Insights

June 2026 BTO: 6,900 Flats, Half of Them Plus or Prime. Should You Apply — or Buy Resale Instead?

Bishan's first new flats in 40 years, a second bite at Berlayar, and Ang Mo Kio by Mayflower MRT — at the price of a 10-year MOP, a clawback on the resale price, and a permanently restricted flat. We run the numbers.

By TRIBE Editorial · 12 June 2026 · 9 min read

The June 2026 BTO exercise puts about 6,900 flats across seven projects in five towns on the table: Ang Mo Kio, Bishan, Bukit Merah, Sembawang, and Woodlands. The headline is location — Bishan's first new flats in the Lakeview area in over four decades, and a second 1,960-unit launch on the former Keppel Club site at Berlayar. The fine print is classification: roughly half the supply is projected to fall under Plus or Prime, which means a 10-year MOP, a subsidy clawback on the eventual resale price, and a flat you can never rent out whole.

That changes the apply-versus-resale question from "discount versus waiting time" into something closer to a 15-year contract. Here is what's on offer, what the tighter rules actually cost, and the math both ways.

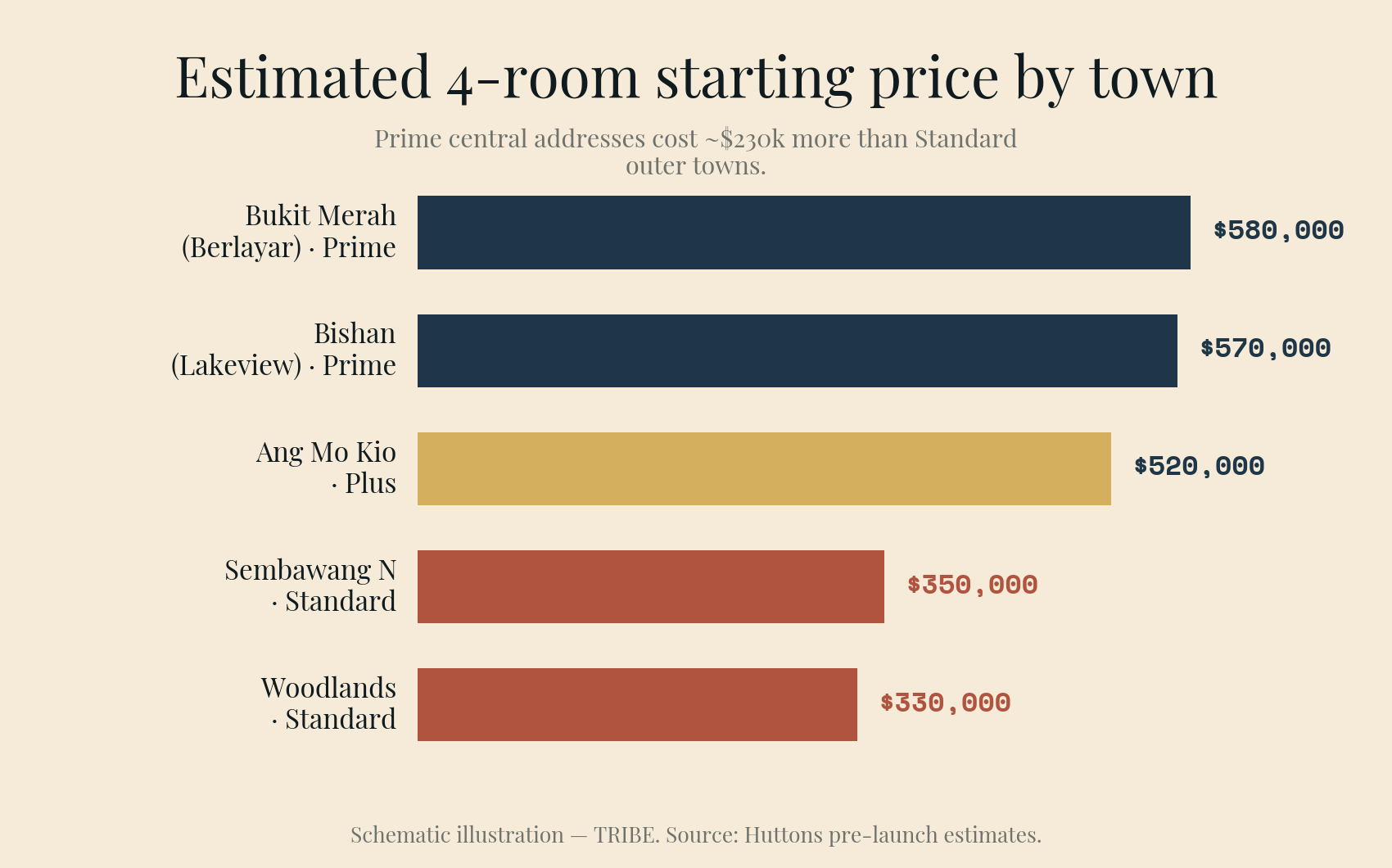

What's actually launching

From HDB's preliminary launch information and Huttons' pre-launch projections of classification and pricing:

| Town | Units | Flat types | Expected class | Est. 4-room from |

|---|---|---|---|---|

| Bishan (Lakeview, Upper Thomson Rd) | 1,210 | 2R Flexi, 4R | Prime | ~$570,000 |

| Bukit Merah (Berlayar) | 1,960 | 2R Flexi, 3R, 4R | Prime | ~$580,000 |

| Ang Mo Kio (Ave 1 & Ave 2, two projects) | 1,050 | 2R Flexi, 3R, 4R | Plus | ~$520,000 |

| Sembawang North (two projects) | 2,000 | 2R Flexi, 3R–5R, 3Gen | Standard | ~$350,000 |

| Woodlands (Woodgrove Ave) | 640 | 2R Flexi, 3R–5R | Standard | ~$330,000 |

Classifications and prices are confirmed only at launch; the figures above are estimates from Huttons' Lee Sze Teck, who projects about 47% of the exercise as Prime and 5% as Plus. HDB has confirmed that 2,520 flats carry wait times of around three years or less — concentrated in the Standard projects. Lakeview sits beside Marymount MRT with MacRitchie views; Berlayar is near Telok Blangah MRT on the Greater Southern Waterfront; the two Ang Mo Kio sites flank Mayflower MRT, with CHIJ St Nicholas Girls' within 1km of the Avenue 2 site. Huttons expects 3–4 first-timer applicants per AMK unit, 2–3 at Lakeview, 1–2 at Berlayar.

One procedural note: applying requires a valid HFE letter, with documents due by 15 May. Missed the window? This read applies equally to October's ~8,000-flat exercise — the framework doesn't change.

What Plus and Prime actually cost you

Under the classification framework in force since October 2024, Plus and Prime flats get extra subsidies upfront in exchange for tighter conditions for as long as you own the flat:

| Standard | Plus | Prime | |

|---|---|---|---|

| MOP | 5 years | 10 years | 10 years |

| Rent out whole flat after MOP | Allowed | Never | Never |

| Subsidy recovery on resale | None | Yes (lower) | Yes (highest) |

| Resale buyer pool | Open | Restricted | Most restricted |

Three of these deserve translation from policy language into money.

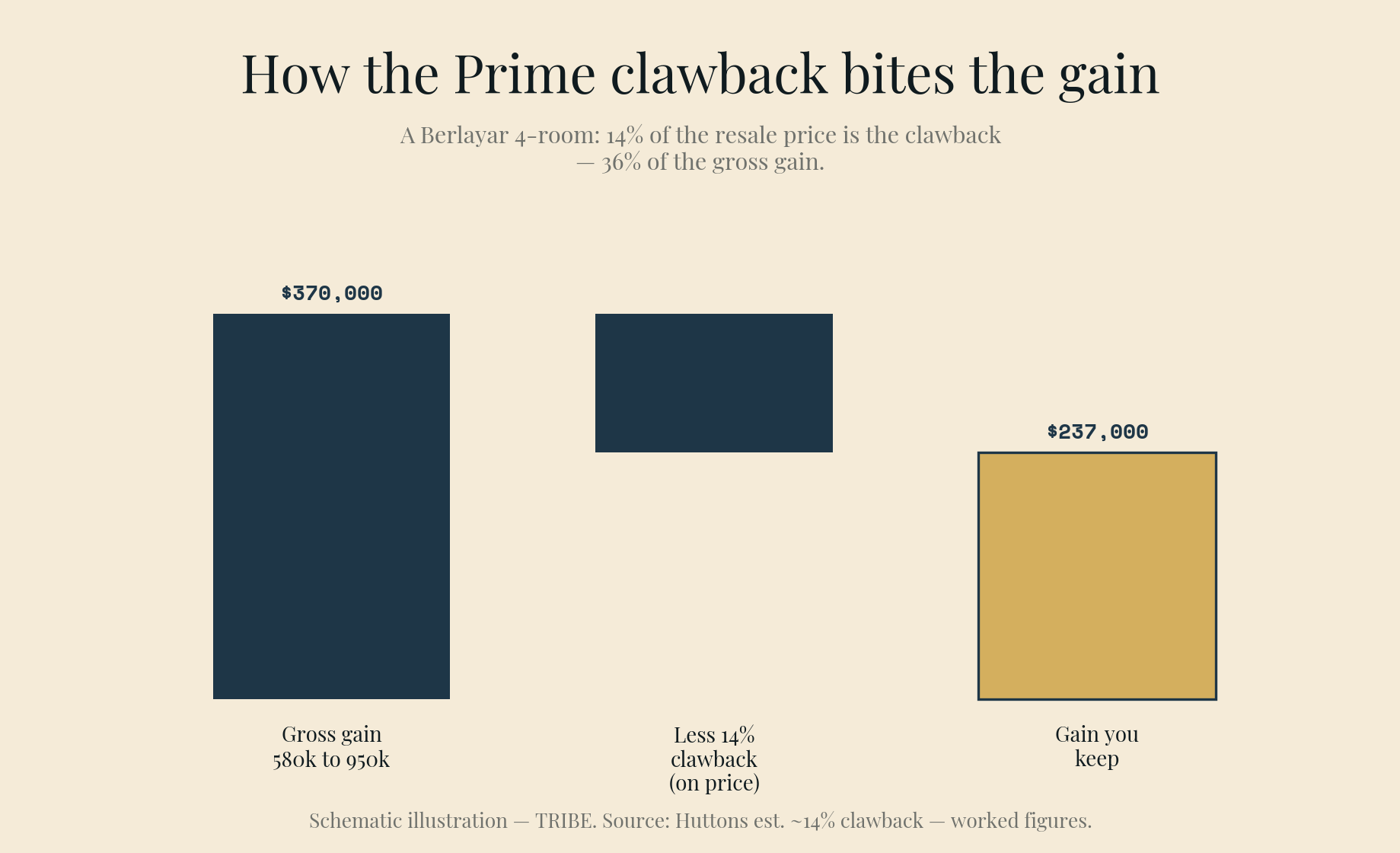

The clawback is on the resale price, not your profit. When a Plus or Prime owner sells, HDB recovers a fixed percentage of the full resale price. The rate is set at launch: the first batch in October 2024 was 9% for Prime and 6–8% for Plus; more recent Prime projects have been steeper — 12% at Mount Pleasant Crest and 14% at the first Berlayar launch, and Huttons expects similar rates for this exercise (~12% Lakeview, ~14% Berlayar). Because the percentage applies to price rather than gain, it bites hardest when appreciation is modest. A Berlayar 4-room bought at $580,000 and sold at $950,000 pays a $133,000 clawback — 36% of the $370,000 gross gain. The same flat sold at $750,000 pays $105,000 — 62% of the gain. The clawback never puts you underwater on its own, but it compresses the upside asymmetrically.

Your future buyer pool is regulated. Resale buyers of Plus and Prime flats must meet prevailing BTO conditions: a $14,000 household income ceiling, a 30-month wait-out for private property owners, and singles limited to 2-room Flexi units for Prime resale (any size except 3Gen for Plus). Today's unclassified resale flats face none of these. When the first classified flats hit the market in the late 2030s, they will compete against unrestricted older stock — newer and better located, but sellable to fewer people.

The rental option is gone, permanently. A Standard or unclassified flat can be rented out whole after MOP — the classic upgrader bridge. Plus and Prime owners may only ever rent out bedrooms. If your ten-year plan includes "keep the flat, rent it, move on," these flats structurally cannot do that.

Add the timeline: apply this month, collect keys around 2030–31, finish the 10-year MOP around 2040–41. That is a roughly 15-year commitment from today before the flat is sellable.

The Bishan test case, worked

The cleanest live comparison this launch offers: a Lakeview 4-room at the estimated starting price, against an actual June 2026 resale transaction one street away — a 95 sqm 4-room on Shunfu Road, sold this month for $768,000 with about 57.5 years of lease remaining (data.gov.sg). Both rows computed on an HDB loan at 2.6%, 75% LTV, 25 years:

| Lakeview BTO (Prime, est.) | Shunfu Rd resale (actual) | |

|---|---|---|

| Price | $570,000 | $768,000 |

| Lease | Fresh 99 years | ~57.5 years left |

| Downpayment (25%, CPF/cash) | $142,500 | $192,000 |

| Buyer's stamp duty | $11,700 | $17,640 |

| Loan / monthly repayment | $427,500 / $1,939 | $576,000 / $2,613 |

| Move in | ~2030–31 | ~3 months |

| Sellable from | ~2040–41 | 2031 |

| Future sale | ~12% of price to HDB, buyers capped at $14k income | No clawback, open buyer pool |

The headline gap is $198,000, or 25.8% — and the BTO buys 41 more years of lease. But the gap is narrower than it looks: first-timers buying resale get the $80,000 CPF Family Grant that BTO buyers don't (EHG applies to both sides equally; the Proximity Housing Grant of up to $30,000 can narrow it further). Grant-adjusted, the discount is about $118,000 — roughly 17%. In exchange for that 17%, the BTO buyer accepts five years of waiting, five extra years of MOP, the 12%-of-price clawback, the restricted future buyer pool, and no whole-flat rental, ever. The resale buyer pays $674 more a month and inherits a lease that will read "42 years remaining" when a 2050s buyer comes looking — the lease-decay risk is real and priced in both directions.

At Berlayar the same logic runs against Bukit Merah's resale stock, where 4-room prices have pushed to a $1.36 million record on Boon Tiong Road — the implied discount on a ~$580,000 BTO is larger, and so is the 14% clawback when you exit.

So: apply or buy resale?

Apply for the Plus/Prime projects if you are buying one home to live in for 15+ years, your household clears the eligibility bar but values the central location more than flexibility, and the entry price — not the exit price — is what's binding. On those terms, Lakeview and Berlayar are among the cheapest ways a $14k-and-under household will ever access these addresses, and the clawback only ever takes a slice of a sale you may never make.

Apply Standard (Sembawang, Woodlands) if you want the BTO discount with the old rules: 5-year MOP, no clawback, whole-flat rental after MOP, open resale. At ~$350,000 for a 4-room with sub-one application rates expected and ~3-year waits, this is the quietly rational corner of the launch.

Buy resale if you need the flat before 2030, your income is above $14,000 (you have no BTO route anyway), your plan involves renting out the flat or upgrading on a 5–7 year clock, or you're a single who wants more than a 2-room in a central area. You pay more per month — $2,613 versus $1,939 in our Bishan case — but every exit door stays open, five years sooner.

The honest summary: HDB has priced these Plus/Prime flats as homes, not assets, and the rules enforce it. Applicants who read the 25.8% discount as pure arbitrage are mispricing a 15-year lock-in with a regulated exit. Applicants who actually want to live in Bishan or on the Greater Southern Waterfront for two decades are being offered a genuinely subsidised way in. Know which one you are before the ballot, not after.

Worked figures computed on stated assumptions: HDB concessionary loan at 2.6%, 75% LTV, 25-year tenure; indicative BTO prices are Huttons Asia pre-launch estimates and grants are excluded except where stated; actual prices, classifications, and subsidy recovery rates are confirmed by HDB at launch. Resale comparator is an actual June 2026 transaction from data.gov.sg. This article is general information, not financial advice. Methodology published. No spin.

Know what you can afford

Loan, stamp duty, CPF, and monthly repayments — work out your real budget before you commit. No registration required.

Plan my purchase →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.