Insights

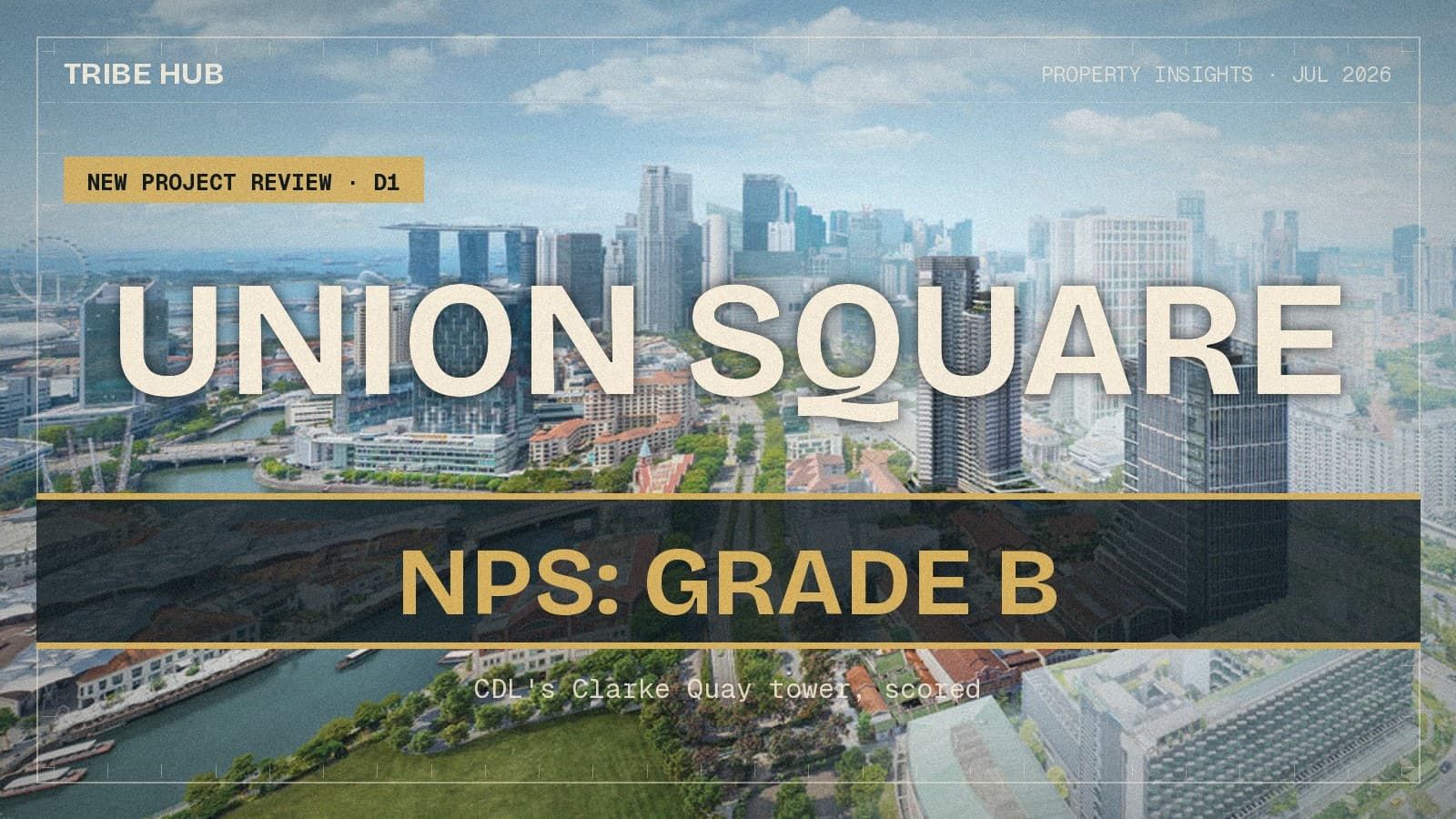

Honest Insights On Union Square Residences

Union Square Residences grades B (5.9) on the New Project Scorecard — City Developments' 366-unit, 99-year leasehold tower at Clarke Quay, District 1, where the ~3.2% projected growth is carried less by capital appreciation than by a central-core rental and location story.

By TRIBE Editorial · 18 July 2026 · 10 min read

Union Square Residences is a 366-unit, 99-year leasehold tower at 28 Havelock Road, in the Clarke Quay precinct of District 1, by City Developments Limited — a 40-storey block anchoring CDL's larger Union Square mixed-use redevelopment on the Singapore River, about a five-minute walk (0.49km) to Clarke Quay MRT on the North East Line. It grades a B (5.9) on our New Project Scorecard (NPS). The lease runs from October 2024, the project launched that November, and roughly 188 of the 366 units have transacted so far — so this is a live, still-marketing launch with real inventory left. This is a look at what the B rests on, where the remaining stock actually prices against the District 1 leasehold set, and why the honest read here is a yield-and-location hold rather than a capital-growth one. Methodology published. No spin.

The NPS grades a project's district-level fundamentals over a 10-year window — capital appreciation, rental growth, schools, MRT access and project size — from real URA transacted data. It is backward-looking by design: it reflects the district's history, lifted for the project's own size, transport and schools, not a forecast. Union Square Residences has its own transacted record now, so the fair-value basis below is the project's median transacted PSF by bedroom, not a launch guide.

The scorecard: what a B actually says

Union Square Residences' 5.9 is a central-location grade: strong on scale and transport, average on growth, and genuinely soft on rental momentum.

| NPS factor | Score /10 | What it reflects |

|---|---|---|

| Project Size | 8.0 | 366 units — a mid-to-large scale with a liquid resale pool |

| MRT Proximity | 7.0 | About a five-minute (0.49km) walk to Clarke Quay MRT (North East Line) |

| Capital Appreciation | 5.8 | 1km resale grew ~2.6%/yr over the decade; lifted for size and transport → ~3.2%/yr projected |

| School | 5.7 | One primary school within 1km — River Valley Primary (1.09km, oversubscribed) |

| Rental Growth | 2.0 | District 1 rents grew ~3.7%/yr over the decade — soft |

The strengths are real but ordinary for the core. The 366-unit scale scores 8.0 — deep enough for a full facilities deck and an active resale market — and transport scores 7.0, a genuine short walk to Clarke Quay MRT with the whole Downtown Core, Marina Bay and Orchard within a couple of stops. The address is about as central as Singapore gets.

The middle of the card is where the honesty lives. Capital appreciation scores 5.8: resale homes within a kilometre grew about 2.6% a year over the past decade — modest, and typical of the Core Central Region, where prime prices have lagged the mass market through this cycle. After the model's lift for the project's size and transport, projected growth runs to about 3.2% a year — over the 3% bar, but with almost no margin. Schools score 5.7, with only River Valley Primary inside the one-kilometre ring, and Primary 1 priority measured door-to-door, so a family counting on the ballot should confirm the distance on OneMap rather than trust a marketing sheet.

The clear soft spot is income growth. Rental growth is only 2.0 — District 1 rents grew about 3.7% a year over the decade, soft on the model's absolute scale. That said, the level of yield is respectable: gross rental yield here sits near 3.3%, better than most prime-district new stock, because the entry PSF, while high in absolute terms, buys a genuinely rentable central-core address. That distinction — soft rent growth, decent rent level — shapes the holding read below.

What's left, and what it's asking

Union Square Residences previewed with prices from about S$1.38 million (S$2,981 psf) for a one-bedroom and averaged near S$3,200 psf at its November 2024 launch, per EdgeProp. Roughly 20% sold on launch weekend and take-up passed 37% by early 2026 — so more than half the project is still available. The more useful benchmark for a buyer today is not the launch guide but the project's own transacted record: what the units have actually been changing hands at.

| Type | ~Median size | Median transacted PSF | Caveats |

|---|---|---|---|

| 1 Bedroom | 506 sqft | S$3,066 | 46 |

| 2 Bedroom | 732 sqft | S$3,119 | 86 |

| 3 Bedroom | 1,066 sqft | S$2,888 | 51 |

| 4 Bedroom | 1,518 sqft | S$3,370 | 5 |

The pattern is the compact-unit premium you see across the core: one- and two-bedders carry the highest PSF (S$3,066–3,119), the three-bedroom is the value stack at about S$2,888 psf, and the handful of four-bedders sit at the top on absolute quantum. Leftover stock is broadly pricing in line with this record — which means a buyer today is entering at, not below, what the early cohort already paid.

The benchmark: against adjusted District 1 leasehold

You cannot set a new launch's PSF against a resale comp's raw PSF. Two adjustments lift each comp to a like-for-like, as-new level: lease decay back to a fresh 99 years (via Bala's Table), and GFA harmonisation — a +6% (1–2BR) / +8% (3BR+) uplift for any comp whose planning permission predates 22 January 2023, because those older strata areas still count air-conditioner ledges and void space, understating their true PSF. Run against the nearest District 1 / River Valley leasehold set, on the calculator's as-new basis:

| Comparable | Tenure · what | Raw PSF | As-new adjusted |

|---|---|---|---|

| Martin Modern | 99-yr, TOP 2021, 0.84km | S$2,792 | S$3,093 |

| Martin Place Residences | Freehold, TOP 2011, 0.88km | S$2,768 | S$3,093 |

| One Pearl Bank | 99-yr, TOP 2024, 0.69km | S$2,497 | S$2,497 |

| The Landmark | 99-yr, TOP 2025, 0.48km | S$2,475 | S$2,475 |

| People's Park Complex | 99-yr, TOP 2002, 0.44km | S$1,251 | S$2,286 |

Against that set, Union Square Residences' two-bedroom at ~S$3,119 psf sits at the very top of the District 1 leasehold pack — level with an as-new Martin Modern and Martin Place, and a clear step above the newer One Pearl Bank (~S$2,497) and The Landmark (~S$2,475). Its three-bedroom at ~S$2,888 psf is more competitive, roughly mid-pack once the older comps are adjusted. The read is straightforward: the market is paying a premium for the newest, riverfront, integrated-precinct product — and a buyer is underwriting that premium up front. The compact stacks give away the least room to the resale field; the three-bedroom is where the relative value sits.

How long you'd likely hold

Seller's stamp duty runs for four years (16%, 12%, 8%, 4%), so no exit before year four is realistic, and the shortest tier we publish is four-to-six years. Using the NPS calculator's model — ~3.2% expected growth, a 3% target — here is the estimated holding period for each remaining stack, on price growth alone, entering at the project's own median transacted PSF.

| Available stack | PSF | Hold (price only) |

|---|---|---|

| 1 Bedroom · ~506 sqft | S$3,066 | 4–6 yrs |

| 2 Bedroom · ~732 sqft | S$3,119 | 4–6 yrs |

| 3 Bedroom · ~1,066 sqft | S$2,888 | 4–6 yrs |

| 4 Bedroom · ~1,518 sqft | S$3,370 | 4–6 yrs |

Every stack lands in the same four-to-six-year tier, but that uniformity hides a thin margin: modelled growth of ~3.2% clears the 3% bar by only about two-tenths of a point, so on price alone this is a slow, low-margin appreciation hold with little room for error if District 1 growth stays soft. What actually carries the case is yield, not growth — at a gross ~3.3%, the rent here is stronger than the price trend, which is the opposite of a Lentor or Turf City growth story. For an investor, the total-return math leans on the rental line; for an own-stay buyer, the value is the address and the connectivity, not a quick capital lift. Figures are gross of stamp duty, financing and selling costs.

The honest verdict

Union Square Residences is what a B looks like in the core: an unimpeachable location, a large and liquid project, a genuine short walk to the MRT — paired with the modest capital-appreciation record that has defined prime Singapore this cycle. The remaining stock prices at the top of the District 1 leasehold set, so a buyer is paying up front for the newest, riverfront, integrated product rather than buying a discount. The honest caveats are clear: projected growth of ~3.2% clears the 3% bar by a whisker, District 1 rent growth is soft, and the compact stacks give away the least to the adjusted resale field — the three-bedroom is where the relative value sits. Where this earns its keep is the ~3.3% gross yield and the central address: this is a rental-and-location hold for an investor who wants a prime-core tenant pool, or an own-stay buyer who values being a stroll from Clarke Quay, Marina Bay and Orchard — not a capital-growth play. Enter with that expectation and the B is credible.

See the full scorecard and run your own unit price through the holding-period calculator at tribesg.com/nps.

Sources: NPS quality grade (B, 5.9), the five factor scores, modelled growth (~3.2%/yr) and gross rental yield (~3.3%) per the TRIBE New Project Scorecard (URA Data Service transacted PSF; 1km resale trend lifted for project size, transport and schools; figures as at July 2026). Median transacted PSF by bedroom (1BR ~S$3,066 across 46 caveats; 2BR ~S$3,119 across 86; 3BR ~S$2,888 across 51; 4BR ~S$3,370 across 5) from URA caveats via the NPS dataset. Project facts — 366 units, 99-year lease with effect from 11 October 2024, 28 Havelock Road, TOP expected 2028, part of CDL's Union Square mixed-use redevelopment — and launch details (previewed from S$1.38m / S$2,981 psf for a 1BR; ~S$3,200 psf launch average; ~20% sold on launch weekend in November 2024; over 37% sold by February 2026) per EdgeProp and CDL developer materials. Comparable projects (Martin Modern, Martin Place Residences, One Pearl Bank, The Landmark, People's Park Complex): recent transacted PSF from URA caveats, lifted to an as-new basis via Bala's Table (fresh-99-year lease) and GFA-harmonisation uplift of +6% (1–2BR) / +8% (3BR+) per the NPS calculator's published methodology. Primary 1 priority distance is measured door-to-door, so confirm any 1km claim on OneMap before relying on it. Scores and holding periods are model outputs, not financial advice.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the New Project Scorecard (NPS) and Resale Project Scorecard (RPS) on URA transacted data. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.