Insights

The Upgrader's Real Risk Isn't the ABSD

Most HDB upgraders pour their energy into the tax timing. The harder question — the one that decides whether your private home holds its value — is one a dataset of more than 2,300 scored condos can answer.

By TRIBE Editorial · 2 June 2026 · 6 min read

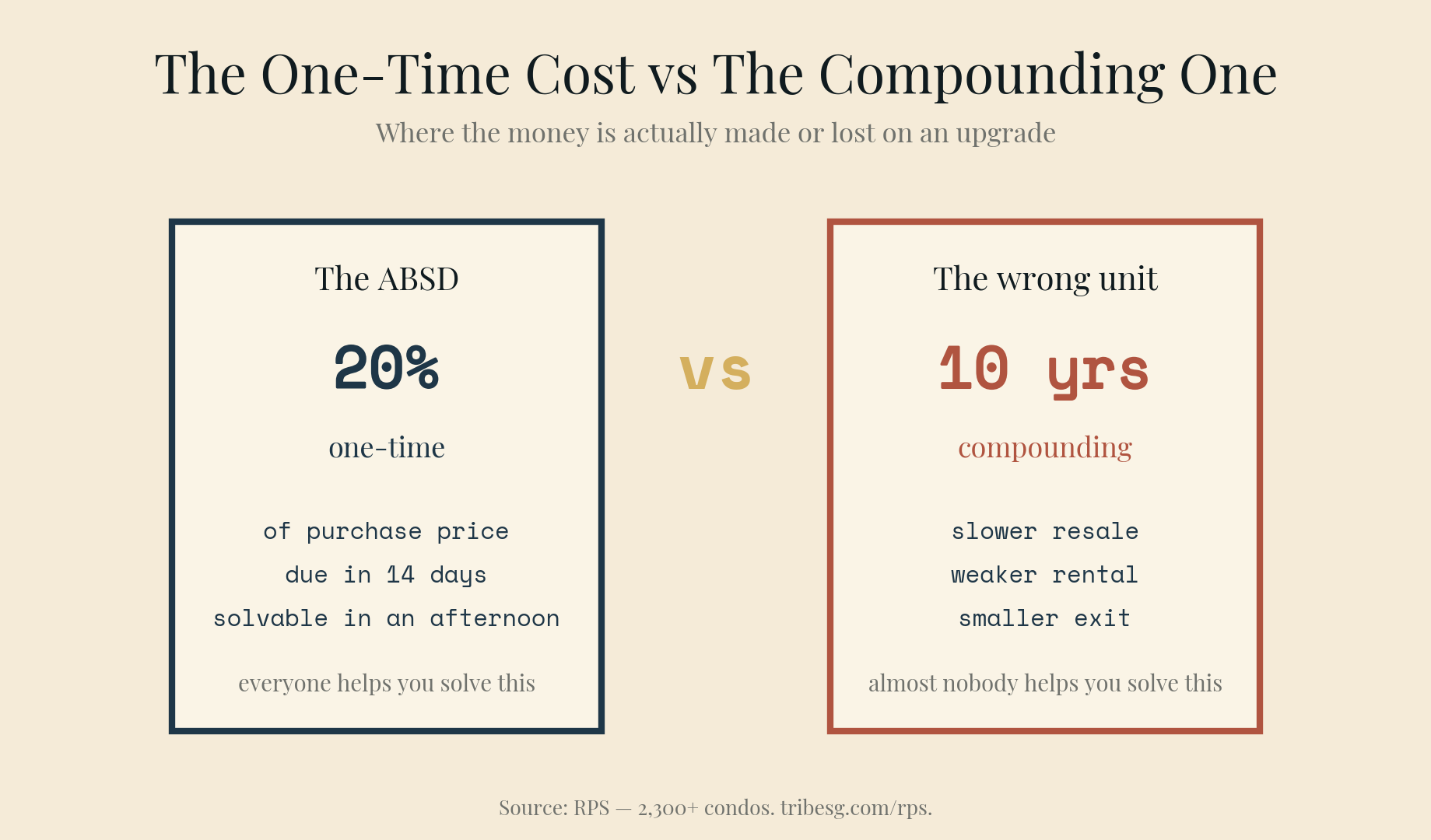

If you're sitting on a flat that's appreciated nicely and you're ready to move into private, you've probably already had the ABSD conversation. Sell first, or buy first and claim it back? It's a real decision with real money attached — 20% of the purchase price on a second property for a Singapore citizen, due within 14 days of exercising the Option to Purchase.

But here's the uncomfortable part. The ABSD is the problem everyone rushes to help you solve, because it's concrete, it's urgent, and it has a deadline. The problem almost nobody helps you solve is the one that compounds quietly for the next ten years: which unit you actually buy.

Two problems — and which one you're being sold

Every upgrade has two moving parts.

The first is timing, and it's a fork:

- Sell first. You're treated as a first-time buyer again, so no ABSD. The trade-off is a possible housing gap and the pressure of buying on the clock.

- Buy first. You pay the full 20% upfront and claim it back — provided you sell your existing home within six months of completing the new purchase, and meet IRAS' conditions. The trade-off is that you need the bridging cash to float that 20% in the meantime.

Both are solvable with a bit of planning. (Timelines and conditions are set by IRAS and have shifted before, so confirm the current rules before you commit.)

The second part is selection — and this is where the money is actually made or lost. The timing question costs you once. The selection question pays you, or bleeds you, every year you hold the asset. Yet it's the part most upgraders decide on a Sunday afternoon, standing in a showflat, reacting to a render and a launch-day countdown.

What the data actually rewards

We built RPS to take the emotion out of that second problem — scoring every condo in the resale market on the factors that genuinely drive long-term value, using URA transaction data rather than vibes.

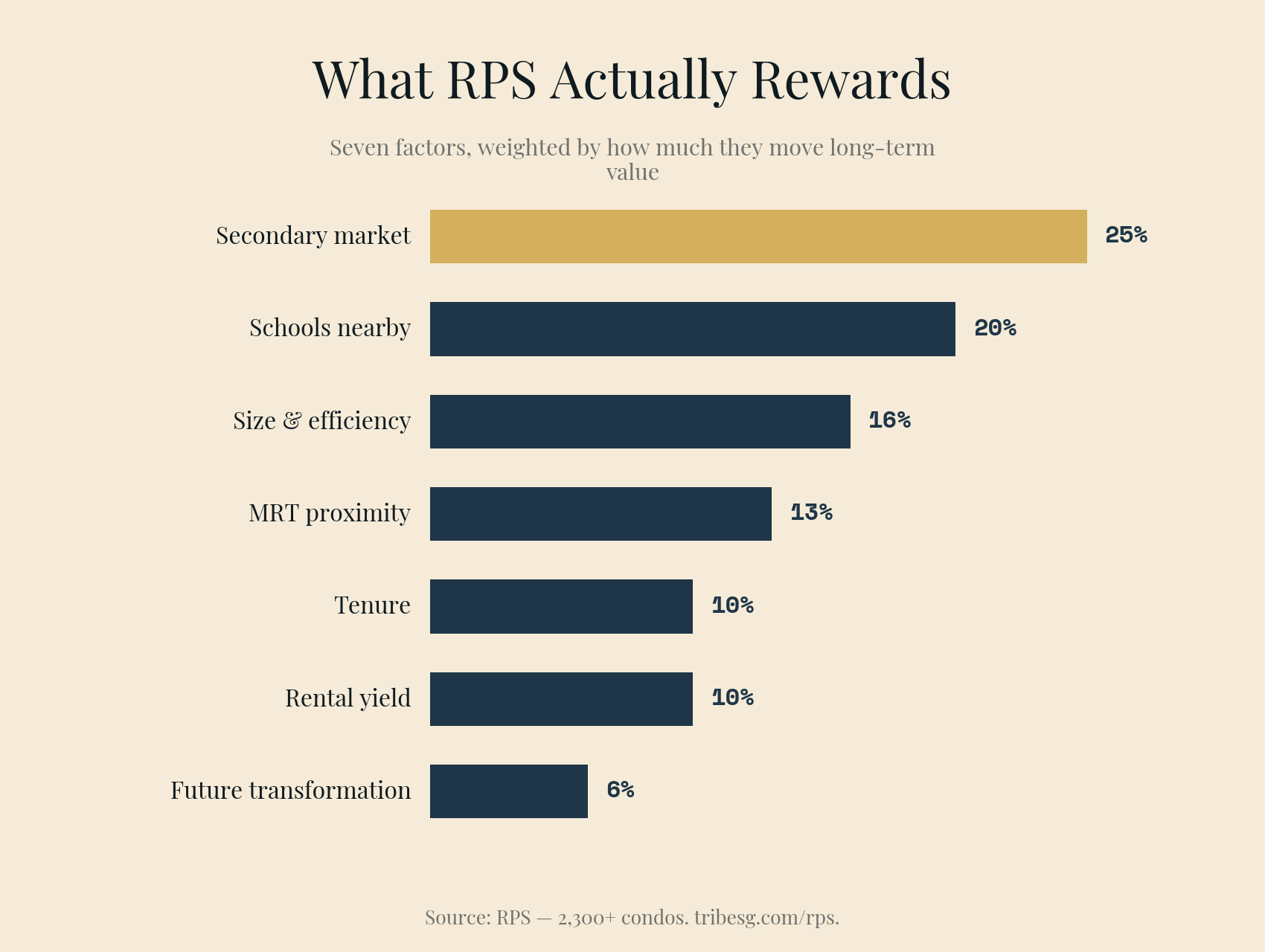

Seven factors, weighted by how much they move outcomes:

- Secondary market strength — 25%

- Schools nearby — 20%

- Unit size and efficiency — 16%

- MRT proximity — 13%

- Tenure — 10%

- Rental yield — 10%

- Future transformation (Master Plan upside) — 6%

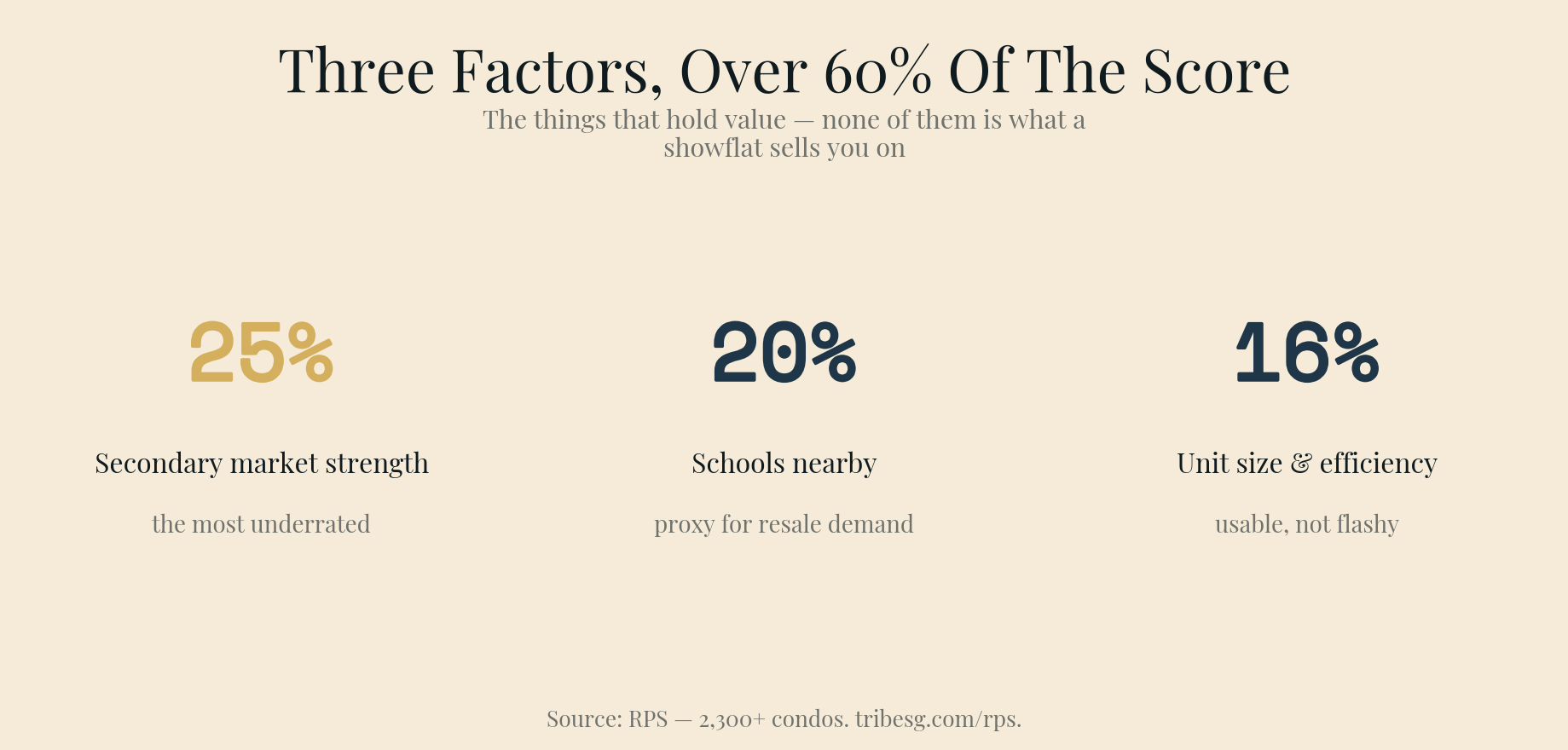

Look at the top three. Resale-market liquidity, schools, and size together make up more than 60% of the score — and not one of them is what a showflat is built to sell you on. Showflats sell finishes, facilities, and the fear of missing the launch. The data says the things that hold value are duller and more durable: can people buy this from you, do families want to live here, and is the space actually usable.

That heaviest weight — secondary market strength at 25% — is the one upgraders underrate the most. It's the answer to a simple question: in a soft market, who buys this unit from you, and how quickly? A home that only moves when sentiment is hot is a home you don't fully control. You control the one with a deep, steady pool of buyers underneath it.

The reality check most upgraders never see

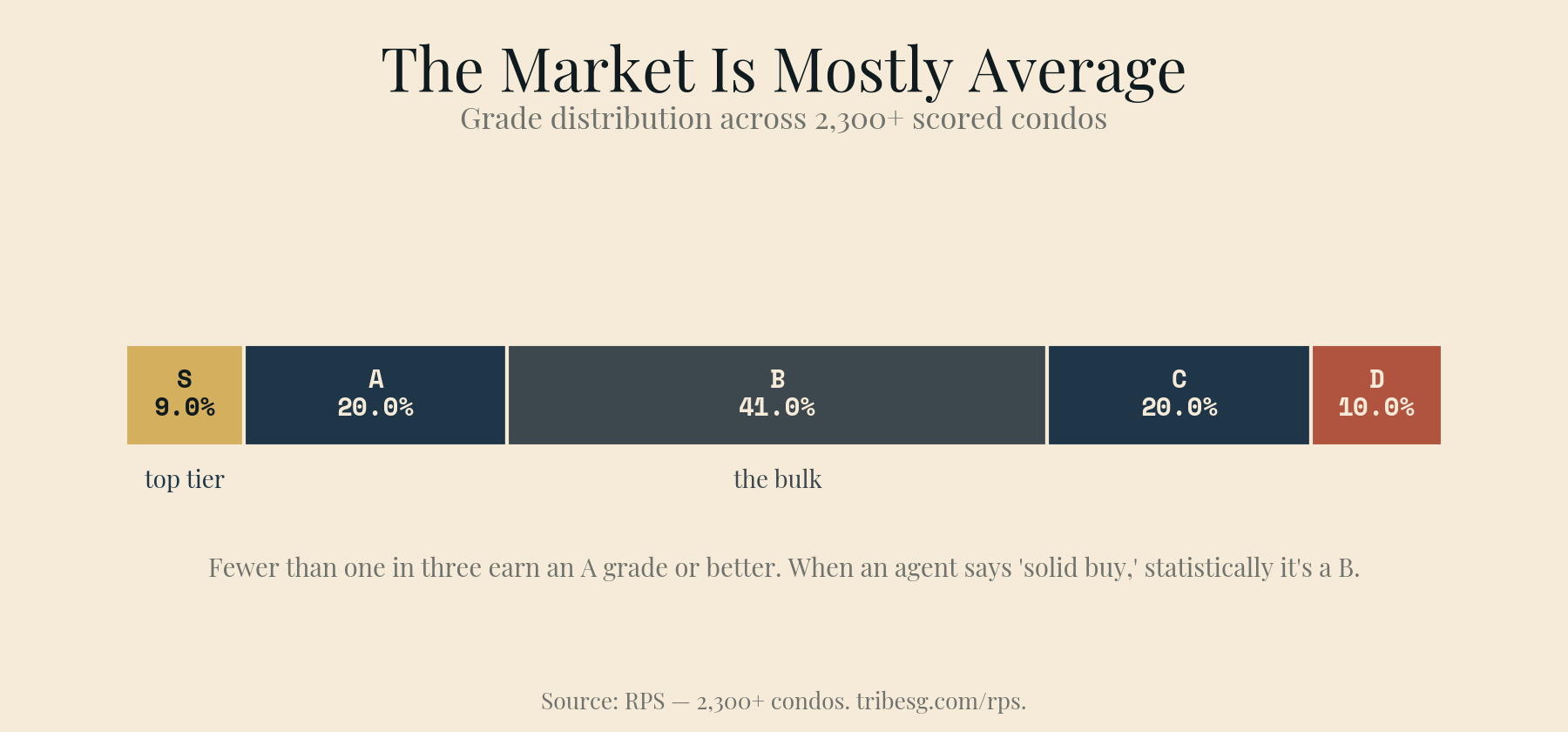

Across more than 2,300 condos, fewer than one in three earn an A grade or better. The bulk of the market — roughly four in ten — sits in the B band. Here's the rough shape:

- S — around 9% (the top tier)

- A — around 20%

- B — around 41% (the bulk of the market)

- C — around 20%

- D — around 10%

Read that honestly and it reframes the whole search. When an agent calls a unit "a solid buy," statistically it's most likely a B — average. That's not a knock; average can still be the right home at the right price. The danger is paying an aspirational price for a C dressed up in marble and mood lighting. Your job as an upgrader isn't to chase a unicorn S. It's to know exactly which band you're buying into, and refuse to pay a grade above what you're getting.

Three filters that survive the showflat

Turn the factor weights into questions you ask before you fall for the layout:

- Liquidity first. Who's my exit buyer, and how fast do they show up when the market turns? If you can't answer that, you don't understand the asset yet.

- Buy where families want to be — even if you don't have kids. Proximity to good schools is a proxy for durable resale demand. You're not buying it for your own child; you're buying it for the next buyer's.

- Don't pay a premium for a shrinking floor plate. New launches have steadily compressed unit sizes. An older, efficient layout can out-live a tight new one — and cost less per usable square foot.

And one honesty check on tenure. Upgraders tend to make one of two mistakes: overpaying for freehold they don't actually need, or waving away lease decay they should be pricing in. RPS scores freehold and 999-year at the top and steps the score down by decade of remaining lease — not because freehold always wins, but because the exit maths changes with every decade you have left. Pick your trade-off with your eyes open instead of inheriting a default.

From "can I afford it" to "will it hold"

For most families, the move from HDB to private is the biggest financial decision after the flat itself. The ABSD is a one-time cost you can plan around in an afternoon. The wrong asset is a cost that compounds silently for a decade — in slower resale, weaker rental, and a smaller exit when you eventually move again.

So solve the timing. Then spend your real energy on selection. That's the entire logic of scoring a condo before you view it, not after you've already fallen for it.

You can run any resale condo through RPS at tribesg.com/rps. And if you want a second pair of eyes on the selection problem — the one that actually decides how this move ages — that's exactly what we built the tool to help with. Talk to us before you sign the OTP, not after.

General information only, not financial or investment advice. ABSD rates, remission conditions, and sale timelines are set by IRAS and subject to change — verify current details against the IRAS website before making any commitment.

Know what you can afford

Loan, stamp duty, CPF, and monthly repayments — work out your real budget before you commit. No registration required.

Plan my purchase →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.