Insights

Sam Is 35, Single, and Earns $7,500. He's $500 Above Every Line That Was Drawn to Help Him.

At $7,500 a month, a single buyer clears no grant, no HDB loan — and the showflat says condo. We run both paths: the $560k flat the rulebook caps him at, and the $720k condo his cash actually allows.

By TRIBE Editorial · 11 June 2026 · 6 min read

Sam turned 35 this year — the birthday that finally lets a single Singaporean buy a resale flat. He earns $7,500 a month, has $90,000 in cash and $110,000 in CPF after thirteen working years, and one question: HDB or condo?

Sam is a composite of a profile we meet constantly — but every number below is computed against the rules as they stand, and the first thing the computation shows is uncomfortable: at $7,500, Sam is just above every threshold designed to help him.

The $500 problem

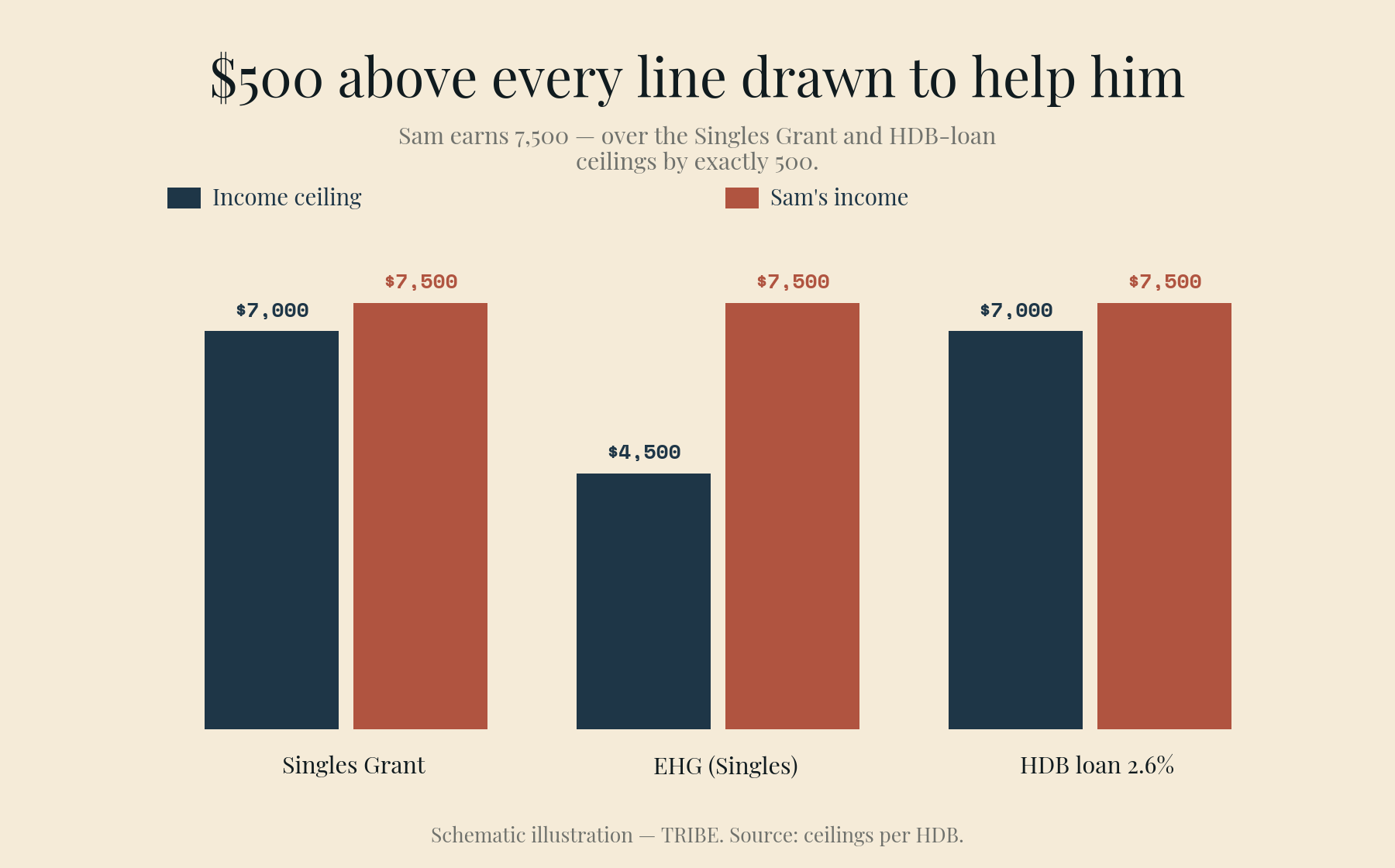

Singapore's housing support for singles is real, but it has edges, and Sam stands $500 past all of them (HDB's singles eligibility page has the full map):

| Support | Income ceiling | Sam at $7,500 |

|---|---|---|

| CPF Singles Grant (up to $40,000) | $7,000 | Misses by $500 |

| Enhanced CPF Housing Grant (Singles) | $4,500 | Misses by $3,000 |

| HDB concessionary loan (2.6%) | $7,000 | Misses by $500 |

| Buying a resale flat at all | No ceiling | Eligible |

So Sam buys at full price, with a bank loan, whichever door he picks. That doesn't decide the question — it just means the two paths get compared honestly, with no subsidy thumb on the scale.

Path one: the four-room flat — and the ceiling he didn't expect

Sam looks at four-room resale flats around $560,000 in the non-mature estates. Because it's an HDB flat financed by a bank, the Mortgage Servicing Ratio applies: housing repayments capped at 30% of gross income, stress-tested at 4%, over a maximum 25-year tenure for full financing.

Run that: 30% of $7,500 is $2,250 a month, which supports a maximum loan of about $426,000 — meaning the most expensive flat Sam can fully finance is about $568,000. The rulebook has, almost to the dollar, priced his ceiling at exactly the flat he's looking at.

| Four-room resale at $560,000 | Amount |

|---|---|

| Downpayment (25%) | $140,000 |

| BSD | $11,400 |

| Upfront total | $151,400 |

| Loan (75%) | $420,000 |

| Monthly at 1.50% fixed, 25 yrs | $1,680 (22% of income) |

| MSR check at 4% stress | $2,217 vs $2,250 cap — passes, barely |

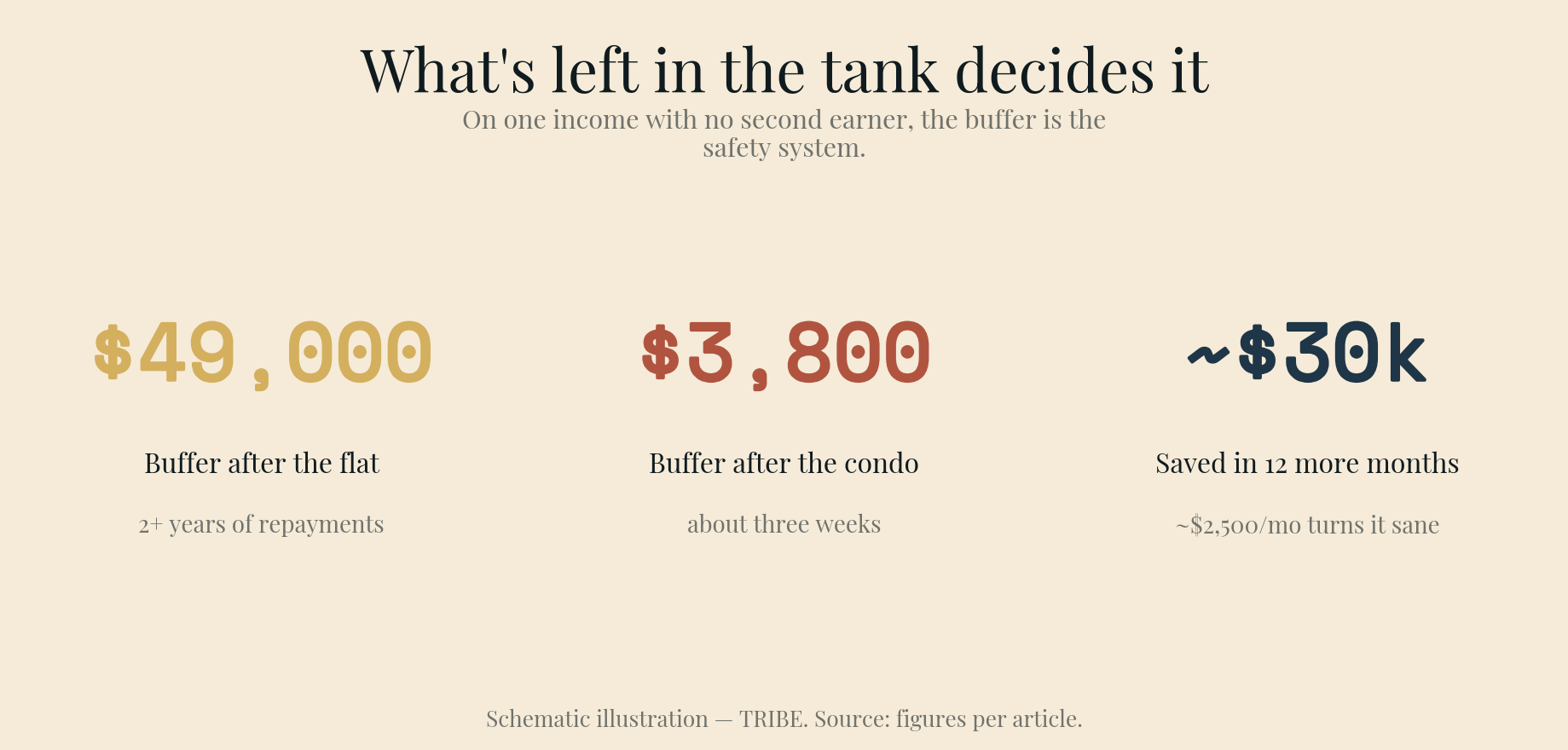

After buying, Sam keeps roughly $49,000 of his $200,000 — a healthy buffer of over two years of repayments.

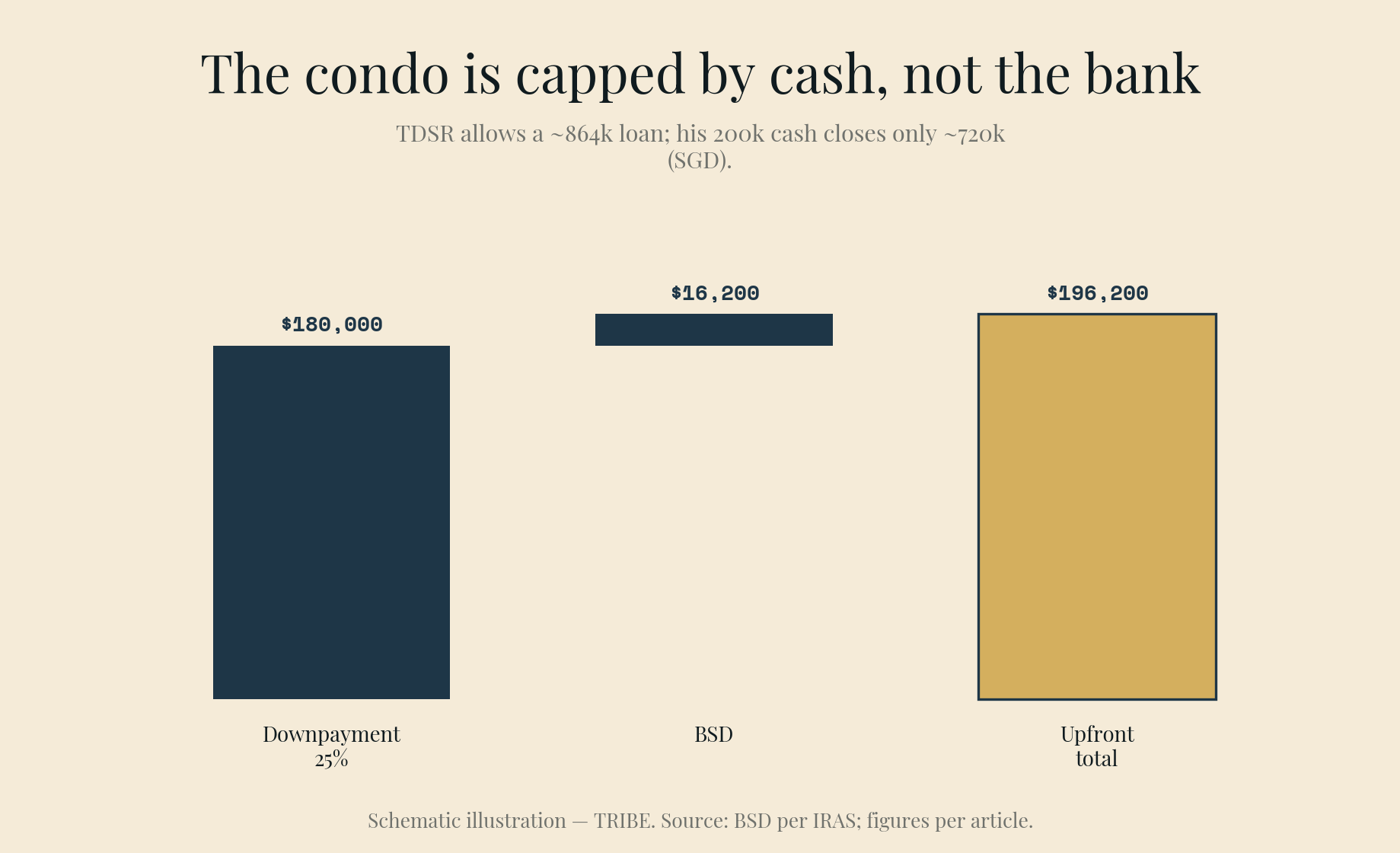

Path two: the condo — capped by cash, not by the bank

Here's where it gets interesting. On the private side, TDSR (55%, stress-tested at 4%) over a 30-year tenure supports a loan of up to about $864,000 — in theory a $1.15M condo. The bank is not Sam's constraint.

His $200,000 is. Working backwards from 25% down plus BSD, the most condo his money can close is about $730,000 — call it $720,000 in practice. In today's OCR resale market that's an older one-bedroom or a compact two-bedder.

| Entry condo at $720,000 | Amount |

|---|---|

| Downpayment (25%) | $180,000 |

| BSD | $16,200 |

| Upfront total | $196,200 |

| Loan (75%) | $540,000 |

| Monthly at 1.40% fixed, 30 yrs | $1,838 (25% of income) |

| TDSR check at 4% stress | $2,578 vs $4,125 cap — comfortable |

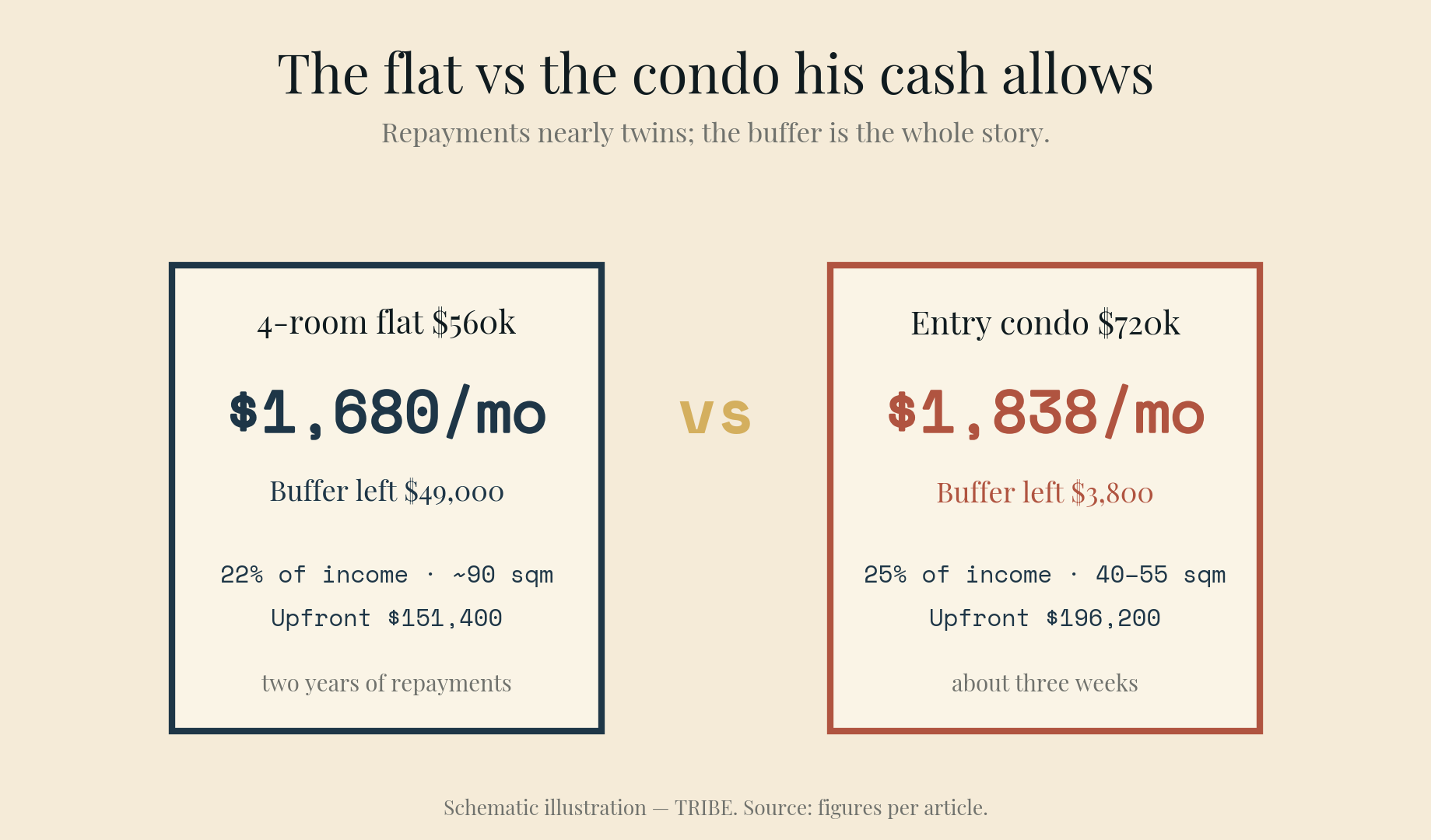

Leftover after buying: about $3,800. Read that against the flat's $49,000 and you have the real shape of the choice.

The honest comparison

The monthly repayments are nearly twins — $1,680 against $1,838, at today's rates. What differs is everything around them.

Space. The flat is roughly 90 square metres; the $720k condo is 40–55. Same money, half the home.

Buffer. The flat leaves Sam two years of repayments in reserve. The condo leaves him three weeks. On one income with no second earner to catch a fall, that buffer isn't a nicety — it's the whole safety system. Buying the condo responsibly means another year of saving first, or a smaller target.

The asset. The condo is the more flexible asset: rentable immediately (a flat can only be rented whole after its five-year MOP), no resale restrictions on who can buy it, and historically the path that keeps a second move open — sell, upgrade, or keep as an investment when Sam's income grows. The flat is the better home per dollar but a more regulated asset.

The exit. This is the part most singles underweight at 35 and care about most at 45. A four-room flat's buyer pool is deep and steady. A compact one-bedder's buyer pool is investors and other singles — narrower, more sentiment-driven. If Sam goes private, which $700k condo he buys matters enormously — at this quantum the spread between an A-grade and a C-grade project on RPS is the difference between an asset and a regret. Liquidity, MRT, and rental yield carry most of the score at this price point.

What we'd actually tell Sam

If the goal is the best home for the money and sleep at night: the flat, without apology. $1,680 a month at 22% of income with $49,000 in reserve is a position of strength, and nothing stops Sam buying private later from it — many do, post-MOP, with equity behind them.

If the goal is the asset and the optionality, the condo is legitimate — but the math says not yet. At $3,800 of buffer it's a coin-flip on nothing going wrong for a year. Twelve more months of saving at his rate (~$2,500/month puts $30k away) turns the same purchase into a sane one.

What Sam shouldn't do is let the $500 sting — the grants he just misses — push him into "might as well go private then." That's a feeling, not a number. The numbers are above, and they're calm.

Run your own version: stamp duty, sale proceeds if you're selling something first, and RPS for any condo on your shortlist.

Sam is an illustrative composite, not a client; his figures are stated assumptions. Computations are exact against June 2026 rules — MSR/TDSR per MAS, BSD per IRAS tiers, grant and loan ceilings per HDB's published criteria, rates from the linked source. General information only, not financial advice; verify current rules with HDB, MAS, and your bank.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.