Insights

Both 45, Thirteen Years of CPF on Autopilot — the Decoupling Case That Doesn't Work

A couple, both 45, serviced their condo almost entirely with CPF since 2013 and now want to decouple for a second property. We ran every number — the refund, the BSD, the TDSR at their age. It fails at three separate gates.

By TRIBE Editorial · 12 June 2026 · 8 min read

David and Serene are both 45. They bought a $1.25 million condo in 2013, set the mortgage GIRO to CPF in week one, and never touched it again. Now the property is worth about $1.78 million, a friend has just decoupled to buy a second condo "ABSD-free," and they want to do the same: Serene exits, becomes a first-timer again, and buys a $1.3 million two-bedder to rent out. We ran the full ledger. It fails — not at one gate, but at three, and the thing that kills it is the very habit that made the first condo feel painless: thirteen years of paying the bank with CPF.

David and Serene are an illustrative composite of a profile we meet constantly; their figures are stated assumptions, and every computation below is run exactly against the rules in force in June 2026. We've written before about how a banker reads a decoupling — this is the case study of the couple that article warns about.

The property, thirteen years in

The starting position, with the loan amortised at an assumed average rate of 2% since 2013:

| The condo in June 2026 | Amount |

|---|---|

| Purchase price (2013) | $1,250,000 |

| Market value (2026) | $1,780,000 |

| Outstanding loan (after 161 instalments of $3,696) | $625,563 |

| Ownership | 50% / 50% |

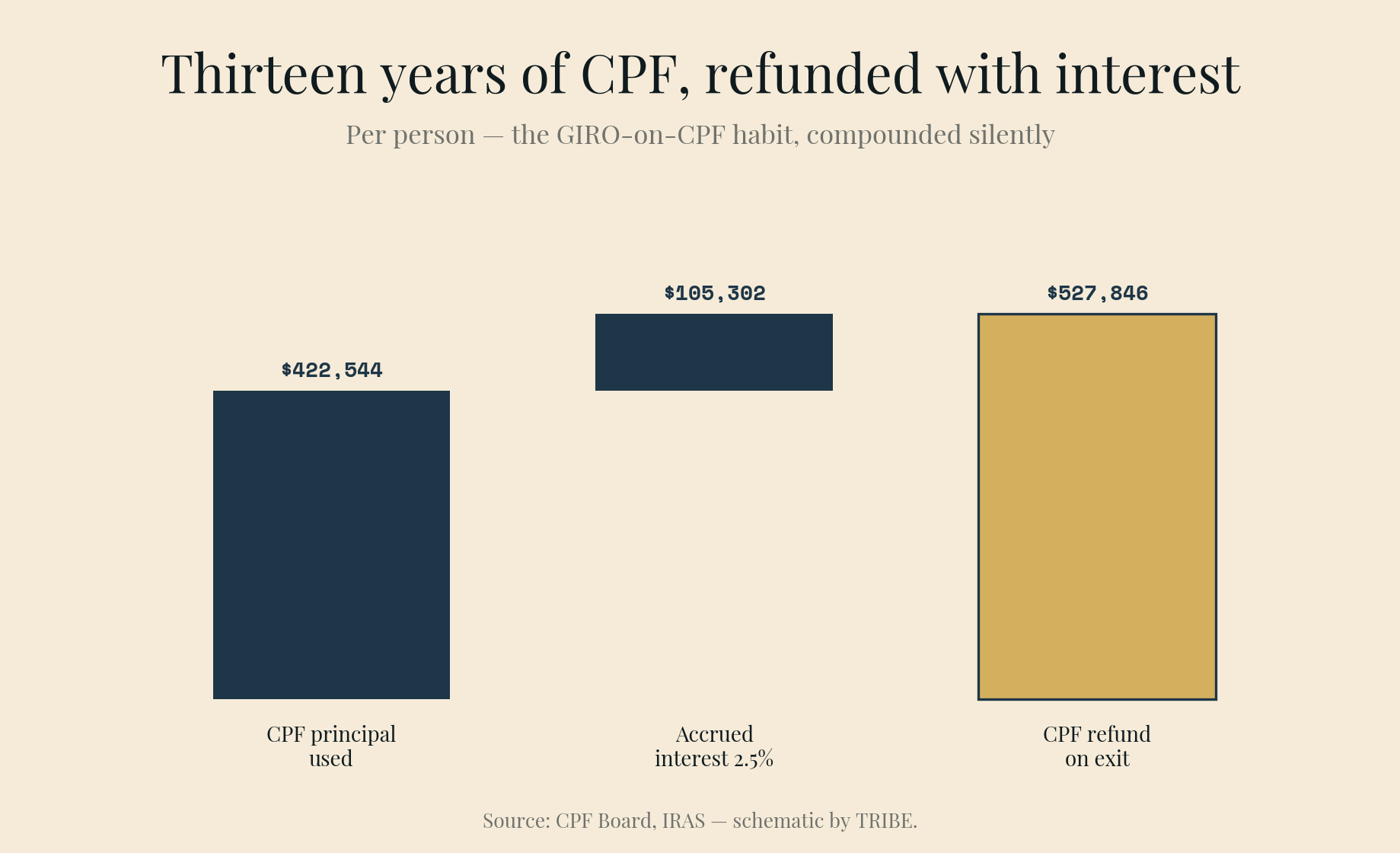

| CPF principal used — each | $422,544 |

| CPF accrued interest — each | $105,302 |

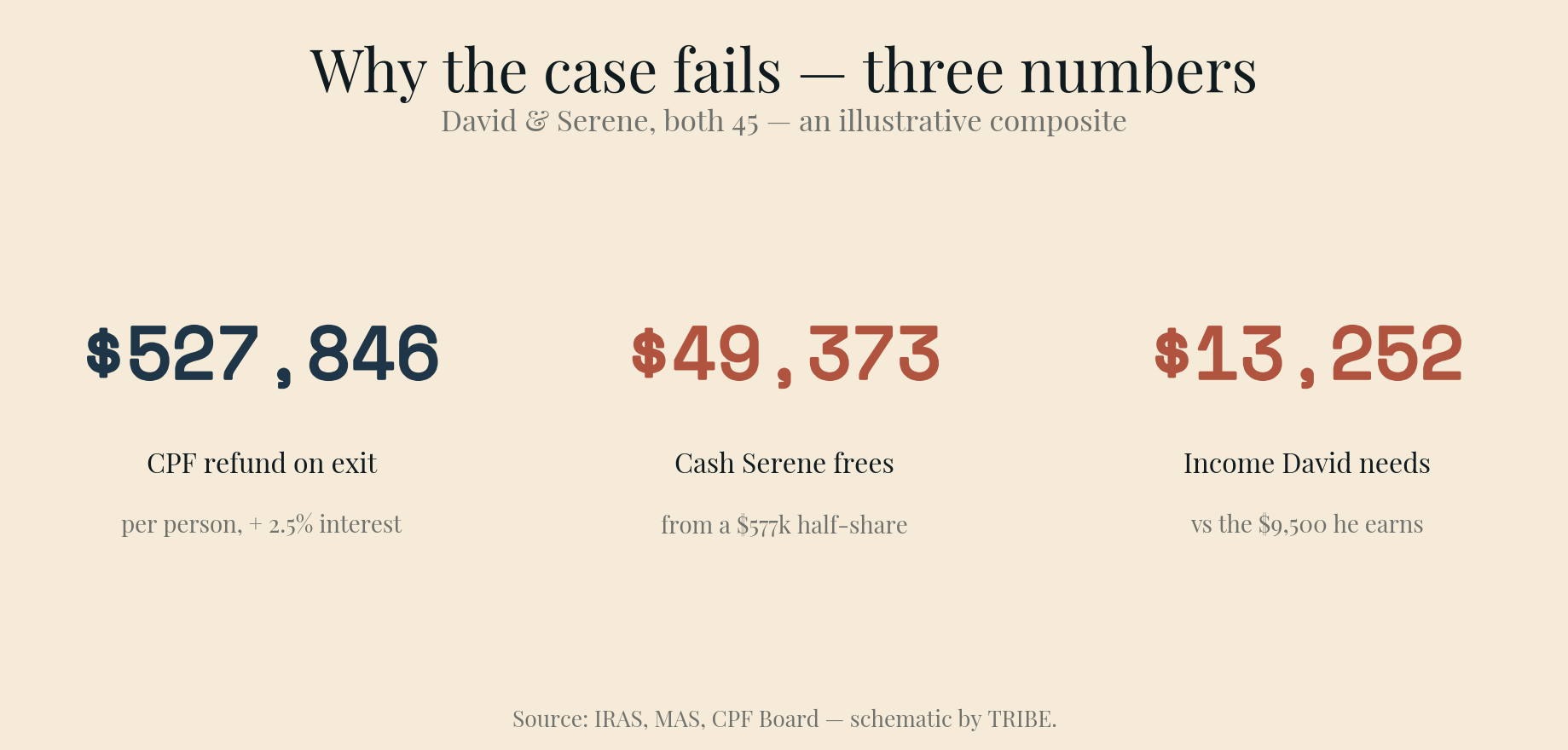

| CPF refund on exit — each | $527,846 |

That last block is the heart of this case. Each of them put $125,000 of CPF into the downpayment, then $1,848 a month — half the instalment — for 161 months. The principal alone is $422,544 per person. But CPF used for housing must be refunded with accrued interest at the OA rate of 2.5% a year, compounding the entire time the money sits in the property. Thirteen years of compounding adds $105,302 per person on top of the principal — roughly five years' worth of instalments, created silently by the GIRO setting nobody revisited.

The entry fee, paid win or lose

Decoupling by part-share sale is a real conveyance, and it's billed like one. David is buying Serene's 50% share — worth $890,000 — so he pays Buyer's Stamp Duty on it at the standard progressive rates (1% to 6%): $21,300. Because the two of them are on opposite sides of the same transaction, conflict-of-interest rules mean two separate law firms, typically $5,000–$7,000 in total, plus a valuation. Call the bill $27,700.

| The decoupling bill | Amount |

|---|---|

| BSD on the $890,000 half-share | $21,300 |

| Legal fees (two firms) | ~$6,000 |

| Valuation | ~$400 |

| Total, payable regardless of outcome | ~$27,700 |

This bill is not the reason decoupling fails — $27,700 against a six-figure ABSD saving is a fine trade. It matters because it is certain and upfront, while the saving sits behind three gates this couple can't pass. Here they are, in transaction order.

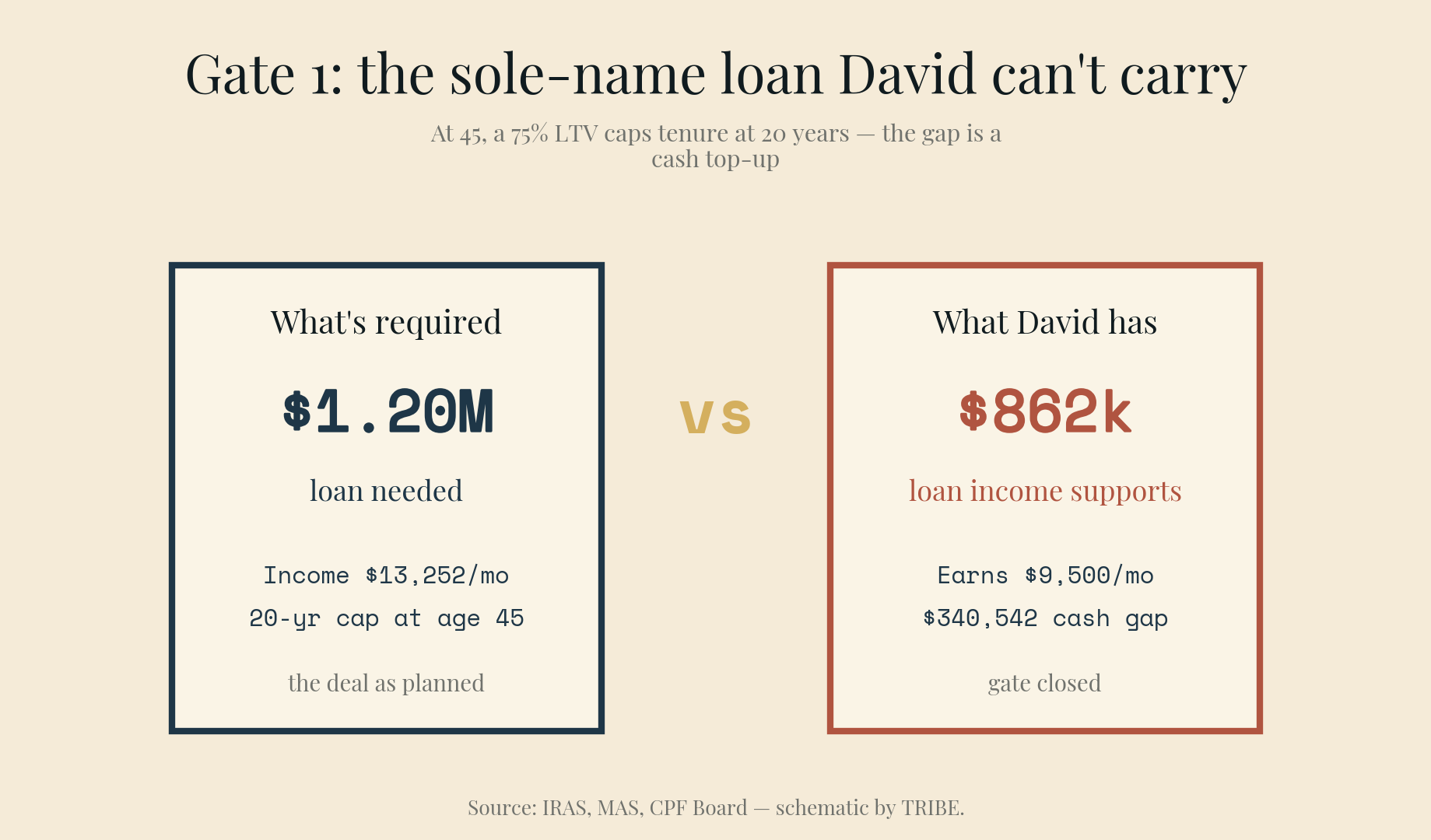

Gate 1: David's sole-name loan

For David to buy Serene out, his new sole-name loan must redeem the joint $625,563 and fund her equity of $577,218 (her $890,000 share minus her half of the loan). That's a loan of about $1,202,800.

At 45, the loan-to-value rules bite: a 75% LTV requires the loan to end by age 65 — a 20-year tenure, no more. Stretch to 25 years and the LTV ceiling drops to 55%, which caps the loan at $979,000 — below what he needs — so the longer tenure is a dead end before TDSR is even tested. On 20 years, stress-tested at the 4% floor with a 55% TDSR and no other debts:

| David's gate | Amount |

|---|---|

| Loan required | $1,202,781 |

| Stress-test repayment (4%, 20 years) | $7,289 / month |

| Gross income required | $13,252 / month |

| David's gross income | $9,500 / month |

| Maximum loan his income supports | $862,239 |

| Cash shortfall to close anyway | $340,542 |

David fails the gate by $3,752 a month of income, which translates into a $340,542 cash top-up to shrink the loan to what he can carry. The couple's actual cash savings are about $120,000. Gate 1 is closed. (For context: even if approved, the real repayment at today's ~1.5% fixed rates would be $5,804 a month — 61% of his gross income on one payslip.)

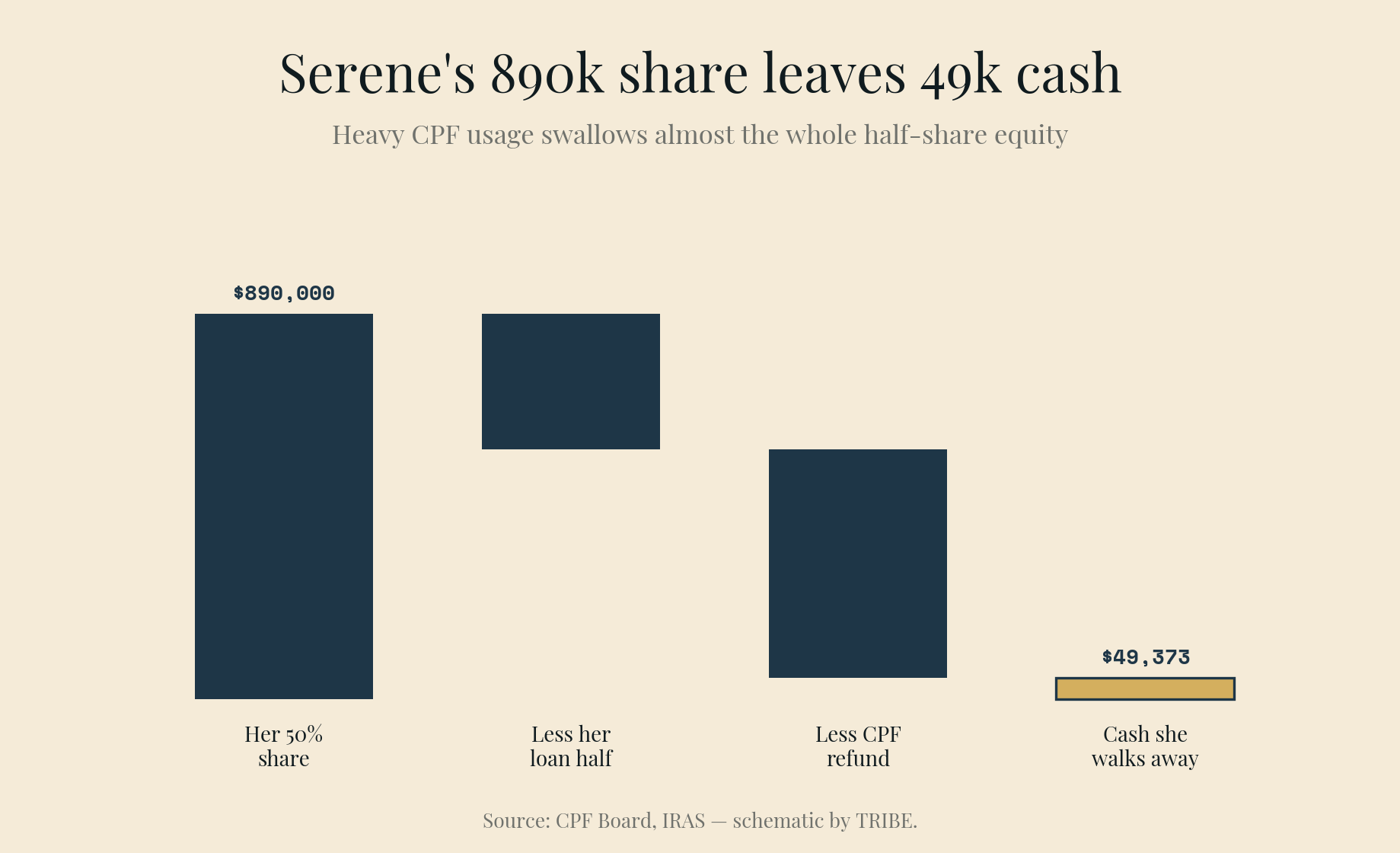

Gate 2: Serene's cash-out

Suppose the loan had cleared. Serene's half-share is worth $890,000. Subtract her half of the outstanding loan ($312,782) and her equity is $577,218 — but $527,846 of it goes straight back into her own CPF before she sees a dollar.

| Serene's exit | Amount |

|---|---|

| Value of her 50% share | $890,000 |

| Less: her half of the loan | −$312,782 |

| Less: CPF refund (principal + accrued interest) | −$527,846 |

| Cash she walks away with | $49,373 |

The $527,846 isn't lost — it lands in her OA, earns 2.5%, and can fund the next downpayment. But it is not cash, and the margin is thinner than it looks: another $50,000 of CPF used per person and the refund would exceed her equity — David would be topping up cash on completion just to unwind his own wife's CPF. Past a point, heavy usage makes the exit itself cost money.

Gate 3: what Serene can actually buy at 45

The plan was a $1.3 million two-bedder. Serene faces the same age math David does: 20-year tenure for 75% LTV, stress-tested at 4%. A $975,000 loan (75% of $1.3M) needs $10,742 a month of income. She earns $8,000.

Her income supports a maximum loan of $726,096, which at 75% LTV caps her purchase at about $968,000. A $950,000 one-bedder clears her TDSR by $150 a month; the ABSD she'd avoid on it — 20% for a Singapore Citizen's second property — is $190,000, not the $260,000 the $1.3M plan implied. And that saving only exists if Gates 1 and 2 are passed first. They aren't — so the realised ABSD saving is zero, and the $27,700 bill (plus a failed loan application) is what's left.

The age-45 cliff, made explicit

Same incomes, same property, ten years younger: a 30-year tenure is available at 75% LTV, and David's $9,500 income would support a $1,094,435 loan instead of $862,239 — 21% more borrowing power from age alone, close enough for a modest cash top-up to bridge. At 45, every year of age is a year off the tenure, and the same payslip carries a visibly smaller loan. Decoupling is, among other things, a young couple's instrument.

What this profile should run instead

The honest alternative isn't a cleverer structure — it's a different transaction. If the goal is genuinely two properties, selling the condo outright resets both of them: the sale discharges the $625,563 loan, refunds $1,055,692 of CPF across both OAs, and frees about $98,700 in cash. Each spouse then buys in a sole name as a first-timer — 0% ABSD on both purchases, no buyout premium inflating either loan. David's income carries a home of up to about $1.15 million; Serene's an investment unit up to about $968,000. The same TDSR limits apply, but there's no $1.2 million sole-name monster in the middle, because nobody is buying out anybody. The costs are two BSDs and a move — and the loss of a condo they like, which is a real cost too.

Or they do nothing, keep paying down a loan at $3,696 a month between two incomes, and accept that the second-property window at their age and CPF position has largely closed. That's not a failure of nerve; it's what the arithmetic says. Run your own version with our stamp duty calculator and sale proceeds calculator — and if your CPF GIRO has been on autopilot for a decade, pull your CPF property withdrawal statement before you talk to anyone. That one number decides more of this than the ABSD table does.

David and Serene are an illustrative composite, not clients; the purchase price, valuation, incomes, CPF history and loan terms are stated assumptions, and the loan balance assumes an average 2% rate since 2013. Computations are exact against June 2026 rules: BSD and ABSD per IRAS, TDSR/LTV per MAS (4% stress floor, 55% TDSR, tenure-linked LTV), CPF refunds with 2.5% accrued interest per CPF Board. General information only, not financial, tax, or legal advice — confirm your own numbers with IRAS, CPF Board, your banker, and a conveyancing lawyer before acting.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.