Insights

The 3 Condos We Won't Recommend in Bukit Panjang & Choa Chu Kang

Strip District 23 down to the two towns and the three lowest scorers aren't underperformers — two of them beat their own vintage on appreciation. They're held down by a schools data gap, thin unit counts, and, for the 2025 pair, no resale track record yet.

By TRIBE Editorial · 16 June 2026 · 10 min read

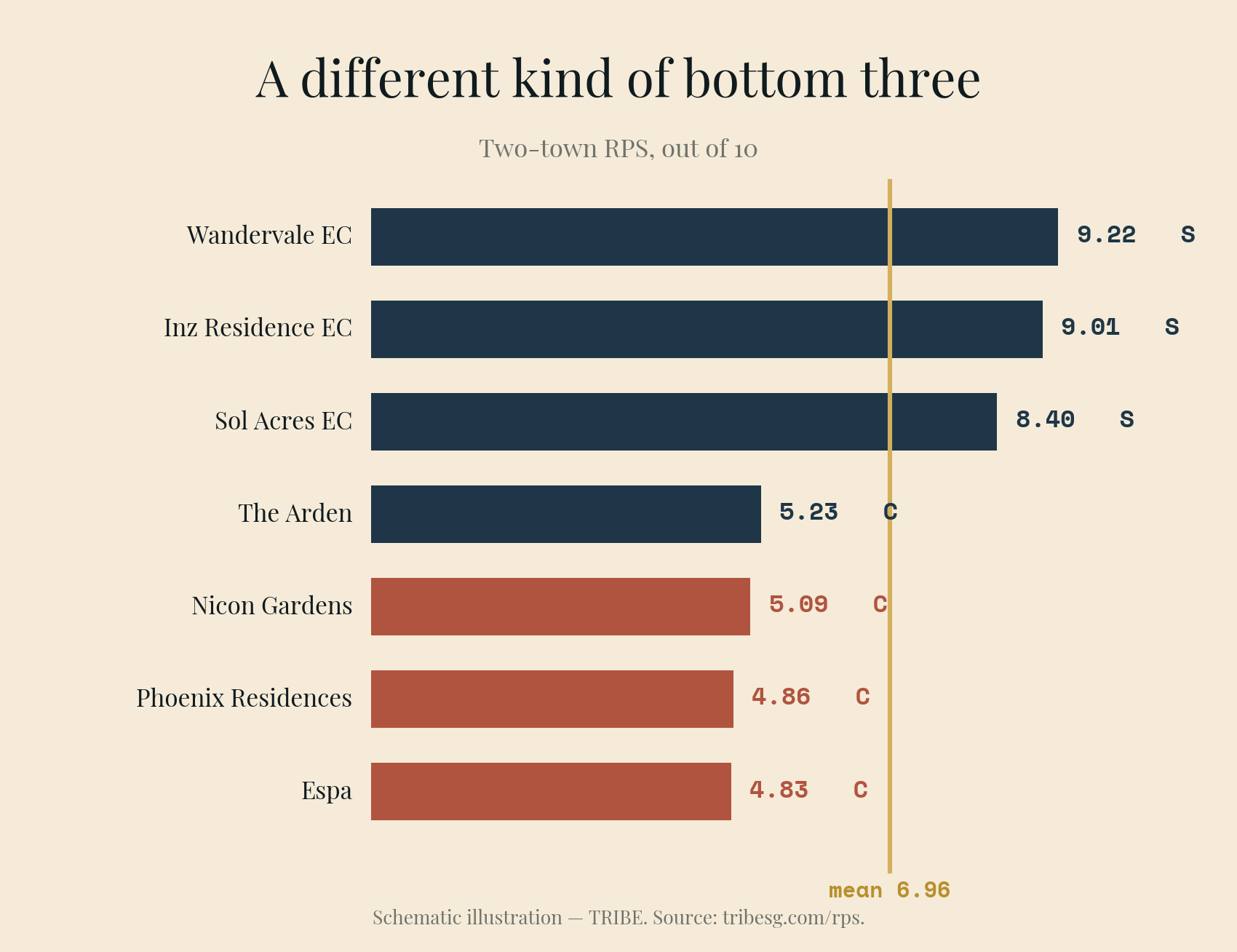

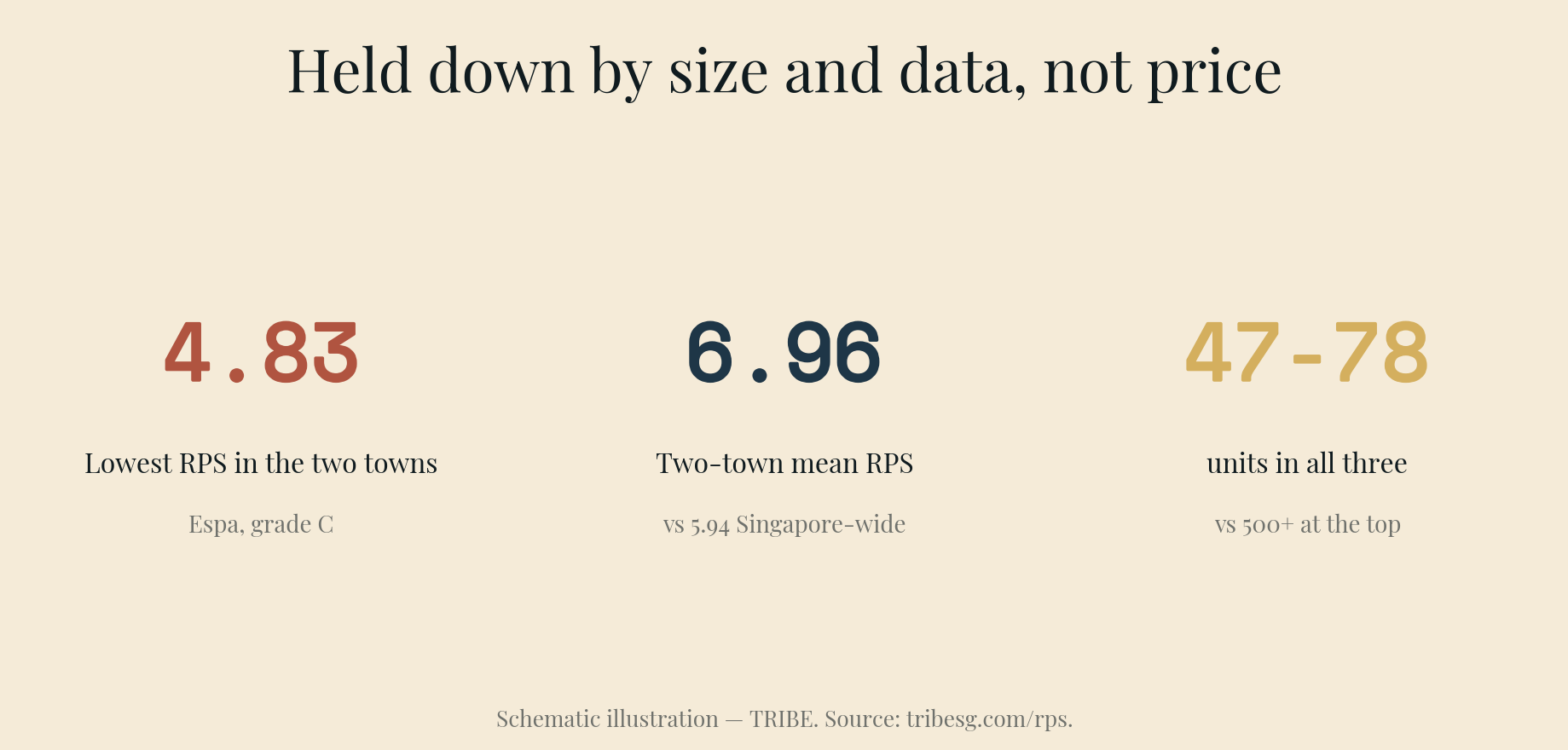

District 23 is a genuinely strong condo district. Across the 32 projects we score inside Bukit Panjang and Choa Chu Kang, the mean RPS is 6.96 out of 10 — well above the Singapore-wide mean of 5.94 — and 13 of them hold an S grade. So the bottom of this table needs reading carefully, because the three lowest scorers here are not the cautionary tales the rank suggests. Two of the three actually beat their own same-vintage peers on capital appreciation. What pulls them down is a mix of thin unit counts, a schools data gap, and — for the two newest — simply not having a resale history yet.

Here are the three projects with the lowest RPS that are actually in Bukit Panjang and Choa Chu Kang, with the exact sub-scores behind each grade, and an honest account of what those scores do and don't measure.

How we ranked this — and what we set aside

The Resale Project Scorecard (RPS) grades 2,357 resale condos on seven weighted factors: secondary market strength (25%), schools (20%), project size (16%), MRT proximity (13%), tenure (10%), rental yield (10%) and future transformation (6%). The secondary-market score is cohort-relative — each condo is measured against projects that reached TOP in the same two-year window, so an old project isn't penalised for being old, only for trailing its own vintage.

The filtering note matters here, because District 23 is not one town. It spans three planning areas: Bukit Panjang, Choa Chu Kang and Bukit Batok. The lowest raw scorers in D23 — The Amston (4.50), Hilltop Grove (4.53), Chantilly Rise (4.54) and the rest of the bottom cluster — sit around Hillview and Bukit Gombak, in the Bukit Batok planning area. They are not in Bukit Panjang or Choa Chu Kang, so they're excluded. What remains, ranked below, is the genuine bottom three of the two towns.

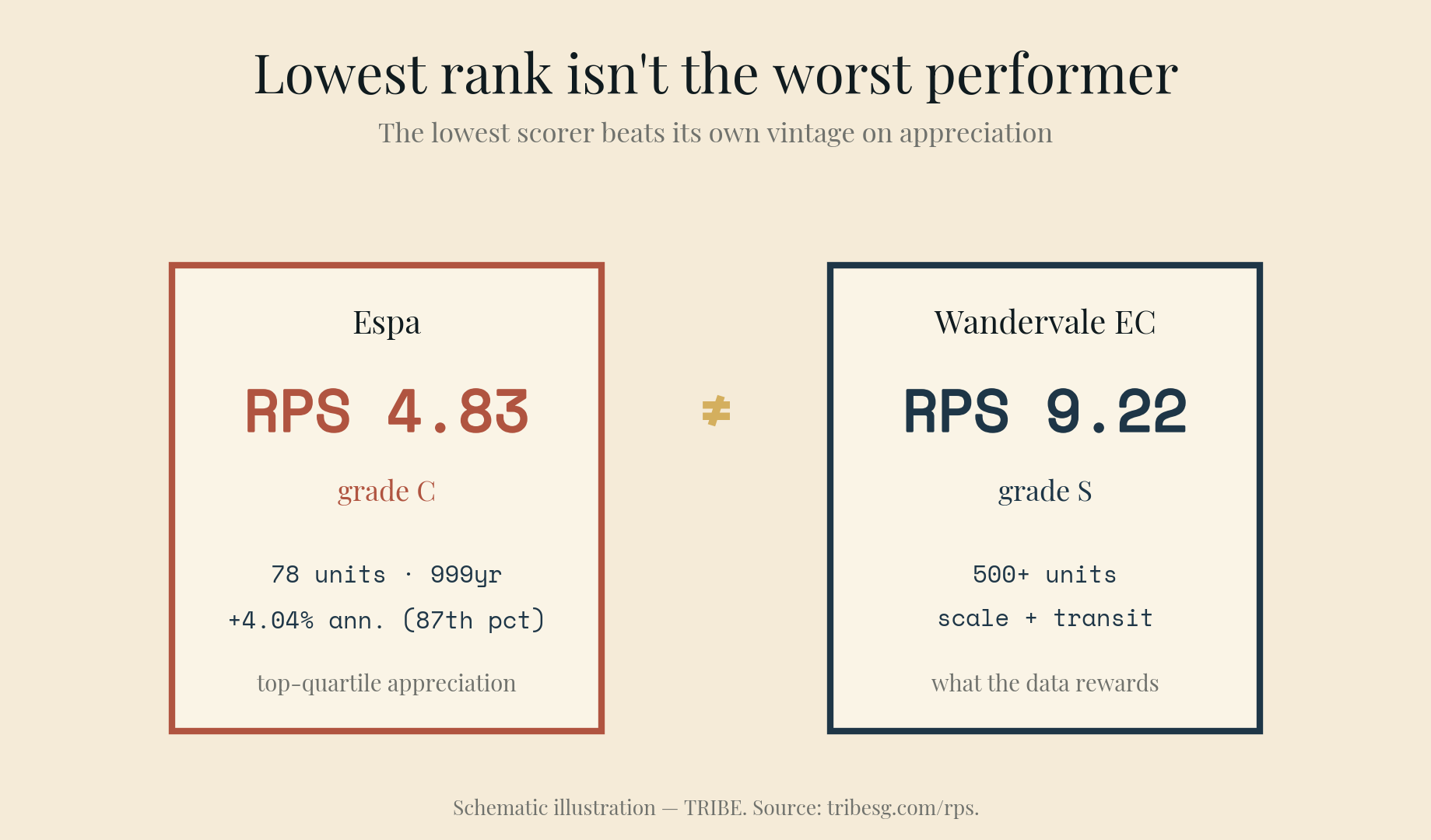

1. Espa — RPS 4.83, Grade C

A 78-unit, 999-year-leasehold project off Cashew Road, near Pending LRT, completed in 2009. It holds the lowest RPS in either town — but the reasons are narrow. The scorecard's own summary names its strengths first: "Standout strengths: tenure, capital appreciation. Key weaknesses: project size, schools."

- Capital appreciation: 9/10. "Avg Ann. of +4.04% — top-quartile performance within its 2009-era cohort (87th percentile)." This is the factor with the heaviest weight in the model, and Espa is in the top 13% of its vintage on it.

- Tenure: 10/10. "999-year tenure — effectively freehold from a valuation standpoint."

- Project size: 3/10. 78 units — "very small project; niche product with thin resale market."

- MRT: 3/10. 0.36km from Pending LRT (BP8) — "weaker MRT access, likely requires bus or car for most trips," since the LRT itself feeds the Bukit Panjang interchange rather than the city directly.

- Rental yield: 3/10. 2.75% — "below-average income return."

- Schools: 1/10. Flagged in the data as "school proximity could not be measured — address geocoding incomplete for this development." That is a placeholder, not a measured absence — we stress-test it below.

A freehold-equivalent project with top-quartile appreciation lands at the bottom of the table mainly because it is small, transit-light, and carries an unmeasured schools score. Hold that thought.

2. Phoenix Residences — RPS 4.86, Grade C

A 74-unit, 99-year-leasehold project off Choa Chu Kang Road by Phoenix LRT, completed in 2025. Unlike Espa, almost everything about its low score is fully measured — and one number explains most of it. Summary: "Standout strengths: tenure. Key weaknesses: schools, project size."

- Secondary market: 4/10. "Avg Ann. of +0.00% — below-median performance vs same-vintage peers (39th percentile of 2025-era cohort)." That +0.00% is not a price drop; it's a project that TOP'd in 2025 with essentially no resale history to measure yet. The model can't reward appreciation that hasn't had time to happen.

- Project size: 3/10. 74 units — "very small project; niche product with thin resale market."

- Schools: 3/10. "2 primary schools within 1km (nearest: West View Primary at 0.96km). Moderate school access." This one is measured.

- MRT: 7/10. 0.38km from Phoenix LRT (BP5) — "good transport convenience."

- Tenure: 9/10. ~92 years remaining — "no near-term decay concern." Rental yield is a solid 3.52% (6/10).

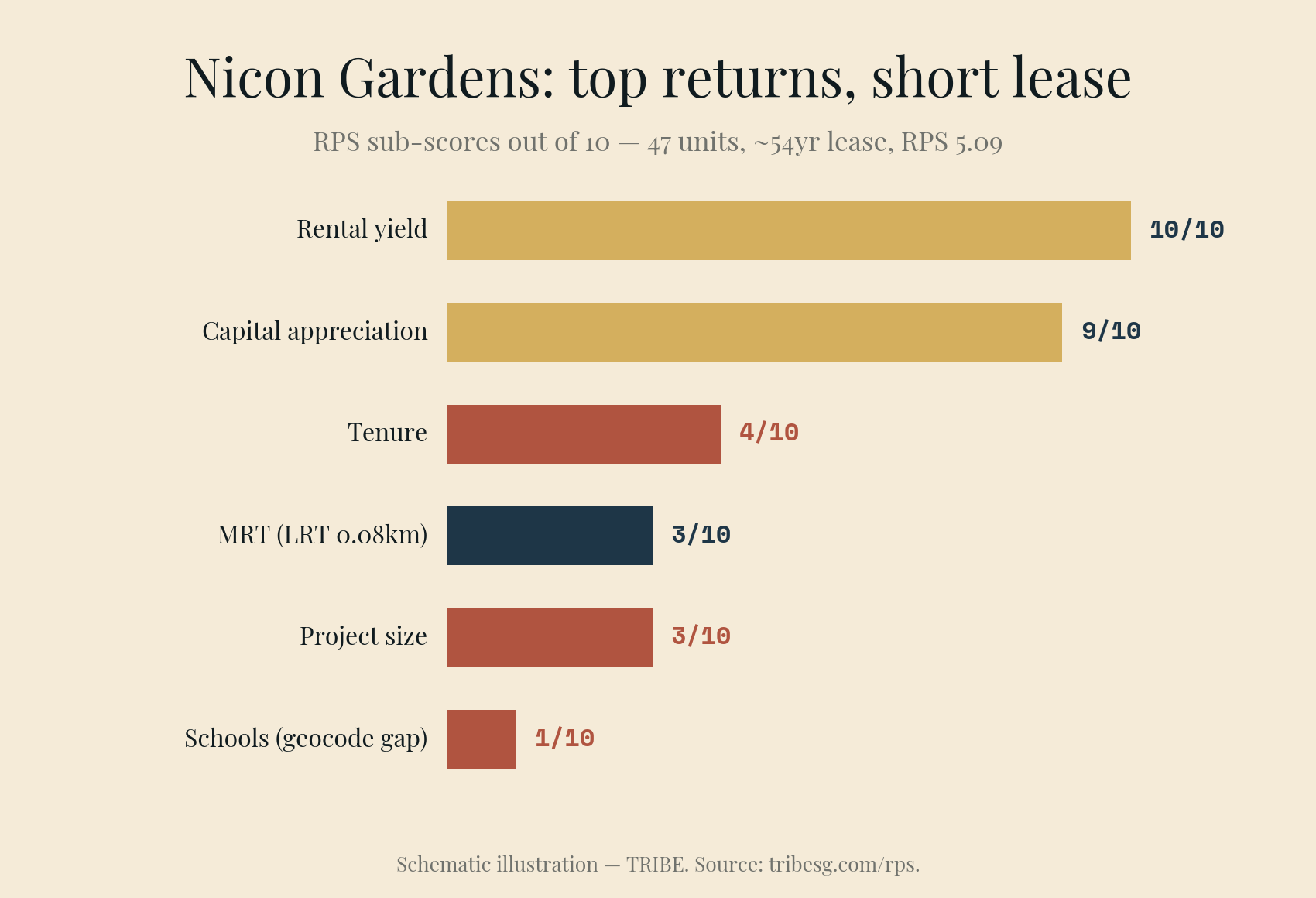

3. Nicon Gardens — RPS 5.09, Grade C

A 47-unit, 99-year-leasehold project completed in 1984, sitting almost on top of Phoenix LRT (0.08km). It is the smallest and oldest of the three — and, like Espa, scores far better on returns than its rank implies. Summary: "Standout strengths: total returns, capital appreciation. Key weaknesses: project size, schools."

- Capital appreciation: 9/10. "Avg Ann. of +4.39% — top-quartile performance within its 1984-era cohort (83rd percentile)."

- Rental yield: 10/10. 6.35% — "exceptional income return," the highest of any project in this article by a wide margin.

- Project size: 3/10. 47 units — the thinnest resale market of the three.

- Tenure: 4/10. ~54 years remaining — "lease decay is starting to impact bank valuations and CPF usage." This is the genuine, measured risk in Nicon's profile, and the one a buyer should weigh hardest.

- Schools: 1/10. Again flagged as "could not be measured — address geocoding incomplete." A placeholder, not a finding.

The scores, side by side

| RPS | Grade | Appreciation | Yield | Size | MRT | Tenure | |

|---|---|---|---|---|---|---|---|

| Espa | 4.83 | C | 9/10 (+4.04%) | 3/10 (2.75%) | 3/10 (78 units) | 3/10 (0.36km) | 10/10 (999yr) |

| Phoenix Residences | 4.86 | C | 4/10 (+0.00%) | 6/10 (3.52%) | 3/10 (74 units) | 7/10 (0.38km) | 9/10 (~92yr) |

| Nicon Gardens | 5.09 | C | 9/10 (+4.39%) | 10/10 (6.35%) | 3/10 (47 units) | 3/10 (0.08km) | 4/10 (~54yr) |

One trait is common to all three and does most of the work: size. At 47, 74 and 78 units, these are the three thinnest resale markets in the two towns, against the 500-plus-unit projects — Wandervale, Inz Residence, Sol Acres, Hillion Residences — that anchor the top. Small projects transact rarely, which makes price discovery slow and exits harder to time. That is the real, measured weakness the three share.

The data caveat — and what it changes

Methodology published, independently scored — so here is ours. Two of these three (Espa and Nicon Gardens) score 1/10 on schools because of incomplete geocoding, not a measured absence of schools. So we stress-tested it. The Phoenix/Cashew pocket is not school-poor: West View, Teck Whye and Greenridge Primaries all sit within roughly a kilometre. Under the published 20% schools weight, granting each project a measured but modest 5/10:

- Espa rises from 4.83 to about 5.63 — out of the bottom three.

- Nicon Gardens rises from 5.09 to about 5.89 — also out of the bottom three.

Grant a stronger 7/10 and both clear 6.0. In other words, the two lowest raw scores in these towns are partly an artefact of a data gap. Correct it and the genuinely measured bottom passes to Phoenix Residences (4.86, whose 3/10 schools is real) and The Arden (RPS 5.23, grade C) — the 105-unit project next door on Phoenix LRT, also completed in 2025, also scored at +0.00% appreciation for the same no-track-record reason. The two projects whose low scores survive every correction are the two newest ones, and their weakness is structural rather than performance-based: small, boutique, and too young to have a resale record.

What this doesn't mean

None of these are bad homes. Espa is effectively freehold with top-quartile appreciation — a strong long-hold for an owner who values the tenure and doesn't need a deep resale market. Nicon Gardens throws off a 6.35% gross yield, though its ~54-year lease is a real constraint a buyer must price in. Phoenix Residences and The Arden are brand-new, well-located by the LRT, with full leases — the model simply has no appreciation history to credit them with yet.

What the data does say is narrower than the headline: in Bukit Panjang and Choa Chu Kang, the lowest RPS scores are driven by thin unit counts, a schools data gap, and a lack of resale track record — not by measured price weakness. That is a very different bottom three from the one in districts where the low scorers have genuinely trailed their peers. The same two towns hold thirteen S-grade projects, led by the large mass-market ECs — Wandervale (9.22), Inz Residence (9.01) and Sol Acres (8.40) — near Keat Hong, South View and Choa Chu Kang. The data rewards scale, transit and a track record, and these three simply have less of one or more of those.

Check How Your Condo Scores

Every project in this article is among the 2,357 independently scored across Singapore — each graded on seven weighted factors: secondary market performance, schools, size, MRT proximity, tenure, rental yield, and future transformation.

Score your resale condo on RPS →

No registration required. No agent call to follow. Just the data.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the Resale Project Scorecard (RPS) using 236,000+ URA REALIS transactions. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.