPF dollar you don't sink into the mortgage is earning more than the loan costs, with none of the accrued-interest refund drag when you eventually sell. That logic flips back if rates rebound past 2.5%, so it's a thing to monitor, not a set-and-forget — but in June 2026 the math runs the unfamiliar direction.

What we'd actually do

If you're locked in above 3%: check your lock-in expiry today. Within six months of expiry, start the refinancing conversation now — repricing offers improve when the bank knows you can leave.

If you're choosing fixed versus floating on a new loan: the gap between 1.40% fixed and 1.27% floating is 13 basis points — about S$65/month on S$1M. You are being charged very little for two years of certainty at a near-cyclical-low rate. Unless you have a firm reason to expect SORA at the bottom of the forecast band (or plan to sell within the lock-in), paying 13bps for the floor is cheap insurance.

If low rates are tempting you to stretch the budget: re-read the stress-test section. The bank already refused to let the cheap money raise your ceiling. Let that discipline stand in your own planning too — buy the property that works at 4%, and bank the difference while it costs 1.4%.

General information only, not financial advice. Rates cited are indicative board rates for a S$1M loan as of early June 2026 and change without notice; actual pricing depends on loan size, property type, and borrower profile. TDSR, LTV, and CPF rules are set by MAS, HDB, and CPF Board and can change — verify current terms with your bank and the relevant agencies before committing.

Know what you can afford

Loan, stamp duty, CPF, and monthly repayments — work out your real budget before you commit. No registration required.

Plan my purchase →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.