Insights

New PRs, First Purchase: The $75,000 Question — Keep Renting or Buy Now?

A newly minted PR couple pays 5% ABSD on their first home — $75,000 on a $1.5M condo. We run the rent-vs-buy breakeven under four price scenarios, plus the math on waiting for citizenship.

By TRIBE Editorial · 12 June 2026 · 8 min read

Hao and Yann are both 32. They received Singapore permanent residency in February, earn a combined $16,000 a month, and pay $4,200 for the two-bedroom condo they rent in Sengkang. Their landlord wants to renew at the same rent. Their question is the one every new PR couple eventually asks: keep renting, or buy — knowing that the moment they sign, the state collects an extra 5% of the purchase price purely because their passports aren't pink yet.

Hao and Yann are an illustrative composite of a household we meet constantly, and their figures are stated assumptions. Every number below is computed, not estimated — and the answer turns out to hinge on a single variable neither of them controls.

The entry tax, itemised

Under IRAS's current ABSD schedule — unchanged since April 2023 — a Singapore PR buying a first residential property pays 5% ABSD. (A second property as a PR costs 30%, which matters later.) On top of that sits ordinary Buyer's Stamp Duty, tiered at 1% to 6%. Note that two PRs married to each other get no spousal remission — that route exists only where at least one spouse is a citizen.

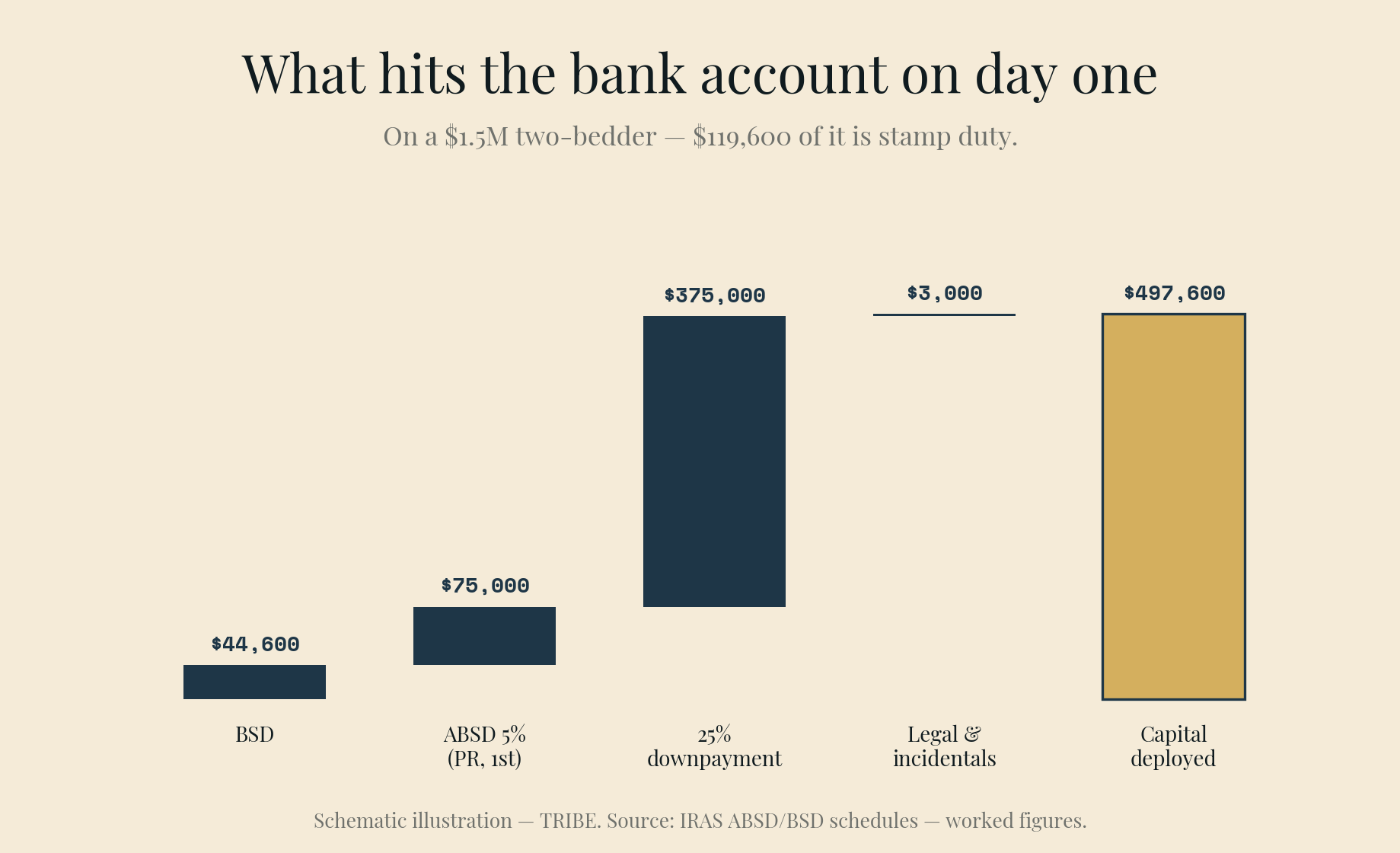

On the $1.5 million two-bedder they're eyeing:

| At signing | Amount |

|---|---|

| BSD (1–4% tiers up to $1.5M) | $44,600 |

| ABSD at 5% (PR, first property) | $75,000 |

| Total stamp duties | $119,600 |

| Downpayment (25%) | $375,000 |

| Legal and incidentals (assumed) | $3,000 |

| Capital deployed on day one | $497,600 |

That $119,600 of tax equals 28.5 months of their current rent. As new PRs their CPF Ordinary Accounts are nearly empty — only a few months of contributions — so effectively all of it is cash. We assume they have it; if they don't, this article is moot and the answer is rent.

Can they carry the loan? At current fixed rates around 1.50%, a $1,125,000 loan over 30 years costs $3,883 a month. The TDSR stress test at 4% prices the same loan at $5,371 against their $8,800 cap (55% of $16,000) — they pass with room to spare. Affordability isn't the question. The $119,600 is.

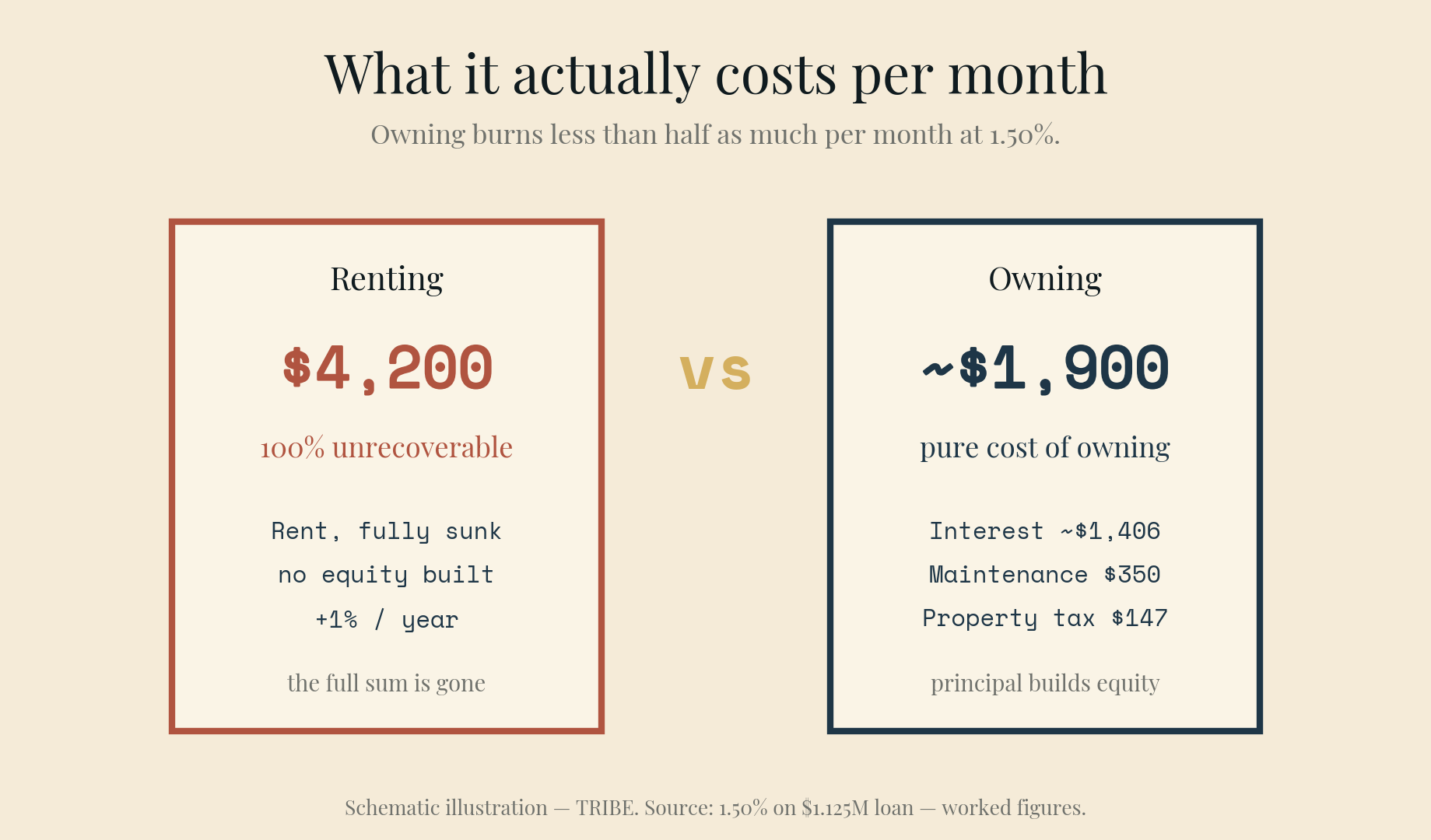

What owning actually costs per month

Here is the part the showflat never itemises. The mortgage payment is not the cost of owning — most of it is principal, which is just money moving from their bank account into their own home equity. The unrecoverable monthly cost of owning is interest, maintenance, and property tax:

| Owning, month one | Amount |

|---|---|

| Interest portion (~1.50% on $1.125M) | ~$1,406 |

| Condo maintenance fee (assumed) | $350 |

| Owner-occupier property tax (AV $50,400) | $147 |

| Pure cost of owning | ~$1,900 |

Against $4,200 of rent — which is 100% unrecoverable — owning burns less than half as much per month at today's rates. That is the entire engine of the buy case. The stamp duty is the entire counterweight: a $119,600 toll gate in front of a ~$2,300-a-month saving.

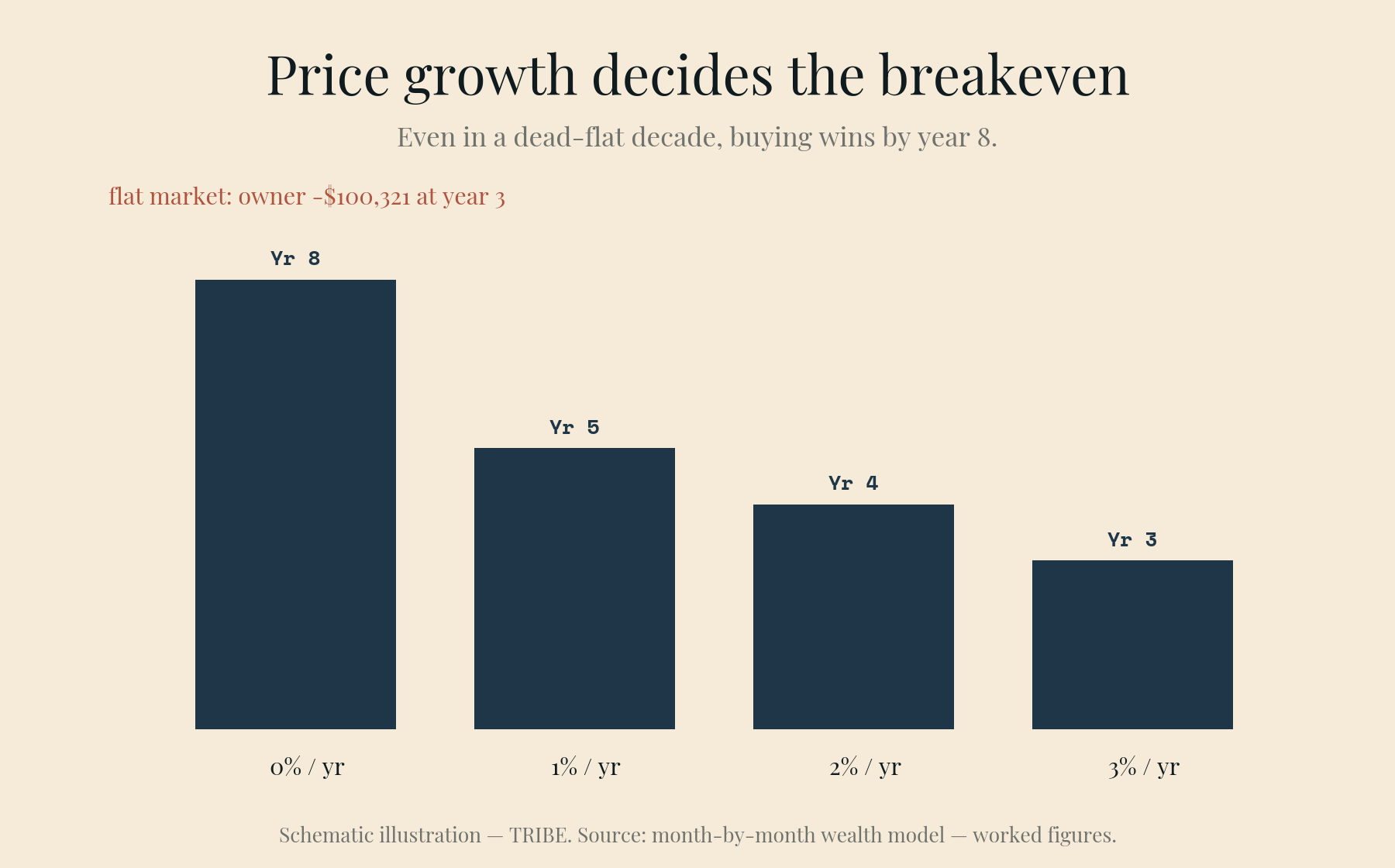

The breakeven, computed

We modelled both paths month by month. Buy: $1.5M purchase, 75% loan at 1.50% fixed over 30 years, $350 maintenance, owner-occupier tax, and a 2% agent commission plus $3,000 legal on eventual exit. Rent: keep the $497,600 invested at a safe 2.0% (roughly T-bill territory now that 3M-SORA sits near 1.1%), pay rent escalating 1% a year, and invest any monthly difference at the same 2.0%. The breakeven is the year the owner's net wealth — property equity after selling costs — overtakes the renter's.

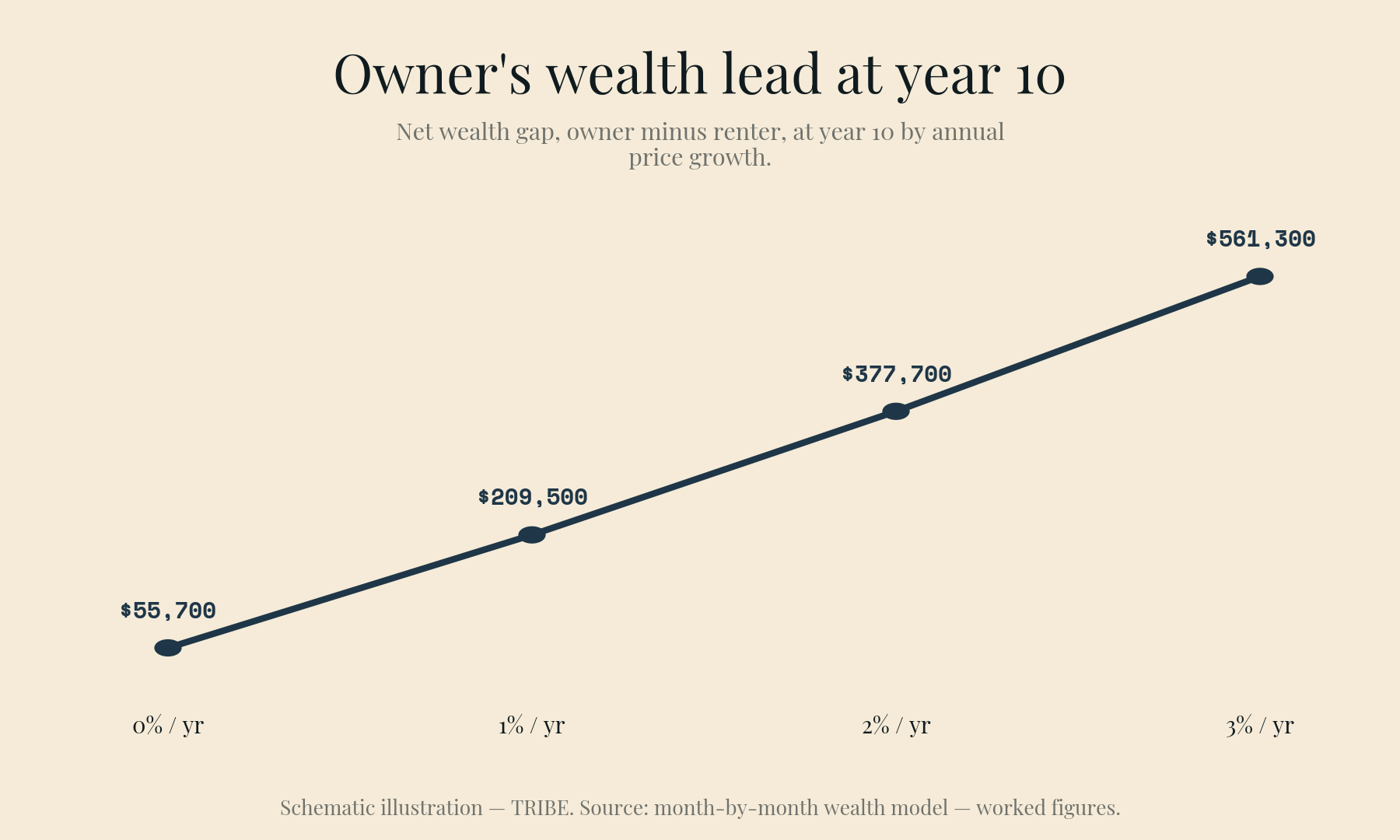

The one variable that dominates everything is price growth:

| Price growth | Owner pulls ahead | Gap at year 5 | Gap at year 10 |

|---|---|---|---|

| 0% a year | Year 8 | −$59,800 | +$55,700 |

| 1% a year | Year 5 | +$15,200 | +$209,500 |

| 2% a year | Year 4 | +$93,200 | +$377,700 |

| 3% a year | Year 3 | +$174,400 | +$561,300 |

Read the first row carefully: even if prices go nowhere for a decade, buying still wins by year 8 — because at 1.5% interest, the rent saved outruns the stamp duty eventually. What the duty really buys the renter is time: in a flat market, the owner is $100,321 behind at year 3. Sell early and the loss is real and large — the sale price needed just to exit whole, covering both duties, commission and legal, is $1,658,776, or 10.6% above purchase.

For calibration, not prediction: URA's Q1 2026 statistics showed overall private prices up 0.9% in a single quarter, with OCR non-landed up 2.2%, while the rental index rose just 0.4%. Recent history sits well above the 2% row. A flat or falling stretch — 2014–2017 was one — sits at or below the first.

The citizenship wrinkle

Hao and Yann intend to apply for citizenship, and citizens pay 0% ABSD on a first home. So why not rent three more years and save the $75,000?

Because waiting has a price too: three years of rent ($152,717 at their escalating $4,200), versus only $48,647 of interest plus $17,880 of maintenance and tax had they owned — and the house may not wait at their price. We ran the full version: rent three years, then buy the same unit at its grown price with 0% ABSD, compare net wealth at year ten. The waiting strategy wins only if prices grow slower than about 0.5% a year. At 2% growth, buying now ends roughly $82,000 ahead despite paying the $75,000 duty — the price runs away faster than the tax savings accrue. The naive version of the same sum — $75,000 saved versus price growth alone — breaks even at 1.56% a year; the full cashflow model is harsher on waiting because renting bleeds more per month than owning does.

And that's assuming citizenship arrives on schedule. It is discretionary and not guaranteed; if they're still PRs in year three, the wait bought nothing — buying now beats waiting by about $60,000 even in a flat market.

The honest caveats

The 1.50% rate is a window, not a promise. Fixed packages reset in two to three years. Our model holds the rate constant; reprice it at 2.5% and the owner's monthly interest burn rises by roughly $900, pushing every breakeven out by a year or so. The direction of the conclusion survives; the margin thins.

Appreciation scenarios are scenarios. The 2% row is not a forecast. Anyone who promises you the third row is selling something.

The 30% second-property ABSD locks the choice. As PRs, upgrading later means selling first or paying 30%. This purchase should be a 7–10 year home, not a stepping stone — which is exactly the holding period the breakeven table demands anyway.

Liquidity and flexibility have value the model can't price. A renter can leave Singapore in 60 days. A new PR couple unsure whether Singapore is permanent should weight that heavily — the table shows the cost of early exit precisely.

The bottom line

The 5% ABSD is real money — 28 months of rent, paid at the door. But at today's borrowing costs it is a toll, not a wall: under any price-growth assumption of 1% or better, buying overtakes renting within five years, and even in a dead-flat decade the owner wins by year 8. The cases for continuing to rent are specific and legitimate: a holding horizon under five years, doubt about staying in Singapore, or a war chest that the $497,600 outlay would exhaust. Otherwise, for a couple like Hao and Yann, the math says the question isn't really rent or buy — it's whether they're sure enough about the next eight years to pay the toll once.

Run your own numbers: our stamp duty calculator prices the entry for your profile and price point, and if the shortlist is resale condos, score them on RPS before committing.

Hao and Yann are an illustrative composite, not clients; their income, rent, savings and target price are stated assumptions. Computations are exact against June 2026 rules: ABSD and BSD per IRAS schedules in force since April 2023 and February 2023 respectively, TDSR per MAS, owner-occupier property tax per IRAS 2025 bands, mortgage rates from the linked source. Breakeven figures follow the stated model and assumptions; actual outcomes depend on rates, rents and prices realised. General information only, not financial advice.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.