Insights

The 3 Condos We Won't Recommend in Marine Parade / East Coast

The bottom of the Marine Parade / East Coast table isn't in a forgotten corner — it's the Meyer Road enclave, freehold and steps from a new TEL station. The sub-scores agree: cohort-lagging appreciation, sub-2% yields, no primary school within 1km.

By TRIBE Editorial · 12 June 2026 · 9 min read

District 15 is the largest district in our data — 439 scored resale projects, more than any other postal district in Singapore. The bottom of its Marine Parade / East Coast / Katong table is not where you might guess. It is not a remote walk-up far from transit. It is the Meyer Road enclave: freehold, sea-adjacent, and — since the Thomson-East Coast Line opened through here in 2024 — minutes on foot from an MRT station.

Three projects there carry a D grade, and the sub-scores behind each one tell the same story. Freehold tenure and doorstep MRT access are worth real points on the scorecard. They are not enough to outweigh appreciation that trails the same-era cohort, rental yields below 2%, and no primary school within a kilometre.

How we ranked this

The Resale Project Scorecard (RPS) grades 2,357 resale condos on seven weighted factors: secondary market strength (25%), schools (20%), project size (16%), MRT proximity (13%), tenure (10%), rental yield (10%) and future transformation (6%). The secondary market score is cohort-relative — each condo is measured only against projects that reached TOP in the same two-year window, so an old project isn't penalised for being old, only for trailing its own vintage.

Three filters before ranking, stated plainly:

- Location. Districts aren't towns. D15 stretches from Tanjong Rhu and Mountbatten in the west to the Geylang fringe in the north. We kept only projects actually in the Marine Parade / East Coast / Katong area — which excludes, for instance, Park Court (RPS 3.91, at Lorong 101 Changi on the Eunos side).

- Still standing. Two of the area's lowest scorers no longer exist as resale options: Meyer Park (RPS 3.29) was sold en bloc for $392.18 million to a UOL–Singapore Land joint venture in February 2023 and is being redeveloped as Meyer Blue, and Lodge 77 (RPS 3.17) has likewise gone to collective sale.

- Fully measured data only. Where the scorecard itself flags a placeholder — incomplete geocoding or a district-proxy yield — we set the project aside rather than rank it. That excludes Amber Glades (RPS 3.15, nominally the lowest in D15, but its schools and future transformation scores are flagged defaults; its measured factors are still weak — appreciation in the bottom 10% of its 1990-era cohort, 1.29% yield), along with Pomex Court, Klassic Court, Suites Twenty Two, Tian Court, Pengs Court and Grace Court.

What remains is the three lowest fully-measured projects in the area. All three sit within a few hundred metres of each other.

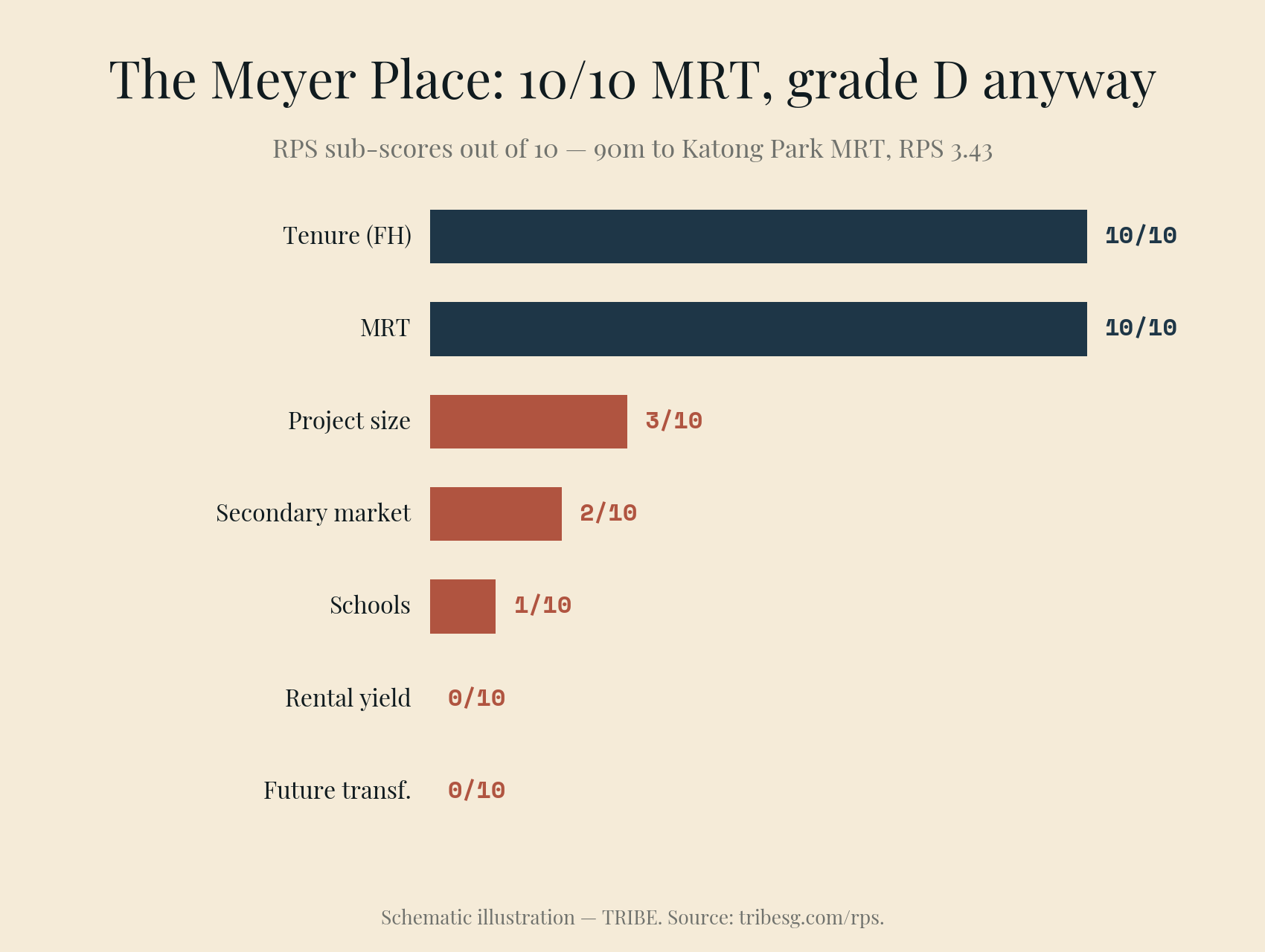

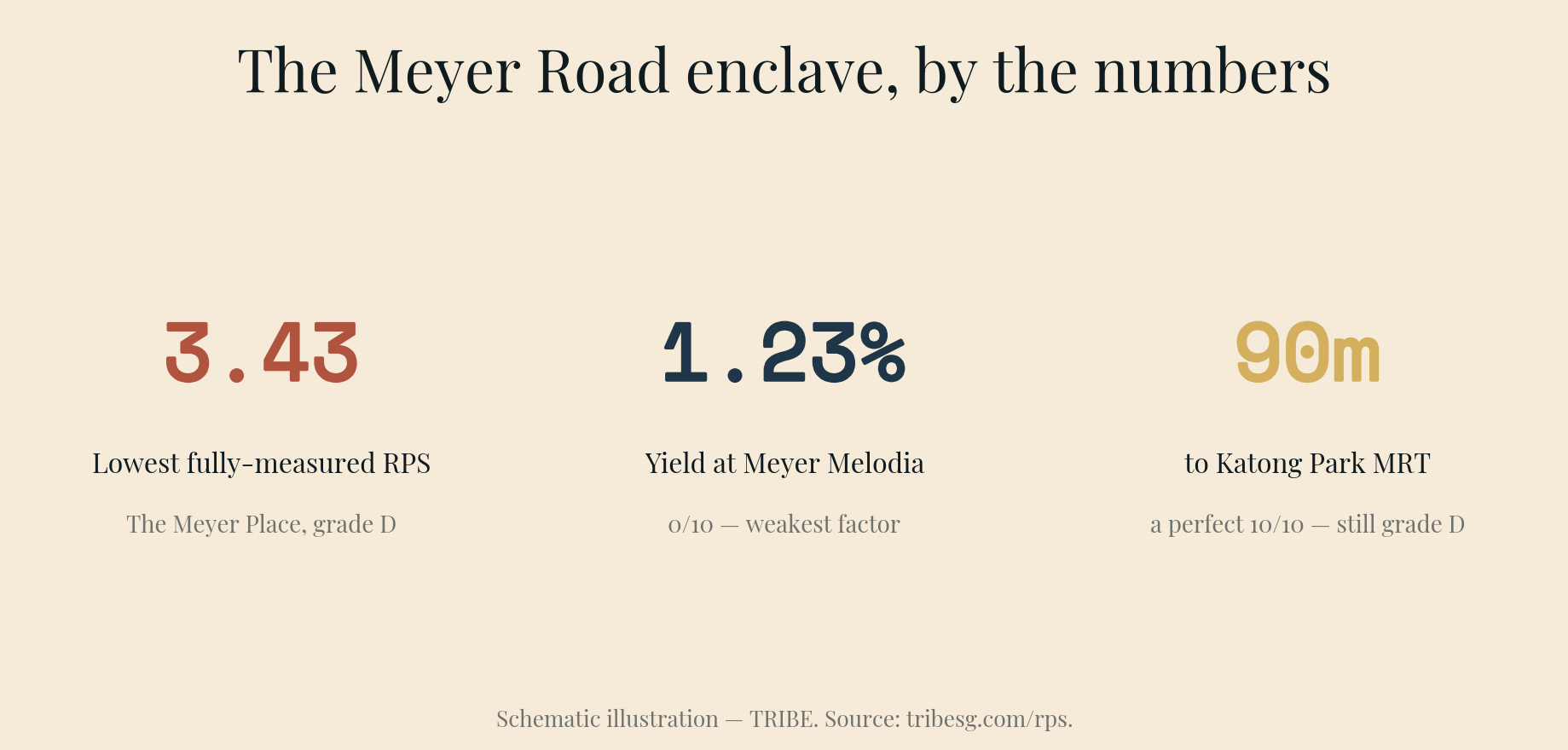

1. The Meyer Place — RPS 3.43, Grade D

A 24-unit freehold project on Meyer Place, completed in 1993. It has the single best MRT score in this article — and the weakest everything else.

- Secondary market: 2/10. The scorecard reads: "Avg Ann. of +0.00% — bottom 4% within its 1993-era cohort. Weak capital appreciation, even when judged against vintage peers."

- Rental yield: 0/10. 1.77% — in the scorecard's words, a "weak income return."

- Schools: 1/10. "No primary schools within 1km — school access is limited, particularly for parents prioritising Primary 1 registration."

- Project size: 3/10. 24 units — a "very small project; niche product with thin resale market."

- Future transformation: 0/10. No URA Master Plan zone or upcoming MRT station within 3.5km.

Its two strong factors are exactly the ones you'd expect: tenure 10/10 (freehold) and MRT 10/10 — 90 metres from Katong Park station, "direct, walk-in MRT access." On the published weights, those two factors contribute 2.3 points. Almost everything else on the card rounds to zero.

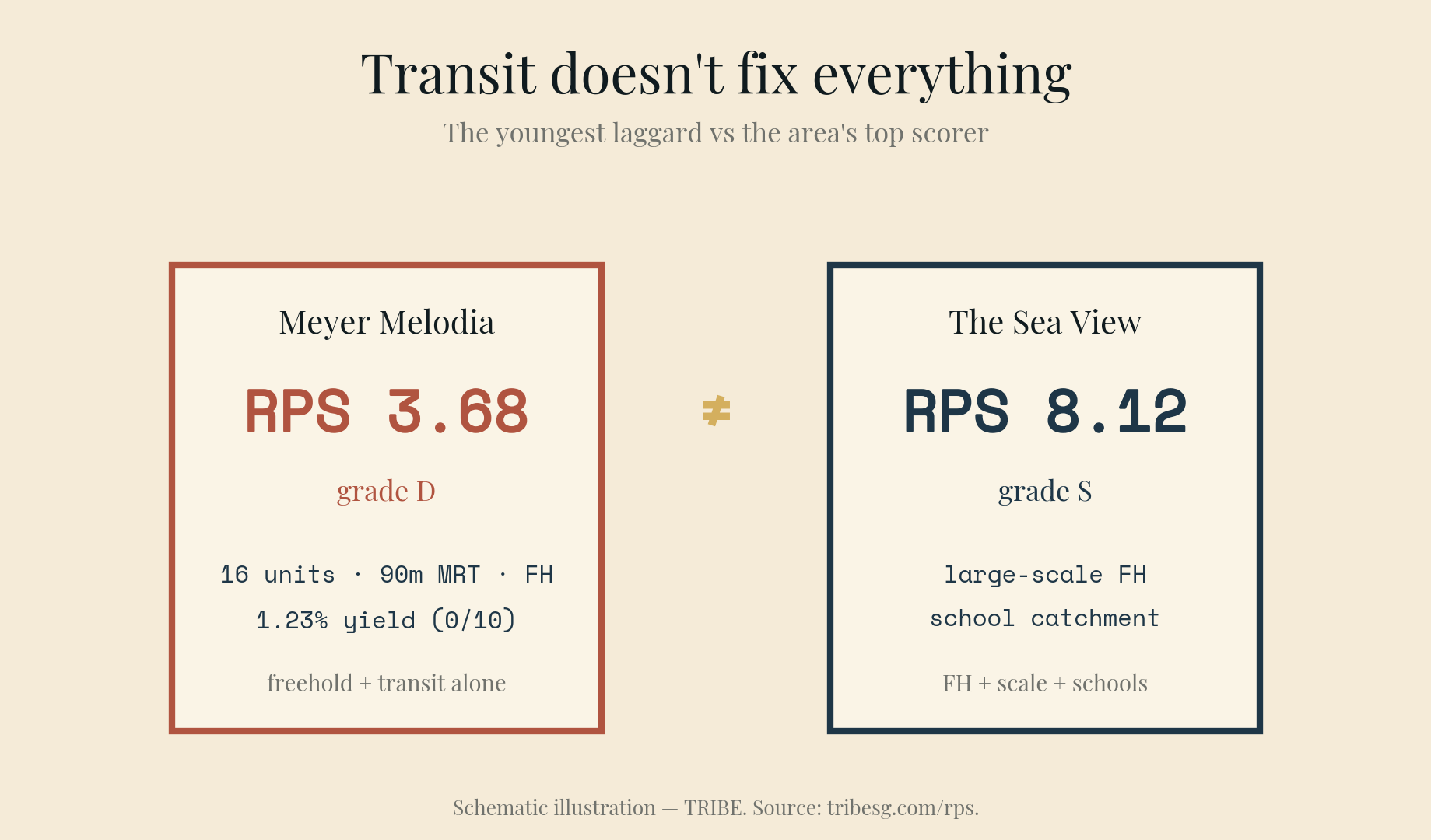

2. Meyer Melodia — RPS 3.68, Grade D

The youngest project in this article: a 16-unit freehold boutique at 2B Meyer Place, completed in 2017, the same 90 metres from Katong Park MRT.

- Secondary market: 2/10. "Avg Ann. of +0.00% — bottom 18% within its 2017-era cohort." Its contemporaries — the 2016–2018 TOP generation — have moved ahead; it hasn't kept pace.

- Rental yield: 0/10. 1.23% — the lowest yield of the three, against capital values priced for freehold sea-fringe land.

- Schools: 2/10. No primary school within 1km.

- Project size: 3/10. 16 units. Thirteen of them are two-bedders under 730 sq ft — a single motivated seller can reset the project's comparable price for everyone.

A 2017-completion project with walk-in MRT access is the strongest possible test of the "transit fixes everything" thesis. The card says it doesn't: MRT 10/10 and tenure 10/10, and the total still lands at 3.68.

3. The Sovereign — RPS 3.92, Grade D

The biggest and best-known of the three: 87 freehold units on Meyer Road, completed in 1993, with the large-format floor plates the enclave is known for.

- Secondary market: 2/10. "Avg Ann. of +3.12% — below-median performance vs same-vintage peers (36th percentile of 1993-era cohort)." Positive appreciation, but persistently behind its own generation.

- Rental yield: 0/10. 1.94% — "weak income return."

- Schools: 4/10. Again, no primary school within 1km.

- Project size: 3/10. 87 units — better than its two neighbours here, still thin.

- MRT: 8/10. 0.54km from Tanjong Katong station (TE25) — "short walk to MRT," the one factor where it concedes ground to the smaller two.

The scores, side by side

| RPS | Grade | Secondary | Yield | Schools | Size | MRT | Tenure | |

|---|---|---|---|---|---|---|---|---|

| The Meyer Place | 3.43 | D | 2/10 | 0/10 (1.77%) | 1/10 | 3/10 (24 units) | 10/10 (90m) | 10/10 (FH) |

| Meyer Melodia | 3.68 | D | 2/10 | 0/10 (1.23%) | 2/10 | 3/10 (16 units) | 10/10 (90m) | 10/10 (FH) |

| The Sovereign | 3.92 | D | 2/10 | 0/10 (1.94%) | 4/10 | 3/10 (87 units) | 8/10 (0.54km) | 10/10 (FH) |

What separates these three from the rest of the area is not project size — the D15 average size score is just 3.6/10, because boutique stock dominates the whole district. And it is not future transformation, where the district averages a low 1.4/10 now that the TEL has opened and the catalyst is delivered. The separation is on the three factors that carry 55% of the weight: secondary market (these three score 2/10 against a district mean of 6.7), schools (1–4 against 6.6) and yield (0 against 3.9).

The en bloc wrinkle

There is one thing the RPS deliberately does not score: redevelopment optionality. Meyer Park — 60 freehold units, two doors down, RPS 3.29 before it left the data — sold collectively for $392.18 million in 2023, on its third attempt. Owners of ageing freehold boutiques on Meyer Road are, in part, holding a land position, and The Sovereign in particular is routinely named as a future collective-sale candidate.

That is a real but very different bet: multi-year timelines, 80% consensus requirements, and two failed attempts for every success on this street. The RPS measures what the resale market pays a unit-by-unit seller today. On that measure, all three have lagged for decades.

What this doesn't mean

These are not bad homes. The Meyer enclave is quiet, genuinely near the sea, freehold, and now better connected than it has ever been. The Sovereign's oversized layouts are the kind of stock that is no longer built. If you are buying space and address to live in, the scorecard is not measuring your use case.

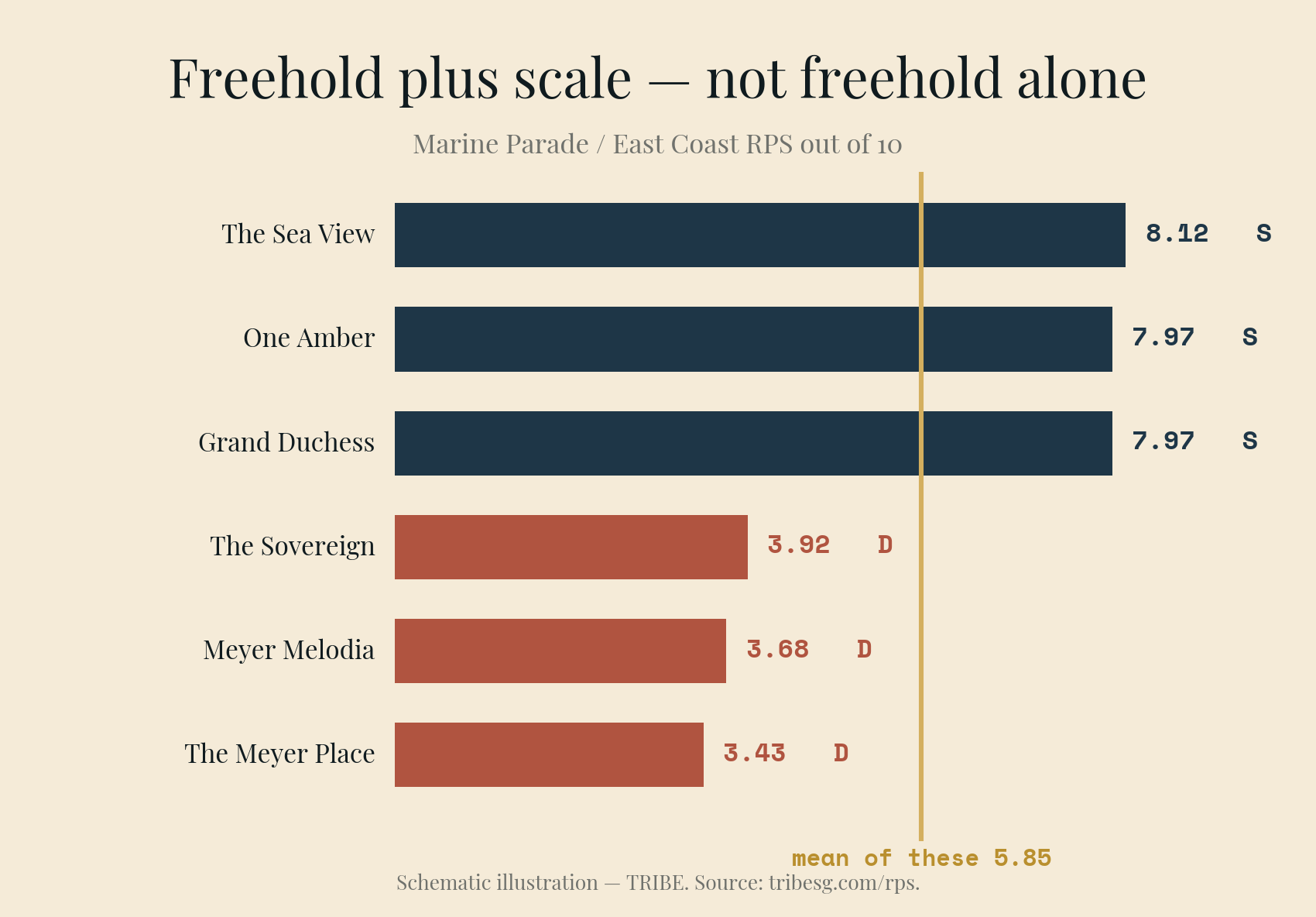

What the data does say: as resale investments, judged against their own same-era peers, all three sit in the bottom 3% of D15's 439 scored projects, with appreciation between the 4th and 36th percentile of their cohorts and yields of 1.23–1.94%. For contrast, the top of the same area — The Sea View (RPS 8.12), One Amber (7.97) and Grand Duchess @ St Patrick's (7.97), all S grade — shows what the market does reward here: freehold plus scale, school catchments and yields, not freehold alone.

Check How Your Condo Scores

Every project in this article is among the 2,357 independently scored across Singapore — each graded on seven weighted factors: secondary market performance, schools, size, MRT proximity, tenure, rental yield, and future transformation.

Score your resale condo on RPS →

No registration required. No agent call to follow. Just the data.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the Resale Project Scorecard (RPS) using 236,000+ URA REALIS transactions. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.