Insights

After the Divorce, Mei Can Keep the Flat — She Passes the Bank's Test by Twenty-One Dollars. Should She?

A divorced parent, 41, one income of $8,000, two kids, and a four-room flat the court says she can take over. The buyout math works — barely. We run keeping it against selling and resetting, number by number.

By TRIBE Editorial · 12 June 2026 · 7 min read

Mei is 41. The divorce was finalised three months ago. She has care and control of the kids — ten and seven — a gross income of $8,000 a month, and a court order that splits the matrimonial flat's net equity 50/50, with an option for her to take over the flat. The Punggol four-room is worth $620,000 and is past its five-year MOP, so retaining it is permitted — if she can finance it. That's the whole question: can she keep it, and separately, should she?

Mei is an illustrative composite of a household we meet often, and her figures are stated assumptions. The computations below are exact against the rules as they stand in June 2026, and the first one comes out almost unbelievably close.

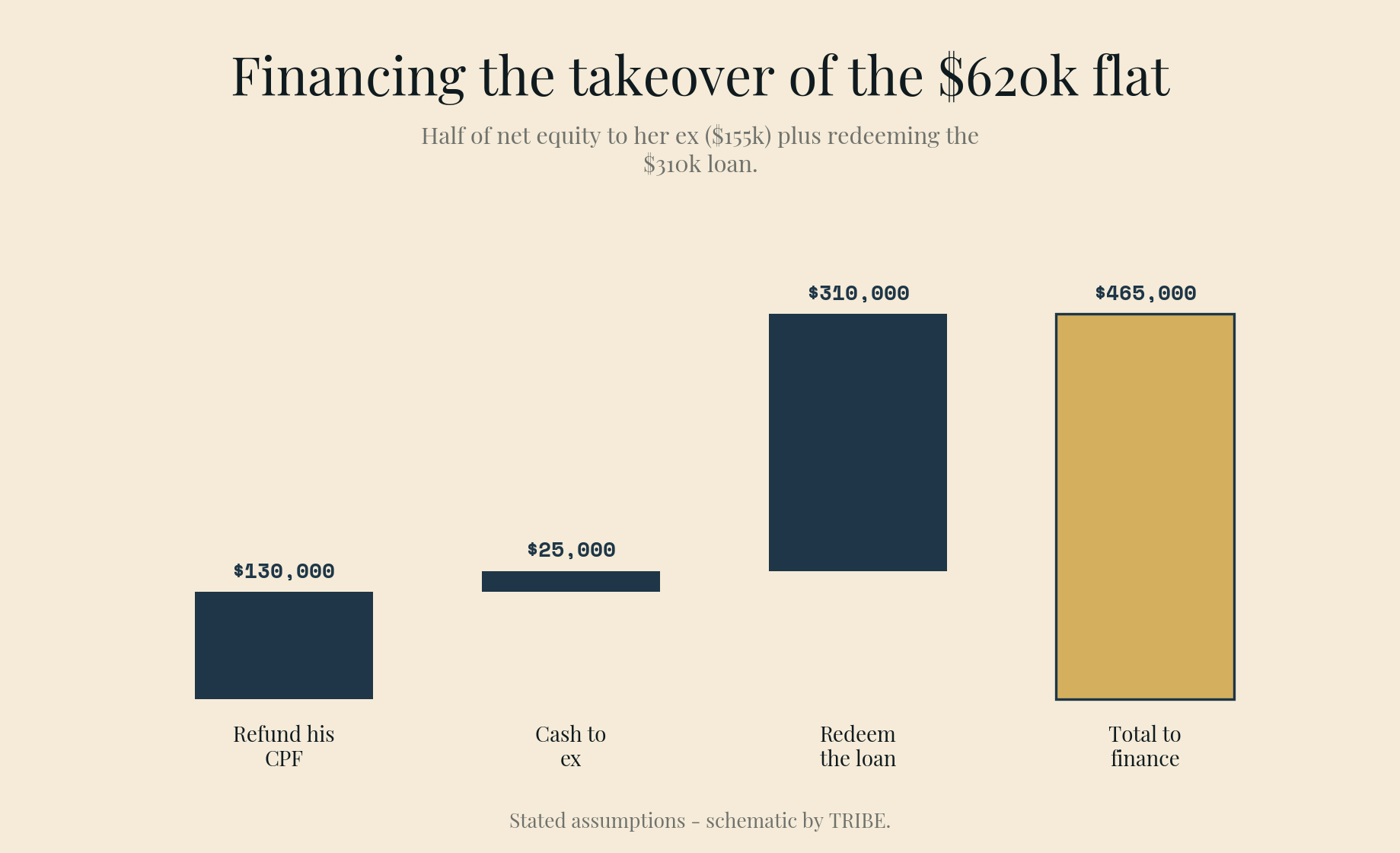

The buyout, priced

The flat is worth $620,000 with $310,000 outstanding on a bank loan. Net equity: $310,000. The court order gives her ex half.

| Taking over the flat | Amount |

|---|---|

| Pay ex-spouse: 50% of net equity | $155,000 |

| — of which, refund to his CPF (used + accrued interest) | $130,000 |

| — of which, cash to him | $25,000 |

| Redeem/refinance the outstanding loan | $310,000 |

| Total to finance | $465,000 |

Two pieces of rare good news first. One: a transfer pursuant to a divorce court order is remitted from stamp duty — no BSD on the share she's acquiring. Two: $465,000 is exactly 75% of the flat's value, so the loan-to-value ceiling isn't her constraint.

The Mortgage Servicing Ratio is.

Twenty-one dollars

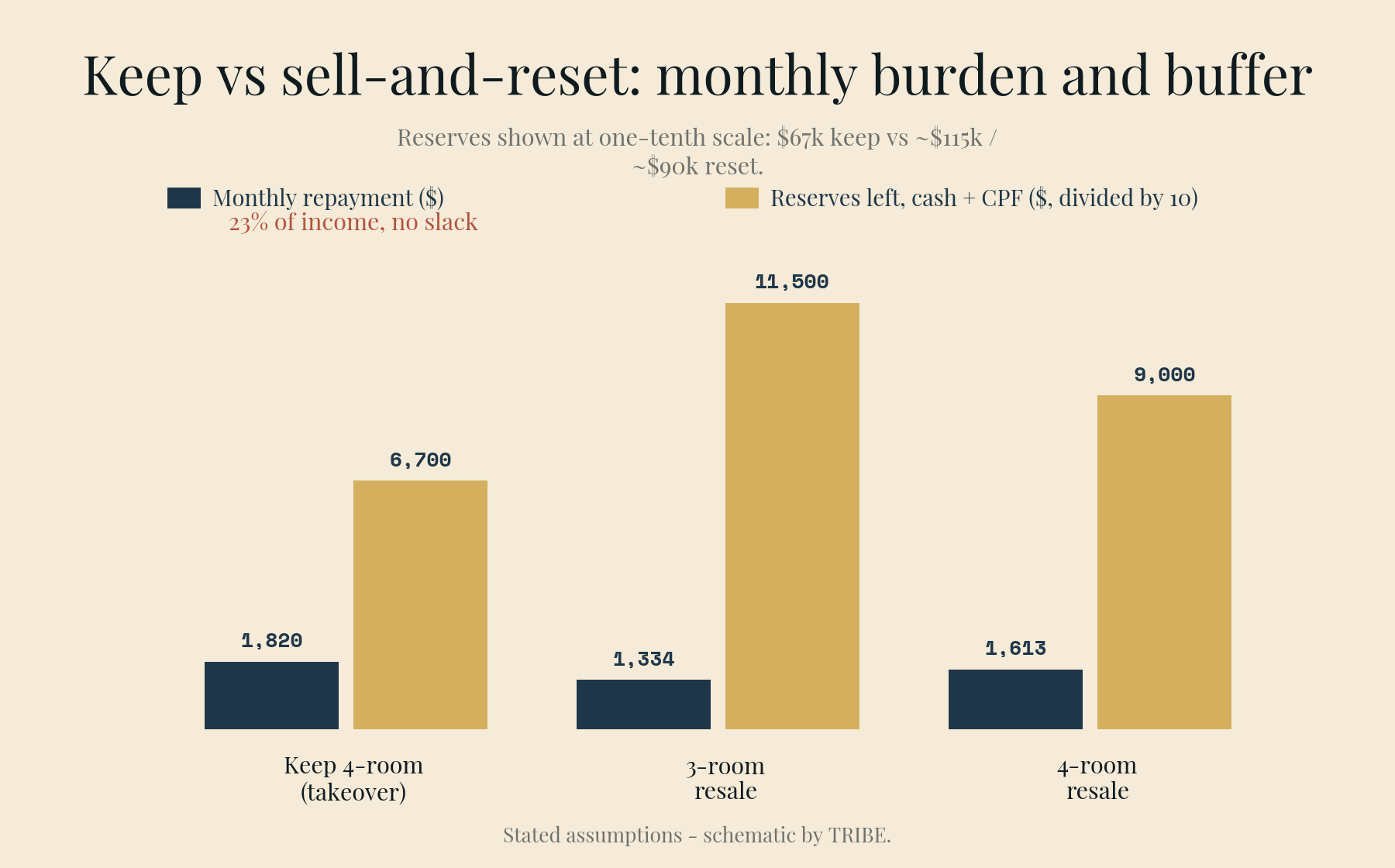

An HDB flat on a bank loan is governed by MSR: housing repayments capped at 30% of gross income, stress-tested at 4%. On $8,000, that's a $2,400 ceiling. At 41, a loan that ends by 65 — the condition for full 75% financing — runs 24 years at most.

The maximum loan those parameters support is about $443,800. She needs $465,000. So the bank won't finance the whole takeover — she takes a $440,000 loan and closes the gap herself:

| The refinancing | Amount |

|---|---|

| New loan in her name (24 years) | $440,000 |

| From her own funds (cash + OA) | $25,000 |

| Monthly repayment at 1.50% fixed | $1,820 (23% of income) |

| MSR stress test at 4% | $2,379 vs $2,400 cap — passes by $21 |

Twenty-one dollars. If her income were $7,930 instead of $8,000, this entire path would be off the table. She passes — the flat is keepable. Whether it's wise is where the second half of her ledger comes in.

She has $55,000 in cash and $40,000 in her Ordinary Account (her own $90,000 of CPF is in the flat and stays there if she keeps it). After the $25,000 gap and roughly $3,000 of legal and refinancing costs, she holds about $67,000 — three years of repayments, but on one income, with two children, and a repayment that already consumed every dollar of MSR headroom. There is no room to refinance upward later if anything changes. The flat also keeps the kids in their schools, on their bus routes, in the only home they've known through a hard year — which is not a number, but it isn't nothing either.

The other path: sell and reset

Now the same ledger if the flat is sold at $620,000 and the order's 50/50 split applies to net proceeds.

| The sale | Amount |

|---|---|

| Sale price | $620,000 |

| Less: outstanding loan | −$310,000 |

| Less: CPF refunds (his $130,000 + hers $90,000) | −$220,000 |

| Cash pool | $90,000 |

| Her half | $45,000 |

Her war chest after the sale: $45,000 + her $55,000 savings = $100,000 cash, plus $90,000 refunded CPF + $40,000 existing OA = $130,000 CPF. As a divorcee with care and control of her children, she forms her own family nucleus and can buy a resale flat immediately; having used her grants on the matrimonial flat, we assume no further grant support — the comparison stays unsubsidised on both sides.

Two realistic landings, both on a 24-year bank loan at today's 1.50% fixed rates:

| 3-room resale, $430,000 | 4-room resale, $520,000 | |

|---|---|---|

| Downpayment (25%) | $107,500 | $130,000 |

| BSD | $7,500 | $10,200 |

| Upfront total | $115,000 | $140,200 |

| Loan (75%) | $322,500 | $390,000 |

| Monthly repayment | $1,334 (17%) | $1,613 (20%) |

| MSR stress test at 4% | $1,744 — clears by $656 | $2,109 — clears by $291 |

| Left over (cash + CPF) | ~$115,000 | ~$90,000 |

The upfront is paid from CPF first, so most of what survives is cash. Either way she carries a repayment several hundred dollars lighter than the takeover, with an actual buffer behind it — and the 4-room option keeps the kids in their own rooms.

The honest comparison

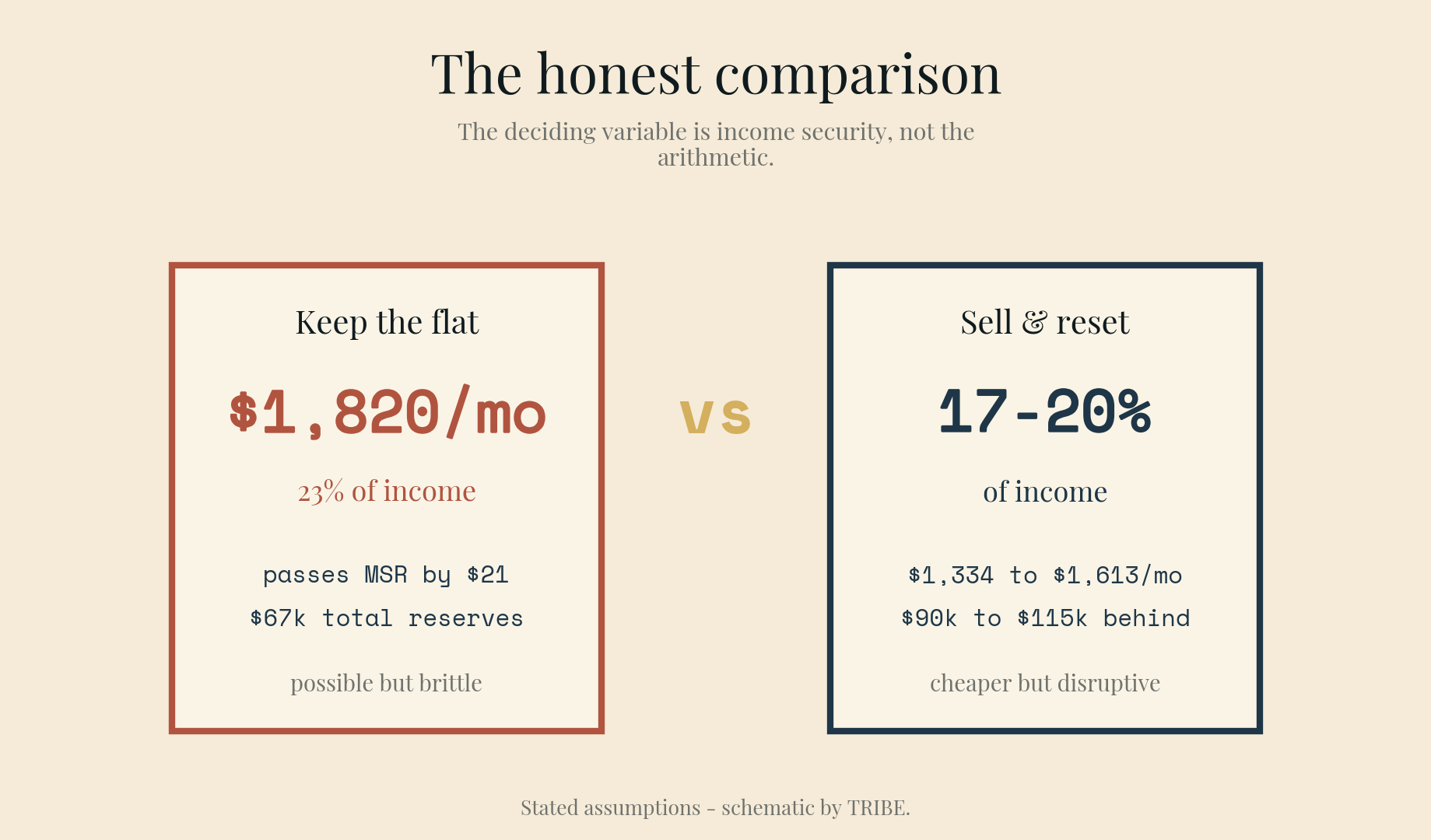

Keeping the flat costs $1,820 a month at the absolute edge of what regulation permits, leaves $67,000 of total reserves, and preserves continuity — schools, friends, routine — at the exact moment continuity is worth the most. It is a defensible choice. It is also a position with zero slack: one retrenchment, one medical year, one rate reset above the fixed period, and the math that passed by twenty-one dollars fails by hundreds.

Selling and resetting crystallises the split cleanly, returns her CPF to her own name, and lands her in a home she controls outright on numbers that breathe — 17–20% of income, with $90,000–$115,000 behind her. The cost is the move itself, borne by children who have already absorbed one upheaval.

The showflat version of this article would tell Mei the bank approved her, so keep it. The bank-statement version says something more careful: the takeover is possible but brittle, and the reset is cheaper but disruptive. In our experience the deciding variable is income security — a Mei in a stable civil-service or healthcare role can defend the $21 margin; a Mei on commission or in a volatile industry cannot. The arithmetic is the same; the resilience isn't.

One more thing worth saying plainly: none of this math has to be done in week one. The flat is past MOP; the court order sets the split, not the calendar (within whatever deadline the order itself specifies). A decision this close deserves a settled month and a real spreadsheet, not a lawyer's-office estimate.

Run your own version

The shape generalises: value the flat, subtract the loan, subtract both CPF ledgers, split per your order, then test the keep-path against MSR at your income and the reset-path against your actual war chest. Our sale proceeds calculator handles the middle rows; the stamp duty calculator prices the re-entry; and if the reset path points private instead of HDB, score the shortlist on RPS before committing a single-income household to it.

Mei is an illustrative composite, not a client; her flat value, loan balance, CPF figures and court-order terms are stated assumptions — actual divorce settlements vary and are set by the court, not by formula. Computations are exact against June 2026 rules: MSR per MAS, stamp duty remission per IRAS's matrimonial proceedings rules, retention eligibility per HDB/MSF guidance, rates from the linked source. General information only, not legal or financial advice; divorce-related housing decisions should be taken with your lawyer, HDB, and your bank.

Check how your condo scores

2,357 condos independently scored across 7 weighted factors. No registration required.

Score my resale →Prefer a personal read on your situation? Arrange a consultation →Keep reading

TRIBE Editorial · Reviewed by Silas Tan

Co-Founder, TRIBE · District Director, Huttons Asia · Ex-Mortgage Banker (AVP) · >1,000 families advised · CEA R000303I

This article is for informational purposes only and does not constitute financial or investment advice.