Insights

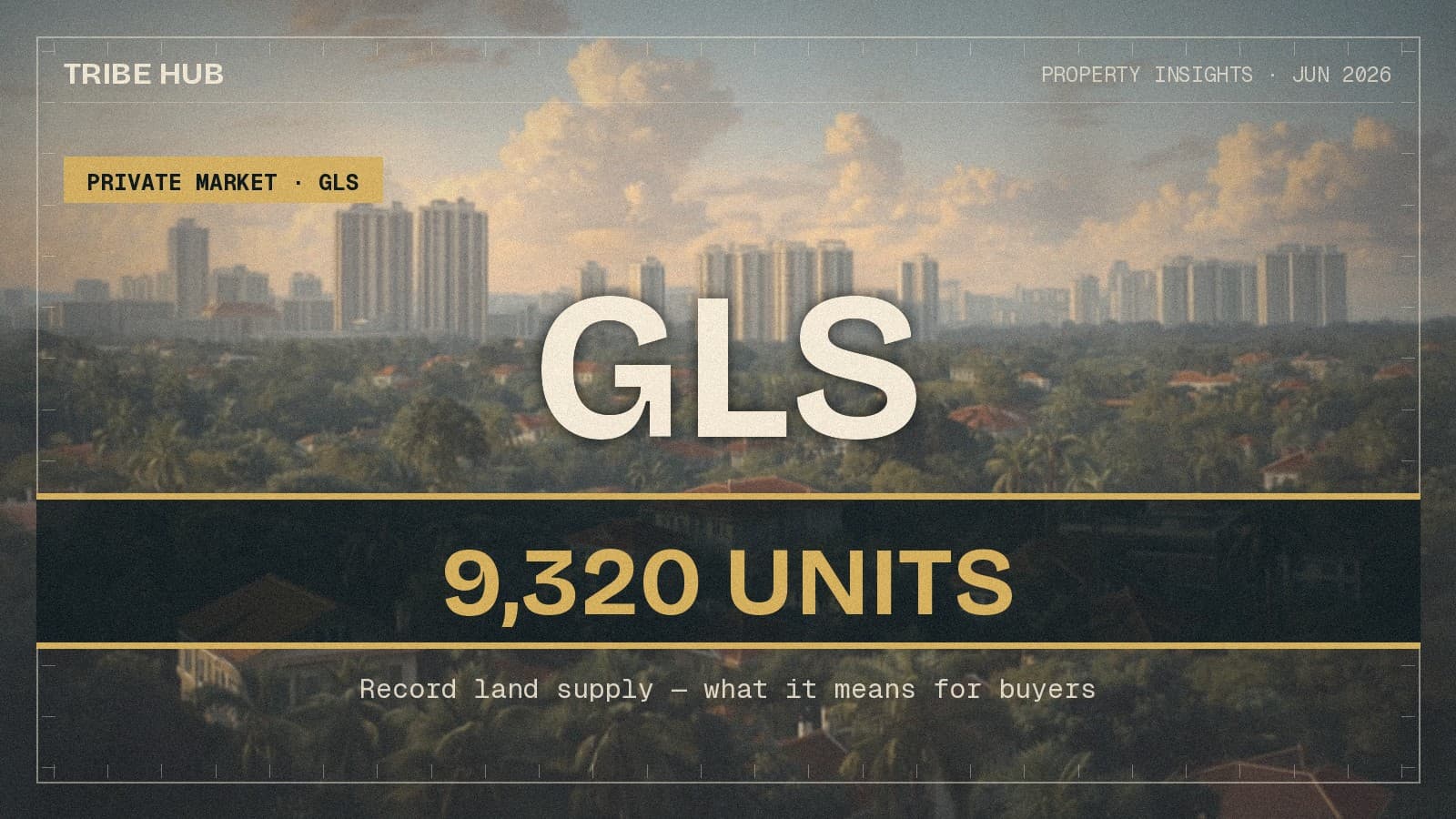

A Record Land-Supply Year — What 9,320 New Units Mean for Buyers

The 2H2026 Government Land Sales list adds nine sites and 4,745 homes, taking the full-year Confirmed List to 9,320 units — more than 50% above the 10-year average. That's the government's answer to a thin launch pipeline. Here's what it does, and doesn't, do for a buyer.

By TRIBE Editorial · 22 June 2026 · 7 min read

On 3 June, URA released the second-half 2026 Government Land Sales (GLS) programme, and the headline is supply. The Confirmed List — the sites the state commits to selling regardless of demand — adds nine plots that can yield 4,745 private homes, including 735 executive condominium units. Add the 4,575 units already committed in the first half, and the full-year Confirmed List reaches 9,320 units — more than 50% above the average annual Confirmed List supply of the past decade. For a market that spent the first half of 2026 worrying about a thin launch pipeline, that is the most consequential number of the quarter. It is also widely misread. A land-sales programme is a pipeline, not an inventory — so it is worth being precise about what record GLS supply actually changes for a buyer, and when.

What the government actually released

The GLS programme runs on two lists. The Confirmed List is sold on a fixed schedule whether or not developers ask for it — it is the government's deliberate supply lever. The Reserve List is held back and only triggered when a developer applies with an acceptable minimum bid. The 2H2026 Reserve List adds a further 13 sites — eight private residential, one commercial, two white and two hotel plots — that could yield another 4,455 private homes if developers pull them, plus commercial space and 970 hotel rooms. The committed number, the one that will reach the market regardless, is the Confirmed List.

The nine Confirmed List sites are spread deliberately across the island and the price spectrum. The largest is the Town Hall Link white site in the Jurong Lake District, at 3.72ha able to yield up to 1,200 homes plus office and retail space, with the tender opening in July — the next major phase of the JLD. The rest range from city-fringe to suburban: Berlayar Close (about 695 units) in the emerging Greater Southern Waterfront; Tanjong Rhu Close (about 505 units) on the Kallang waterfront; De Souza Avenue (about 415 units) in Upper Bukit Timah; Marina Gardens Lane (about 390 units) in Marina South; Holland Plain (about 500 units); the boutique Orchard Boulevard plot (just 110 units); a small East Coast Road site in the Siglap landed enclave (85 units); and the lone EC site at Jurong East Avenue 1 (735 units) — the first executive condominium launched in Jurong East in nearly three decades.

Two features matter more than the individual addresses. First, the prime core is being kept deliberately thin: the two Core Central Region sites — Orchard Boulevard and Holland Plain — together carry about 720 units, down from roughly 1,065 in the first half. The volume is being directed to the city fringe and suburbs, where genuine owner-occupier demand sits. Second, the full-year EC supply on the Confirmed List comes to 1,370 units, well below the 1,970 supplied in 2025 — a measured response while the market digests May's tightening of EC rules.

Why now — supply as a price lever

This is not a neutral schedule. Releasing record Confirmed List supply is the policy answer to two pressures TRIBE has tracked all year. The first is the thin new-launch pipeline — relatively few projects launching in 2026 against a stock of unsold units, which concentrates buyer demand and supports prices. The second is firm land bidding. Developers have stayed hungry: the average GLS tender this year (excluding EC sites) has drawn 4.6 bidders, up from 2.4 in 2024 and close to last year's 5.6, and recent launches such as those in Tengah and the city fringe have sold strongly on opening weekends. When developers compete that hard for land, the land cost feeds into future selling prices.

A bigger Confirmed List works on both. More committed sites mean more future launches, which spreads demand thinner across more choices. And clustering several plots in the same emerging precinct — as the 2H2026 list does in Holland Plain, the Greater Southern Waterfront and Marina South — builds critical mass while tempering the scarcity premium a developer would otherwise pay for a one-off site. The government is, in effect, using supply to take some heat out of land prices before it reaches buyers. EdgeProp's own framing of the release was blunt: more land, less heat.

What it does — and doesn't — do for a buyer

Here is the part that gets lost. GLS supply is a forward pipeline, not inventory you can buy this year. A Confirmed List site released in late 2026 is tendered, awarded, designed, approved and built — the new homes on these nine plots will mostly reach the market between roughly 2028 and 2030. The 9,320 figure tells you about price pressure in 2028 and beyond. It tells you very little about the flat or condo you are choosing between this quarter.

So the honest reading splits by horizon. Near term, record GLS supply does not crack prices: today's resale market is governed by the existing thin pipeline and firm land bids, not by sites that are still empty. Anyone hoping the announcement signals an imminent price drop is misreading the timeline. Medium term, the case is real and directional. A sustained Confirmed List running 50% above its decade average — if the government keeps it up — argues against the scarcity story that justifies paying a premium today on the assumption supply will stay tight forever. It won't. The state has both the land bank and the demonstrated will to release it.

For a buyer, that turns into three practical points. If you are buying to live in and have found the right home, the supply pipeline is not a reason to wait years — your horizon is longer than the noise. If you are buying partly on the bet that scarcity keeps pushing prices up, the 9,320 number is a caution: the structural supply response is larger than the launch-drought headlines suggest. And if a specific precinct on the list fits you — the Jurong Lake District, the Greater Southern Waterfront, Marina South, Jurong East for an EC — the clustering means more choice and more price discipline are coming to that exact area, which is worth factoring into how much you stretch for the first project to launch there.

The launch drought is real, and it is supporting prices now. But it has a delivery date. The 2H2026 GLS programme is the clearest signal yet of when the supply answer arrives — and a record Confirmed List is a reminder that, in Singapore's market, persistent scarcity is usually a policy choice rather than a permanent condition.

See where every resale project lands on the fundamentals at tribesg.com/rps.

Sources: URA, 2H2026 Government Land Sales Programme (3 June 2026); EdgeProp Singapore; ERA Singapore; bidder data from Huttons Data Analytics via URA. Figures as at June 2026.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the Resale Project Scorecard (RPS) using 236,000+ URA REALIS transactions. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.