Insights

Foreign and PR Buyers Are Vanishing — What It Means for OCR Resale Demand

Foreigners made up roughly 9% of private home buyers before 2023. After the 60% ABSD, that share has collapsed toward a rounding error. But here's the part most headlines miss: the pullback is overwhelmingly a CCR luxury story — not an OCR resale one.

By TRIBE Editorial · 16 June 2026 · 7 min read

You will have seen the headline in some form: foreign buyers are disappearing from Singapore's private housing market. It is true, and the scale is genuinely striking. But the conclusion most people draw from it — that demand for private homes is hollowing out — does not survive contact with the data. The foreigner pullback is real; it is also, overwhelmingly, a Core Central Region luxury story. For the typical Outside Central Region resale buyer or HDB upgrader, the vanishing foreigner was never really part of their market to begin with.

This piece walks through how big the drop actually was, why it happened, who is buying now, and what it does — and does not — mean for OCR resale demand.

How big was the drop

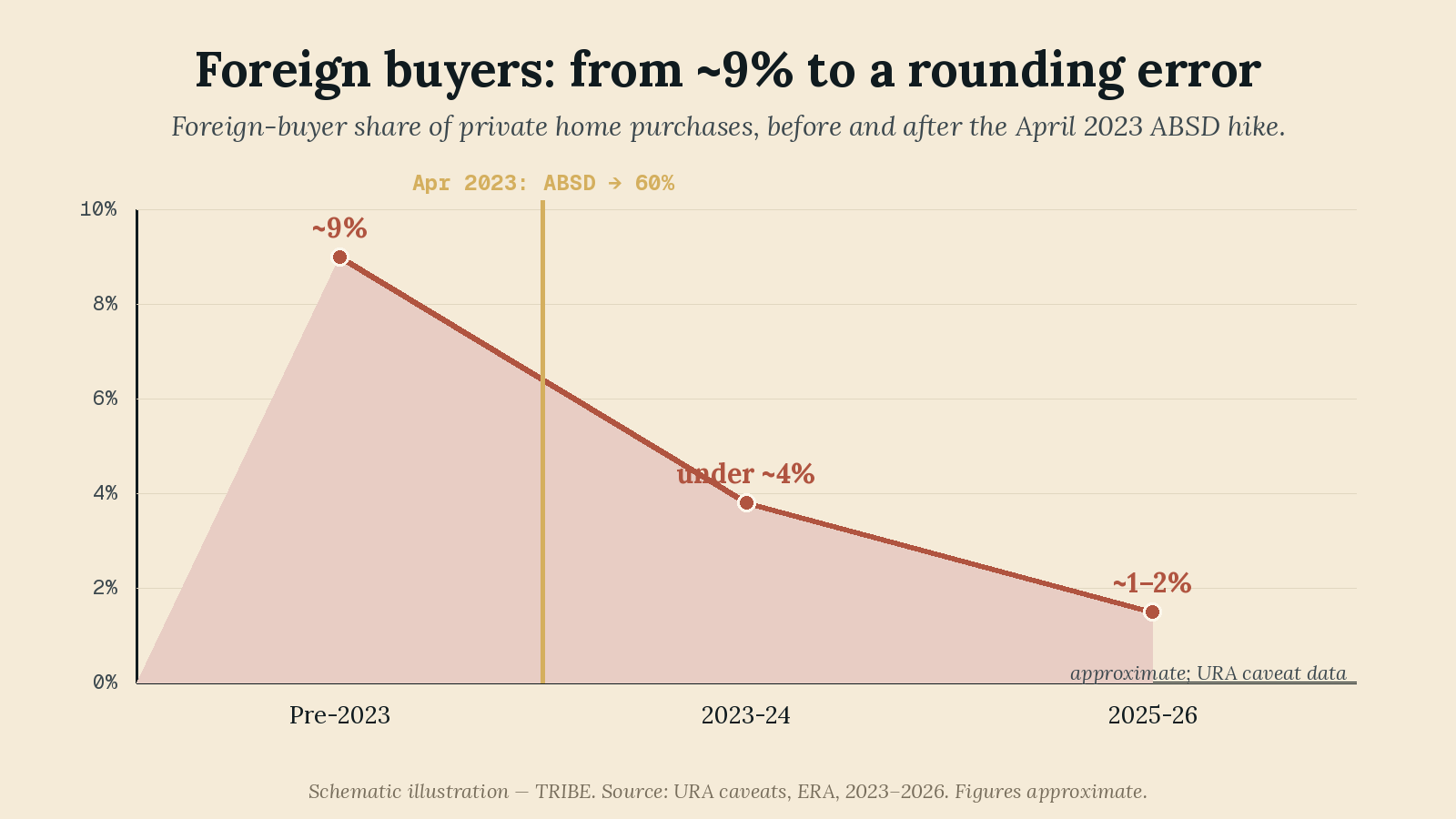

Before the April 2023 cooling measures, foreigners accounted for roughly 9% of private new home purchases — some measures put the earlier peak nearer 7%, so treat the figure as approximate and directional. After the 60% Additional Buyer's Stamp Duty (ABSD) landed, that share fell under about 4% across 2023–24, and then to roughly 1–2% by 2024–25. These are approximate figures based on URA caveat data, but the direction is unambiguous.

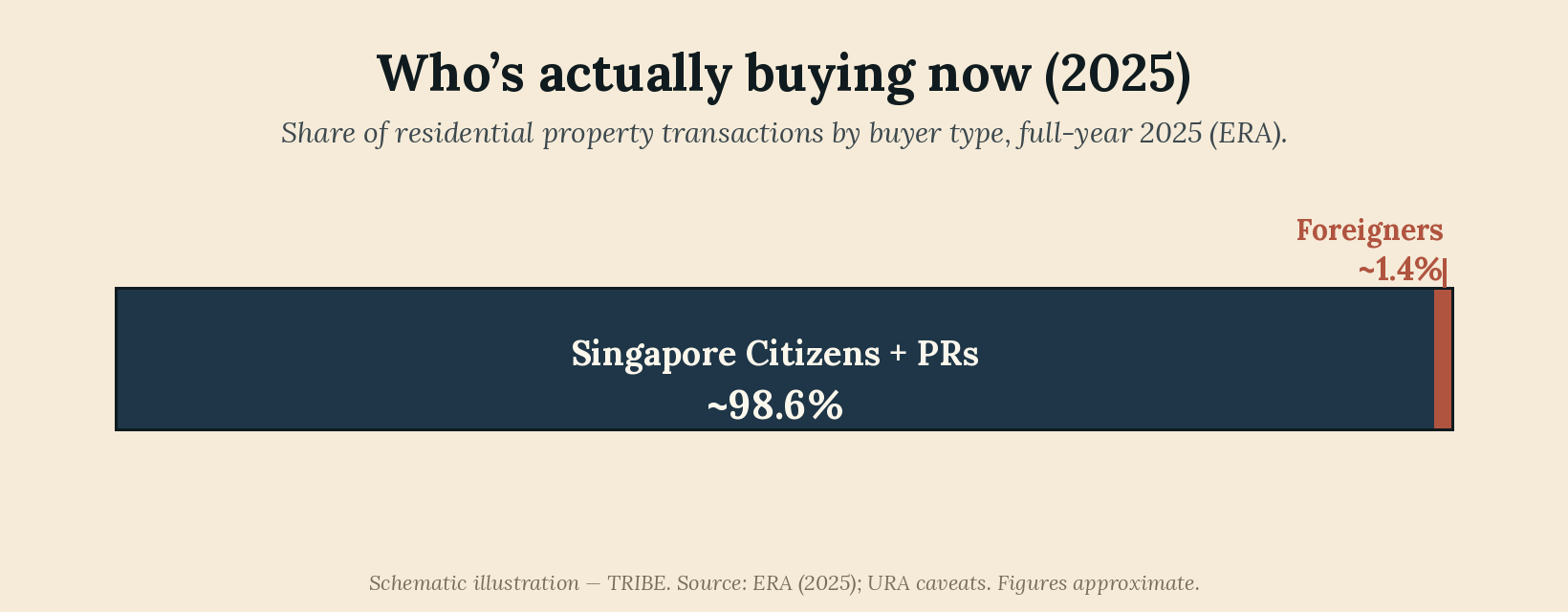

ERA's read on 2025 puts a finer point on it: more than 98.6% of residential property transactions that year were made by Singapore citizens and permanent residents — which leaves foreigners at roughly 1.4% of the market. A buyer group that once moved close to one in ten private deals now moves something closer to one in seventy. That is not a soft decline; it is a structural exit.

Why: the ABSD wall

The cause is not a mystery, and it is not a change in how attractive Singapore is to live in. It is a number.

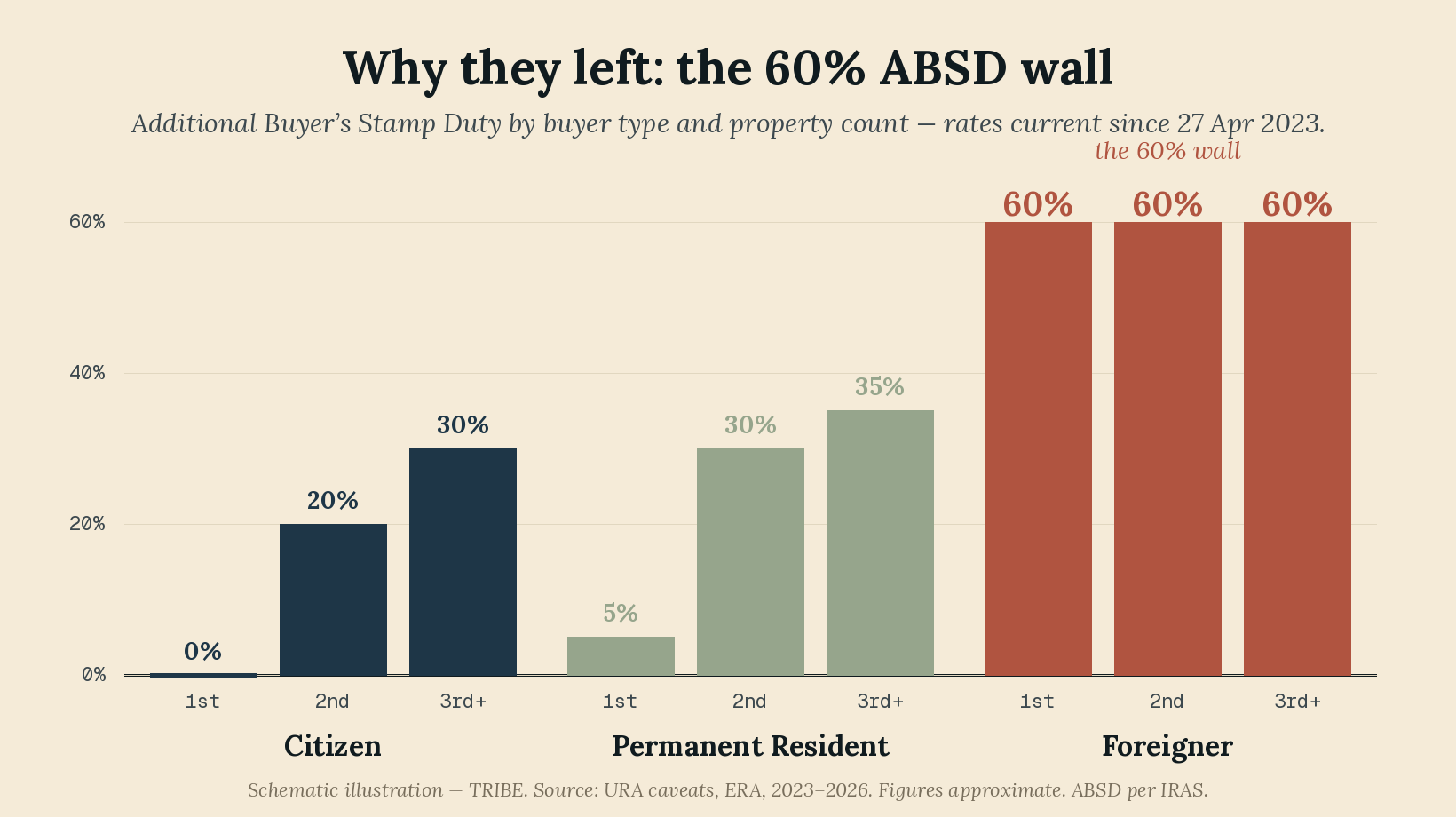

Since 27 April 2023, foreigners pay 60% ABSD on any residential purchase — double the previous 30%. The contrast with everyone else is stark. Citizens pay nothing on a first home, 20% on a second, and 30% on a third or more. Permanent residents pay 5% on a first property, 30% on a second, and 35% on a third or more. A foreigner buying a S$2 million home pays S$1.2 million in ABSD alone, on top of the price and the standard Buyer's Stamp Duty.

At that level the duty is not a friction; it is a wall. It is meant to be. The Government has signalled that the 60% rate would only ease if the market has "clearly stabilised" — so for planning purposes, this is the operating environment, not a temporary spike.

Who's buying now

If foreigners have left, the natural question is who filled the gap. The answer is: nobody had to, because the gap was small to begin with. The market was already overwhelmingly local.

On ERA's figures, citizens and PRs made up more than 98.6% of 2025 transactions. The private market is, and for some time has been, a domestic market with a luxury fringe. When that fringe contracts, the headline share of foreign buyers falls sharply — but the volume of homes changing hands between Singaporeans and PRs is barely touched. This is the single most important fact to hold onto: the foreigner exit changes the composition of demand far more than the level of it for the mass market.

What it means for OCR

Here is where the OCR angle comes in, and where the story diverges sharply by region.

Foreign demand has always concentrated in the Core Central Region — the prime, luxury end. OCR demand, by contrast, is overwhelmingly local: citizens and PRs, many of them HDB upgraders moving into their first or second private home. So when foreigners step back, the pressure lands on CCR luxury, not on OCR resale.

The price data bears this out. In URA's Q1 2026 statistics, private home prices rose 0.9% quarter-on-quarter (revised up from the +0.3% flash estimate), and the OCR led at about +2.2% — the most resilient sub-market — even as overall transaction volumes fell sharply, around 40% versus the prior quarter. The regional split of transactions in Q1 2026 ran roughly OCR 50%, RCR 26%, CCR 24%. The suburbs are where the deals are, and those deals are local.

For an OCR resale seller, the practical takeaway is reassurance with a caveat. Your buyer pool was never the foreigner; it is the upgrader and the local owner-occupier, and that pool is intact. The soft spot in your market is volume and price discipline — buyers are deliberate and the broader transaction count is down — not a demographic collapse on the demand side.

For an OCR resale buyer or HDB upgrader, the "vanishing foreigner" narrative is largely noise. It does not loosen the segment you are competing in, because foreigners were barely in it. If you are waiting for foreign withdrawal to soften OCR prices, the mechanism you are counting on does not really exist at this end of the market.

The close

Two markets are being described by one headline. For the CCR luxury segment, the foreigner pullback is close to the whole game: a buyer group that defined the prime end has been priced out by a 60% wall, and that segment now leans on a much thinner pool of local high-net-worth and PR demand. For the typical OCR resale buyer or seller — the HDB upgrader, the local owner-occupier — it changes very little, because their market was always domestic. Read the foreigner story for what it is: a precise statement about prime property, not a verdict on the suburbs where most Singaporeans actually transact.

Sources: URA Q1 2026 private residential statistics; ERA 1Q 2026 URA private residential report; ABSD rates per IRAS (current since 27 Apr 2023). Buyer-share figures are approximate, based on URA caveat data.

Silas Tan is a District Director at Huttons Asia and co-founder of TRIBE. He built the Resale Project Scorecard (RPS) using 236,000+ URA REALIS transactions. This article is for informational purposes and does not constitute financial or investment advice. CEA Registration R000303I.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.