Insights

Decoupling Isn't an ABSD Trick. It's a Financing Decision.

Decoupling saves a Singapore Citizen the 20% ABSD on a second home — easy arithmetic. The two numbers that actually decide whether it works sit on the financing side, and almost nobody runs them: how much CPF the exiting owner must refund, and whether the one who stays can carry the whole loan alone.

By Silas Tan · 3 June 2026 · 8 min read

Most couples arrive at decoupling with a single number in their head: the 20% ABSD they'll avoid on the next property. On a $1.5M second home that's roughly $300,000 saved, against $40,000 to $50,000 to decouple. The decision looks settled before the conversation even starts.

It isn't. The ABSD saving is the easy part — it's arithmetic, and it's real. But the two numbers that actually decide whether decoupling works sit on the financing side, and almost nobody runs them before they commit: how much CPF the exiting owner has to refund, and whether the remaining owner can carry the entire loan on one income. Get either wrong and a "$250,000 saving" quietly becomes a cash crunch, or a loan the bank simply won't approve.

Here's how a banker reads the deal.

What decoupling actually does

Two spouses jointly own a private property. One transfers their share to the other, so one ends up owning 100% and the other owns nothing. The spouse who exited is now, for ABSD purposes, a first-timer again — free to buy the next property at 0% instead of 20%.

A few guardrails before we go further. This route works for private property only; HDB decoupling was closed years ago and is now allowed only in narrow cases like divorce, death, or genuine financial hardship. The contrived 99-to-1 splits that were popular a few years back are also done — IRAS clawed back tens of millions in stamp duties from arrangements it viewed as structured purely to dodge ABSD. And if you're transferring within three years of purchase, add Seller's Stamp Duty on the transferred share to the bill. A full, genuine transfer of a real share, well past the SSD window, is the clean version. Everything below assumes that.

So far, standard. Now the parts that get skipped.

The 99-1 illusion

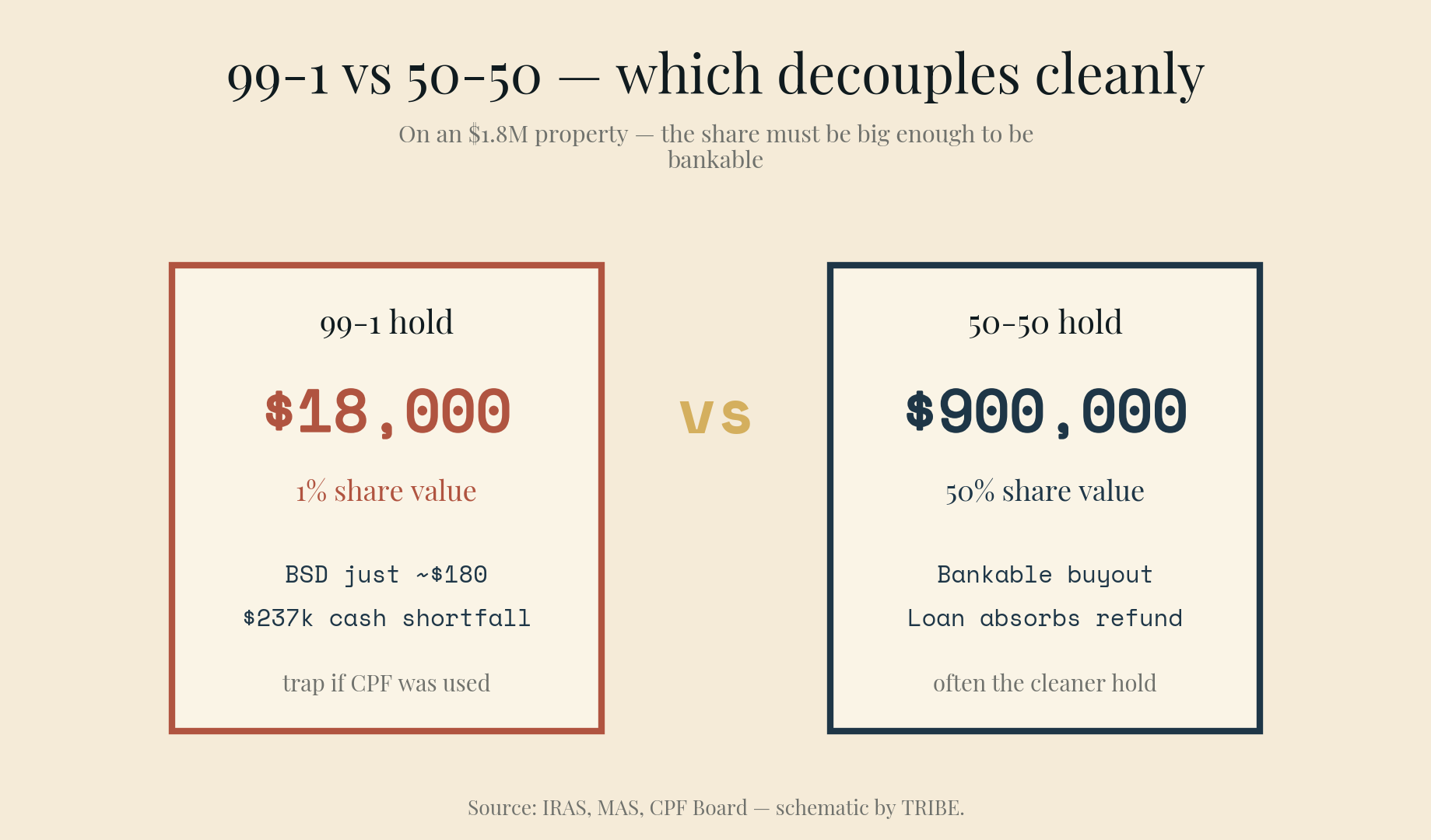

The instinct is to hold the property 99-1, with one spouse owning just 1%. The logic is seductive: when the 1% owner exits, the share being "sold" is only 1% of the value, so the buyer's stamp duty is calculated on almost nothing.

On an $1.8M property, a 1% share is worth $18,000. BSD on that is about $180. Set against a $300,000 ABSD bill, it feels like you've found a loophole.

You haven't — unless one specific thing is true: the 1% owner barely touched their CPF.

Here's what the structure can't engineer away. When that owner sells their share, they must refund every dollar of CPF they used on the property — plus the accrued interest — back into their own CPF account. CPF you withdraw for a home isn't free money; it's a loan from your future self, and it compounds at 2.5% the whole time it sits in the property. That refund comes out of the sale proceeds first, before anyone sees cash.

So if the 1% share is worth $18,000 but the exiting owner used $250,000 of CPF, the proceeds don't come anywhere close to covering the refund. The shortfall — about $237,000 in this case — has to be found in cash, out of pocket, on completion day.

That's the trap. A 99-1 hold only stays cheap if the minority owner used almost no CPF. The moment they've put real CPF into the home, the refund dwarfs their tiny share, and you need to be sitting on a large pile of cash just to unwind your own retirement money. Most couples aren't.

Why 50-50 is often the better hold

This is the counterintuitive part. A 50-50 hold usually decouples more cleanly than 99-1 — precisely because the share is large.

When one spouse owns 50% of an $1.8M home, the share being bought over is worth $900,000. That's a real asset. The remaining owner can take a fresh bank loan against it, and the sale proceeds are large enough to absorb the CPF refund and still leave cash on the table. The buyout is bankable.

A 1% share isn't. No bank is writing a meaningful loan against $18,000, so in a 99-1 unwind every dollar has to come from cash. A 50-50 unwind lets the bank do the heavy lifting.

The trade-off is honest: a bigger share means a bigger BSD bill, and a much bigger loan for the person staying on. Which brings us to the number that actually kills deals.

A worked example

Take a real-shaped case. A couple bought in 2018, the property has appreciated, and they want to decouple in 2026 so one of them can buy again.

| The property in 2026 | Amount |

|---|---|

| Purchase price (2018) | $1,000,000 |

| Market value (2026) | $1,800,000 |

| Outstanding loan | $500,000 |

| Owner A — CPF used + accrued interest | $250,000 |

| Owner B — CPF used + accrued interest | $250,000 |

| Ownership | 50% / 50% |

Owner A is going to buy out Owner B. Here's the full breakdown.

| Decoupling — A buys out B | Amount | Note |

|---|---|---|

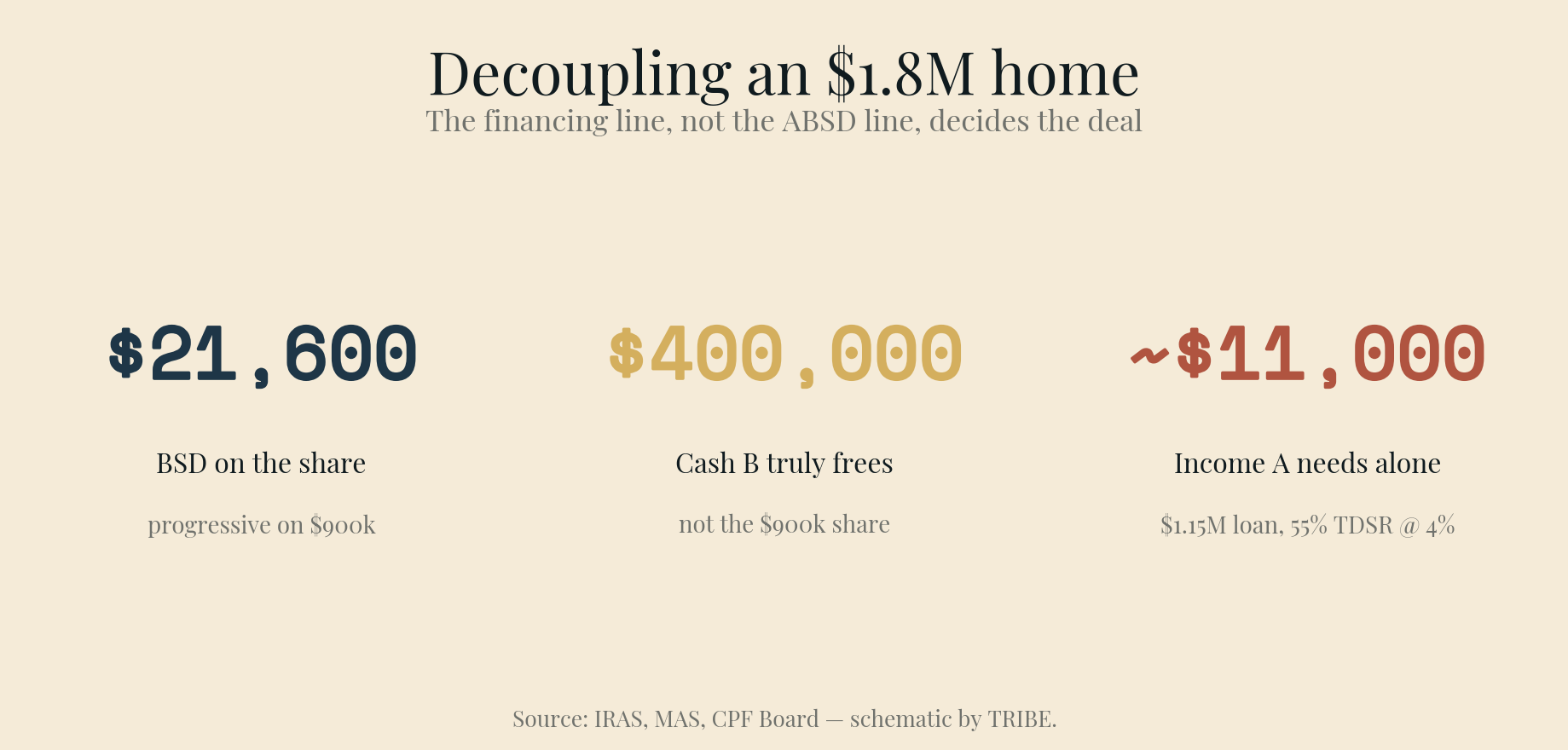

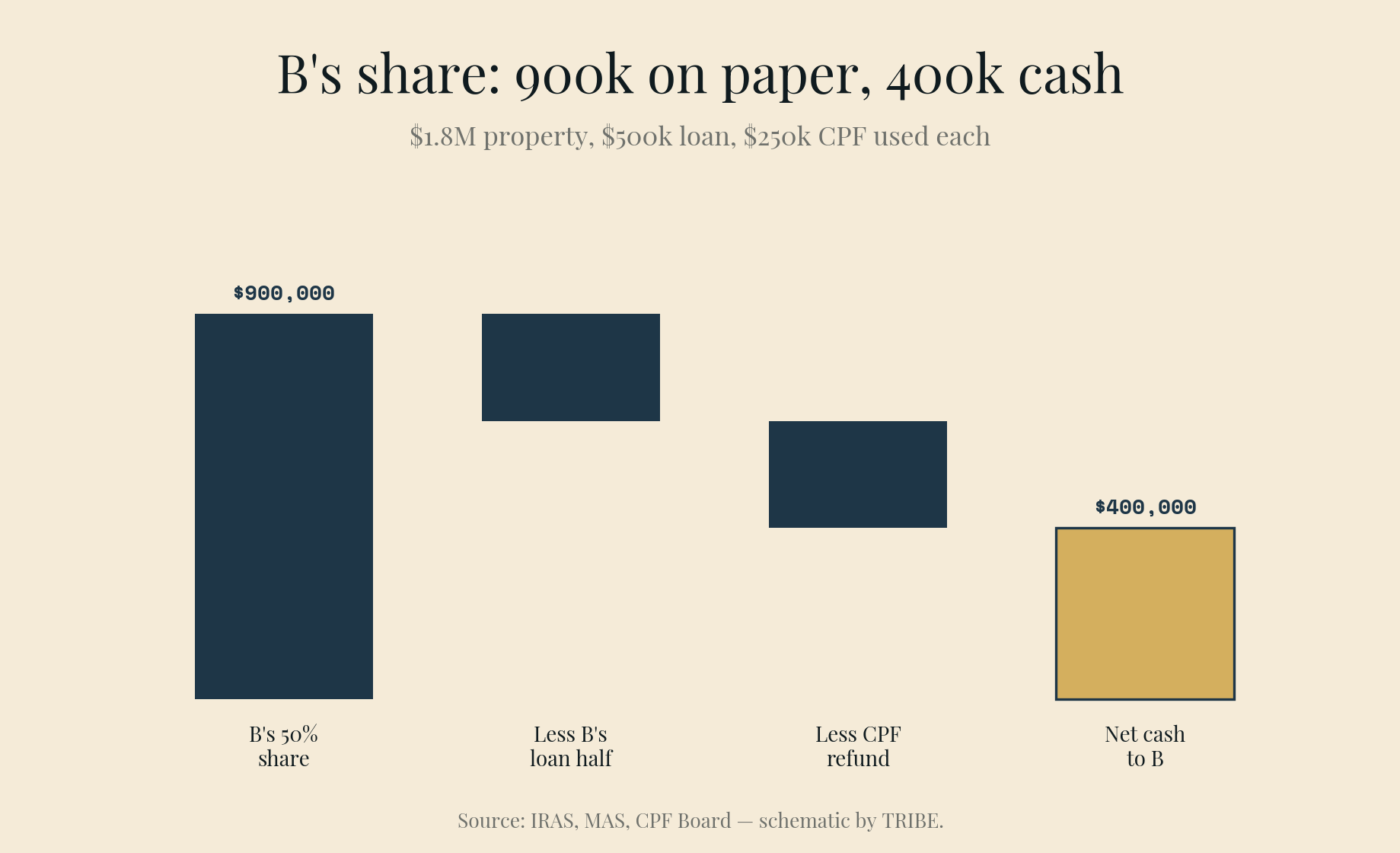

| Value of B's 50% share | $900,000 | 50% × $1.8M |

| BSD payable by A on the share | $21,600 | progressive BSD on $900k |

| Less: B's half of the loan | −$250,000 | 50% × $500k, released on refinance |

| Less: B's CPF refund | −$250,000 | back into B's CPF — not cash |

| Net cash B walks away with | $400,000 | the real freed-up amount |

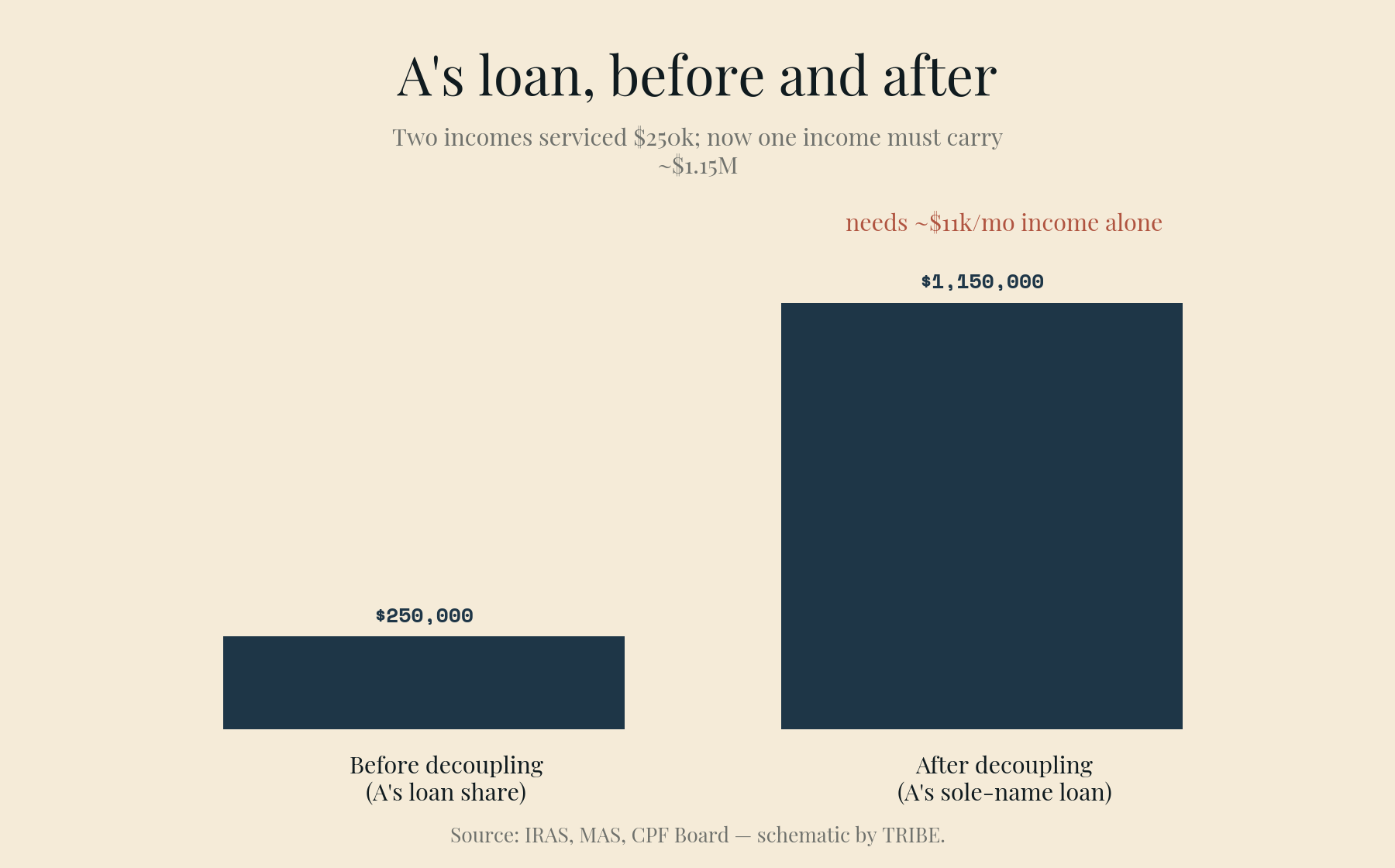

| A's new sole-name loan | ~$1,150,000 | redeems the $500k joint loan + funds B's $650k equity buyout |

| Gross income A needs to clear TDSR alone | ~$11,000 / month | $1.15M stress-tested at 4% over 25 years, 55% TDSR |

Read the bottom three rows, because that's the whole article.

First, Owner B refunds $250,000 into CPF. That's not lost — it sits in B's CPF earning 2.5% — but it is $250,000 that does not come out as spendable cash. Of the $900,000 share value, half clears B's loan and half goes back to CPF, leaving B with $400,000 in actual cash. If B is going to fund the next purchase, plan around the $400,000, not the $900,000.

Second — and this is the one that stops deals at the bank — Owner A's loan jumps from an effective $250,000 share of the old loan to about $1,150,000 in their sole name. Two incomes used to service this property. Now one income has to. Stress-tested at 4% over 25 years, a $1.15M loan needs Owner A to show roughly $11,000 a month in gross income to clear TDSR at 55% — on their own, before any car loan or other commitment eats into it.

If Owner A doesn't earn that, the decoupling doesn't fail politely at the planning stage. It fails at loan approval — after you've already paid the conveyancing and the BSD.

The banker's bottom line

Decoupling is a genuinely good move for the right couple. Typically that means one spouse comfortably out-earns the other, the higher earner stays on title and can carry the full loan solo, and the exiting spouse's CPF position is clean enough that the refund doesn't blow a hole in their cash.

It's the wrong move when both incomes were needed to service the original loan, when the exiting party has heavy CPF usage relative to their share, or when the "saving" was only ever modelled on the ABSD line and never on the financing line.

So run all four numbers before you commit, not just the first: the BSD on the transfer, the CPF refund, the cash you actually free up, and — most importantly — the income the remaining owner needs to hold the whole loan alone. The ABSD saving is real. But it's the financing that decides whether you ever get to keep it.

This is a general explainer, not financial, tax, or legal advice, and every decoupling turns on its own numbers and the rules in force at the time. Stamp duty rates, the TDSR framework, and CPF refund treatment can all change — confirm current figures with IRAS, your conveyancing lawyer, and your banker before acting on anything here.

Know what you can afford

Loan, stamp duty, CPF, and monthly repayments — work out your real budget before you commit. No registration required.

Plan my purchase →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.