Insights

Mei and Daniel Earn $9k Combined. The EC Brochure Says They Qualify. The Math Says Otherwise.

A couple at 28 with $130k saved, choosing between BTO, resale, and an EC. One path costs $1,293 a month, one buys time back with $100k of grants — and one is an eligibility letter their income can't actually cash.

By TRIBE Editorial · 11 June 2026 · 5 min read

Mei and Daniel are both 28, recently engaged, earning $9,000 a month between them — $4,800 and $4,200. They have about $60,000 in cash and $70,000 in combined CPF. Like every couple at this stage, they're staring at three doors: BTO, resale, or — the one the weekend showflat trip planted — an executive condominium.

They're a composite of the most common first-home profile we see. The math below is exact, and it starts with the door that should close first.

The EC: eligible on paper, not in practice

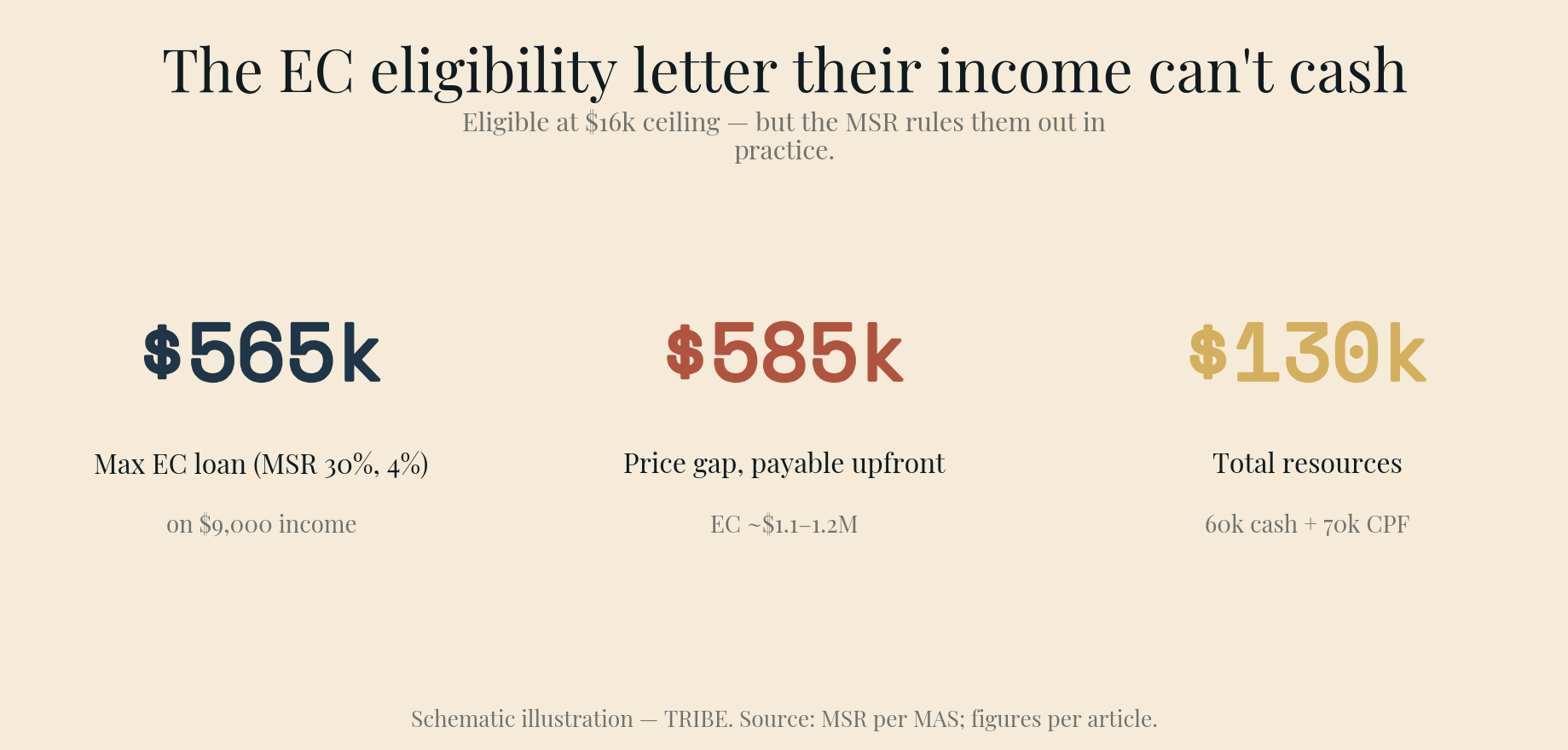

The EC income ceiling is $16,000, so at $9,000 Mei and Daniel qualify easily — there's even a CPF Family Grant for ECs at their income. The brochure isn't lying.

The Mortgage Servicing Ratio is what the brochure doesn't dwell on. EC loans are capped at 30% of gross income, stress-tested at 4%. For them: $2,700 a month, which supports a maximum loan of about $565,000 over 30 years.

Now price a new EC. Even a compact unit starts around $1.1–1.2 million. The gap between the price and the largest loan the rules allow them is roughly $585,000 — payable upfront, before BSD. Against $130,000 of resources, the conversation is over. It was over before they walked into the showflat; nobody there was incentivised to run this number out loud.

The honest restatement of the EC rule: the $16,000 ceiling describes who may apply. At today's EC prices, the MSR means the buyers who can actually fund one typically earn $13,000+ or carry serious capital. At $9,000, "EC eligibility" is a letter their income can't cash. Walk away without regret.

The real decision: BTO versus resale

Both remaining doors work. They price two different things — money and time.

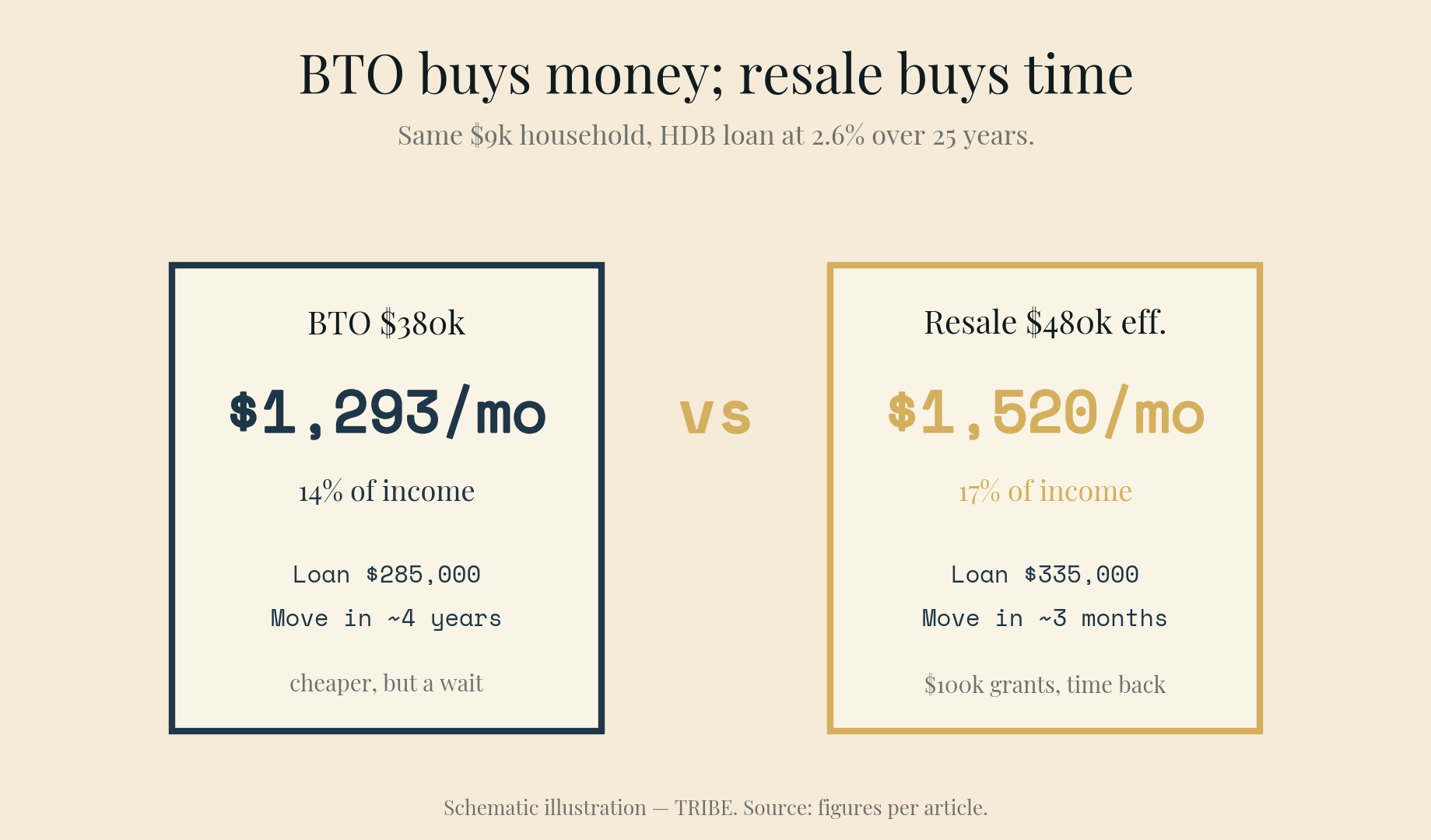

BTO — say a four-room in a newer estate at $380,000. At exactly $9,000 they scrape into the Enhanced CPF Housing Grant's last income band — worth a few thousand dollars, not the $120,000 headline (that belongs to incomes under $1,500). The real subsidy is in the price itself.

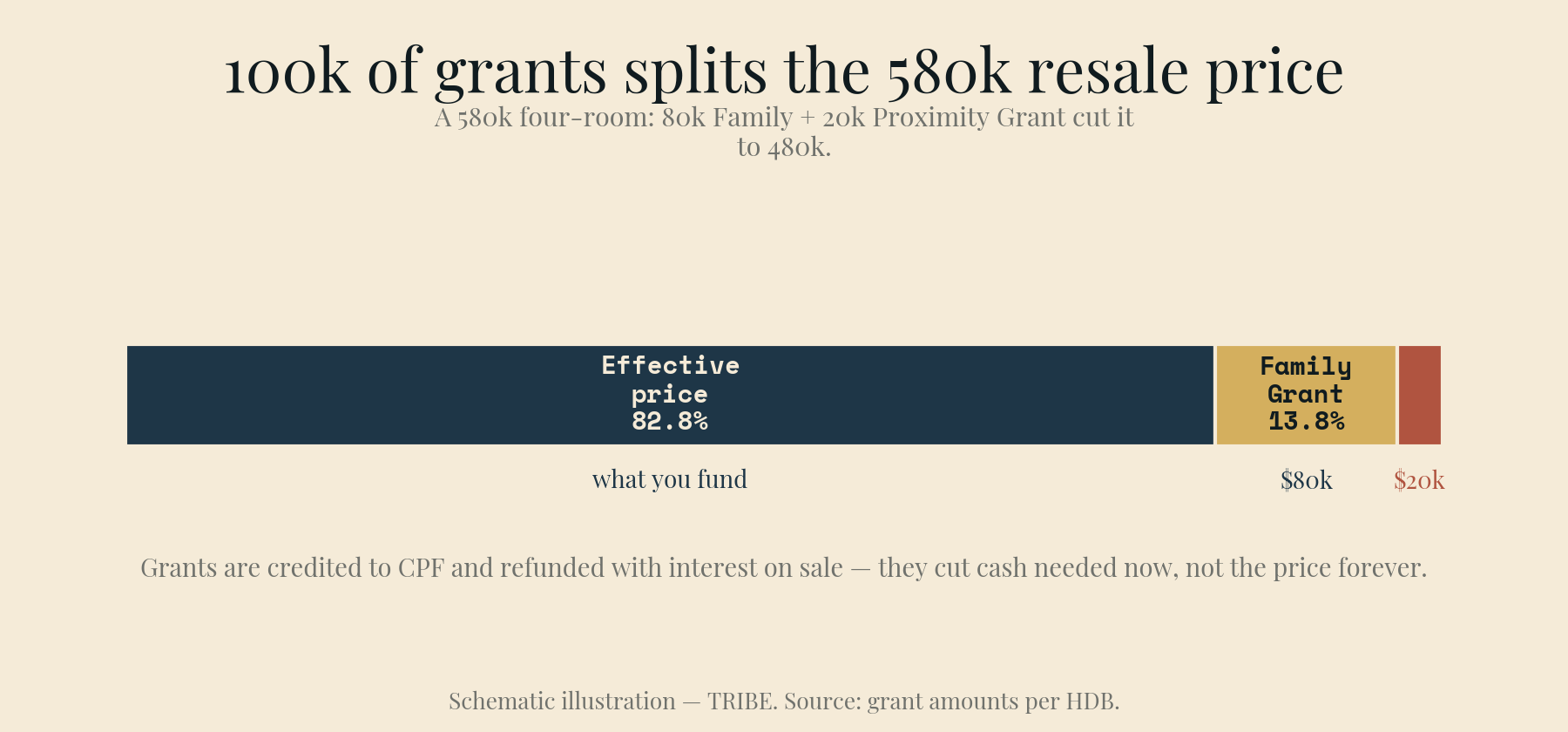

Resale — a comparable four-room near Daniel's parents at $580,000, where the grants are the story: the $80,000 Family Grant (four-room or smaller, income ceiling $14,000) plus the $20,000 Proximity Grant for living within 4km of parents — $100,000, cutting the effective price to $480,000.

| BTO $380k | Resale $580k − $100k grants | |

|---|---|---|

| Effective price | $380,000 | $480,000 |

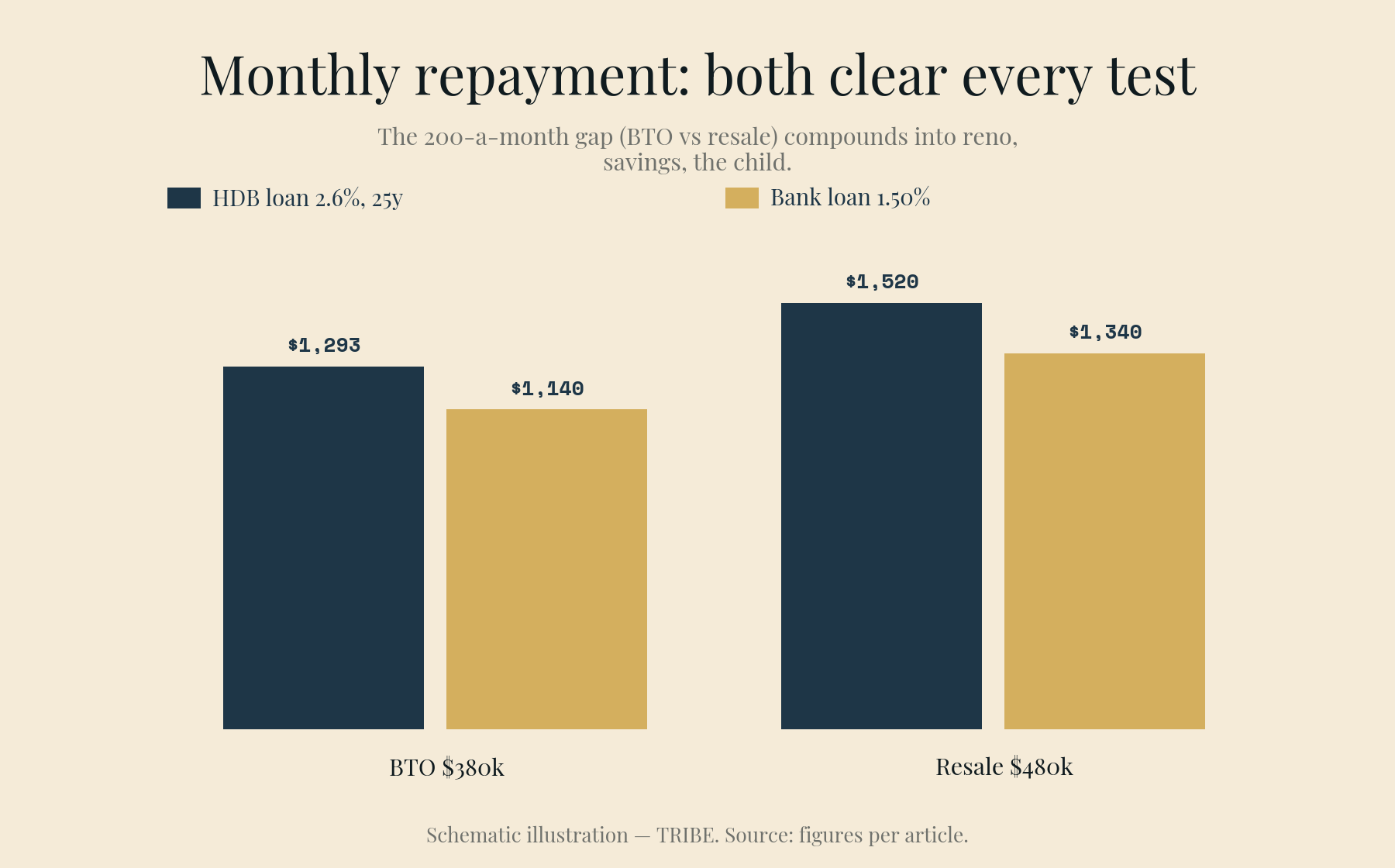

| Loan (HDB 2.6%, 25 yrs) | $285,000 | $335,000 |

| Monthly repayment | $1,293 (14% of income) | $1,520 (17% of income) |

| On a bank loan at 1.50% instead | $1,140 | $1,340 |

| When do you move in? | ~4 years | ~3 months |

| Where? | Where ballots land | Exactly where you choose |

Both clear every affordability test with room to spare — this is what buying inside your income band looks like, and it's the position the upgrader articles on this site all start from ten years later.

A note on the loan row: at $9,000 they're under the $14,000 HDB-loan ceiling, so they get to choose — HDB's 2.6% with its no-penalty flexibility and fully-CPF downpayment, or a bank loan at today's ~1.5% fixed that's cheaper but a one-way door. We've worked that exact trade here.

So which one?

The table makes it look close. The deciding variables aren't in the table:

Time. Four years of waiting is free if you have somewhere good to live (a parents' home that works) and expensive if you don't (rent at $2,500+/month for four years is $120,000+ — more than the resale grants). Couples planning a child soon are usually buying time, not flats.

The grant clawback. That $100,000 isn't a discount — it's credited to CPF and refunded (with accrued interest) to their own accounts when they sell. It lowers the cash they need now, not the price forever. Worth taking; worth understanding.

Resale risk runs both ways. The BTO's discount is genuine but its location is a lottery ticket. The resale flat's location is certain — and bought near the top of a market that just went flat, with a record MOP supply wave arriving through 2027. Negotiate accordingly; the data is on the buyer's side this year for the first time in seven.

Our lean, for this profile: if the parents' home genuinely works for four more years, BTO — $1,293 a month at 14% of income is the strongest financial start a $9k household can buy, and the $200 saved monthly versus resale compounds into the renovation, the emergency fund, the child. If living arrangements are the strain — and for most engaged couples they are — the resale with $100,000 of grants is not a consolation prize. It's the same prudence, with the four years bought back.

The door to skip is the one with the nicest showflat.

Mei and Daniel are an illustrative composite, not clients; their figures are stated assumptions. Computations are exact against June 2026 rules — MSR per MAS, grant amounts and ceilings per HDB, rates from the linked source. Grant amounts, ceilings, and BTO pricing change; verify current terms with HDB before committing. General information only, not financial advice.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.