Insights

Jessie and Joel Earn $18k a Month. The Bank Will Lend Them $1.87M. Here's Why They Shouldn't Take It.

A couple in their thirties, two kids, a Sengkang four-room past its MOP, and a combined $18,000 income. Every upgrader maths question in one household — the sale proceeds, the loan the bank approves, and the smaller number they should actually spend.

By TRIBE Editorial · 11 June 2026 · 7 min read

Jessie is 33, Joel is 38. Two kids, six and three. A four-room in Sengkang bought at BTO, now past its MOP, and a combined gross income of $18,000 a month. They've decided to upgrade to a private condo, and they're carrying the three questions every upgrader carries: what does our flat actually give us, what will the bank let us do, and what should we do.

Jessie and Joel aren't real clients — they're a composite of the profile we see most often. But every number below is computed, not vibes, and you can re-run all of it on your own figures.

Step one: what the flat actually frees up

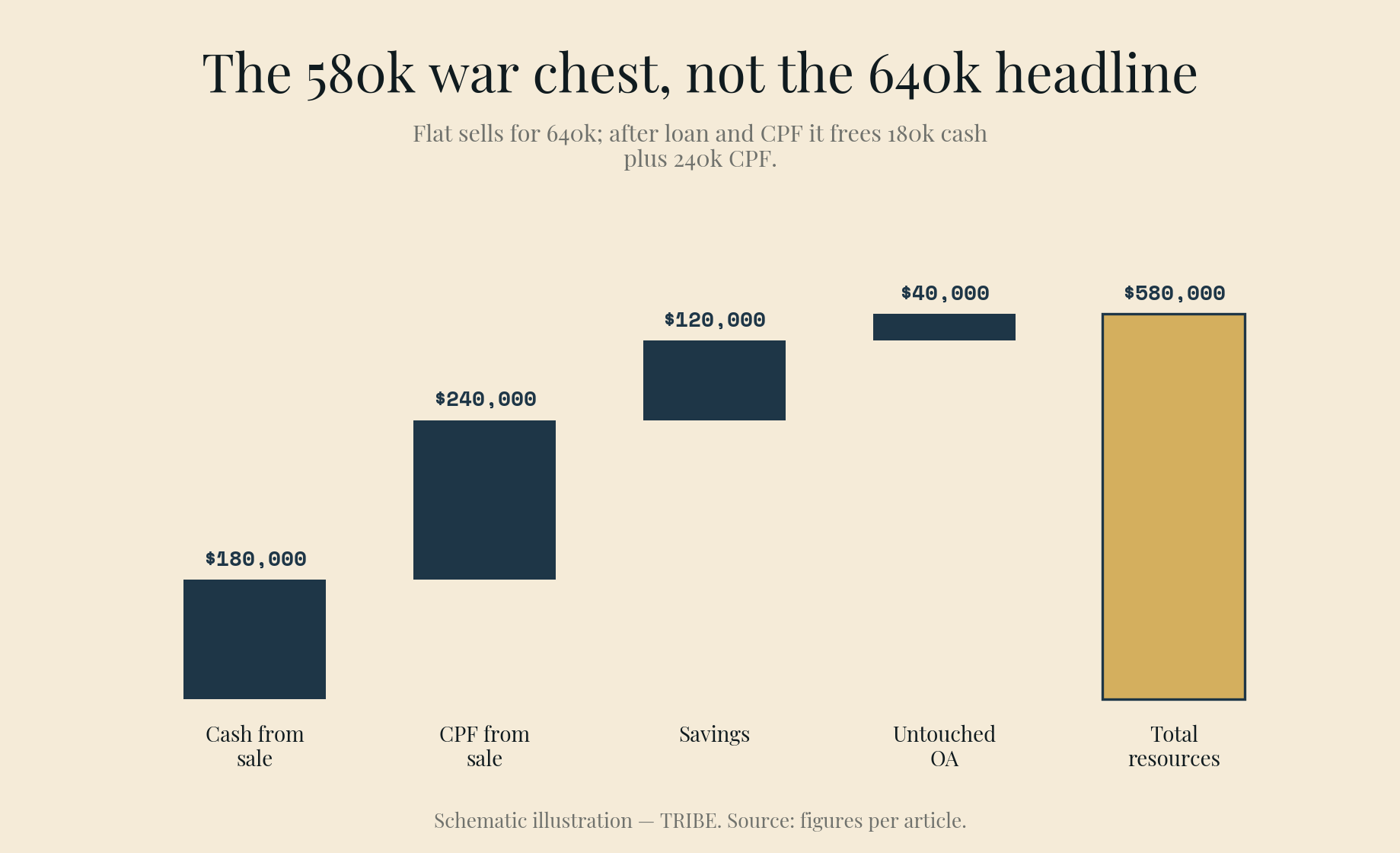

Say the flat sells for $640,000 — a realistic figure for a high-floor Sengkang four-room in 2026. That is not the number they get to spend.

| The sale | Amount |

|---|---|

| Sale price | $640,000 |

| Less: outstanding HDB loan | −$220,000 |

| Less: CPF used + accrued interest (both, combined) | −$240,000 |

| Cash in hand from sale | $180,000 |

The $240,000 isn't lost — it goes back into their CPF Ordinary Accounts and can fund the next downpayment. But the split matters: the sale gives them $180,000 of cash and $240,000 of CPF. Add their savings ($120,000) and the OA balances they hadn't touched ($40,000), and the war chest is:

$300,000 cash + $280,000 CPF = $580,000.

That number — not the $640,000 headline — is what the whole upgrade gets built on.

Step two: what the bank says (a dangerously large number)

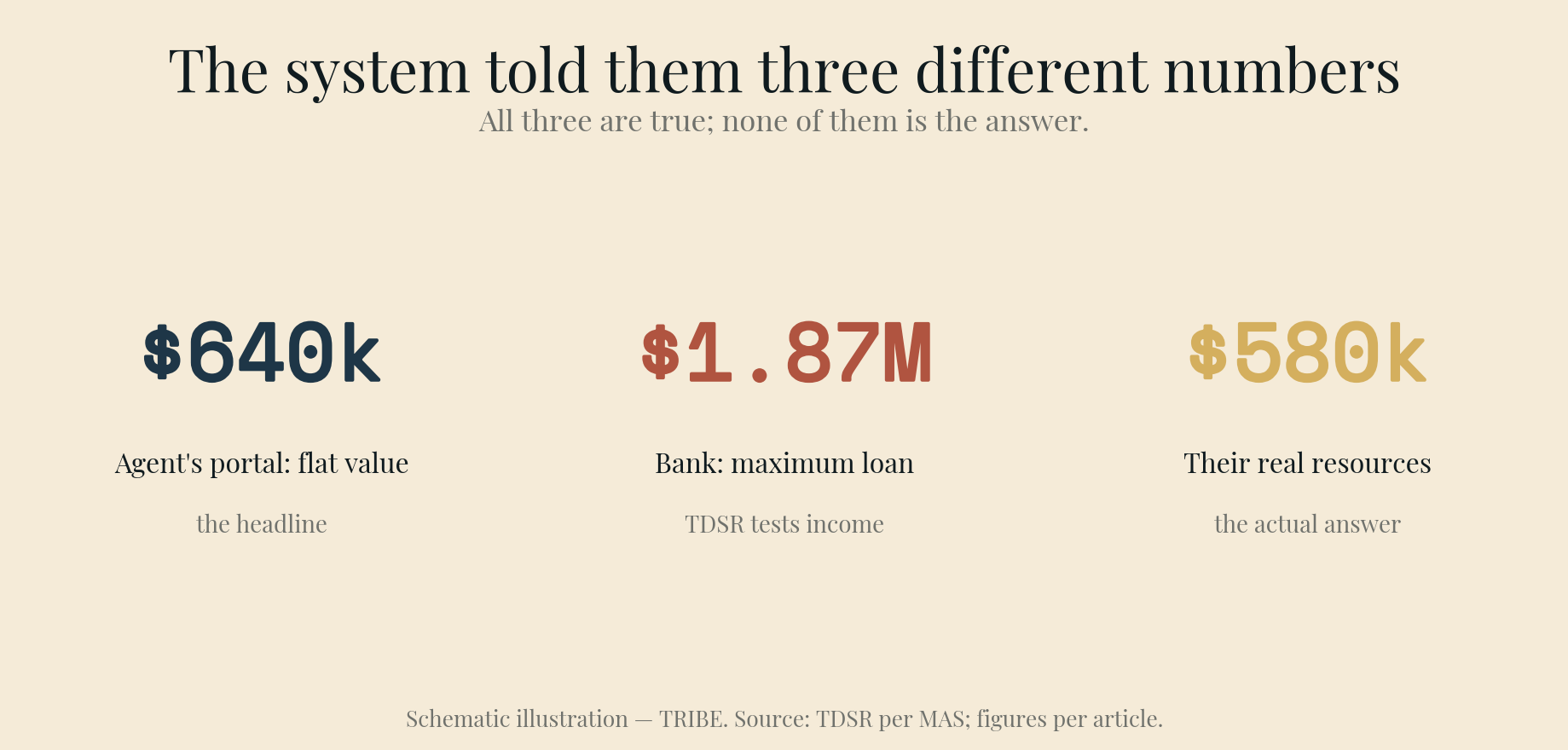

Under TDSR, the bank stress-tests the new loan at 4% and caps total debt repayments at 55% of gross income. On $18,000 a month, that's a $9,900 ceiling — which works out to a maximum loan of roughly $1.87 million over 25 years.

Read that again. A couple with $580,000 to their name can be approved for close to two million dollars of debt — because TDSR tests income, not resilience. At today's 1.40% two-year fixed rates, the monthly repayment on a big loan looks deceptively gentle. The approval is real. The wisdom of using all of it is a separate question, and it's the one this article is actually about.

(One technical note: their income-weighted average age is about 36, so a 25-year tenure keeps them inside full 75% LTV territory with the loan ending before 65. Stretching tenure further is possible but starts trading LTV away.)

Step three: the constraint nobody at the showflat mentions

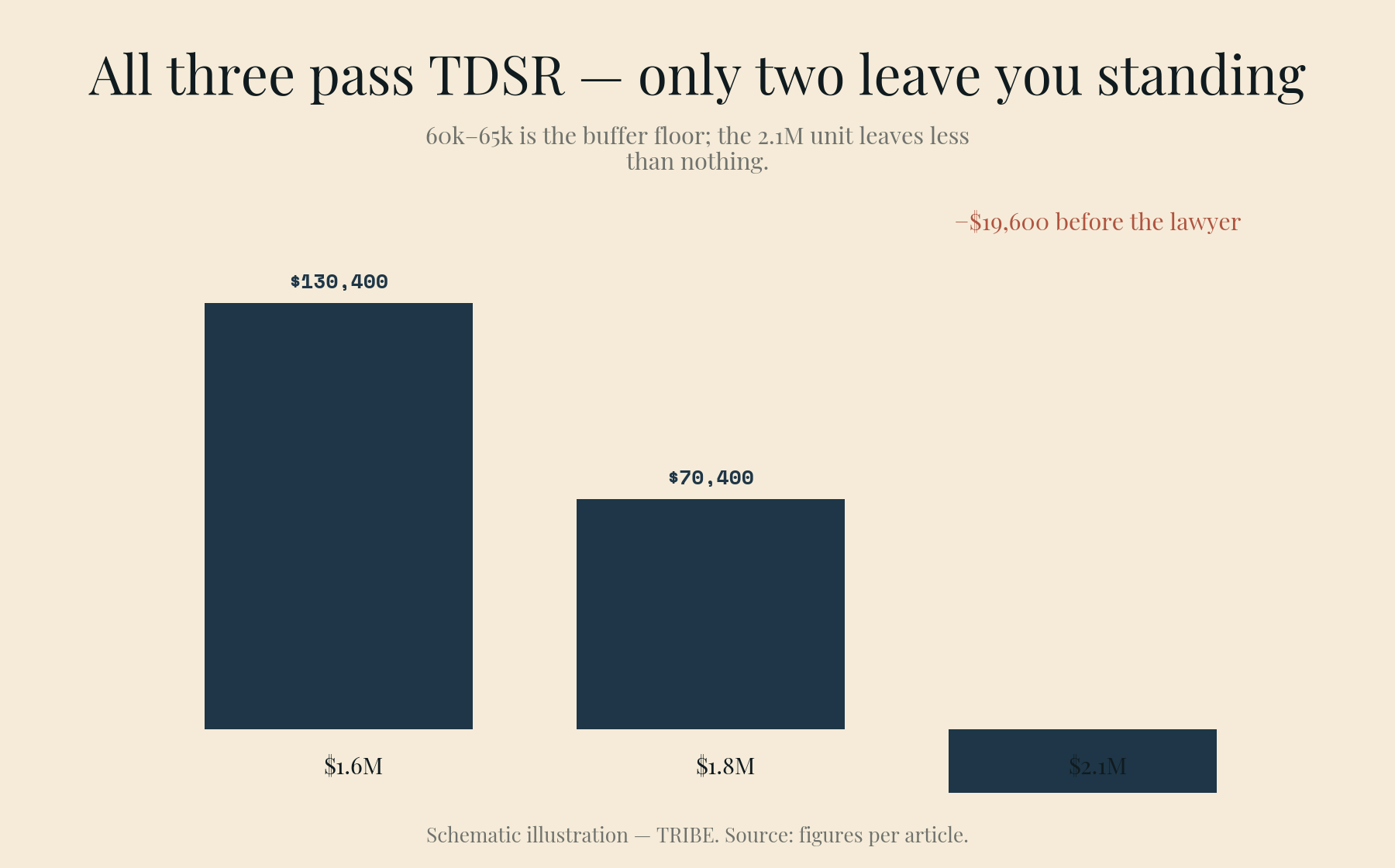

The real ceiling isn't the loan. It's the cash and CPF needed upfront — 25% down plus Buyer's Stamp Duty — and what's left in the tank afterwards. Run their $580,000 against three price points:

| $1.6M condo | $1.8M condo | $2.1M condo | |

|---|---|---|---|

| Downpayment (25%) | $400,000 | $450,000 | $525,000 |

| BSD | $49,600 | $59,600 | $74,600 |

| Upfront total | $449,600 | $509,600 | $599,600 |

| Left over after buying | $130,400 | $70,400 | −$19,600 |

| Loan (75%) | $1,200,000 | $1,350,000 | $1,575,000 |

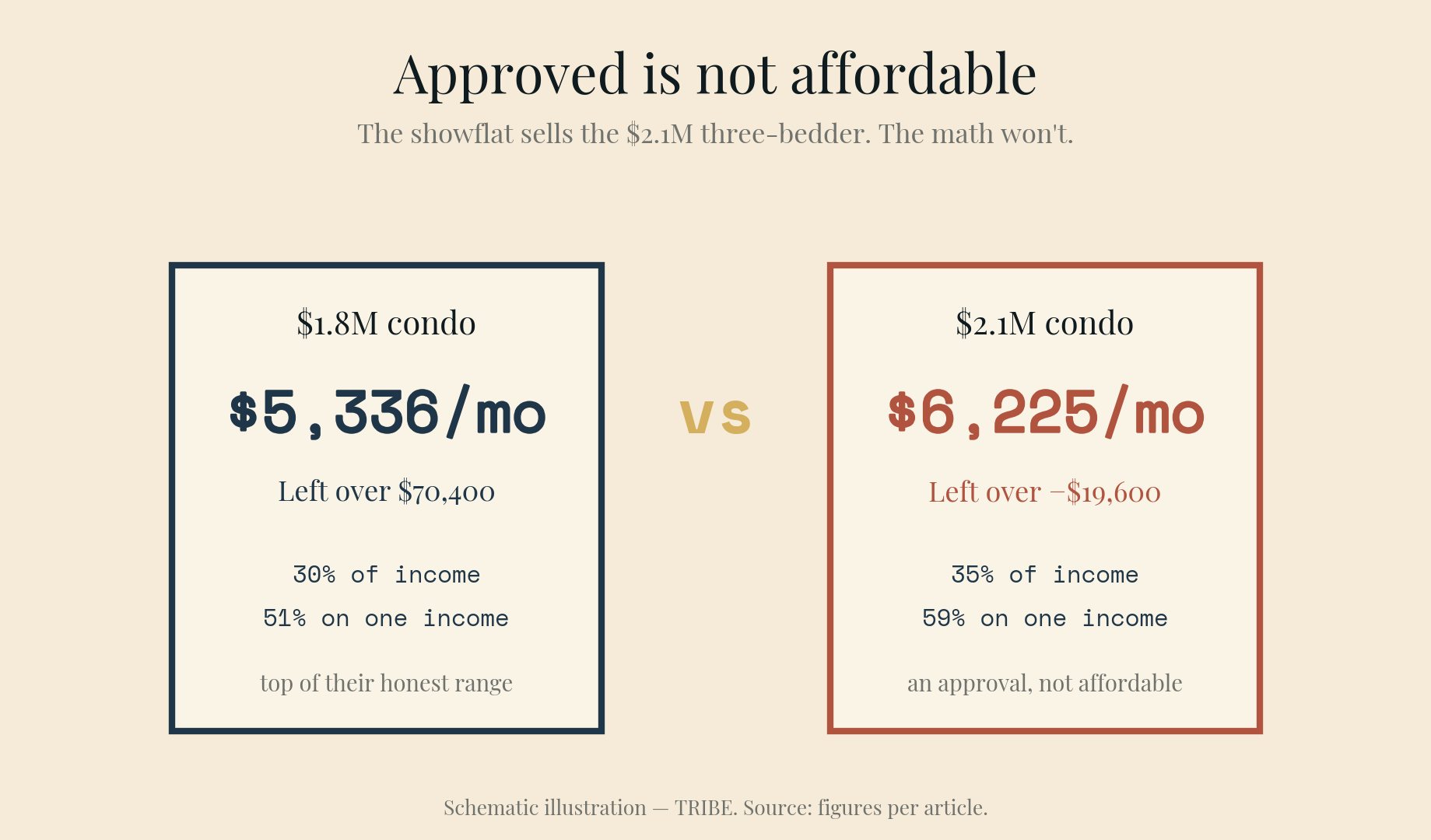

| Monthly at 1.40% | $4,743 | $5,336 | $6,225 |

| As % of $18k income | 26% | 30% | 35% |

| TDSR at 4% stress | 35% ✓ | 40% ✓ | 46% ✓ |

Look at the bottom row first: all three pass TDSR. The bank will approve every one of these purchases, including the one that leaves Jessie and Joel nineteen thousand dollars short before they've paid a lawyer, a mover, or a renovation deposit.

Now look at the row that should drive the decision: what's left over.

The three tests that separate approved from affordable

The comfort test. A widely used rule of thumb keeps housing at or under 30% of gross income. At $1.6M they're at 26%; at $1.8M exactly 30%; at $2.1M they're past it. Today's 1.40% rates make big repayments look manageable — but fixed periods end, and the 4% stress test exists because rates round-tripped from under 1% to nearly 4% within a single lock-in cycle this decade.

The one-income test. Joel earns $10,500 of the $18,000. If Jessie stops working — retrenchment, a third child, a parent who needs care — the $1.6M repayment is 45% of his income alone: painful but survivable for a stretch. The $1.8M repayment is 51%. The $2.1M repayment is 59%, on top of zero reserves. A home that only works if nothing changes for 25 years is not a plan; it's a bet.

The buffer test. Twelve months of repayments plus condo maintenance fees is the floor we'd want liquid after completion — roughly $60,000–$65,000 at these price points. The $1.6M purchase leaves double that. The $1.8M purchase leaves just about exactly that. The $2.1M purchase leaves less than nothing.

Three tests, one verdict: their honest range is $1.6M to $1.8M — the lower end if they value slack, the upper end if both incomes are secure and they accept a thinner cushion. The $2.1M three-bedder the showflat will happily sell them is an approval, not an affordability.

What $1.6M–$1.8M should buy them

This is where the second half of the upgrade decision starts — the one that determines whether the condo holds its value, which we've argued before matters more than the timing everyone obsesses over.

With kids aged six and three, the schools factor is not abstract: P1 registration distance bands are a structural, decade-long driver of resale demand, which is why schools carry 20% of the RPS score. In their budget band, the OCR offers plenty of B-grade stock and a meaningful number of A and S grades — the spread between them is the difference between a flat decade and a compounding one. Score the shortlist before the viewing, not after.

On timing: their selling leg just got harder to procrastinate on. HDB resale prices stalled in Q1 2026 while OCR condo prices rose 2.2% — the gap they need to bridge is widening, and with 13,480 flats reaching MOP this year, waiting doesn't improve their flat's competitive position. Selling first also resets their ABSD count — no 20% outlay, no remission paperwork.

The bottom line

The system told Jessie and Joel three different numbers. The agent's portal said their flat is worth $640,000. The bank said they can borrow $1.87 million. The showflat said a $2.1M unit is "within reach." All three are technically true, and none of them is the answer.

The answer came from their own ledger: $580,000 of real resources, three stress tests, and a price band of $1.6M–$1.8M that survives a rate cycle, a single income, and a bad year. That's not a smaller ambition. It's the version of the upgrade they get to keep.

If your numbers rhyme with theirs but don't match — different flat, different income, different fears — the arithmetic is the same shape. Run your sale through the sale proceeds calculator, your duties through the stamp duty calculator, and your shortlist through RPS. Or bring us the inputs and we'll run the whole thing with you — before the showflat does its own version of this math, with very different incentives.

Jessie and Joel are an illustrative composite of a typical upgrader household, not real clients; their figures are stated assumptions. All computations (loan repayments, BSD, TDSR) are exact against the stated rules as of June 2026 — rates from the linked source, BSD per the prevailing residential tiers, TDSR per MAS's framework. General information only, not financial advice; verify current rules with IRAS, MAS, and your bank before committing.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.